Reports

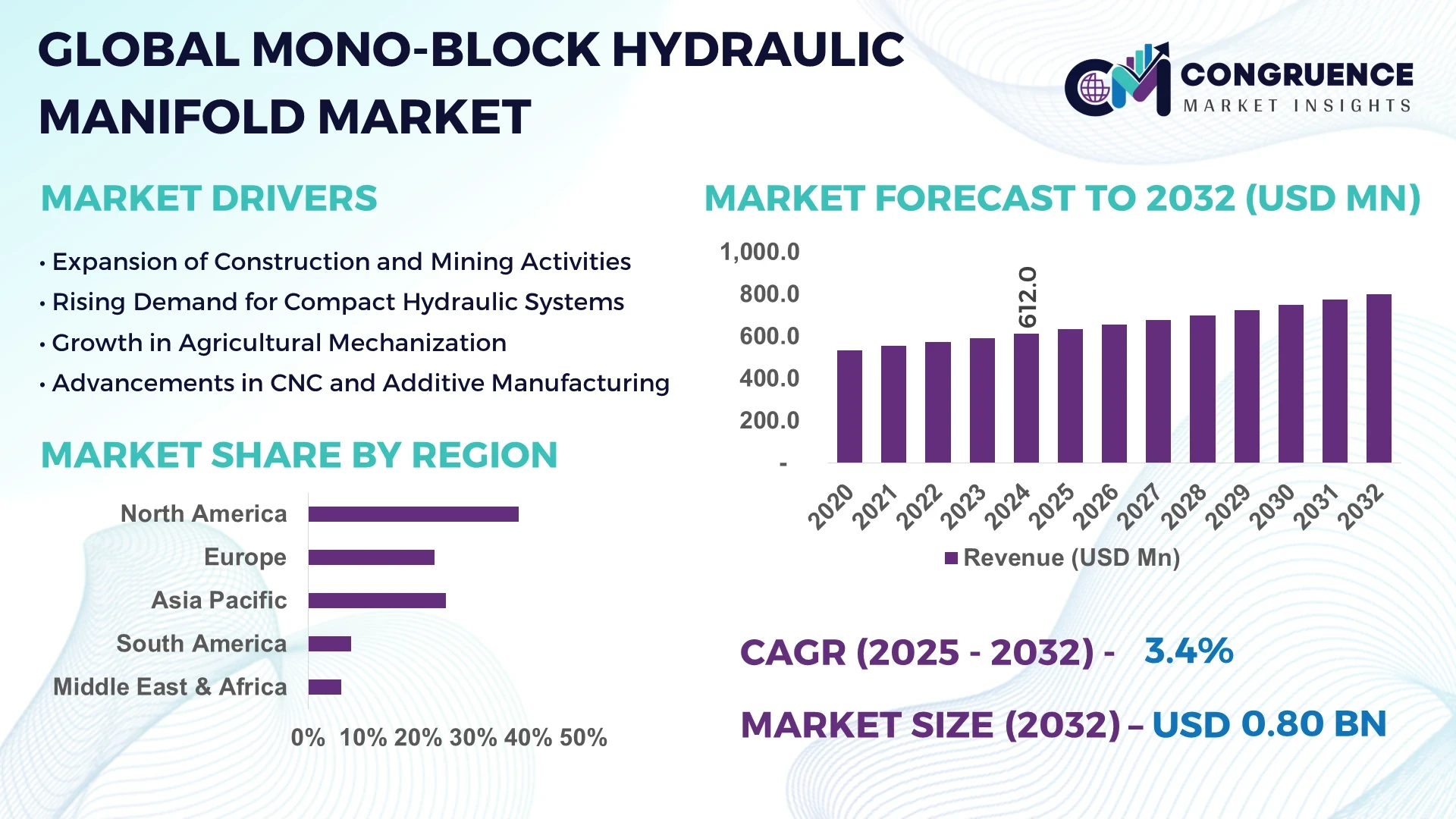

The Global Mono‑Block Hydraulic Manifold Market was valued at USD 612 Million in 2024 and is anticipated to reach a value of USD 799.7 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032.

In 2024, the United States dominated the market, holding over 30% of global revenue. This leadership is fueled by strong demand across construction and off-highway sectors, where compact, integrated manifolds are now standard for OEM hydraulic systems.

Across international markets, emphasis on modular hydraulic solutions is increasing. Customers in Europe and Asia are transitioning from large, welded manifolds to mono-block designs due to benefits in leak reduction, serviceability, and system compactness. This trend supports rapid scaling in automation and smart manufacturing.

AI is revolutionizing mono-block hydraulic manifold design, production, and operation. During 2024, manufacturers have adopted predictive maintenance through vibration and pressure sensors integrated into manifold blocks. Real-time data feeds are processed via AI models to predict valve fatigue and seal failures. Early adopters in North America have reported a 25% decline in unplanned downtime and 20% longer service intervals.

Another key application is in flow-path optimization. AI-driven simulation tools analyze thousands of manifold channel configurations to minimize pressure loss and ensure even flow distribution—reducing energy consumption by 10–15%. These algorithms incorporate thermal and hydraulic data, automating internal layout design without manual CAD iterations.

Quality assurance also benefits: vision-coupled machine learning inspects manifold surfaces and port alignment during production, halving defect rates related to channel misalignment and improving assembly consistency across batches.

Furthermore, AI contributes to lifecycle monitoring. Combine in-field sensor data with process logs to develop "digital twins" of manifold units. These twins enable scenario modeling, forecasting component wear, and providing maintenance recommendations with 90% forecasting accuracy for part replacements.

“In 2025, An OEM integrated AI-based CFD design tools to simulate and validate over 2,000 channel path variants, resulting in a 12% average gain in flow efficiency.”

OEMs in heavy equipment and off-highway vehicles are shifting to mono-block manifolds to replace multi-valve assemblies and hoses. This reduces leak risk, improves system reliability, and shrinks footprint by up to 30%, making it easier for compact machine designs and faster assembly.

Mono-block manifold production requires precision CNC machining or additive manufacturing, driving initial costs 40–60% higher than traditional valve blocks. Small-to-mid-size OEMs often avoid adoption due to budget constraints and capital investment cycles.

Emerging electric and hybrid heavy vehicles necessitate compact hydraulic solutions compatible with battery or fuel-cell integration. Mono-block manifolds’ smaller size and precise control fit well with these emerging architectures, offering improved integration and system response.

Integrating intelligent sensors and AI controllers into compact mono-block manifolds requires co-design of electronics, hydraulics, and signal processing. Ensuring data integrity under vibration, thermal stress, and hydraulic loads presents both engineering and validation challenges.

Rise in Modular Prefabricated Valve Clusters: Manufacturers now offer standardized mono-block manifold modules that can be combined to build larger valving systems, minimizing hose runs and assembly time. Adoption in Europe and North America is high in construction and agricultural OEMs.

Expansion of Additive Manufacturing (AM): 3D-printed aluminum and sand-cast manifolds are gaining traction. OEMs using AM have reported 20–30% weight and lead-time savings, enabling quicker prototyping and on-demand part production.

Smart, Sensor-Embedded Manifolds: Integration of pressure, flow, and temperature sensors directly into manifold bodies enables real-time monitoring and in-system diagnostics. Field trials show 10% lower energy consumption and 15% uptime gains in mobile hydraulic applications.

Eco-Friendly and Recyclable Materials: A push toward sustainable manufacturing has encouraged the use of recyclable aluminum alloys and biodegradable hydraulic oils compatible with mono-block designs, addressing stricter environmental regulations and green-branding initiatives.

The Mono-Block Hydraulic Manifold Market is segmented based on type, application, and end-user, each offering unique growth opportunities and market dynamics. By type, the market includes cast mono-block manifolds and machined mono-block manifolds, which differ in manufacturing complexity and usage environments. Application-wise, these manifolds are deployed across construction machinery, agricultural equipment, material handling systems, and industrial automation setups. Among end-users, original equipment manufacturers (OEMs), aftermarket service providers, and R&D institutions form the key consumer base. The growing demand for compact, reliable, and energy-efficient hydraulic systems is pushing innovation across all segments, with significant advancements in sensor integration, modularity, and automation compatibility.

The Mono-Block Hydraulic Manifold Market is primarily segmented into cast mono-block and machined mono-block manifolds. Machined mono-block manifolds hold the largest market share, accounting for approximately 58% of total volume in 2024, owing to their precision, compact form factor, and ability to integrate complex hydraulic circuits within a single block. These manifolds are widely used in mobile equipment and high-performance systems due to their reliability and leak resistance.

On the other hand, cast mono-block manifolds are gaining traction, especially in cost-sensitive markets where bulk manufacturing and simplified circuit configurations are preferred. Despite being less flexible in terms of customization, cast types are often more affordable and sufficient for low- to medium-pressure applications. The fastest-growing segment is the machined mono-block category, expected to expand rapidly due to the increasing demand for performance-critical and space-constrained hydraulic systems in compact construction and industrial equipment.

The Mono-Block Hydraulic Manifold Market is utilized in various applications including construction machinery, agriculture equipment, material handling, and industrial automation. In 2024, construction machinery led the application segment with over 35% share, driven by widespread usage in excavators, loaders, and compact track machines. These machines demand highly durable and space-saving hydraulic components, making mono-block manifolds an ideal fit. Material handling equipment, including forklifts and cranes, represents the fastest-growing segment, driven by rapid growth in logistics, warehousing, and e-commerce fulfillment centers. These applications require highly responsive and compact hydraulic systems to support automated lifting and movement. Agricultural equipment also remains a strong segment, as modern farming machinery evolves toward precision agriculture. Meanwhile, industrial automation applications—especially in robotics and smart factories—are increasingly adopting sensor-integrated manifolds to support closed-loop fluid control and remote diagnostics.

The end-user landscape of the Mono-Block Hydraulic Manifold Market comprises OEMs (Original Equipment Manufacturers), aftermarket service providers, and research & development institutions. OEMs dominate the market, representing more than 65% of total demand in 2024. These manufacturers rely heavily on custom-designed mono-block solutions integrated directly into heavy machinery, particularly in mobile hydraulics and industrial systems. Aftermarket service providers also form a significant segment, especially in regions like Asia-Pacific and Latin America, where machinery lifecycle extensions and cost-effective repairs are prioritized. This segment shows promising growth due to increasing demand for retrofits and field-replaceable components. The fastest-growing segment is R&D institutions, fueled by government initiatives and private sector investments into smart hydraulics, mechatronics, and energy-efficient systems. These entities often lead innovation in manifold design, especially for sensor integration, predictive maintenance, and AI-enhanced control systems—areas crucial for the next generation of hydraulic systems.

Asia-Pacific accounted for the largest market share at 38.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.9% between 2025 and 2032.

The strong manufacturing infrastructure and continued investments in industrial machinery, agricultural equipment, and construction vehicles have positioned Asia-Pacific as the leading region. Rapid industrial automation and the growing integration of hydraulic systems in various sectors contribute to this leadership. Meanwhile, North America is showing significant potential due to advancements in electro-hydraulic integration, smart fluid power systems, and a surge in demand for customized hydraulic solutions. The region’s growth is supported by robust infrastructure investments, especially in the U.S. and Canada, alongside growing demand in defense and aerospace applications.

Advanced Machinery Adoption Driving High-Precision Demand

In North America, there is a rising demand for high-performance hydraulic manifolds in precision-controlled machinery across sectors such as aerospace, defense, construction, and automotive. The U.S. leads with a growing number of smart farming equipment and autonomous vehicles requiring compact, multi-function manifolds with built-in sensors. Additionally, the integration of manifold systems in energy-efficient industrial automation is witnessing steady growth. Canada also shows momentum in manufacturing and heavy equipment modernization, driving increased orders for mono-block manifolds designed for extreme environmental conditions and ease of serviceability.

Sustainability and Compliance Boost Demand for Compact Systems

Europe’s mono-block hydraulic manifold market is being shaped by stringent environmental regulations, particularly in Germany, France, and Italy. Manufacturers are focusing on compact, lightweight designs that enhance energy efficiency and comply with EU fluid power emission standards. Germany remains a hub for innovation, with growing demand from automotive component manufacturers for leak-proof and integrated manifold solutions. The market is also witnessing rising investment in electric and hybrid off-highway machinery, which integrates smart hydraulic systems. Moreover, Industry 4.0 initiatives are driving adoption of AI-integrated manifolds for predictive maintenance.

Construction and Agricultural Equipment Fueling Market Expansion

Asia-Pacific’s dominance stems from its booming construction, mining, and agriculture industries. China, India, and Japan are witnessing substantial demand for mono-block hydraulic manifolds in excavators, tractors, and material handling equipment. In China, large-scale infrastructure projects and smart city developments are pushing demand for durable, cost-effective hydraulic control systems. Japan’s precision manufacturing sector is also investing in high-spec manifolds for robotics and industrial automation. India’s Make-in-India push is encouraging local production of mono-block systems to reduce import dependence and increase customization.

Infrastructure Renewal and Agriculture Drive Demand

In South America, Brazil and Argentina are the primary drivers of market growth for mono-block hydraulic manifolds. Brazil’s focus on revitalizing public infrastructure and its growing agricultural machinery exports are creating significant opportunities for hydraulic system manufacturers. The demand for rugged and weather-resistant manifolds is increasing, especially in rural agricultural areas and mining zones. Additionally, domestic manufacturers are forming partnerships to improve product affordability and regional distribution networks. Argentina is also observing growing interest in hydraulic automation in food processing and packaging sectors.

Oil & Gas and Mining Operations Fuel Market Penetration

The Middle East & Africa region is witnessing a notable increase in demand for mono-block hydraulic manifolds driven by oil & gas exploration, mining, and construction activities. Countries like Saudi Arabia and the UAE are investing in advanced fluid power technologies for drilling rigs, pipeline systems, and heavy-duty earthmovers. In Africa, South Africa leads the market due to its vast mining operations where durable, high-pressure compatible manifolds are essential. There is also growing attention toward mobile hydraulic applications in construction machinery across urbanizing areas.

China - holds the largest market share in 2024 at USD 122.6 Million, driven by its vast manufacturing base, extensive construction and agricultural activities, and rapid industrial automation, which create high demand for mono-block hydraulic manifolds.

United States - follows with a market share of USD 104.4 Million, fueled by strong adoption of advanced machinery, growing demand in aerospace and defense sectors, and integration of smart hydraulic systems in precision industrial applications.

The mono-block hydraulic manifold market is fiercely competitive, dominated by industry leaders and innovative specialty firms alike. An estimated 60–80 global manufacturers are active in 2024, with the top 10 players accounting for roughly 65% of total revenue. Competition revolves around technological innovation—smart manifolds with embedded sensors, modular designs, and lightweight materials are key differentiators. Price sensitivity remains high in emerging markets, driving mid-tier players to offer cost-effective alternatives. Leading manufacturers maintain robust service networks, often spanning 30+ countries, and differentiate via shorter lead times and regional support. Consolidation is accelerating as larger firms acquire specialized hydraulic outfits to expand capabilities in additive manufacturing or smart fluid controls. Additionally, OEM partnerships—particularly in construction, agriculture, and off-highway machinery—play a crucial role, with preferential supply contracts driving market positioning. Contracts for integrated hydraulic systems, which include manifold blocks, sensors, valves, and controllers, continue to be a focus area. Manufacturers further compete on energy efficiency, hygiene, and compliance features, adapting to customer demands for sustainability and reduced hydraulic oil usage. Aftermarket support—parts, refurbishment, and digital diagnostics—has become a competitive front as fleets demand service longevity and ease of maintenance.

Parker Hannifin Corporation

Bosch Rexroth AG

Eaton Corporation

Hydac International

Sun Hydraulics Corporation

Bucher Hydraulics

Moog Inc.

Tokyo Keiki Inc.

SCHROEDER Industries

Technological innovation is transforming mono-block hydraulic manifolds into smarter, more efficient fluid control devices. Additive manufacturing – notably 3D printing – enables complex internal channel geometries, delivering up to 20–30% weight and lead-time reductions compared to CNC-machined models. Material innovation is another trend, with high-strength aluminum and stainless alloys improving corrosion resistance and pressure ratings. Additionally, modular block systems allow easy assembly and expansion, facilitating scalable architectures without extensive redesign. Sensor integration is now common; pressure, flow, and temperature sensors embedded into manifold blocks support real-time monitoring, enabling predictive maintenance and holistic diagnostics. IoT connectivity offers fleet-wide data analysis, raising uptime and reliability metrics. Simulation tools—including AI-enhanced CFD analysis—are being adopted by OEMs to optimize fluid paths and reduce internal losses before production, improving volumetric efficiency by approximately 10–15%. Lastly, eco-focused designs are delivering recyclable aluminum blocks, biodegradable hydraulic fluid compatibility, and reduced hydraulic leakage potential.

In February 2023, Bosch Rexroth AG introduced a modular manifold block range with built-in IoT sensors and digital connectivity for predictive maintenance in automotive and industrial equipment.

In April 2024, Parker Hannifin Corporation launched a lightweight engineered manifold system designed for aerospace hydraulic circuits, claiming a 25% weight reduction compared to legacy blocks.

In June 2024, Eaton Corporation unveiled eco-friendly manifold blocks compatible with biodegradable hydraulic fluid, aligning with low-emission machine initiatives.

In September 2024, Sun Hydraulics Corporation completed integration of additive manufacturing capabilities, bringing 3D-printed manifold prototypes into full-scale testing with rapid lead-time reductions.

This market report offers a wide-ranging analysis of the global mono-block hydraulic manifold sector, covering key segments such as manufacturing type (CNC-machined, cast, and additively-manufactured blocks), application across industries like construction, agriculture, material handling, industrial automation, automotive, oil & gas, aerospace, and custom engineering. It examines distribution channels, distinguishing OEM supply, aftermarket support, and retrofit actions. The report provides comprehensive regional and country-level insights across Asia-Pacific, North America, Europe, South America, and Middle East & Africa, including market share, emerging infrastructure trends, and local manufacturing dynamics. Core market dynamics—drivers such as industry 4.0 demands and hydraulic efficiency mandates, restraints like high fabrication costs, opportunities in electric/hybrid machinery adoption, and challenges around sensor integration—are explored. It dives into technology trends including additive manufacturing, sensor-embedded smart blocks, simulation-led flow optimization, and sustainable materials. Competitive landscape coverage highlights strategies among global and regional players, partnerships, and acquisition trends. The report also outlines recent industry developments from 2023–2024, and delivers an eight-year projection through 2032 with demand forecasts, adoption scenarios, and potential entry point analysis, enabling stakeholders to mitigate risks and capitalize on sectoral shifts.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Mono-Block Hydraulic Manifold Market |

| Market Revenue (2024) | USD 612 Million |

| Market Revenue (2032) | USD 799.7 Million |

| CAGR (2025–2032) | 3.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Parker Hannifin Corporation, Bosch Rexroth AG, Eaton Corporation, Hydac International, Sun Hydraulics Corporation, Bucher Hydraulics, Moog Inc., Tokyo Keiki Inc., SCHROEDER Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |