Reports

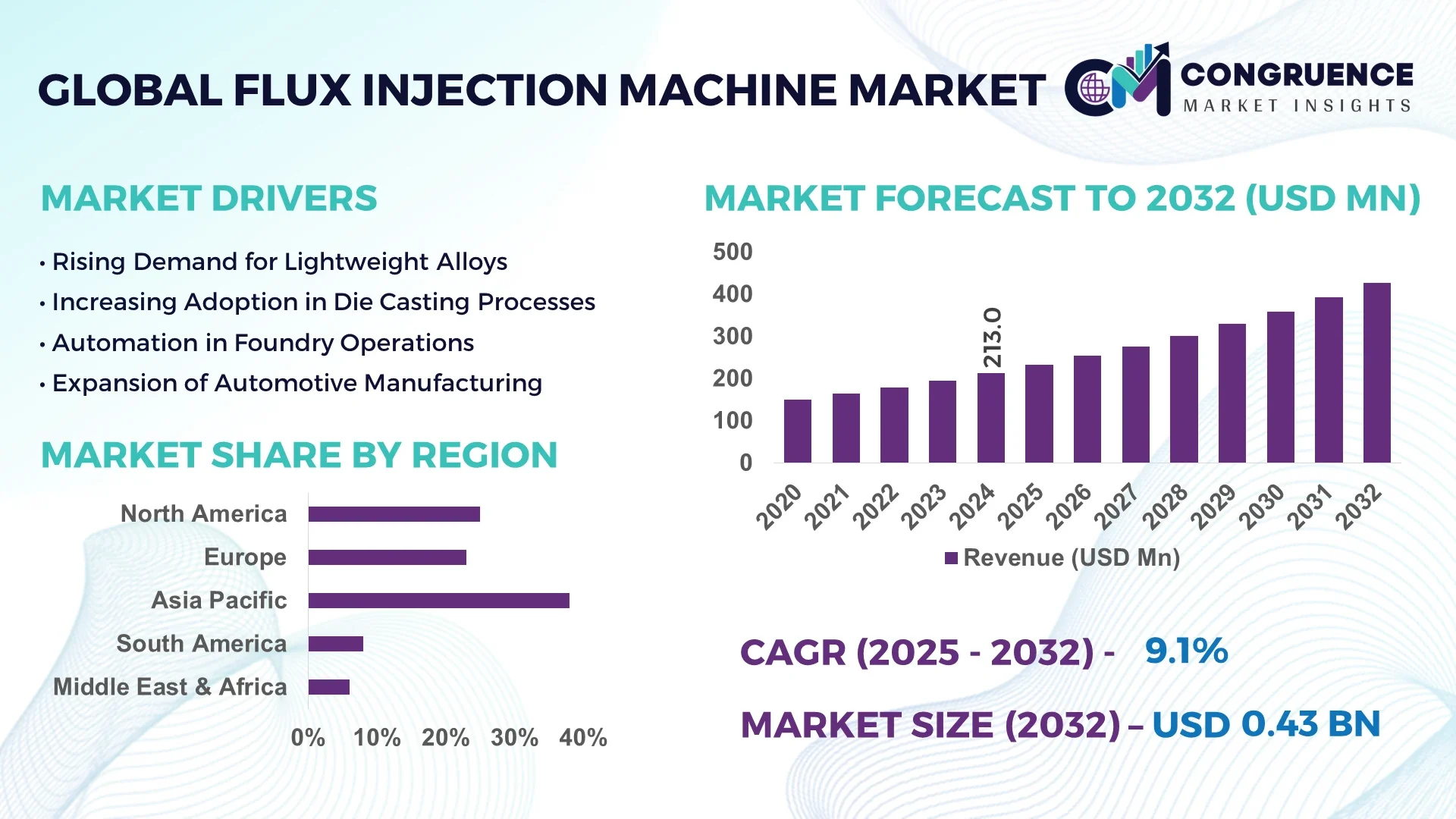

The Global Flux Injection Machine Market was valued at USD 213 Million in 2024 and is anticipated to reach a value of USD 427.54 Million by 2032 expanding at a CAGR of 9.1% between 2025 and 2032.

Japan, with its advanced manufacturing infrastructure and high investment in precision casting technology, maintains a leading position in the Flux Injection Machine market, supported by its strong production capacity, continuous technology integration in production lines, and high adoption across aerospace and automotive sectors.

The Flux Injection Machine Market has witnessed significant technological upgrades across aerospace, automotive, and defense sectors, which are key industry sectors driving adoption. Recent innovations in control systems, sensor-based automation, and modular designs are enabling consistent powder flow rates, reduced material waste, and improved casting quality. Regulatory shifts toward reducing environmental impact in foundry operations are encouraging the use of high-efficiency flux injection systems that minimize emissions during casting processes. Economic drivers such as rising automotive and aerospace component production in Asia-Pacific, coupled with regional consumption growth in India and China, are supporting market expansion. Additionally, trends in integrating IoT-based monitoring within flux injection machines to enhance predictive maintenance and reduce operational downtimes are contributing to a more agile and sustainable operational framework across the global Flux Injection Machine Market.

Artificial intelligence is rapidly transforming the Flux Injection Machine Market by enhancing operational efficiency, reducing manual errors, and streamlining process controls. AI-enabled sensors and machine learning algorithms are now used within flux injection systems to monitor and adjust powder injection rates dynamically, resulting in consistent molten metal quality while reducing material waste during the casting process. Advanced predictive maintenance powered by AI is reducing downtime by identifying system wear and component degradation in real-time, allowing for planned interventions that extend machine lifespan and reduce costly disruptions in high-volume foundry operations.

In the Flux Injection Machine Market, AI-driven image recognition is integrated with robotic arms to monitor mold fill patterns, optimizing injection parameters to maintain quality standards across aerospace and automotive casting applications. AI-based energy management within flux injection machines is enabling foundries to reduce energy consumption by automating power adjustments based on load demand. Additionally, the integration of cloud-based AI monitoring allows multi-location foundries to track performance metrics of flux injection machines, improving decision-making and ensuring adherence to sustainability goals across operations. These advancements are supporting industry-wide adoption of AI-powered flux injection machines to meet the demand for high-precision casting with lower operational costs while aligning with global sustainability initiatives.

“In March 2025, a Japanese aerospace components manufacturer integrated an AI-based real-time monitoring system into its flux injection machines, enabling the optimization of flux powder flow rates with accuracy improvements of 22% while reducing energy consumption by 14% in the production of turbine blades.”

The Flux Injection Machine Market is experiencing evolving dynamics driven by increasing demand for high-precision casting in aerospace and automotive sectors, technological innovation in powder injection control, and regulatory focus on sustainable foundry practices. Advanced integration of automation and IoT technologies within flux injection systems is enabling real-time monitoring and quality control, driving operational efficiencies and material utilization improvements in global foundries. Additionally, the rising demand for lightweight components in electric vehicles and aircraft production is supporting the adoption of advanced flux injection systems capable of handling complex alloys with higher consistency. Industry players are increasingly investing in modular flux injection machines, allowing for flexible configurations suited to varying production scales, while emerging regional consumption in Asia-Pacific is fueling the expansion of manufacturing bases, impacting the global landscape of the Flux Injection Machine Market.

Growing demand for lightweight yet durable components in the automotive and aerospace industries is significantly driving the Flux Injection Machine Market. Flux injection machines facilitate the precise addition of flux powders during molten metal processing, ensuring the removal of impurities and stabilizing alloys for improved mechanical properties in end components. With the rise in electric vehicle production and the expansion of aerospace manufacturing, the need for high-integrity aluminum and titanium alloy parts is increasing globally. The precision offered by modern flux injection systems supports consistent quality in casting processes, aligning with industry requirements for stringent tolerances and enhanced product reliability, which is boosting the demand for advanced flux injection machines across high-growth manufacturing facilities.

One of the major restraints impacting the Flux Injection Machine Market is the high initial investment required for advanced flux injection systems, which include sensor-integrated control units and automation features necessary for modern foundry operations. Small and medium-sized foundries often face financial constraints in adopting these high-cost systems, limiting their ability to upgrade aging equipment. Additionally, the integration of flux injection machines into existing production lines can require downtime for reconfiguration and staff training, leading to temporary production disruptions. These factors collectively affect the adoption pace in cost-sensitive markets and can hinder the modernization of foundries aiming to improve efficiency and quality using advanced flux injection technologies.

Emerging technological advancements in sensor-based monitoring, AI-driven predictive maintenance, and IoT integration present significant opportunities for the Flux Injection Machine Market. The incorporation of real-time sensors within flux injection machines allows for accurate monitoring of powder flow rates and injection consistency, ensuring optimized casting quality while reducing material waste. Predictive maintenance systems using machine learning can analyze equipment usage data, enabling preemptive servicing that minimizes unplanned downtimes in high-volume foundries. The increasing trend of smart manufacturing across the automotive and aerospace sectors is creating demand for advanced flux injection machines with connectivity features that support Industry 4.0 environments, providing foundries with the capability to improve productivity while aligning with sustainability initiatives.

Stringent environmental and worker safety regulations pose significant challenges for the Flux Injection Machine Market, especially in regions with strict emission control and occupational safety standards. Foundries are under increasing pressure to reduce particulate emissions during flux injection processes and to implement safety systems that protect operators from exposure to hazardous powders. Compliance with these regulations often requires additional investments in emission control systems and operator safety infrastructure, increasing operational costs for foundries adopting flux injection technology. Navigating these regulatory landscapes while maintaining production efficiency and profitability represents a critical challenge for manufacturers and end-users within the flux injection segment of the global casting industry.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping demand dynamics in the Flux Injection Machine market. Pre-bent and cut alloy components are produced off-site using automated flux injection machines, reducing labor dependency while maintaining high dimensional accuracy and consistency. In Europe and North America, construction firms prioritizing fast project delivery are increasingly investing in high-precision flux injection machines to support prefabricated structural component manufacturing, driving a notable increase in system orders across advanced casting facilities.

• Integration of IoT-Based Monitoring Systems: The Flux Injection Machine market is witnessing growing implementation of IoT-based monitoring, enabling foundries to track powder flow rates, injection parameters, and temperature control in real time. Manufacturers are leveraging IoT connectivity to remotely monitor machine health, reducing downtime while ensuring consistent product quality in automotive and aerospace casting applications. This trend supports predictive maintenance models, with some facilities reporting up to 17% reductions in unplanned downtime after adopting IoT-enabled flux injection systems.

• Transition Toward Eco-Friendly Flux Powders: The market is experiencing a shift toward the use of eco-friendly flux powders within injection machines to reduce emissions and comply with environmental standards in foundry operations. Facilities in Asia-Pacific and Europe are actively transitioning to low-emission powders compatible with advanced flux injection machines, ensuring reduced pollutant discharge during metal purification processes. This transition aligns with global sustainability targets while maintaining melt quality in aluminum and magnesium alloy casting.

• Adoption of Advanced Robotics and Automation: Automation in flux injection machines is advancing through the adoption of robotic arms for precise positioning and powder delivery, enhancing safety and consistency during casting. In high-volume aerospace component production lines, robotic integration has improved powder injection accuracy by up to 20%, reducing wastage and manual intervention. The trend of deploying robotics within flux injection machine setups is accelerating across large foundries aiming to increase productivity while reducing operational risks associated with manual powder handling.

The Flux Injection Machine market is segmented by type, application, and end-user insights, providing a clear structure for understanding market behavior across industries. By type, the market includes portable and stationary flux injection machines, with varied adoption depending on production scale and mobility needs in foundries. By application, the machines are utilized across aerospace, automotive, defense, and energy sectors, with differing operational parameters aligning with specific alloy and melt requirements. End-user segmentation reveals adoption across large-scale foundries, specialized alloy producers, and component manufacturers, reflecting unique demands for machine configurations, automation levels, and environmental compliance. Each segment contributes to shaping procurement strategies, supporting optimized investments aligned with operational goals, sustainability initiatives, and regional market growth patterns within the Flux Injection Machine market.

Portable flux injection machines are gaining attention due to their flexibility in small-batch alloy processing and maintenance operations, particularly in specialized workshops requiring mobility for casting various components. However, stationary flux injection machines remain the leading segment within the market due to their suitability for high-volume continuous casting lines in aerospace and automotive industries, supported by robust powder delivery systems and integrated quality control features. The fastest-growing type is advanced stationary machines with IoT and AI-enabled controls, driven by increasing demand for precision alloy purification in large foundries prioritizing reduced operational downtime and automated monitoring. Other types, including modular flux injection setups and customized dual-injection machines, contribute to niche requirements in high-alloy and defense applications, supporting process adaptability and complex alloy production requirements within the global Flux Injection Machine market.

Aerospace component manufacturing is the leading application in the Flux Injection Machine market due to the high demand for defect-free, lightweight alloy parts required for critical engine and structural components. The market’s fastest-growing application is in automotive lightweight alloy casting, driven by the rise of electric vehicle production and the need for enhanced thermal management components produced using high-purity aluminum and magnesium alloys. Other application areas, including defense and industrial machinery component manufacturing, utilize flux injection machines to improve melt quality while adhering to strict metallurgical standards. Energy sector applications are also gaining relevance, with flux injection supporting the production of components for renewable energy infrastructure, such as wind turbine parts, where alloy integrity and operational consistency are essential.

Large-scale foundries are the leading end-users in the Flux Injection Machine market due to their capacity for continuous casting operations, requiring robust machines capable of maintaining consistent powder flow rates and melt quality. The fastest-growing end-user segment is specialized alloy producers, driven by increasing demand for high-performance alloys in electric vehicles, aerospace, and renewable energy component manufacturing. These producers require advanced flux injection systems with precise monitoring capabilities to handle complex alloy compositions effectively. Other relevant end-users include automotive parts manufacturers and contract casting facilities, which contribute to the market landscape by adopting flux injection machines to enhance production efficiency, reduce material wastage, and meet the evolving quality demands of clients across multiple industrial sectors.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2025 and 2032.

Asia-Pacific’s position is supported by the strong manufacturing base across China, India, and Japan, where the deployment of advanced casting processes and automation in foundries is steadily increasing. The region benefits from expanding automotive and aerospace sectors and increased production of aluminum and magnesium alloy components, directly impacting flux injection machine installations. Meanwhile, South America’s anticipated growth is driven by rising investments in industrial modernization, the expansion of the mining and energy sectors in Brazil and Chile, and the adoption of sustainable manufacturing practices requiring advanced flux injection systems. These regional dynamics are shaping procurement priorities and modernization plans across the global Flux Injection Machine market.

Precision-Centric Casting Driving Advanced Equipment Adoption

North America held a 21% volume-based share in the Flux Injection Machine market in 2024, driven by advanced aerospace, automotive, and defense manufacturing sectors. The region’s precision casting operations in turbine blade, EV battery casing, and structural component production are key drivers of demand for high-performance flux injection machines. Regulatory changes under energy efficiency and emission control initiatives have pushed foundries to adopt eco-friendly flux powders and upgrade to systems with improved emission control. Technological advancements such as sensor-based monitoring, IoT integration for predictive maintenance, and automated powder flow control systems are becoming standard in many foundries across the region, aligning production with sustainability targets and operational efficiency goals within the Flux Injection Machine market.

Automation Integration in High-Precision Alloy Foundries

Europe accounted for 24% of the global Flux Injection Machine market volume in 2024, led by advanced manufacturing economies such as Germany, France, and the UK. The region’s focus on producing lightweight automotive and aerospace components drives the adoption of flux injection systems that maintain alloy purity while reducing waste. Regulatory bodies are reinforcing decarbonization policies within the foundry sector, prompting facilities to upgrade to energy-efficient flux injection machines with advanced emission control. Emerging technologies, including AI-enabled process control and robotics integration, are seeing increased adoption in European foundries, enhancing operational accuracy and reducing manual intervention while aligning with Industry 4.0 frameworks within the Flux Injection Machine market.

Foundry Modernization and Scale-Driven Growth

Asia-Pacific leads in market volume for the Flux Injection Machine market, driven by top consumers China, India, and Japan, which continue to expand their casting capacity in automotive, aerospace, and industrial machinery production. Investments in infrastructure development and industrial automation across China and India are propelling demand for advanced flux injection machines to improve casting efficiency and alloy consistency. Japan’s focus on high-precision aerospace components further strengthens regional demand. Technological innovation hubs across Asia-Pacific are supporting the integration of real-time monitoring systems, predictive analytics, and modular automation within flux injection machines, enabling foundries to meet rising quality and sustainability standards.

Industrial Modernization and Energy Sector Expansion Supporting Growth

Brazil and Argentina are the primary drivers in the South America Flux Injection Machine market, with Brazil leading regional share due to its large-scale industrial base and expanding infrastructure projects. The region’s growing energy sector, including renewable energy component manufacturing, is fueling demand for reliable casting processes supported by advanced flux injection systems. Government incentives promoting industrial modernization and local manufacturing have encouraged investment in foundry automation and environmental compliance measures, increasing the adoption of high-performance flux injection machines. The push for improved product quality and operational sustainability is shaping the region’s trajectory within the global Flux Injection Machine market.

Strategic Infrastructure Investments Fueling Equipment Demand

Regional demand in the Middle East & Africa Flux Injection Machine market is driven by oil & gas and construction industries, with the UAE and South Africa being major growth hubs. As construction and infrastructure investments expand, the need for high-quality alloy components is increasing, necessitating advanced flux injection systems to maintain consistency in casting processes. Technological modernization is visible through the adoption of semi-automated flux injection machines and basic IoT monitoring for equipment maintenance. Local regulatory measures promoting industrial sustainability and emerging trade partnerships within Africa are supporting foundries in adopting newer technologies, aligning operational goals with evolving industry standards in the Flux Injection Machine market.

China – 27% Market Share: High production capacity and strong end-user demand in automotive and aerospace sectors drive China’s leadership in the Flux Injection Machine market.

Germany – 15% Market Share: Strong end-user demand in precision casting and advanced foundry technologies positions Germany as a leader in the Flux Injection Machine market.

The Flux Injection Machine market is characterized by a moderately consolidated competitive environment with over 45 active global and regional players providing advanced flux injection solutions to diverse end-use industries. Market participants compete on the basis of technological capabilities, product reliability, automation compatibility, and operational efficiency enhancements. Companies are actively engaging in strategic initiatives such as technology collaborations, digital service expansions, and precision upgrade programs to strengthen their market positioning. For instance, several leading manufacturers have launched sensor-integrated flux injection machines with real-time monitoring and IoT-enabled predictive maintenance features, aligning with the increasing demand for automated and data-driven foundry operations. Partnerships with casting facilities for pilot installations and product validation are common practices to expand market presence while ensuring compliance with evolving environmental and quality standards. Additionally, the competitive landscape is influenced by the continuous development of eco-friendly flux powders compatible with injection systems, driving suppliers to differentiate through system-powder compatibility and emissions control technology. Regional players in Asia-Pacific and Europe are focusing on localized production and service support to strengthen their foothold while addressing region-specific regulatory and operational requirements within the Flux Injection Machine market.

Inductotherm Group

Buhler Group

Otto Junker GmbH

Sintokogio Ltd.

StrikoWestofen GmbH

Foshan Hengyang Furnace Manufacturing Co., Ltd.

Yizumi Holdings Co., Ltd.

ABP Induction Systems GmbH

Krown SA

Electrotherm (India) Ltd.

Technological advancements in the Flux Injection Machine market are enhancing operational efficiency, quality consistency, and sustainability within foundry and precision casting operations. Modern flux injection machines now integrate advanced sensor technology to monitor powder injection rates, melt temperatures, and alloy composition in real time, enabling precise control of flux distribution during casting. This ensures uniform alloy purification while reducing material waste and improving the mechanical integrity of final components. IoT-enabled connectivity is increasingly standard, allowing remote monitoring, predictive maintenance scheduling, and production data analytics, reducing unplanned downtimes and extending equipment life.

AI-powered control systems are being adopted to automatically adjust flux injection parameters based on live feedback from sensors, reducing manual intervention while maintaining consistent product quality. Robotics integration, particularly in automated positioning and powder handling, has enhanced safety and accuracy during the flux injection process, addressing labor challenges in high-volume foundry environments. Additionally, energy-efficient induction systems and modular machine designs are gaining traction to reduce operational energy consumption and improve flexibility in installation across different production scales. Eco-friendly flux powder compatibility is another area of focus, with machines being designed to handle new low-emission fluxes aligned with global environmental standards. Collectively, these technologies are shaping a modern, intelligent, and sustainable operational landscape within the Flux Injection Machine market.

• In February 2023, Buhler Group unveiled its next-generation flux injection machine with integrated AI-powered adaptive control, which achieved a 15% reduction in flux powder usage during aluminum casting trials while maintaining alloy purity across automotive component production lines.

• In May 2023, Otto Junker GmbH launched a new modular flux injection unit compatible with eco-friendly flux powders, which was installed in a European aerospace foundry, enabling a 12% reduction in emissions while improving melt quality consistency for high-alloy parts.

• In March 2024, Inductotherm Group introduced an IoT-enabled flux injection machine series featuring real-time monitoring and remote diagnostics, helping a major US automotive supplier reduce unplanned downtime by 18% and optimize maintenance cycles within its high-volume casting operations.

• In April 2024, Foshan Hengyang Furnace Manufacturing Co., Ltd. completed the deployment of its advanced robotic-assisted flux injection system in a Chinese foundry, increasing powder injection accuracy by 21% and reducing manual handling requirements, supporting improved operator safety and operational consistency.

The Flux Injection Machine Market Report comprehensively analyzes the evolving market across types, including portable and stationary systems, and explores applications in aerospace, automotive, defense, and energy sectors. The report covers geographic regions such as Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, providing insights into regional consumption patterns, technology adoption trends, and infrastructure readiness for flux injection equipment. It examines technological advancements including AI-integrated control systems, sensor-based powder flow monitoring, IoT-enabled predictive maintenance capabilities, robotics-assisted flux injection, and compatibility with eco-friendly flux powders.

The report also considers emerging niches, such as automated flux injection systems for electric vehicle battery casing production and high-performance alloy component manufacturing for renewable energy infrastructure. It evaluates the operational, regulatory, and sustainability factors influencing procurement and modernization decisions within foundries and specialized alloy production facilities globally. With a focus on end-user dynamics across large foundries, alloy producers, and automotive component manufacturers, the report provides a strategic overview of factors impacting market positioning and competitive landscape while identifying growth opportunities driven by technological modernization and evolving industrial demand. This analysis is structured to assist decision-makers in understanding the full market spectrum, supporting investment planning and operational strategy formulation within the Flux Injection Machine market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 213 Million |

|

Market Revenue in 2032 |

USD 427.54 Million |

|

CAGR (2025 - 2032) |

9.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Inductotherm Group, Buhler Group, Otto Junker GmbH, Sintokogio Ltd., StrikoWestofen GmbH, Foshan Hengyang Furnace Manufacturing Co., Ltd., Yizumi Holdings Co., Ltd., ABP Induction Systems GmbH, Krown SA, Electrotherm (India) Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |