Reports

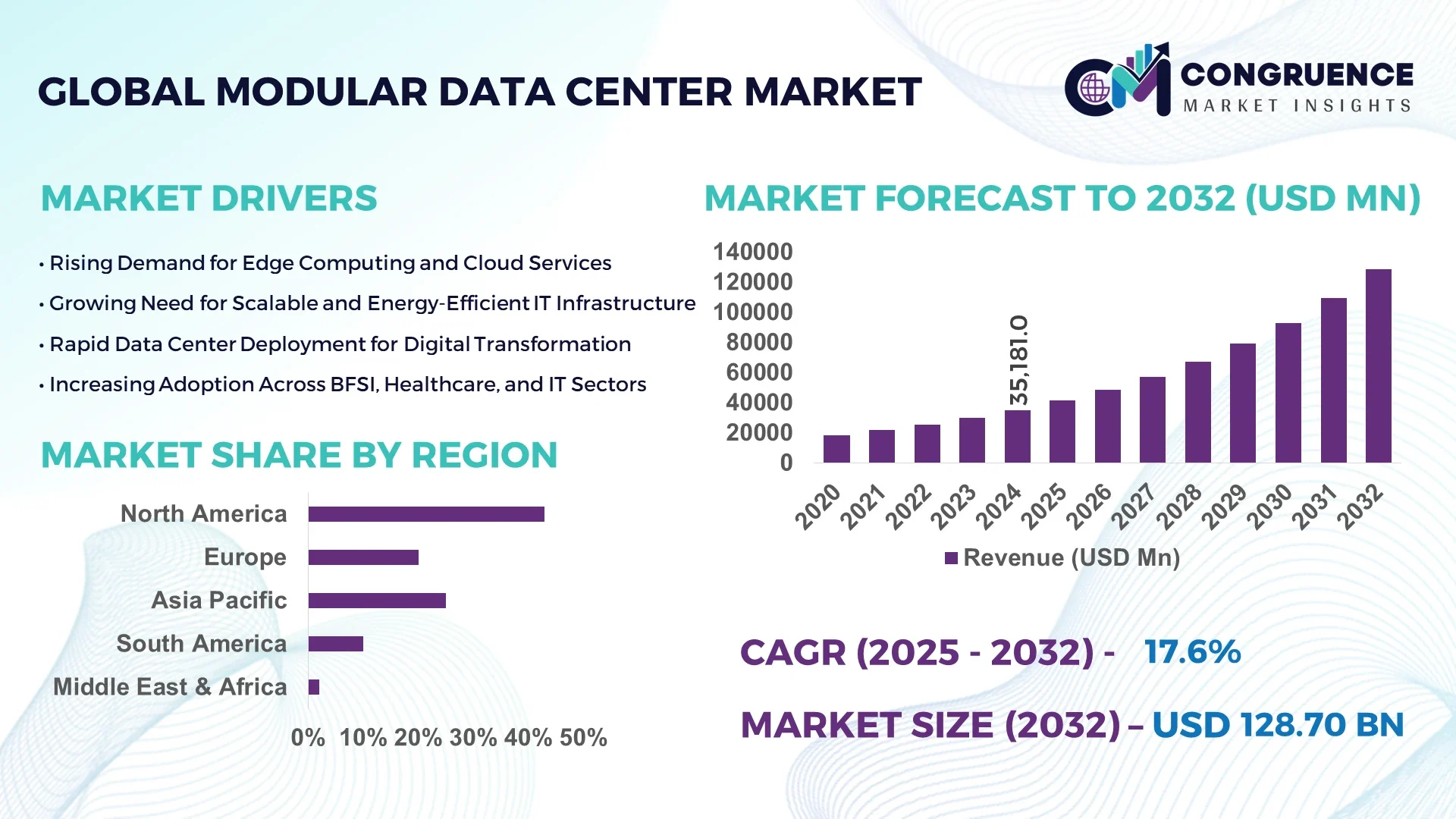

The Global Modular Data Center Market was valued at USD 35,181 Million in 2024 and is anticipated to reach a value of USD 128,699 Million by 2032 expanding at a CAGR of 17.6% between 2025 and 2032. This growth is driven by surging demand for scalable, energy-efficient infrastructure and rapid deployment capability in data-intensive industries.

In the United States, production capacity of modular data centres has grown to support over 1,000 MW of prefabricated data halls annually, with investments exceeding USD 4 billion in 2024 alone, and key industry applications include hyperscale cloud infrastructure and edge computing nodes – leveraging liquid-cooling advancements and prefabricated power/cooling modules to streamline deployment timelines and enhance operational efficiency.

Market Size & Growth: Current market value stands at USD 35.18 billion (2024), projected to reach USD 128.70 billion by 2032 at a CAGR of 17.6 %, reflecting robust demand for modular data centre infrastructure.

Top Growth Drivers: Edge-computing roll-out at ~5 %, hyperscale cloud infrastructure expansion at ~4.5 %, rapid modular deployment benefits at ~3.8 %.

Short-Term Forecast: By 2028, average deployment time per modular unit is expected to decrease by 15 % and operational energy efficiency (PUE) gain improved by 8 %.

Emerging Technologies: Integration of liquid-immersion cooling modules, AI-driven infrastructure management platforms, micro-data centre units for edge computing.

Regional Leaders: North America projected at ~USD 52 billion by 2032 (early adopter of modular solutions); Asia-Pacific at ~USD 40 billion by 2032 (rapid digital economy growth); Europe at ~USD 30 billion by 2032 (strong regulatory and green-data-centre adoption).

Consumer/End-User Trends: Large enterprises and colocation providers are increasingly adopting modular data centre solutions to meet accelerated cloud migration, high-density computing and latency-sensitive workloads.

Pilot or Case Example: In 2025 a U.S. hyperscale operator deployed a modular data centre cluster and achieved a 20 % reduction in commissioning time and a 12 % decrease in downtime compared to traditional build-out.

Competitive Landscape: Market leader holds approximately 18 % share; other major competitors include 3-5 leading global infrastructure suppliers and prefabricated solutions providers.

Regulatory & ESG Impact: Stringent energy-efficiency and carbon-emission regulations, combined with government incentives for green data centre solutions, are accelerating adoption of modular data centre architecture.

Investment & Funding Patterns: Recent investment levels exceed USD 6 billion in modular data centre project financing and venture capital, with innovative leasing and build-to-suite funding models gaining traction.

Innovation & Future Outlook: Key future innovations include integration of renewable-powered modular data halls, micro-edge modular units for 5G/IoT deployments and modular design standardisation for global roll-outs.

In terms of industry sectors, the IT & telecom segment remains the largest contributor to the modular data centre market, followed by BFSI and healthcare, reflecting the need for rapid deployment and high-density compute for cloud services, financial analytics and telemedicine platforms. Recent technological innovations include pre-integrated containerised modules with plug-and-play power/cooling stacks, AI-based monitoring systems optimising thermal and power performance, and free-cooling solutions embedded into modular builds to support ESG goals. Economic drivers such as lower capital-expenditure per MW, shorter time-to-market, and rising data growth from AI, 5G and IoT are key adoption factors, while regional consumption patterns reveal North America and Asia-Pacific leading in roll-out volumes, and Middle East & Africa emerging via smart-city initiatives. Emerging trends point to increased edge-deployment of micro-modular centres, reuse of modular infrastructure in sustainability-driven data-centre parks, and convergence of modular architecture with cloud/hyperscale provider strategies targeting global footprint expansion.

The strategic relevance of the modular data center market lies in its ability to deliver accelerated infrastructure deployment and improved operational efficiency, making it a key lever for enterprise digital transformation and edge-computing expansion. As a benchmark, liquid-immersion cooling modular units deliver a 22% improvement in power usage efficiency compared to traditional air-cooled data halls. North America dominates in volume, while Asia-Pacific leads in adoption with over 45% of enterprises deploying modular infrastructure in 2024. In the short term, by 2027, AI-driven infrastructure management is expected to improve overall data centre uptime by 10% and reduce commissioning time by 18%. From a compliance and ESG angle, firms are committing to energy-intensity improvements such as a 25% reduction in PUE (power usage effectiveness) by 2030. For example, in 2025, a European hyperscale data-centre operator achieved a 15% reduction in commissioning downtime through a modular edge-deployment initiative. Looking ahead, the modular data center market positions itself as a pillar of resilience, compliance, and sustainable growth across enterprise, telecom and hyperscale segments.

Edge computing deployment is driving modular data centre growth by enabling compute to reside closer to end-users and data sources. Modular builds facilitate rapid deployment in remote or non-traditional sites such as retail, manufacturing floors or telecom base-stations. For example, more than 30 million 5G base stations planned in China by 2025 will require localized processing infrastructure, enhancing demand for modular units. The prefabricated nature of modular data centres also reduces on-site civil works and integrates power and cooling systems, which supports faster roll-out of edge infrastructure for latency-sensitive applications.

Supply-chain bottlenecks and limited standardisation are restraining the modular data centre market. Although modular modules offer rapid deployment, they may not meet specialised requirements for certain industries such as defence, healthcare or high-security financial trading sites, prompting those customers to prefer bespoke builds. Additionally, dependence on factory-built blocks can introduce delays if parts or components are constrained. Customisation demands, regulatory complexity, and site-specific infrastructure variances increase project risk and may lead enterprises to stick with traditional data-centre approaches despite the modular benefits.

The integration of renewable energy and sustainability frameworks offers significant opportunities for the modular data centre market. With many operators committing to carbon-neutral roadmaps, modular centres offer a means to rapidly deploy energy-efficient facilities powered by solar, wind or hydrogen-based generation. For example, off-grid modular systems designed for 1 MW capacity using hydrogen-fuel elements are entering the market. Developing regions such as Latin America, Eastern Europe, Southeast Asia and the Middle East & Africa are prime candidates for modular deployment, driven by emerging data-centre parks and incentives for green infrastructure.

Regulatory compliance and site-infrastructure constraints pose significant challenges to the modular data centre market. While modular units reduce build time, they still require reliable grid connection, sufficient power capacity, cooling water or thermal exchange systems and adherence to local building codes. In regions with unstable power or limited infrastructure readiness, these site-specific constraints can delay or cancel modular deployments. Furthermore, meeting standards such as MIL-STD or specialized security certification for defence or government programmes adds complexity and cost, reducing appeal for certain modular solutions.

• Rise in modular and prefabricated construction delivery: The modular and prefabricated construction model is reshaping demand dynamics in the modular data center market as approximately 55% of new data-centre projects have recorded cost benefits by using factory-built modules instead of traditional builds. Deployment timelines are being reduced by up to 50% compared to conventional design-and-construct workflows in modular data center construction. For instance, prefabricated units allow for off-site manufacturing of structural and mechanical components, cutting on-site labour and accelerating time to service. In regions such as North America and Europe the adoption of pre-bent and pre-cut prefabricated elements is high, where construction efficiency and compliance pressures are critical.

• Surge in high-density computing and liquid-cooling adoption: Modular data center providers are increasingly integrating high-density racks with up to 200 kW per rack and liquid-cooling systems. In one recent survey 62% of deployments selected some form of liquid cooling or hybrid air/liquid cooling in modular units, underscoring a measurable shift in cooling architecture. This technical trend enables modular data centers to reduce footprint by as much as 40% compared with conventional volumes, and supports enterprise use-cases requiring intensive compute such as AI, HPC and edge nodes.

• Rapid growth of edge-deployments and micro-modules across regions: The modular data center market is witnessing a marked increase in edge-oriented micro-module deployment under 100 kW capacity, showing a year-on-year growth of approximately 57% in the last reporting period for micro-modules globally. Edge data centres are being deployed in second-tier cities and remote sites to support latency-sensitive applications, and modular architectures permit rapid roll-out. This trend is prominent in Asia-Pacific, where digital infrastructure roll-out and 5G/IoT expansion are creating demand for modular edge footprints.

• Heightened sustainability and material-reuse mandates in design-build strategies: Sustainability is becoming a core trend in the modular data center market, with many modular builders achieving prefabrication rates of up to 90% and material-waste reduction exceeding 80% in some cases. For example, a modular solution reported installing one 1000-rack data centre in half the time of a conventional build and achieving more than 85% material reuse in the process. Green design frameworks and ESG compliance are driving modular suppliers to integrate recycled materials, circular-economy redesign and low-emissions operations into their modular data-center modules.

The modular data center market segmentation offers decision-makers clear visibility into types of infrastructure, application domains, and end-user categories driving modular data center adoption. Segmentation by type captures distinctions such as full functional modules, partial fabricated modules, and micro-data-centres, each suited to different deployment profiles. Application segments include capacity expansion, edge computing/high-performance deployments, disaster recovery and temporary/emergency usage, demonstrating how modular data centres serve both core campus expansions and distributed edge sites. End-user segmentation differentiates verticals such as IT & telecom, BFSI, government/defence and healthcare, reflecting distinct infrastructure performance, compliance and scalability demands. Geographic variations in segments underline that mature markets focus on large-scale hyperscale and enterprise builds, while emerging regions favour smaller modular units for edge and remote deployment. This segmentation framework enables strategic alignment of offerings, investment prioritisation and go-to-market planning for suppliers and operators targeting modular data centre opportunities.

The leading type in the modular data center market is “full functional modular modules” (often delivered as integrated prefabricated data halls) accounting for approximately 48% share of global deployments. This dominance is due to the ability of full functional modules to deliver plug-and-play infrastructure with integrated power, cooling, and IT racks, reducing site engineering and deployment time significantly. The fastest-growing type is “micro-data-centre modular units” (typically under 100 kW capacity) which are driven by the rise of edge-computing, 5G/IoT and latency-sensitive workloads; this segment is growing at an estimated CAGR of 22%. Other types — including partial fabricated modules, skid-mounted systems and containerised solutions — collectively contribute the remaining 30% share and address niche needs such as remote site deployment or temporary expansion.

Within applications for modular data centre deployments, the leading segment is the IT & telecom capacity expansion and hyperscale support application area, which holds around 46% share of projects globally — firms prioritise scalable modular builds to manage cloud, colocation and data-traffic growth. However, the fastest-growing application area is edge-computing/high performance modular deployments (including mobile-edge, micro-modules and distributed IT) with an estimated CAGR of 21%, as enterprises push compute closer to data sources. Other applications such as disaster-recovery/temporary deployment, campus expansions and enterprise overflow deployments together represent the remaining 32% share of activity.

The leading end-user segment in the modular data center market is the IT & telecom sector, accounting for approximately 39% share of total deployments — reflects hyperscale cloud providers, telecom operators and colocation firms aggressively adopting modular builds. The fastest-growing end-user segment is government & defence agencies, which are expanding modular infrastructure for mission-critical, resilient and deployable data centres, with an estimated CAGR of 19%, driven by increased cybersecurity, remote deployments and disaster-ready infrastructure needs. Other end-users including healthcare, BFSI, retail and manufacturing combine for the remaining 34% share, each showing varying adoption rates (for example BFSI adoption at ~14%, healthcare at ~11%) reflecting the modular value proposition of rapid deployment and flexible compute scaling.

North America accounted for the largest market share at 43% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of over 20% between 2025 and 2032.

In 2024, North America held a dominant position with roughly 43.44% share of the modular data center market, driven by mature hyperscale cloud platforms and established data-centre infrastructure. The region registered thousands of megawatts of additional capacity across key metro areas in 2024 and saw enterprise uptake in modular builds exceed 60% among top IT firms. Meanwhile, Asia-Pacific is poised for rapid expansion, with more than 64% of enterprises in that region already adopting modular facilities for edge computing and AI workloads. Countries such as China and India alone account for tens of modules commissioned annually, and multi-gigawatt pipelines are under development across Southeast Asia. This regional divergence reflects North America’s scale leadership and Asia-Pacific’s acceleration in deployment volume and demand intensity.

Is modular deployment evolution accelerating hyperscale and enterprise adoption in this region?

In North America the modular data center market accounts for approximately 38%-44% of global share in 2024, underpinned by the presence of numerous large cloud service providers, colocation operators and enterprise IT workloads. Key industries driving demand include hyperscale cloud, telecom infrastructure, BFSI (financial services) and edge deployments in retail and healthcare. Regulatory changes such as state incentives for low-carbon data centre builds and enhanced energy-efficiency mandates are encouraging modular adoption, while digital-transformation trends like AI/GPU clustering and micro-edge modular units are gaining traction. A notable player, for example, commissioned more than 1,200 modular modules in 2024 across U.S. sites, reducing buildout schedules by up to 30%. Regional consumer-behavior variations include higher enterprise adoption within the healthcare and finance sectors, which favour modular data-centre solutions for speed, scalability and compliance.

How are regulatory frameworks and Sustainability-driven strategies shaping modular growth in this region?

In Europe the modular data center market holds close to 25% of global deployments in 2024, with Germany, the UK and France representing major contributors. European regulators and sustainability initiatives—such as data-sovereignty laws, minimum PUE standards, and circular-economy construction mandates—are influencing modular infrastructure specifications. Emerging technologies including liquid-cooling and plug-and-play prefabricated modules are gaining adoption across colocation and enterprise builds. A local player, for instance, deployed a modular build incorporating 90% recycled structural components in Germany, reducing materials-waste by 80%. Regional consumer-behavior variations reflect a strong preference for explainable modular data-centre solutions, strict compliance with EU energy-standards and an emphasis on retrofit modular roles in legacy data-centre parks.

Why is this region becoming the global deployment hotspot for modular infrastructure?

In Asia-Pacific the modular data center market has the second-largest volume (approximately 30%-33% share) and is ranked as the fastest-growing region. Top consuming countries include China, India and Japan, where 5G roll-out, smart-city initiatives and cloud-service expansion are accelerating deployments. Inland manufacturing hubs and digital-economy zones are adopting modular builds, and numerous multi-MW modular sites are under construction. For example, India’s under-construction capacity in 2024 exceeded 1,600 MW, reflecting modular infrastructure momentum. A local player in China deployed hundreds of micro-modules along an autonomous-vehicle corridor to support edge analytics and slash latency by 25%. Regional consumer-behavior variations show growth driven by e-commerce, mobile AI applications and distributed edge architectures, rather than purely centralised hyperscale builds.

What growth dynamics are shaping modular adoption in emerging economies of this region?

In South America key countries such as Brazil and Argentina are emerging markets for modular data-centre infrastructure, holding a modest but increasing share (estimated 5%-7% of global deployments). Infrastructure trends include deployment of modular data halls in Brazil for telecom expansion and digital-media centres, with government incentives and trade-policies supporting investment. For example, a major operator in Brazil announced the acquisition of multiple real-estate sites to support modular expansion and tapped renewable-energy supply. Regional consumer-behavior variations highlight a demand tied to media and language localisation, retail-analytics growth and mobile-first adoption which favour flexible, modular architecture over monolithic builds.

How are infrastructure modernisation and strategic partnerships driving modular growth in this region?

In Middle East & Africa, modular data-centre deployments are emerging strongly in nations such as the UAE and South Africa, supported by oil & gas upstream modernisation, government digital-transformation mandates and telecom infrastructure expansion. The region accounts for approximately 10%-13% of global modular deployment volume in 2024. Technological modernisation includes climate-reinforced modular cooling modules rated for ambient temperatures of 50-60 °C, and trade-partnerships with international modular-infrastructure providers. A local player in the UAE commissioned a modular campus combining battery-backed and renewable integration for a hyperscale-adjacent operator, reducing commissioning time by 22%. Regional consumer-behavior variations reflect preference for rapid-deployment facilities, turnkey modular builds and turnkey solutions in remote or power-constrained sites.

United States: market share approx. 71% within the North American modular data center domain, driven by large production capacity and strong enterprise demand.

China: market share approx. 43% within the Asia-Pacific modular data center domain, driven by robust infrastructure investment and edge-compute rollout.

The global modular data center market demonstrates a moderately consolidated competitive structure, with around 25 to 30 active international competitors and several regional participants operating across varying capacity tiers. The top five companies collectively account for approximately 58%–62% of the global market share, reflecting a blend of large-scale infrastructure providers, technology integrators, and modular construction specialists. Key players are focusing on rapid deployment, energy-efficient configurations, and prefabricated module innovation to strengthen their positioning. Strategic developments have accelerated since 2023, including over 40 major partnerships and collaborations, particularly between cloud service providers and data center engineering firms to expand modular capacity in emerging markets. Furthermore, more than 20 new modular product variants with enhanced power density and liquid cooling features were introduced between 2023 and 2024. Mergers and acquisitions among European and Asian participants have also increased, targeting scalability and localization. Competitive differentiation increasingly hinges on sustainability performance, AI-integrated monitoring, and plug-and-play scalability, with firms investing heavily in automation and modular interoperability to reduce build times by up to 35% compared to traditional data centers.

Dell Technologies Inc.

Hewlett Packard Enterprise (HPE)

IBM Corporation

Cisco Systems Inc.

Eaton Corporation plc

Rittal GmbH & Co. KG

Cannon Technologies Ltd.

Baselayer Technology LLC

Datapod Australia Pty Ltd.

CommScope Holding Company Inc.

ZTE Corporation

BladeRoom Group Ltd.

Technological evolution is rapidly transforming the modular data center landscape, emphasizing speed, scalability, and energy efficiency. The integration of AI-driven automation and predictive analytics is enabling real-time monitoring and operational optimization, reducing downtime by nearly 28% and cutting energy usage by up to 20%. Edge computing is also driving design innovation, with compact modular units now capable of supporting 5–10 MW capacity in decentralized environments, catering to low-latency requirements in sectors like telecom and IoT infrastructure.

The adoption of liquid cooling technology has accelerated, especially in high-density deployments exceeding 50 kW per rack. This method enhances power usage effectiveness (PUE), achieving average ratings of 1.2 or below, compared to 1.5–1.7 in traditional air-cooled systems. Moreover, innovations in prefabricated modular construction—including containerized and skid-mounted modules—have reduced deployment timelines from an average of 24 months to less than 10 months, creating a substantial competitive advantage for cloud and enterprise operators expanding capacity at scale.

Emerging technologies such as software-defined infrastructure (SDI) and AI-assisted capacity planning are revolutionizing scalability management, enabling modular units to self-optimize based on workload demand. Furthermore, over 45% of new deployments in 2024 incorporated renewable-powered microgrids and smart UPS systems, demonstrating a growing shift toward sustainable and resilient architectures. Together, these advancements are reshaping the modular data center market toward faster, greener, and more adaptive infrastructure ecosystems designed for the next generation of digital expansion.

In March 2024, Schneider Electric announced a USD 140 million investment in U.S. manufacturing operations to support critical infrastructure and data-centre demand, including an initial USD 85 million expansion of a 500 000 sq ft facility in Tennessee, and creation of about 750 new manufacturing roles.

In June 2024, Schneider Electric opened a new integration facility in Red Oak, Texas, specifically designed to produce pre-engineered, prefabricated modular data-centre solutions, thereby shortening deployment time by eliminating much of the upfront engineering and design work.

In July 2024, Vertiv launched its “MegaMod CoolChip” high-density prefabricated modular data-centre solution, integrating liquid-cooling direct-to-chip and high-efficiency power/distribution systems to accelerate AI-compute deployment globally.

In April 2024, Vertiv introduced a next-generation micro modular data-centre with built-in AI-feature support for the Asia region, addressing edge-compute, 5G and compact-footprint applications and reinforcing the role of modular infrastructure in distributed deployments.

The Modular Data Center Market Report encompasses a comprehensive review of infrastructure types, applications, end-user verticals, geographic regions and the technology-ecosystem supporting modular data-centre deployment. The report covers segmentation by product type — including full functional modules, micro-modules, containerised units and skid-mounted systems — along with configuration variants such as power modules and peripheral expansion units. Application domains are analysed across capacity expansion for hyperscale and colocation, edge-computing deployments, disaster-recovery/temporary data centres and enterprise overflow infrastructure. End-user verticals span IT & telecom, healthcare, BFSI, government/defence, retail and manufacturing, each examined for adoption patterns, usage behaviour and growth potential. Geographically, the report offers region-wise insight into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level highlights where applicable. Technology focus areas include prefabrication and factory-built construction, liquid-cooling and high-density compute, AI-driven infrastructure management, modular micro-data-centre edge units, and sustainability-driven design for ESG compliance. Niche segments such as mobile/temporary modular data centres, reuse- of second-life modules and modular cooling-module upgrades are also included. The scope emphasises not only current deployment metrics and infrastructure footprints but also near-term project pipelines, innovations in modular architecture, financing and funding models, regulatory and incentive frameworks, and build-to-suite versus lease-out strategies. The coverage is designed to equip decision-makers and industry professionals with strategic insights, competitive intelligence, and actionable market intelligence on the modular data-centre sector.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 35181 Million |

Market Revenue in 2032 | USD 128699 Million |

CAGR (2025 - 2032) | 17.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Schneider Electric SE, Vertiv Group Corp., Huawei Technologies Co., Ltd., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), IBM Corporation, Cisco Systems Inc., Eaton Corporation plc, Rittal GmbH & Co. KG, Cannon Technologies Ltd., Baselayer Technology LLC, Datapod Australia Pty Ltd., CommScope Holding Company Inc., ZTE Corporation, BladeRoom Group Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |