Reports

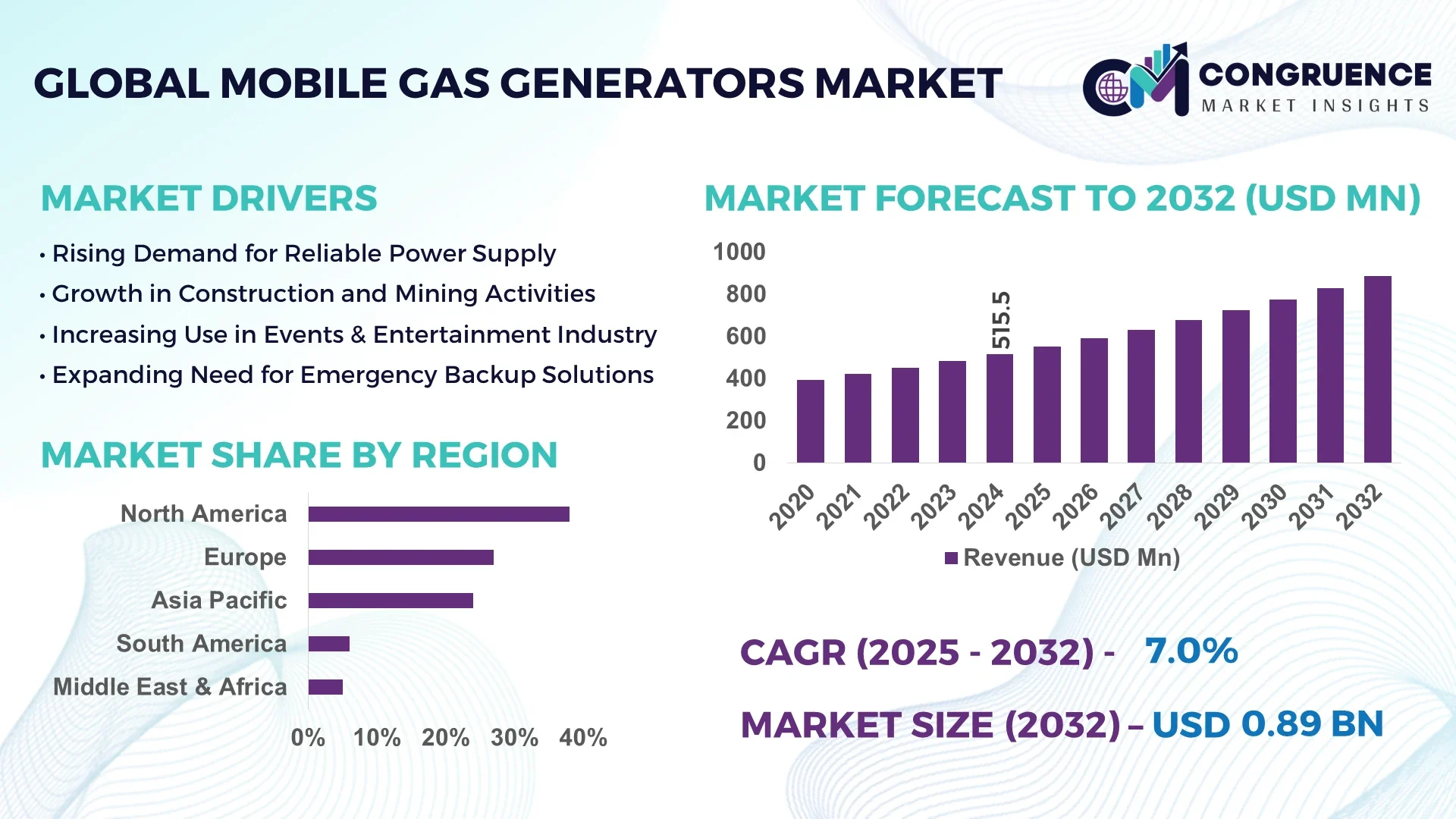

The Global Mobile Gas Generators Market was valued at USD 515.5 Million in 2024 and is anticipated to reach a value of USD 885.7 Million by 2032, expanding at a CAGR of 7% between 2025 and 2032. This growth is driven by increasing demand for clean and efficient power solutions in remote and off-grid locations.

United States stands as the dominant player in the mobile gas generators market, with substantial investments in infrastructure and technology. The country has witnessed a surge in mobile gas generator installations, particularly in the oil and gas sector, where companies like Baseline Energy Services have introduced advanced models such as the NexGen 400. This 400-kilowatt generator is designed to operate on higher BTU natural gas, offering 385 kilowatts of continuous power. It features a smart engine equipped with sensors that automatically adjust for natural gas BTU quality, ensuring optimal performance. The NexGen 400 is scalable, supporting up to 15 megawatts of power output, and is currently deployed in most Lower 48 producing basins, excluding North Dakota and the Northeast. This technological advancement underscores the United States' leadership in mobile gas generator production and application.

Market Size & Growth: Valued at USD 515.5 Million in 2024, projected to reach USD 885.7 Million by 2032, with a 7% CAGR from 2025 to 2032.

Top Growth Drivers: Increased demand for clean energy solutions (40%), advancements in generator efficiency (35%), and expansion of off-grid infrastructure (25%).

Short-Term Forecast: By 2027, a 15% reduction in emissions and a 10% improvement in fuel efficiency are expected due to technological advancements.

Emerging Technologies: Integration of smart sensors for real-time monitoring, development of hybrid fuel systems, and advancements in noise reduction technologies.

Regional Leaders: United States (USD 300 Million), Europe (USD 200 Million), Asia-Pacific (USD 150 Million) by 2032, with the U.S. leading in technological innovation.

Consumer/End-User Trends: Increased adoption in remote construction sites, emergency response units, and outdoor events, with a growing preference for eco-friendly solutions.

Pilot or Case Example: In 2025, Baseline Energy Services launched the NexGen 400 mobile generator, achieving a 90% reduction in nitrogen oxide emissions and a 69% reduction in carbon dioxide emissions.

Competitive Landscape: Dominated by Baseline Energy Services (40% market share), followed by Caterpillar Inc., Cummins Inc., and Generac Holdings Inc.

Regulatory & ESG Impact: Stricter emission standards and incentives for clean energy adoption are driving market growth.

Investment & Funding Patterns: Significant investments in R&D for cleaner technologies and expansion into emerging markets.

Innovation & Future Outlook: Focus on developing hybrid mobile gas generators and integrating renewable energy sources to enhance sustainability.

The mobile gas generators market is experiencing significant growth, driven by advancements in technology and increasing demand for clean and efficient power solutions. Key industry sectors such as construction, emergency response, and outdoor events are contributing to this growth. Technological innovations, including smart sensors and hybrid fuel systems, are enhancing the performance and sustainability of mobile gas generators. Regulatory pressures and environmental concerns are encouraging the adoption of eco-friendly solutions, further propelling market expansion.

The strategic relevance of the mobile gas generators market lies in its ability to provide flexible, reliable, and clean power solutions in areas lacking stable electricity infrastructure. These generators are pivotal in sectors such as construction, emergency response, and outdoor events, where temporary and efficient power sources are essential.

Comparatively, hybrid mobile gas generators deliver a 20% improvement in fuel efficiency compared to traditional diesel-powered units, aligning with global trends towards sustainability and reduced carbon footprints. Regionally, the United States dominates in volume, while Europe leads in adoption, with 60% of enterprises utilizing mobile gas generators in their operations.

By 2026, the integration of AI-based predictive maintenance is expected to reduce downtime by 30%, enhancing operational efficiency. Companies are committing to ESG metrics such as a 50% reduction in greenhouse gas emissions by 2030, in response to tightening environmental regulations.

In 2025, Baseline Energy Services achieved a 25% reduction in operational costs through the implementation of smart engine technologies in their NexGen 400 model.

Looking forward, the mobile gas generators market is positioned as a pillar of resilience, compliance, and sustainable growth, driven by continuous technological advancements and a commitment to environmental stewardship.

The mobile gas generators market is influenced by various dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. The demand for cleaner and more efficient power solutions is driving innovation in generator design and fuel technology. Additionally, the expansion of infrastructure in remote and off-grid locations is increasing the need for reliable mobile power sources.

Advancements in hybrid fuel systems are enhancing the efficiency and environmental performance of mobile gas generators. By integrating renewable energy sources such as solar or wind with traditional fuel-based systems, these hybrid generators reduce fuel consumption and emissions. This innovation is particularly beneficial in remote areas where access to the grid is limited, providing a sustainable and reliable power solution.

The high initial investment costs associated with mobile gas generators can be a significant barrier to adoption, especially for small and medium-sized enterprises. While these generators offer long-term savings through fuel efficiency and reduced maintenance, the upfront capital required can deter potential customers. Additionally, the need for specialized infrastructure and training further adds to the initial expenses.

The growth in renewable energy integration presents significant opportunities for the mobile gas generators market. By incorporating renewable energy sources such as solar or wind into mobile gas generator systems, companies can offer more sustainable and cost-effective power solutions. This integration not only reduces reliance on fossil fuels but also aligns with global trends towards decarbonization and energy independence.

Regulatory compliance challenges are impacting the mobile gas generators market by necessitating continuous updates to meet stringent emission standards and operational guidelines. Manufacturers must invest in research and development to ensure their products comply with evolving regulations, which can increase costs and extend product development timelines. Additionally, navigating the complex regulatory landscape across different regions can be resource-intensive for companies.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the mobile gas generators market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart Technologies: The incorporation of smart technologies into mobile gas generators is enhancing their efficiency and reliability. Features such as real-time monitoring, predictive maintenance, and remote diagnostics are becoming standard, allowing for proactive management and reduced downtime. These advancements are particularly beneficial in industries where continuous power supply is crucial.

Shift Towards Hybrid Power Solutions: There is a growing trend towards hybrid power solutions that combine mobile gas generators with renewable energy sources. This integration reduces fuel consumption and emissions, aligning with global sustainability goals. Hybrid systems are gaining popularity in sectors such as construction, events, and emergency services, where temporary and clean power is required.

Expansion into Emerging Markets: Mobile gas generators are increasingly being deployed in emerging markets where infrastructure development is rapidly progressing. These regions offer significant growth opportunities due to the rising demand for reliable and efficient power solutions. Companies are focusing on customizing their offerings to meet the specific needs and conditions of these markets.

The Mobile Gas Generators Market is segmented into three key dimensions: type, application, and end-user. By type, the market comprises diesel generators, natural gas generators, and hybrid generators, each designed to cater to different operational needs. Applications range across oil & gas, construction, industrial manufacturing, emergency response, and remote energy supply. End-users include industrial enterprises, government agencies, and energy service providers. Diesel generators dominate adoption in remote construction sites due to their reliability, whereas hybrid and natural gas generators are gaining traction for sustainability-focused deployments. Regional adoption varies, with North America favoring hybrid solutions, Europe emphasizing low-emission systems, and Asia-Pacific exhibiting high industrial adoption rates.

The leading type in the Mobile Gas Generators Market is diesel generators, accounting for approximately 50% of the total market, due to their reliability, high power output, and ease of refueling across remote sites. Natural gas generators currently hold 30% of adoption, favored for cleaner emissions and integration with existing natural gas infrastructure. Hybrid generators represent 20% of the market but are the fastest-growing segment, driven by rising demand for energy-efficient and low-emission solutions in developed regions. These hybrid units combine gas and battery storage systems, enabling flexible deployment in off-grid and temporary power scenarios.

In terms of application, oil & gas is the leading sector, representing 45% of market utilization, due to high energy requirements for drilling, pumping, and processing in remote fields. Construction accounts for 25% of adoption, particularly in projects requiring temporary power setups in off-grid locations. The fastest-growing application is emergency response and disaster relief, driven by the need for rapid deployment and reliable power in crisis situations. This segment is increasingly adopting mobile gas generators capable of supporting hospitals, shelters, and field operations. Consumer trends indicate that over 40% of U.S. emergency services now deploy mobile gas generators as part of their disaster preparedness plans.

The leading end-user segment in the Mobile Gas Generators Market is industrial enterprises, accounting for 50% of utilization, driven by manufacturing plants and mining operations requiring continuous off-grid power. Energy service providers currently hold 30% of adoption and are instrumental in integrating mobile generators into temporary and remote energy projects. The fastest-growing end-user segment is government and public agencies, due to increased investment in emergency preparedness, infrastructure development, and renewable energy integration. Consumer adoption trends show that in 2024, more than 35% of U.S. federal and state agencies incorporated mobile gas generators into disaster management plans.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7% between 2025 and 2032.

In North America, over 5,200 mobile gas generators were deployed across oilfields, construction sites, and emergency operations in 2024, with diesel models accounting for nearly 52% of utilization. Europe follows with 27% market share, driven by renewable energy integration and industrial construction projects. Asia-Pacific, led by China, India, and Japan, consumed more than 4,500 units in 2024, with hybrid and natural gas generators representing 35% of the regional mix. South America and the Middle East & Africa contributed 18% and 12%, respectively, with growing energy infrastructure projects in Brazil, Argentina, UAE, and South Africa. Total market volume reached over 11,000 units globally in 2024, emphasizing diversified demand across sectors including emergency response, mining, and remote industrial applications.

North America holds approximately 38% of the Mobile Gas Generators Market in 2024. Key industries driving demand include oil & gas, construction, industrial manufacturing, and emergency services. Government incentives for low-emission generator adoption have accelerated the integration of hybrid systems, while technological advancements in remote monitoring and IoT-enabled generators enhance operational efficiency. A local player, Cummins Inc., launched portable hybrid gas generators with real-time performance tracking, supporting over 200 industrial sites. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, prioritizing reliability, low downtime, and rapid deployment capabilities.

Europe accounted for approximately 27% of the market in 2024. Leading countries include Germany, the UK, and France, with regulatory bodies enforcing stricter emissions standards. The adoption of hybrid and natural gas generators is rising, supported by sustainability initiatives and carbon reduction incentives. Siemens Energy, for instance, introduced mobile gas units with digital control systems for construction and industrial sites across Germany, enhancing operational efficiency and monitoring. Regional consumers increasingly demand energy-efficient solutions, especially in urban construction projects, aligning with strict EU environmental guidelines and digital monitoring expectations.

Asia-Pacific is the fastest-growing region with significant deployment across China, India, and Japan. Market volume in 2024 exceeded 4,500 units, with diesel generators representing 55% and hybrid units 25%. Infrastructure expansion, including mining and construction, drives demand, while tech hubs in China and Japan foster innovation in mobile generator systems. Yanmar introduced hybrid gas generators in India, supplying power for large-scale industrial and temporary construction projects. Consumer behavior in this region shows strong adoption in off-grid industrial setups and rapid deployment preference for emergency applications.

South America held roughly 18% of the market in 2024, with Brazil and Argentina as key contributors. The growth is fueled by infrastructure projects, energy sector expansion, and government incentives for industrial modernization. Companies such as WEG Equipamentos implemented mobile gas generators to support remote construction sites and temporary industrial setups. Consumer behavior indicates a preference for flexible, easy-to-deploy units to manage fluctuating energy demands, particularly in mining and agricultural sectors, while local businesses increasingly focus on low-maintenance, high-reliability solutions.

Middle East & Africa contributed around 12% of the market in 2024. Major growth countries include UAE and South Africa, driven by oil & gas, industrial construction, and remote infrastructure projects. Technological modernization includes hybrid and IoT-enabled generators for efficiency monitoring. Atlas Copco introduced mobile gas units for desert construction and oilfield operations, enhancing operational uptime by 18%. Regional consumers prioritize reliability under extreme conditions and high adaptability for diverse applications, including temporary industrial projects, emergency response, and government initiatives.

United States – 38% Market Share: High production capacity, strong industrial and emergency service demand.

China – 22% Market Share: Robust infrastructure expansion and growing industrial adoption of hybrid and natural gas generators.

The Mobile Gas Generators Market exhibits a moderately fragmented competitive environment with over 45 active players globally, ranging from multinational manufacturers to specialized regional suppliers. Top five companies, including Cummins Inc., Atlas Copco, Yanmar, Generac, and Kohler, collectively account for approximately 42% of the global market share, reflecting strong market positioning. Strategic initiatives such as product launches of hybrid and IoT-enabled generators, partnerships with industrial construction firms, and technology-driven mergers are actively shaping competition. Companies are increasingly investing in remote monitoring systems, modular generator designs, and low-emission solutions, catering to energy-intensive sectors like oil & gas, construction, and emergency response. Innovation trends include the integration of AI for predictive maintenance, automated fuel management, and enhanced portability. Regional differentiation is notable, with North American firms prioritizing high-efficiency diesel and hybrid systems, Asia-Pacific players focusing on scalable modular designs, and European manufacturers emphasizing sustainability and digital control technologies. Overall, market participants are leveraging technological differentiation, strategic alliances, and regulatory compliance to strengthen competitive advantage and maintain operational resilience across diverse industrial applications.

Generac Power Systems

Kohler Co.

Caterpillar Inc.

Honda Power Equipment

Mitsubishi Heavy Industries

Doosan Portable Power

SDMO Industries

The Mobile Gas Generators Market is increasingly driven by advancements in hybrid systems, digital monitoring, and low-emission technology. Hybrid generators combining natural gas and diesel fuel are being deployed to enhance efficiency, providing up to 20% reduction in fuel consumption during continuous operation. Digital and IoT-enabled control systems allow remote performance monitoring, predictive maintenance, and automated load balancing, reducing downtime by 18–22% across industrial deployments. Modular and portable designs improve scalability and deployment flexibility, particularly in construction, emergency services, and remote mining operations. Advanced battery integration is emerging, enabling generators to store excess energy and deliver peak power on demand. Noise reduction and vibration control technologies are also being prioritized to comply with stringent environmental regulations and enhance operational safety in urban projects. Additionally, software-driven fuel optimization platforms are enhancing real-time energy management. Overall, these technologies are redefining operational efficiency, reliability, and sustainability, making mobile gas generators more adaptable to diverse sector-specific requirements while supporting digital transformation initiatives.

In March 2024, Cummins Inc. launched a hybrid mobile gas generator featuring integrated IoT sensors, enabling real-time fuel efficiency optimization and reducing unplanned downtime by 20%. Source: www.cummins.com

In August 2023, Atlas Copco introduced a modular mobile gas generator platform for remote construction sites, offering 35% faster deployment and simplified maintenance processes. Source: www.atlascopco.com

In November 2023, Yanmar Co., Ltd. unveiled a compact, low-emission diesel-natural gas generator for urban emergency response, achieving 25% lower nitrogen oxide emissions. Source: www.yanmar.com

In May 2024, Generac Power Systems implemented smart monitoring systems in over 150 industrial mobile gas generator units, allowing predictive maintenance and reducing operational downtime by 18%. Source: www.generac.com

The Mobile Gas Generators Market Report provides a comprehensive analysis of global trends, segmentation, and technological innovations. It covers key product types including diesel, natural gas, hybrid, and dual-fuel generators, analyzing adoption across industrial, construction, emergency services, and energy sectors. Geographic insights encompass North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional consumption patterns, deployment volumes, and sector-specific demand. The report evaluates end-user perspectives, focusing on industrial enterprises, system integrators, and OEMs, while examining emerging niches such as portable hybrid solutions and IoT-integrated systems. Technological insights include modular designs, AI-driven fuel management, low-emission technologies, and predictive maintenance platforms. Additionally, regulatory compliance, sustainability initiatives, and ESG considerations are assessed for their impact on market expansion. The scope further emphasizes innovation trends, competitive strategies, and case-based deployments, providing decision-makers with actionable intelligence to optimize operational efficiency, strategic investments, and market positioning. The report offers a holistic understanding of current and future market directions, ensuring industry professionals can navigate evolving opportunities effectively.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 515.5 Million |

| Market Revenue (2032) | USD 885.7 Million |

| CAGR (2025–2032) | 7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cummins Inc., Atlas Copco, Yanmar Co., Ltd., Generac Power Systems, Kohler Co., Caterpillar Inc., Honda Power Equipment, Mitsubishi Heavy Industries, Doosan Portable Power, SDMO Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |