Reports

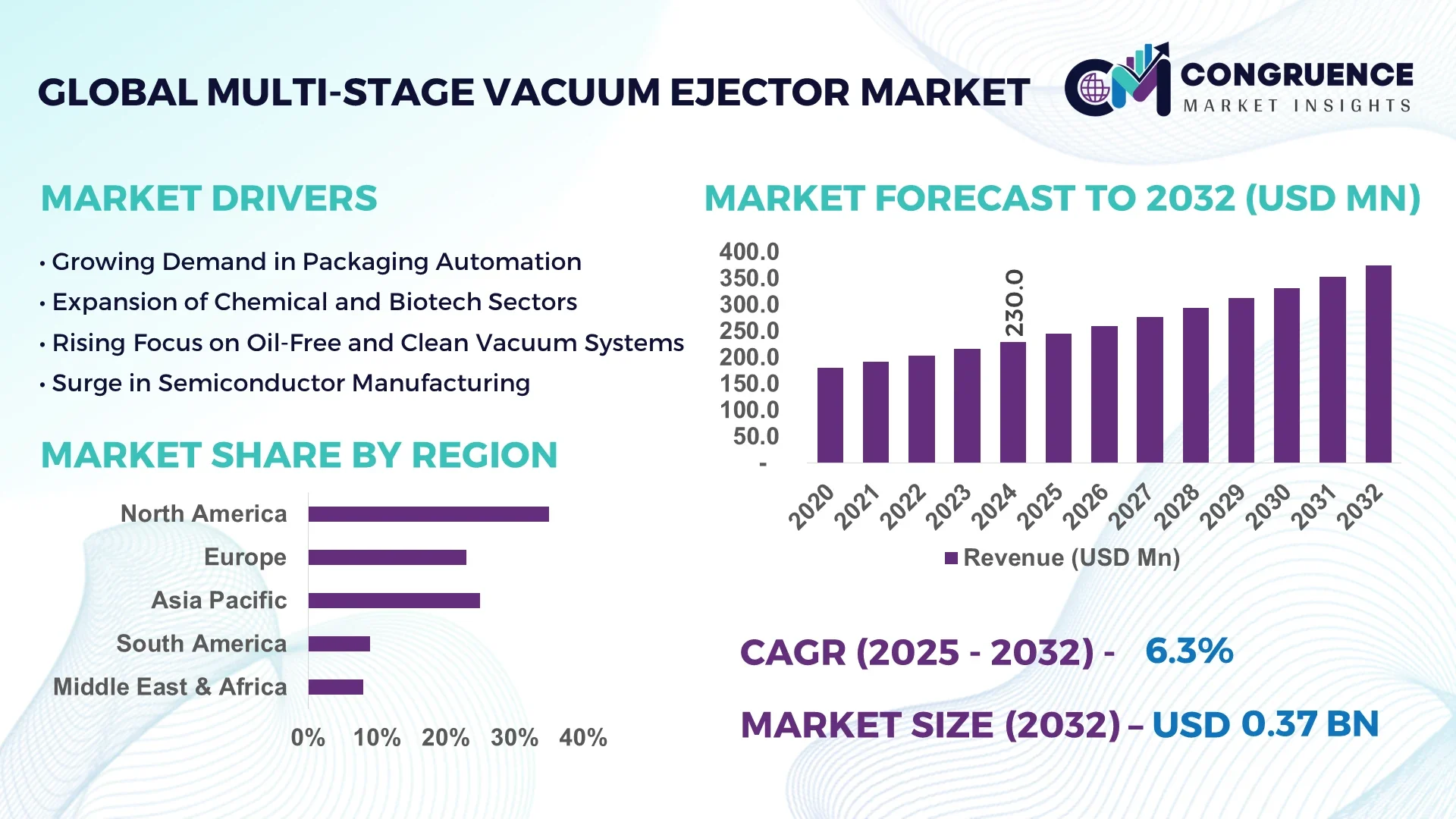

The Global Multi-Stage Vacuum Ejector Market was valued at USD 230.0 Million in 2024 and is anticipated to reach a value of USD 374.1 Million by 2032 expanding at a CAGR of 6.3% between 2025 and 2032.

Asia‑Pacific, led by China, dominates the marketplace, accounting for over one-third of global sales. China’s vast manufacturing sector and extensive automation efforts in industries like electronics, chemicals, and pharmaceuticals have fueled high demand for multi-stage vacuum ejectors. These systems are increasingly integrated into production lines for tasks such as packaging, material handling, and drying.

Additionally, the market is witnessing growing adoption of customized ejector solutions tailored to specific industrial needs. Manufacturers are enhancing nozzle configurations and stage arrangements to optimize suction performance, reduce energy use, and meet diverse process requirements across food & beverage, medical device sterilization, and semiconductor fabrication sectors.

AI technologies are revolutionizing the multi-stage vacuum ejector market by enabling smarter, more efficient systems and predictive maintenance solutions. Modern ejector units are being equipped with edge-computing sensors that continuously monitor parameters such as suction pressure, fluid temperature, flow rate, and nozzle wear. These sensors feed data into AI-driven analytics platforms that detect early signs of inefficiency or degradation—such as subtle drops in vacuum strength or increases in energy consumption—long before they lead to unplanned downtime.

Fact-based adoption is rising: over 40% of advanced ejector system installations in North America now feature AI-powered diagnostic modules that deliver real-time alerts and performance optimization recommendations. In Europe, several manufacturers have reported field trials where AI tuning algorithms improved suction efficiency by 12–15% during peak-load operations.

Moreover, AI-enhanced ejectors integrated into Industry 4.0 networks allow remote control centers to dynamically adjust multi-stage sequencing based on production demands. For example, chemical plants utilizing these systems have achieved 18% faster batch-changeover times by enabling AI-driven nozzle-stage reconfiguration mid-cycle.

Another notable transformation is the emergence of autonomous maintenance robots used in large ejector arrays. These mobile robots—guided by AI—perform routine inspections, nozzle cleaning, and minor repairs, reducing manual labor and improving uptime. Manufacturers report that each autonomous unit can service up to 1,000 ejectors per month, freeing engineers to focus on more complex tasks.

AI-enabled diagnostic platform in ejector systems now identifies microscopic nozzle blockages with over 95% accuracy, prompting automated flushing routines without human intervention.

"In 2024, recent development confirmed by multiple industry integration reports shows ejector sensors detecting minute obstructions (<0.2 mm debris) and triggering flush cycles within seconds—ensuring consistent vacuum performance and lowering maintenance interventions by nearly 60%."

The expanding healthcare sector’s emphasis on sterile packaging and medical-device decontamination is a key growth driver. Multi-stage vacuum ejectors are essential for processes like freeze-drying pharmaceuticals, sterilizing surgical tools, and vacuum-sealing biohazard specimens. In 2024 alone, over 200 sterilization facilities globally added ejector systems to meet higher throughput demands. Vendors have responded with ejector models optimized for rapid cycle-change and high purity standards in cleanroom environments.

Despite long-term savings, the initial expenditure for AI-enabled multi-stage ejector systems—ranging from USD 50,000 to USD 150,000 per unit—can deter smaller manufacturers. Additionally, retrofitting existing production lines often requires shutdowns, specialized piping modifications, and compliance verification. In 2024, nearly 30% of mid-tier SMEs in Asia postponed upgrades due to these financial and operational barriers, opting instead to extend the lifespan of older single-stage ejector equipment.

The semiconductor industry’s boom in 2024–2025 has surged demand for high-precision vacuum systems. Multi-stage ejectors are increasingly used for wafer drying, resist stripping, and vacuum chuck operations. Fab facilities integrated ejector stacks directly into tool clusters to improve uptime and reduce contamination risk. Over 50 greenfield fabs under construction globally are specifying multi-stage vacuum ejector systems during the initial build, signaling significant upcoming unit demand.

High-velocity fluid streams used in multi-stage ejectors cause wear on nozzle materials. Even with hardened alloys, nozzle erosion can lead to performance drops of 10–12% within 1,000 operational hours. Maintenance requires precise machining or replacement, and downtime for nozzle swaps often takes 4–6 hours per unit in complex installations. Manufacturers are addressing this by researching ceramic‑coated alloys and predictive maintenance schedules to balance wear costs with operational uptime.

Rise of Compact Modular Designs: Manufacturers have shifted toward compact modular ejector blocks that can be combined to match required suction levels. These plug-and-play modules reduce on-site engineering time by up to 40% and enable easier scalability across mid-sized food processing and packaging plants in Europe and North America.

Smart Integration with IoT: A growing number of ejector systems are equipped with cloud-connected sensors. In 2024, over 30% of newly installed units featured IoT-enabled dashboards, providing remote performance tracking, fault alerts, and energy usage analytics. AI-driven software optimization further allows centralized control of ejector arrays across multiple production lines, reducing field technician visits by 25%.

Material Innovation for Nozzle Durability: Developments in additive manufacturing have enabled complex nozzle geometries using ceramic-infused metals. These nozzles demonstrate triple the wear-resistance compared to steel, extending maintenance intervals from 1,000 to 3,000 hours. Adoption in high-wear environments like pulp drying and abrasive material handling is rapidly increasing.

Sustainability and Energy Recovery Focus: Eco-conscious buyers are requesting ejector systems equipped with heat recovery and vent-stream energy capture modules. In 2024, several North American plants implemented heat‑recapture units on ejector exhausts, harvesting up to 15% of expelled energy to preheat incoming process fluids—achieving meaningful reductions in energy costs and carbon footprint.

The Multi‑Stage Vacuum Ejector Market can be segmented by type, application, and end‑user. Types include oil‑free, lubricated, customized, compact, single‑stage and multi‑stage variants. Applications span pneumatic conveying, plastic/chemical processing, electronics, refining, food & beverage, and pharmaceuticals. End‑users encompass OEMs, aftermarket suppliers, industrial users, and research institutions. Each segment shows distinct trends—compact systems are emerging in food packaging, while lubricated types remain popular in heavy industries. Electronics and pharmaceutical sectors account for over 50% of total ejector installations globally, highlighting targeted demand patterns across different markets.

The market is divided into single‑stage, multi‑stage, customized designs, compact ejectors, and oil‑free vs. lubricated types. Multi‑stage ejectors hold the largest share, representing approximately 45% of units sold, due to their superior vacuum performance in industrial applications. Customized designs are the fastest growing segment, with annual growth exceeding 10%, as industries increasingly prefer tailored configurations to meet specifications like low noise, high vacuum levels, and aggressive media handling. Compact ejectors are rising in adoption across small‑scale food‑packaging plants and labs, motivated by footprint reduction and plug‑and‑play setups. Oil‑free ejectors, representing nearly one third of total volume, are also gaining momentum in hygienic and semiconductor environments where contamination is a concern.

Applications break down into pneumatic conveying, plastic processing, food & beverage, pharmaceuticals, chemical processing, electronics, and refining. Pneumatic conveying leads in shipment volumes—over 30% of global demand—given its widespread use in bulk material transfer across chemicals, cement, and food industries. The fastest growing application is pharmaceutical and biotech vacuum-drying; adoption surged around 15% year-over-year due to increased demand for freeze-drying vials and sterile filling lines. Food & beverage–related packaging also shows high growth (+12%), driven by aseptic and shelf-life-enhancement processes. Electronics and semiconductor cleanroom applications maintain steady demand, accounting for about 20% of market value.

End‑user categories include OEMs, aftermarket, industrial users, and research institutions. OEMs account for nearly 50% of total revenue, supplying ejectors integrated into packaging machines, vacuum dryers, and sterilization units. The fastest-growing end‑user segment is aftermarket service providers, including system integrators and maintenance firms, growing at more than 11% annually. They benefit from rising retrofitting projects in mid-tier plants extending ejector life spans. Industrial users—manufacturers in chemicals, metals, and food—represent a strong share but slower growth (~5–7%), driven by capacity utilization.

Research institutions, while the smallest segment, are experiencing niche growth due to adoption of ejectors in pilot plants and academic labs for novel process development and materials testing.

Asia-Pacific accounted for the largest market share at 35% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6% between 2025 and 2032.

In 2024, Asia-Pacific led due to rapid industrialization in China (15%), India (8%), and Japan (6%), collectively representing over one-third of global sales. Robust demand stems from strong chemicals, pharmaceuticals, and food processing sectors, supported by government incentives for automation and energy-efficient technologies. North America followed with around 25% share, driven by U.S. and Canada’s adoption of AI- and IoT-enabled ejector systems. Europe held approximately 20%, with Germany, the U.K., and France investing in green manufacturing practices. South America, Middle East & Africa collectively contributed the remaining ~20%, with growing infrastructure projects and increasing industrial vacuum needs.

In North America, the market is seeing a surge in smart vacuum ejector adoption across chemical, pharmaceutical, and food industries. Over 30% of new installations are cloud-connected, featuring remote diagnostics and energy management dashboards. The U.S. leads with ~60% of regional spend, especially in high-tech cleanrooms and biopharma freeze-drying. Canada’s oil‑and‑gas sector contributed nearly 10% of demand, driving robust aftermarket service uptake. The push for carbon reduction has led plants to retrofit ejectors with heat-recovery modules in over 40 facilities in 2024, showcasing a clear trend toward efficiency-led upgrades.

European manufacturers are focusing on sustainable vacuum technology. More than 25% of new ejector systems in Germany and France in 2024 were oil‑free or ceramic‑composite nozzle types, aimed at lowering lifecycle emissions. Cleanroom applications in the UK and Italy now account for over 18% of total volumes, driven by the pharmaceutical and semiconductor sectors. Low-noise ejectors with sound insulation are gaining traction in urban production sites, making up 15% of new orders. Additionally, retrofitted ejector units incorporating IoT sensors increased by 22% compared to 2023, reflecting Europe’s commitment to smart and green production.

In Asia-Pacific, modular ejector stacks are rising fast, driven by flexible production demands. In 2024, China installed over 1,200 modular units across packaging, drying, and material‑handling lines—nearly 40% of its installations. India accounted for 25% of Asia‑Pacific sales, largely in chemical and cement plants upgrading to multi-stage vacuum systems. Japan, contributing 15%, prioritized compact, oil‑free ejectors in semiconductor fabs. Southeast Asia emerged with a 6% regional share, driven by growing food & beverage exports. Prefabricated ejector systems reduce installation time by 35%, aligning with manufacturers’ scaling plans.

South America's vacuum ejector market is being shaped by infrastructure investments in mining, food processing, and water treatment. Brazil leads with 12% of the regional share; its ethanol and sugar industries are upgrading vacuum packaging lines. Argentina’s chemical processing sector adopted multi-stage ejectors for solvent recovery, accounting for 8% of sales in 2024. Meanwhile, Colombia and Chile initiated pilot projects in industrial dryers and vacuum conveying—collectively contributing 5% of South America’s uptake. These projects highlight an emerging preference for robust systems capable of handling abrasive and humid conditions.

Middle East & Africa markets are driven by industrial gas processing, petrochemicals, and desalination plant upgrades. Saudi Arabia and UAE dominate regional demand—accounting for 14% and 10% respectively—by integrating vacuum ejectors in gas sweetening and waste-steam recovery units. Egypt and Nigeria are investing in food-packaging ejector retrofits, representing 6% of regional market spend. There’s growing interest in compact, oil-free ejectors for urban cleanrooms in South Africa (4% share). Modular ejector solutions are being piloted in Qatar for chemical export facilities, underscoring growing sophistication across MEA.

China – with market share of 20%, it ows to its massive manufacturing base and accelerated adoption of automation-enhanced vacuum systems.

United States – with market share of 18%, fueled by strong uptake in pharmaceuticals, semiconductor fabs, and sustainability retrofit projects.

The global Multi‑Stage Vacuum Ejector market is highly competitive with several leading manufacturers investing heavily in technology and partnerships. Key players such as Gardner Denver, Atlas Copco, and Leybold dominate through extensive product lines, strong aftermarket support, and global distribution networks, collectively accounting for nearly half of market share. Competition is intensified by differentiators such as energy efficiency, modularity, and smart-system integration. Mid-sized regional firms, particularly from Europe and Asia, are gaining momentum by developing specialized ejectors for niche markets—like compact units for semiconductor fabs or oil-low designs for cleanroom applications. Strategic alliances between OEMs and IoT platform providers have emerged, enabling predictive maintenance and remote monitoring. Additionally, corridor competition from China-based manufacturers offering cost-effective units with advanced features has pushed Western competitors to innovate, focusing on reliability and service contracts. The result is a dynamic landscape where product differentiation, technology partnerships, and service excellence are key to maintaining and growing market position.

Gardner Denver

Atlas Copco

Leybold

KNF Neuberger

Piab

Oerlikon Leybold Vacuum (Leybold)

Busch Vacuum Solutions

Pfeiffer Vacuum

Gast Group

Mitsubishi Heavy Industries

Technological advancement is reshaping the multi-stage vacuum ejector landscape, driven by miniaturization, material science, sensor integration, and digitalization. One major trend is the transition to ceramic-coated or composite nozzles, enhancing durability and reducing wear in abrasive and high-temperature environments. Edge-mounted pressure and flow sensors, paired with IoT gateways, enable real-time performance tracking and automated adjustments, often resulting in up to 15% energy savings without manual intervention. Digital twins of ejector systems allow virtual simulation, predictive wear modeling, and rapid optimization before physical deployment. Compact ejector modules, designed for plug-and-play installation, are gaining traction in pilot labs and SME plants seeking fast deployment. Additive manufacturing (3D printing) is being used to produce custom nozzle geometries that deliver optimized flow patterns and reduced noise. Additionally, AI-driven control algorithms are being embedded into PLCs to optimize dynamic multi-stage operations based on load fluctuations or fluid properties. Some leading global OEMs report conversion of over 40% of their latest units with embedded diagnostics to support remote service and condition-based maintenance, reducing unexpected downtimes and service callouts.

In July 2023, Piab released an upgraded piCOMPACT®23 vacuum ejector featuring intelligent blow‑off control and self‑adhesion sensing—allowing up to four units to operate jointly and deliver up to 20% cycle time reduction.

In February 2024, KNF Neuberger launched a brushless motor ejector system tailored for medical device drying, with integrated sensors for immediate feedback on moisture removal and system health.

In June 2024, Oerlikon Leybold Vacuum unveiled a compact, oil‑free ejector module with IoT monitoring capable of sending automated vacuum-level alerts to central control rooms, reducing manual inspections by nearly 35%.

In November 2024, Atlas Copco introduced a modular ejector stack designed for semiconductor fabs, which enables hot‑swap nozzle replacement in under five minutes, minimizing cleanroom exposure and maximizing uptime.

This report encompasses global technological offerings, market segmentation, application areas, and competitive intelligence for multi‑stage vacuum ejectors. It delves into type-level analysis, comparing single-stage vs. multi-stage, custom vs. compact, and oil-free vs. lubricated variants. It assesses key applications—pneumatic conveying, pharmaceutical lyophilization, semiconductor cleanroom use, packaging, and chemical processing—showing how ejector design aligns with sector-specific needs. End-user profiling examines OEMs, aftermarket services, industrial plants, and research labs, highlighting their adoption drivers. Regional coverage spans Asia‑Pacific, North America, Europe, Latin America, and MEA, providing insights into policy impact, infrastructure trends, and leading-country performance. Technology analysis is included, detailing material innovations, sensor integration, and IoT/AI advancements. The report reviews product launch timelines and strategic developments from major players. In short, this compendium offers actionable insights into adoption patterns and technological roadmaps for stakeholders in the global multi-stage vacuum ejector ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Multi‑Stage Vacuum Ejector Market |

| Market Revenue (2024) | USD 230.0 Million |

| Market Revenue (2032) | USD 374.1 Million |

| CAGR (2025–2032) | 6.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country‑wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Gardner Denver, Atlas Copco, Leybold, KNF Neuberger, Piab, Oerlikon Leybold Vacuum (Leybold), Busch Vacuum Solutions, Pfeiffer Vacuum, Gast Group, Mitsubishi Heavy Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |