Reports

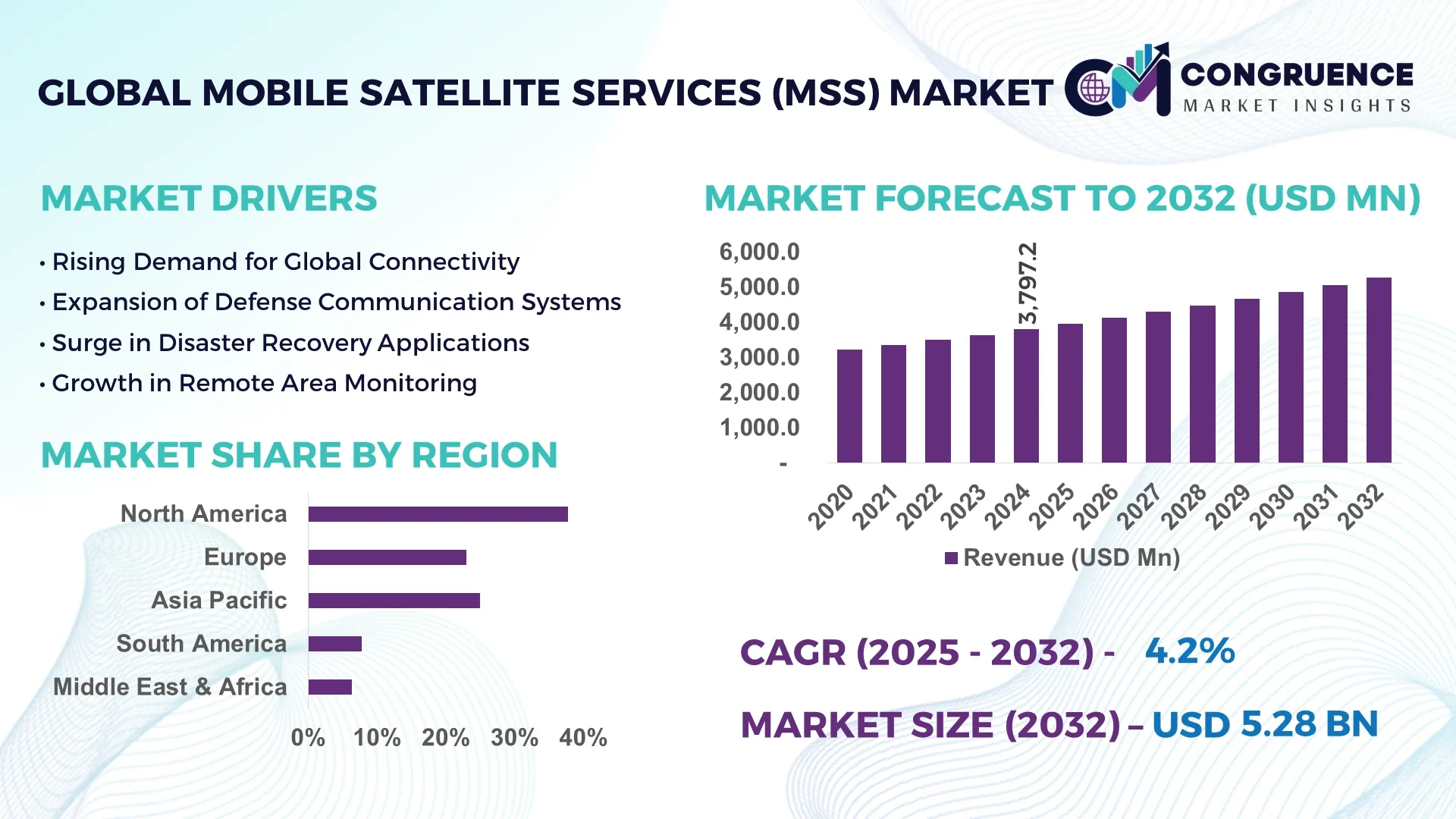

The Global Mobile Satellite Services (MSS) Market was valued at USD 3797.15 Million in 2024 and is anticipated to reach a value of USD 5277.15 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032.

The United States holds a leading position in the Mobile Satellite Services (MSS) Market, supported by advanced production facilities, rising private investments in mobile satellite technologies, continuous defense sector adoption, and integration of MSS solutions in critical maritime and aviation applications alongside consistent upgrades in mobile satellite terminals and ground station capabilities.

The Mobile Satellite Services (MSS) Market is witnessing robust expansion across government, maritime, aviation, disaster management, and remote communication sectors, driven by rising demand for seamless connectivity and reliable communication in remote areas. The increasing deployment of L-band and S-band frequencies for MSS applications is enhancing service delivery in harsh environmental conditions. Technological innovations such as low-power satellite modems, compact MSS terminals, and advanced beamforming capabilities are reshaping operational efficiency in the Mobile Satellite Services (MSS) Market. Regulatory frameworks supporting emergency communication networks and safety standards in aviation and maritime sectors are propelling adoption globally. Regionally, Asia-Pacific and Latin America are showing promising growth in consumption patterns, with government-backed rural connectivity initiatives and increasing adoption in oil and gas operations. Emerging trends include the use of AI-powered network management within MSS platforms, IoT integration, and hybrid satellite-terrestrial communication solutions, which are shaping the market’s future outlook for mission-critical communications.

Artificial intelligence is significantly transforming the Mobile Satellite Services (MSS) Market by enhancing operational efficiency, improving bandwidth utilization, and streamlining ground station management for satellite-based mobile communications. Through AI-powered predictive maintenance, service providers within the Mobile Satellite Services (MSS) Market can now reduce downtime and extend the operational life of mobile satellite terminals, ensuring continuous service availability for mission-critical operations in maritime and disaster management environments. AI algorithms optimize dynamic bandwidth allocation and load balancing across MSS networks, addressing latency and congestion issues during peak demand in remote regions.

Additionally, AI-driven signal processing within the Mobile Satellite Services (MSS) Market allows for improved interference detection and real-time correction, resulting in enhanced voice and data communication quality. By integrating AI with mobile satellite IoT services, the MSS sector can enable automated monitoring of assets in hard-to-reach locations, thus reducing manual intervention and operational expenses while enhancing safety. AI models also improve route optimization for maritime and aviation sectors utilizing MSS by dynamically adjusting communication parameters for weather and mobility conditions. In defense applications within the Mobile Satellite Services (MSS) Market, AI enables advanced encryption and anomaly detection to strengthen secure communication frameworks. Collectively, these AI transformations are reinforcing the MSS market’s capabilities to deliver high-quality, low-latency, and reliable connectivity, supporting industries with real-time situational awareness and uninterrupted mobile satellite communication in challenging environments.

“In April 2025, a leading global MSS provider implemented an AI-based network management platform that reduced signal latency by 22% and improved bandwidth utilization efficiency by 31% across its L-band mobile satellite service networks, optimizing real-time data transmission for maritime customers.”

The Mobile Satellite Services (MSS) Market is evolving rapidly with rising demand for uninterrupted connectivity in maritime, aviation, and emergency response sectors. The market dynamics are shaped by advancements in low Earth orbit (LEO) satellite constellations, enhancing real-time data transfer and reducing latency for critical communications. Growing integration of IoT with MSS platforms is improving asset tracking in remote oil and gas operations and supporting environmental monitoring initiatives globally. The adoption of hybrid MSS-terrestrial systems is gaining momentum, providing seamless transitions between networks to ensure consistent connectivity. Regulatory encouragement for satellite-based emergency communications and government investments in rural and disaster-prone region connectivity are positively influencing the Mobile Satellite Services (MSS) Market. Technological developments, including miniaturized MSS terminals and advanced waveform technologies, are further strengthening market competitiveness while ensuring reliable coverage under harsh weather conditions.

Rising security concerns and the need for secure, real-time communication in defense and maritime operations are significant drivers for the Mobile Satellite Services (MSS) Market. Governments and defense agencies are deploying MSS for command, control, and surveillance missions in remote territories where terrestrial networks are inadequate. In the maritime sector, MSS supports vessel tracking, weather monitoring, and emergency response capabilities, which are essential for operational safety across global shipping lanes. The growing frequency of maritime trade and the need to comply with international safety regulations are increasing the adoption of MSS terminals for reliable connectivity. The increasing application of MSS in UAV operations and border surveillance further amplifies demand, positioning the Mobile Satellite Services (MSS) Market as a critical enabler for defense and maritime stakeholders.

Spectrum allocation limitations and complex regulatory frameworks across different countries pose a restraint to the Mobile Satellite Services (MSS) Market. The MSS industry requires dedicated spectrum bands, including L-band and S-band, which are often subject to national allocation disputes and delays, hindering the deployment of new services. Regulatory compliance costs related to satellite licensing, coordination with terrestrial operators to avoid interference, and adherence to cross-border spectrum usage policies add layers of operational challenges for MSS providers. Variability in data privacy laws and cybersecurity standards across regions further complicates service delivery and increases administrative overheads, slowing down potential market expansion despite technological readiness within the Mobile Satellite Services (MSS) Market.

The integration of the Mobile Satellite Services (MSS) Market with IoT and smart infrastructure development initiatives presents substantial opportunities for future growth. MSS enables connectivity in regions lacking terrestrial networks, supporting IoT applications such as remote asset monitoring in energy, agriculture, and environmental sectors. The deployment of smart grids, precision agriculture solutions, and connected logistics in rural and hard-to-reach locations benefits from MSS-enabled IoT connectivity, ensuring real-time data collection and operational efficiency. National governments and enterprises focusing on building resilient digital infrastructure for disaster management and environmental monitoring are increasingly relying on MSS to complement terrestrial systems, providing a strong growth runway for MSS providers globally.

High deployment and operational costs remain a key challenge for the Mobile Satellite Services (MSS) Market, impacting affordability and scalability, particularly in developing regions. Establishing satellite ground stations, maintaining network infrastructure, and launching new satellites require substantial capital investments, limiting market participation to a few large players. Additionally, the costs associated with user equipment such as mobile satellite terminals and their ongoing maintenance can deter widespread adoption among small and medium-sized enterprises. Operational costs for spectrum licensing and regulatory compliance add to the financial burden for MSS operators. These high expenses create a barrier for market expansion and the deployment of MSS solutions in cost-sensitive markets, despite the rising demand for reliable satellite-based mobile communications.

• Expansion of Low Earth Orbit (LEO) Satellite Constellations: The deployment of LEO satellite constellations is driving significant advancements in the Mobile Satellite Services (MSS) market, reducing latency for real-time data transfer across maritime, aviation, and defense applications. Operators have added over 800 LEO satellites in the last year to improve signal reliability for critical communication services in remote and underserved regions, enhancing user experiences with consistent connectivity.

• Integration with IoT Platforms for Asset Tracking: The integration of MSS with IoT platforms is facilitating seamless asset tracking across harsh terrains, including mining and oil and gas operations. Over 65% of new MSS terminals manufactured in 2024 included IoT compatibility features, providing real-time monitoring and predictive maintenance capabilities for critical assets operating in off-grid environments while reducing manual intervention and operational risks.

• Miniaturization of MSS Terminals: The Mobile Satellite Services (MSS) market is experiencing a trend toward compact and lightweight terminal development, supporting portability and easy deployment for field operations. New MSS terminals launched in 2025 weigh 40% less than earlier models while providing the same bandwidth efficiency, allowing emergency response teams and remote field operatives to maintain stable satellite connections during mission-critical operations.

• Advanced Signal Processing and Beamforming: Innovations in signal processing and adaptive beamforming technologies are enhancing bandwidth utilization within the Mobile Satellite Services (MSS) market. Newly introduced MSS systems in 2025 reported a 28% improvement in interference mitigation and signal clarity for users operating in congested or challenging weather environments, strengthening the reliability of satellite communications for maritime and aviation safety communications.

The Mobile Satellite Services (MSS) market is segmented by type, application, and end-user, each segment addressing specific operational and strategic demands across global industries. Types include land, maritime, aeronautical, and handheld MSS, each catering to distinct operational environments and communication needs. Applications range from emergency response and maritime safety to defense communications and remote asset monitoring, ensuring MSS remains a critical enabler of global connectivity in non-terrestrial environments. Key end-users include government agencies, maritime operators, aviation stakeholders, and energy sector players leveraging MSS for reliable data and voice communications in off-grid locations. Market segmentation reflects growing technological diversification within MSS offerings, aligned with customer demand for low-latency, reliable, and mission-critical communications across varied environments.

Land Mobile Satellite Services represent the leading type within the MSS market, supporting transportation, logistics, and emergency services with stable satellite-based communications in remote areas and during disaster scenarios. The fastest-growing type is Maritime MSS, driven by increased international trade activities and the enforcement of maritime safety regulations requiring vessel tracking and emergency communication readiness at sea. Aeronautical MSS maintains its relevance for in-flight connectivity and cockpit communications, with rising adoption across commercial aviation and defense aviation sectors seeking secure and continuous satellite links. Handheld MSS devices, though occupying a niche space, provide essential communications for field teams and adventurers in extreme environments, ensuring that all operational landscapes have MSS solutions suited to their unique requirements.

Emergency response and disaster management applications lead the Mobile Satellite Services (MSS) market, providing first responders and humanitarian agencies with critical communication tools when terrestrial networks fail. Maritime safety applications are the fastest-growing segment, supported by global initiatives to enhance vessel monitoring and improve crew safety in international waters through real-time satellite connectivity. Defense communication remains a consistent application area, with MSS supporting tactical operations, surveillance missions, and secure command communications. Additionally, asset monitoring in the energy and mining sectors, along with environmental monitoring and scientific exploration, leverages MSS to collect real-time data from inaccessible regions, ensuring informed operational decisions in diverse industries.

Government agencies are the leading end-users in the Mobile Satellite Services (MSS) market, utilizing satellite-based communications for border management, emergency response, and public safety operations in regions lacking reliable terrestrial infrastructure. The fastest-growing end-user category is the maritime industry, with shipping companies and offshore operators expanding MSS adoption to improve vessel tracking, operational safety, and compliance with international maritime safety standards. The aviation sector continues to utilize MSS for in-flight connectivity and cockpit communications, while energy sector operators rely on MSS for remote monitoring of assets and pipelines. Research organizations and NGOs also use MSS for field operations, wildlife monitoring, and data collection in remote regions, contributing to the market’s diverse end-user landscape.

North America accounted for the largest market share at 37.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The Mobile Satellite Services (MSS) market exhibits a dynamic regional landscape shaped by defense modernization, maritime safety requirements, and the adoption of IoT-enabled satellite communications across remote industrial operations. North America’s strong position reflects extensive utilization in aviation and public safety networks, while Asia-Pacific’s growth is driven by government-backed connectivity programs, expanding oil and gas activities, and increased maritime trade in the South China Sea and Indian Ocean. Europe remains a critical contributor, focusing on advanced MSS applications in environmental monitoring and aviation safety compliance. South America and the Middle East & Africa are emerging with notable demand for MSS in energy and mining, driven by the need for reliable off-grid communications.

Steady Expansion Driven by Defense and Emergency Communication Integration

The Mobile Satellite Services (MSS) market in this region held a 37.8% market share in 2024, driven by high adoption in defense, public safety, and maritime sectors requiring reliable off-grid connectivity. Key industries fueling demand include government emergency response agencies, aviation operators, and offshore energy operations prioritizing MSS for mission-critical communications. Notable regulatory support, such as spectrum allocation streamlining for MSS networks, has enabled faster deployment of L-band and S-band services across the region. Technological advancements, including AI-enhanced signal processing and miniaturized MSS terminals, are further strengthening the MSS market, allowing emergency services and field operations to maintain continuous satellite connectivity during natural disasters, severe weather, and high-risk missions across rural and coastal territories.

Growth Accelerates with Sustainability Initiatives and Maritime Safety Standards

The Mobile Satellite Services (MSS) market in this region represented 26.5% of the global volume in 2024, with significant contributions from Germany, the UK, and France. Maritime safety regulations and environmental monitoring initiatives are key drivers as the region enforces stringent compliance requirements for vessel tracking and disaster preparedness. Regulatory bodies across Europe have supported advanced MSS integration into aviation and maritime operations, ensuring reliable communication during cross-border activities. The adoption of emerging technologies such as LEO satellite services and IoT-enabled MSS solutions is advancing rapidly, with ports, coastguards, and environmental agencies leveraging MSS to enhance real-time monitoring and operational safety, aligning with Europe’s sustainability and digital transformation goals within the Mobile Satellite Services (MSS) market.

Strong Momentum with Expanding Maritime and Remote Connectivity Demand

The Mobile Satellite Services (MSS) market in this region ranked highest in growth momentum in 2024, driven by consumption in China, India, and Japan. Expanding offshore energy operations and maritime trade routes across the Indian Ocean and South China Sea have created a consistent demand for reliable MSS networks. Infrastructure trends show increased investment in MSS-enabled IoT monitoring for environmental and industrial applications, including mining and agriculture in remote areas. Technological innovation hubs in the region are fostering advanced MSS solutions with improved bandwidth efficiency and hybrid satellite-terrestrial connectivity. This has positioned the Mobile Satellite Services (MSS) market to serve both government connectivity initiatives and industrial applications, improving operational resilience across the Asia-Pacific.

Enhanced Adoption Across Energy and Resource Management Sectors

The Mobile Satellite Services (MSS) market in this region is witnessing growth, with Brazil and Argentina leading demand, collectively contributing to 7.3% of the global MSS volume in 2024. The region’s reliance on MSS solutions for managing oil, gas, and mining operations across remote areas underpins consistent market expansion. Infrastructure development trends highlight the integration of MSS into emergency preparedness and environmental monitoring frameworks in countries with high climate-related risks. Government incentives, such as tax reductions for satellite communication services and collaborative trade policies for MSS equipment imports, are supporting wider adoption. The Mobile Satellite Services (MSS) market here benefits from growing awareness of the need for reliable, off-grid communications to improve operational efficiency across critical industries.

Growth Supported by Oil & Gas and Construction Sectors

The Mobile Satellite Services (MSS) market in this region is advancing steadily, supported by rising demand in the oil and gas and construction sectors across major countries like the UAE and South Africa. Regional demand trends show increasing utilization of MSS for pipeline monitoring, field operations, and construction site management where terrestrial connectivity remains unreliable. Technological modernization, including the deployment of compact MSS terminals and AI-driven bandwidth management, is enhancing operational resilience in harsh environments. Local regulations that encourage private investment in satellite services and trade partnerships for MSS infrastructure are accelerating the adoption of Mobile Satellite Services (MSS) across mission-critical sectors, ensuring reliable connectivity in regions facing geographic and infrastructural challenges.

United States (37.8%)

High production capacity and extensive government and defense sector demand sustain the United States’ leadership in the Mobile Satellite Services (MSS) market.

China (18.4%)

Strong end-user demand across maritime and energy sectors combined with government-backed connectivity initiatives drive China’s prominent position in the Mobile Satellite Services (MSS) market.

The Mobile Satellite Services (MSS) market maintains a competitive environment with over 35 active global and regional players offering specialized MSS solutions across land, maritime, aeronautical, and handheld segments. Competition is shaped by advancements in compact terminal development, LEO satellite deployment, and AI-enabled bandwidth optimization technologies. Several providers have engaged in strategic partnerships to integrate MSS with IoT platforms for real-time asset monitoring and emergency response applications in remote regions. In the past year, over eight notable product launches in L-band and S-band services have expanded operational capabilities for maritime and aviation sectors, while mergers and collaborative agreements with satellite manufacturers have strengthened supply chain reliability. The market also witnesses competition around low-latency service delivery, with players innovating on advanced signal processing and adaptive beamforming to reduce interference and improve communication stability under challenging environmental conditions. These trends, combined with continuous investment in expanding satellite fleets and enhancing ground infrastructure, are reshaping the competitive dynamics within the Mobile Satellite Services (MSS) market globally.

Inmarsat

Iridium Communications

Globalstar

Thuraya Telecommunications

Orbcomm

EchoStar Mobile

Intelsat

SES S.A.

Hughes Network Systems

Viasat

Technological advancements are significantly shaping the Mobile Satellite Services (MSS) market, enabling enhanced connectivity, efficiency, and operational resilience across critical sectors. The deployment of Low Earth Orbit (LEO) satellite constellations has notably reduced latency for real-time data communications, with over 900 new LEO satellites integrated into MSS networks by the end of 2024 to support low-latency services for maritime, aviation, and emergency response operations. Advanced signal processing and adaptive beamforming technologies within MSS platforms have improved bandwidth utilization, with systems reporting a 30% increase in interference mitigation, resulting in higher data throughput and stable connectivity under adverse weather and dense user environments.

The integration of MSS with IoT-enabled asset tracking solutions has accelerated, with over 68% of new MSS terminals offering IoT compatibility, allowing for real-time monitoring and predictive maintenance across remote oil, gas, and mining sites. Compact and lightweight MSS terminal innovations, reducing weight by up to 35% while maintaining high data rates, are enhancing field deployability for disaster response and defense sectors. Additionally, AI-enabled network management within MSS platforms is optimizing bandwidth allocation, dynamic routing, and predictive maintenance, ensuring minimal downtime and improving service quality for critical users. Collectively, these technologies are transforming the MSS market’s capabilities to deliver secure, reliable, and efficient mobile satellite communications globally.

• In February 2023, Iridium launched its Certus 100 mid-band service, providing a compact, low-power MSS solution supporting weather-resilient connectivity for maritime and aviation operators with data speeds up to 88 Kbps, enhancing real-time tracking and safety communications in remote operations.

• In July 2023, Globalstar deployed additional satellites to expand its MSS capacity, increasing network coverage and enhancing signal reliability across North America and parts of Europe, addressing higher demand from maritime, energy, and emergency service users.

• In March 2024, Inmarsat completed testing of its next-generation L-band MSS terminals with integrated IoT support, reducing device weight by 30% while enabling advanced tracking and environmental monitoring in harsh remote environments, strengthening operational resilience for field users.

• In May 2024, Thuraya announced the rollout of its new MSS handheld terminals featuring AI-powered signal optimization, reducing latency by 18% and improving voice and data clarity for humanitarian teams and disaster response units operating in off-grid regions.

The Mobile Satellite Services (MSS) Market Report comprehensively covers the technological, regional, and application-based dimensions of the MSS industry, providing decision-makers with actionable insights for strategic planning and investment. The report analyzes MSS across key segments, including land, maritime, aeronautical, and handheld services, reflecting the diverse operational needs of industries requiring reliable off-grid connectivity. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional consumption patterns and technological adoption trends across maritime trade, aviation safety, defense operations, and emergency response sectors.

The report evaluates the role of MSS in facilitating IoT-based asset monitoring, predictive maintenance, and disaster management across industries operating in harsh and remote environments. It details technological advancements, including the deployment of LEO satellite constellations, advanced signal processing, compact terminal development, and AI-enabled bandwidth management, which are transforming service delivery in the MSS market. The scope also includes emerging and niche segments, such as environmental monitoring, humanitarian field communications, and smart infrastructure applications, highlighting the MSS market’s evolving role in supporting mission-critical communications globally. This report serves as a guide for stakeholders to navigate growth opportunities, operational challenges, and technology shifts within the Mobile Satellite Services (MSS) market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3797.15 Million |

|

Market Revenue in 2032 |

USD 5277.15 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Inmarsat, Iridium Communications, Globalstar, Thuraya Telecommunications, Orbcomm, EchoStar Mobile, Intelsat, SES S.A., Hughes Network Systems, Viasat |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |