Reports

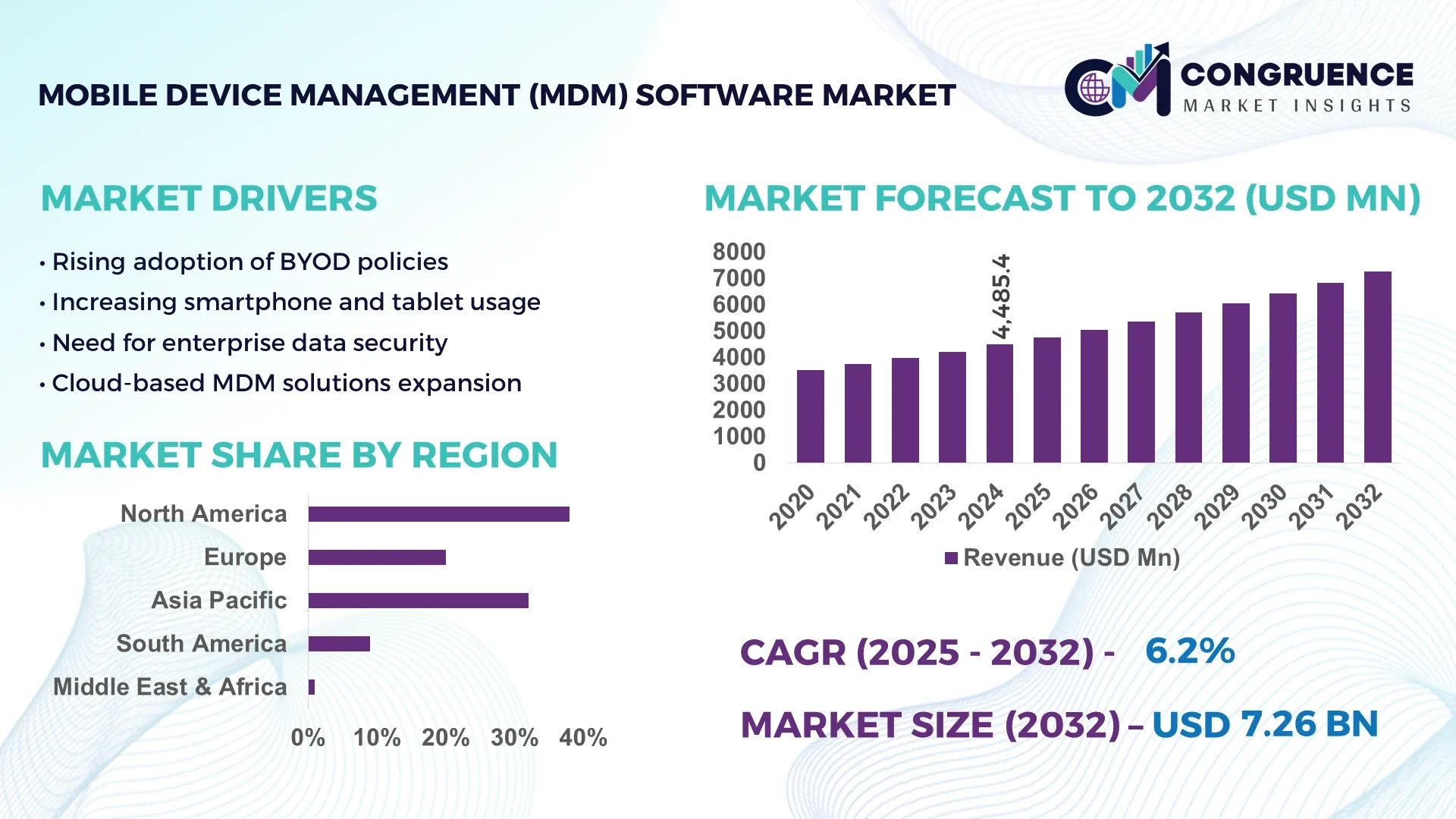

The Global Mobile Device Management (MDM) Software Market was valued at USD 4485.43 Million in 2024 and is anticipated to reach a value of USD 7257.72 Million by 2032 expanding at a CAGR of 6.2% between 2025 and 2032. This growth is fueled by rising enterprise mobility requirements and the increasing need for secure device management across diverse industries.

The United States dominates the global market with a highly advanced enterprise mobility infrastructure, strong regulatory compliance frameworks, and significant investments in AI-driven security technologies. In 2024, U.S. enterprises accounted for more than 36% of global MDM deployments, supported by high adoption of BYOD policies and rapid integration of 5G-enabled device management platforms.

Market Size & Growth: Global market valued at USD 4.49 Billion in 2024, projected to reach USD 7.26 Billion by 2032 with a CAGR of 6.2% driven by increasing mobile workforce and stringent data protection needs.

Top Growth Drivers: 40% enterprise mobile adoption growth, 35% cybersecurity enhancement demand, 25% BYOD policy expansion.

Short-Term Forecast: By 2028, enterprises are expected to achieve 30% cost reduction in IT operations and 25% improvement in device security compliance through advanced MDM solutions.

Emerging Technologies: AI-powered threat detection, predictive analytics for device health, and 5G-enabled device orchestration.

Regional Leaders: North America projected at USD 2.6 Billion by 2032 with mature enterprise mobility adoption; Europe expected at USD 1.8 Billion by 2032 with strict GDPR compliance; Asia Pacific forecasted at USD 1.2 Billion by 2032 driven by rapid digital transformation.

Consumer/End-User Trends: Accelerating enterprise integration of MDM for smartphones, tablets, and IoT endpoints to enhance data security and regulatory compliance.

Pilot or Case Example: In 2024 a multinational healthcare group deployed AI-enhanced MDM, achieving a 40% drop in device security incidents and a 30% reduction in IT support costs.

Competitive Landscape: Market leader holds about 25% share with key competitors including IBM, VMware, Citrix, Microsoft, and MobileIron driving innovation and global expansion.

Regulatory & ESG Impact: Heightened adherence to GDPR, HIPAA, and environmental sustainability standards accelerating cloud-based MDM adoption and eco-friendly device lifecycle management.

Investment & Funding Patterns: Over USD 1.3 Billion invested globally in 2024 across MDM startups and enterprise-scale deployments, reflecting strong venture funding and hybrid cloud project financing.

Innovation & Future Outlook: Integration of AI-driven automation, zero-trust security models, and unified endpoint management expected to redefine enterprise mobility strategies by 2032.

The Mobile Device Management (MDM) Software market is witnessing robust adoption across key sectors including healthcare, banking, and education, each contributing significant market share through large-scale deployments and cross-platform integration. Recent technological advancements such as unified endpoint management and cloud-native security are reshaping product innovation, while evolving data privacy regulations and eco-conscious policies drive sustainable deployment strategies. Regional consumption patterns highlight North America’s leadership, Europe’s strict compliance-based growth, and Asia Pacific’s rapid digital transformation, setting the stage for continued global expansion through 2032.

The Mobile Device Management (MDM) Software Market is strategically vital as organizations increasingly rely on mobile devices for business operations. MDM solutions facilitate secure device management, ensuring compliance with data protection regulations and enhancing operational efficiency. For instance, cloud-based MDM solutions offer scalability and remote management capabilities, reducing the need for extensive on-premise infrastructure. By 2026, the integration of Artificial Intelligence (AI) in MDM solutions is expected to improve threat detection accuracy by 30%, compared to traditional security measures. North America dominates in volume, while Europe leads in adoption with 70% of enterprises implementing MDM solutions. In 2024, a leading healthcare provider in the U.S. achieved a 40% reduction in security incidents through the adoption of AI-enhanced MDM solutions. Firms are committing to sustainability improvements such as a 20% reduction in e-waste by 2030. The MDM Software Market is poised to be a pillar of resilience, compliance, and sustainable growth, addressing the evolving challenges of enterprise mobility.

The Mobile Device Management (MDM) Software Market is experiencing significant growth driven by the increasing adoption of mobile devices in enterprises, the rise of Bring Your Own Device (BYOD) policies, and the need for enhanced security measures. Organizations are seeking solutions that provide centralized control over mobile devices, applications, and data, ensuring compliance with regulatory standards and protecting sensitive information. The shift towards cloud-based MDM solutions is also contributing to market expansion, offering scalability and cost-efficiency. As enterprises continue to embrace digital transformation, the demand for robust MDM solutions is expected to rise, fostering innovation and competition among vendors.

The surge in remote work has significantly increased the need for secure mobile device management. Organizations are deploying MDM solutions to ensure that employees can access corporate resources securely from various locations and devices. This trend has led to a higher adoption rate of MDM solutions, as businesses prioritize data security and compliance with regulatory standards. The flexibility offered by MDM solutions enables organizations to manage a diverse range of devices, ensuring consistent security policies across the enterprise.

Small and medium-sized enterprises (SMEs) often encounter challenges in adopting MDM solutions due to budget constraints and limited IT resources. The initial investment required for implementing MDM software and the ongoing maintenance costs can be prohibitive for SMEs. Additionally, the complexity of integrating MDM solutions with existing IT infrastructure can deter SMEs from adoption. Despite these challenges, the growing awareness of data security risks is prompting SMEs to explore cost-effective MDM solutions tailored to their needs.

The proliferation of Internet of Things (IoT) devices in enterprises presents a significant opportunity for the MDM Software market. As organizations deploy a multitude of IoT devices, the need for centralized management and security becomes paramount. MDM solutions can extend their capabilities to include IoT device management, providing businesses with a comprehensive approach to device security and compliance. This expansion into IoT device management opens new revenue streams for MDM vendors and addresses the growing complexity of enterprise IT environments.

Data privacy regulations such as the General Data Protection Regulation (GDPR) and the Health Insurance Portability and Accountability Act (HIPAA) impose stringent requirements on organizations regarding the handling of personal data. Compliance with these regulations necessitates the implementation of robust MDM solutions that can enforce data protection policies and provide audit trails. The complexity of adhering to diverse regulatory standards across different regions can be challenging for organizations, requiring MDM vendors to offer customizable solutions that meet specific compliance requirements.

The Mobile Device Management (MDM) Software market is segmented into types, applications, and end-users, each contributing uniquely to industry growth. Understanding these segments is essential for stakeholders to tailor solutions, optimize deployment, and target specific markets effectively. Product types, usage applications, and end-user adoption patterns are critical in shaping strategic decisions, investment priorities, and technological innovations. By analyzing these segments, businesses can identify high-potential areas, address market gaps, and align MDM offerings with evolving enterprise mobility needs.

The MDM software market is primarily divided into software and services. The software segment leads the market, accounting for over 63% of total adoption in 2024 due to its robust security features, including encryption, remote wipe, and policy enforcement capabilities. Services, encompassing professional and managed deployment support, are growing steadily as enterprises seek expert assistance to configure, implement, and maintain MDM systems efficiently. Deployment models include on-premises and cloud-based solutions, with cloud-based MDM gaining traction for its scalability, cost-effectiveness, and flexibility, particularly among SMEs.

MDM software applications span healthcare, education, finance, and retail sectors. Healthcare leads with over 40% adoption, ensuring compliance with regulations like HIPAA and protecting sensitive patient data across mobile devices. Education institutions leverage MDM to monitor devices for e-learning, enhancing classroom security and learning continuity. Finance organizations utilize MDM to secure access to critical financial systems and confidential information. Retailers increasingly deploy MDM for point-of-sale management, inventory control, and customer service enhancement. In 2024, more than 38% of enterprises globally reported piloting MDM solutions to support digital transformation initiatives.

Large enterprises dominate the MDM market, representing over 52% of adoption in 2024, driven by the need to manage extensive device fleets across multiple departments. SMEs are the fastest-growing end-user segment, motivated by increasing remote work adoption and demand for cost-effective, secure device management. Individual consumers also contribute to growth, particularly in regions with high smartphone penetration, seeking solutions for personal device security and app permission control. In 2024, over 60% of Gen Z consumers showed higher trust in brands implementing secure mobile device management.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 35.1% between 2025 and 2032.

North America’s dominance is supported by high enterprise adoption in healthcare, finance, and technology sectors, with over 50,000 corporate networks utilizing advanced MDM solutions. Asia-Pacific’s rapid growth is driven by increasing smartphone penetration, expansion of 4G/5G networks, and digital transformation initiatives across China, India, and Japan, where more than 60% of enterprises are implementing cloud-based MDM platforms.

What factors contribute to the dominance of MDM solutions in North America?

North America held a substantial share of the global MDM market in 2024, representing 38% of adoption. Key industries driving demand include healthcare, finance, and IT services, where secure mobile device management is critical. Regulatory frameworks such as HIPAA and data privacy mandates have prompted enterprises to adopt advanced MDM solutions. Technological advancements, including AI-driven threat detection and machine learning policy enforcement, are enhancing operational efficiency. Local players, such as IBM and VMware, are expanding cloud-based MDM offerings to support enterprise mobility. Regional consumer behavior shows higher adoption in healthcare and financial sectors compared to other industries.

How is Europe adapting to the evolving MDM landscape?

Europe accounted for around 20% of the global MDM market in 2024, with key markets including Germany, the UK, and France. Industries such as automotive, manufacturing, and public services are driving demand. Regulatory bodies like the European Union Agency for Cybersecurity (ENISA) have introduced initiatives to enhance cybersecurity, increasing MDM adoption. Emerging technologies including IoT and 5G integration are expanding MDM capabilities. Local players are investing in cloud-based, explainable MDM solutions to meet regulatory demands. Consumer behavior is heavily influenced by compliance requirements, with organizations prioritizing data privacy and security in all mobile deployments.

What is fueling the rapid growth of MDM solutions in Asia-Pacific?

Asia-Pacific is projected to experience the fastest growth in the MDM market, with adoption accelerating across China, India, and Japan. The region benefits from expanding digital infrastructure, 4G/5G networks, and a growing mobile workforce. Top-consuming industries include e-commerce, IT services, and manufacturing, where device security and remote management are priorities. Local companies are developing scalable, cloud-based MDM solutions to address enterprise needs. Consumer trends indicate a preference for flexible and remotely managed MDM platforms to support dynamic business operations and growing mobile AI applications.

What are the key drivers of MDM adoption in South America?

South America’s MDM market is growing, with Brazil and Argentina leading adoption. Key sectors include retail, education, and government, which increasingly rely on mobile devices for operations and service delivery. Infrastructure development and government initiatives to enhance digital connectivity support market expansion. Local MDM providers are offering tailored solutions for multi-language support and secure device management. Regional consumer behavior reflects heightened awareness of mobile security, driving enterprise and institutional adoption of MDM platforms.

How are Middle Eastern and African nations embracing MDM solutions?

Middle East & Africa are witnessing steady growth in the MDM market, with countries like UAE and South Africa leading adoption. Growth is fueled by industries such as oil & gas, construction, and government services. Technological modernization, including smart city initiatives and cloud integration, is enhancing MDM deployment. Local companies are introducing AI-enabled MDM solutions to meet regulatory and operational requirements. Consumer behavior shows increased focus on mobile security and enterprise mobility, prompting enterprises to prioritize secure, scalable MDM implementations.

United States | 38% market share | Dominance driven by strong enterprise adoption in healthcare, finance, and technology sectors, along with advanced IT infrastructure.

China | 22% market share | High adoption fueled by rapid digital transformation, extensive mobile device usage, and government-backed smart enterprise initiatives.

The Mobile Device Management (MDM) Software market exhibits a fragmented competitive environment, with over 50 active competitors globally as of 2024. The top five companies—IBM, VMware, Microsoft, Citrix, and Samsung—collectively hold approximately 23.25% of the market share, reflecting a diverse and highly competitive landscape. Strategic initiatives such as mergers, acquisitions, partnerships, and new product launches are shaping the competition. For example, Jamf acquired Identity Automation in March 2025 to enhance identity lifecycle management for shared devices, while Samsung introduced post-quantum cryptography in its Galaxy S25 devices via Knox Matrix, improving enterprise security using the ML-KEM algorithm. Innovation trends include AI-enabled device monitoring, cloud integration, and advanced threat detection, which are driving differentiation among players. Market participants are also focusing on regional expansion, niche vertical solutions, and scalable MDM offerings to capture enterprise demand in healthcare, finance, education, and government sectors.

Citrix Systems Inc.

Samsung Electronics Co., Ltd.

ManageEngine

SOTI Inc.

Hexnode Technologies Limited

BlackBerry Limited

The Mobile Device Management (MDM) Software market is witnessing rapid technological evolution that is reshaping enterprise mobility strategies. AI-powered security is being integrated into MDM platforms to analyze device behavior patterns and detect anomalies, enabling proactive threat mitigation. Zero Trust architecture is gaining traction, ensuring that all access requests are continuously verified, reducing internal and external security risks. Unified Endpoint Management (UEM) platforms are consolidating the management of smartphones, laptops, tablets, and IoT devices under a single interface, offering enterprises a holistic view of their device ecosystem. Cloud-native MDM solutions are increasing in adoption, providing scalability, remote management, and cost efficiency for organizations implementing BYOD and remote work policies. Advanced compliance tools within MDM systems facilitate adherence to regulations like GDPR, HIPAA, and CCPA through features such as encryption, remote wipe, and detailed audit trails. Integration of machine learning for predictive device management and automated policy enforcement is enhancing operational efficiency. These technological trends make MDM platforms more adaptive, secure, and aligned with modern enterprise demands, supporting continuous innovation and digital transformation initiatives.

In March 2024, Jamf acquired Identity Automation to enhance identity lifecycle management for shared devices. This strategic initiative aimed to streamline user authentication and strengthen security across enterprise and educational environments. Source: www.jamf.com

In June 2024, Samsung introduced post-quantum cryptography in its Galaxy S25 devices via Knox Matrix, using the ML-KEM algorithm. This innovation strengthens device security against emerging quantum computing threats. Source: www.samsung.com

In August 2024, VMware integrated AI-driven threat detection into its Workspace ONE platform, enabling real-time identification and mitigation of endpoint security risks across enterprise networks. Source: www.vmware.com

In November 2023, Citrix expanded its Endpoint Management solution to support Linux-based devices, catering to enterprises with diverse operating system environments and increasing device coverage. Source: www.citrix.com

The Mobile Device Management (MDM) Software Market Report provides a detailed analysis of global MDM solutions, covering key segments, regions, applications, and technologies. The report examines deployment models, including on-premises and cloud-based platforms, highlighting operational efficiency, security benefits, and adoption trends. Device types such as smartphones, tablets, laptops, and IoT endpoints are evaluated to understand enterprise management needs and sector-specific deployment strategies. Industry verticals such as healthcare, finance, education, retail, and government are analyzed for usage patterns, compliance requirements, and digital transformation initiatives. Emerging technologies like AI, machine learning, Zero Trust security, and cloud-native frameworks are explored for their impact on device management and operational optimization. Regional insights focus on North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing adoption rates, local trends, and market opportunities. The report also identifies niche segments, regulatory influences, and technological innovations that shape MDM adoption. This comprehensive coverage equips decision-makers with actionable intelligence to implement effective, secure, and future-ready device management strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4485.43 Million |

|

Market Revenue in 2032 |

USD 7257.72 Million |

|

CAGR (2025 - 2032) |

6.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, VMware Inc., Microsoft Corporation, Citrix Systems Inc., Samsung Electronics Co., Ltd., ManageEngine, SOTI Inc., Jamf Software LLC, Hexnode Technologies Limited, BlackBerry Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |