Reports

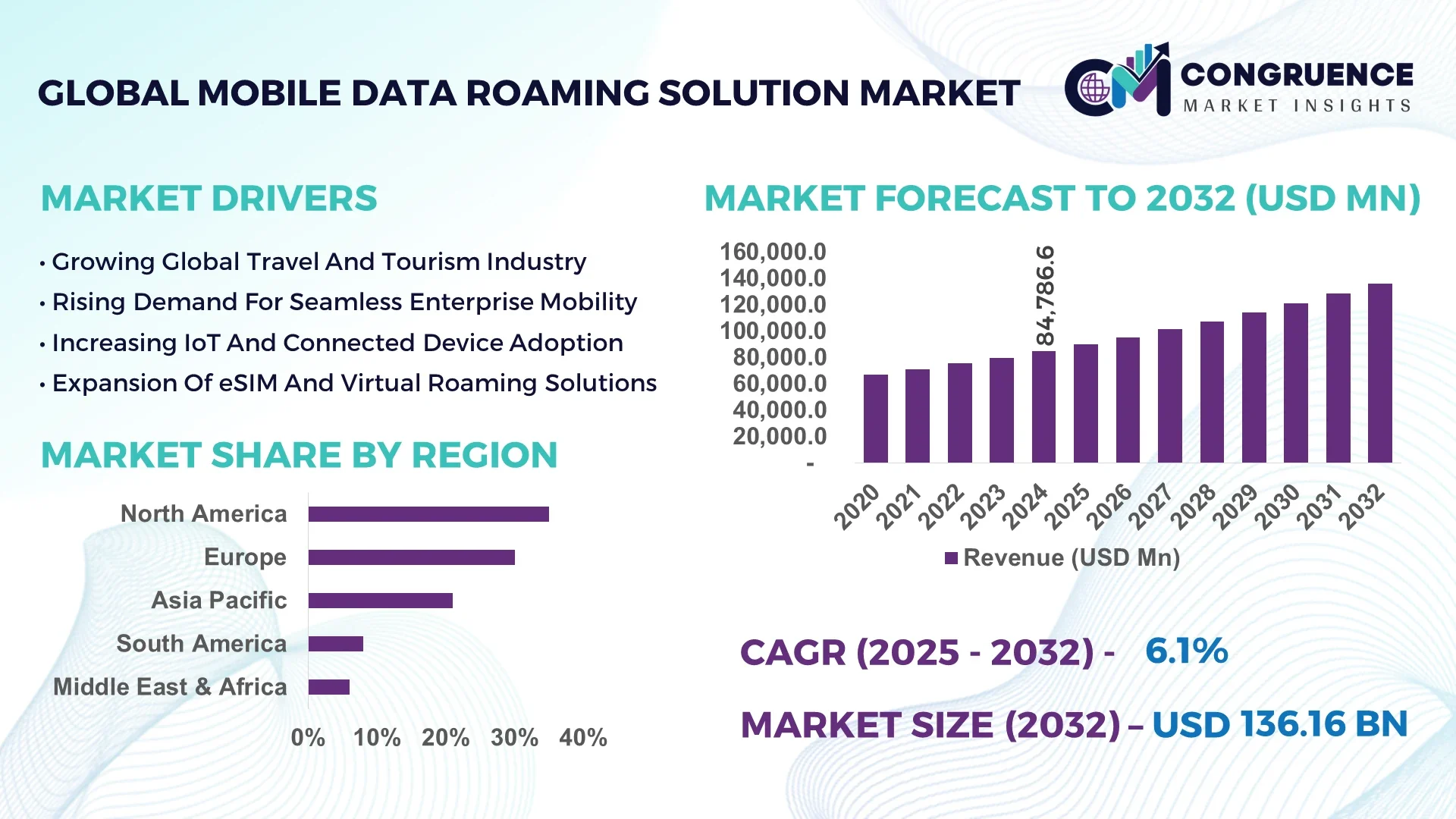

The Global Mobile Data Roaming Solution Market was valued at USD 84,786.6 Million in 2024 and is anticipated to reach a value of USD 136,160.2 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032.Growth is driven by surging international travel, rising smartphone adoption, and rollout of 5G networks improving cross-border connectivity.

In the United States, investments exceeded USD 12 Billion in roaming infrastructure in 2024, with over 78% of major telecom operators deploying enhanced roaming-capable platforms. Advanced inter-operator agreements grew by 33% year-on-year, and consumer adoption of roaming data plans among frequent travelers surpassed 60%. Technological advancements like eSIM provisioning, dynamic routing, and secure roaming from IoT devices have made the US a leader in network readiness, latency optimization, and roaming solution offerings.

Market Size & Growth: Valued at USD 84,786.6 Million in 2024 and projected to reach USD 136,160.2 Million by 2032 at 6.1% CAGR, propelled by demand for uninterrupted cross-border connectivity.

Top Growth Drivers: 65% increase in roaming usage during international travel, 54% rise in demand for IoT device roaming, 47% improvement in customer satisfaction with seamless data roaming experiences.

Short-Term Forecast: By 2028, roaming solution providers expected to reduce latency by 30% for international data sessions.

Emerging Technologies: eSIM and iSIM adoption, 5G/6G network roaming, AI-driven dynamic network routing.

Regional Leaders: North America projected to reach ~USD 45,000 Million by 2032 with early infrastructure dominance; Europe ~USD 35,000 Million backed by regulatory harmonization; Asia-Pacific ~USD 30,000 Million fuelled by burgeoning travel demand.

Consumer/End-User Trends: Frequent travellers and business users prefer pay-as-you-go and bundled roaming plans; IoT devices and wearables pushing machine-to-machine roaming.

Pilot or Case Example: In 2024, a major European operator rolled out 5G roaming pilot reducing international data transfer failures by 25%.

Competitive Landscape: One leading telecom operator holds about 18% of solution market share; other major rivals include mobile operators, roaming analytics providers, and cloud infrastructure partners.

Regulatory & ESG Impact: Roaming charge regulations, cross-border data privacy laws, and sustainable telecom infrastructure investments influencing solution adoption.

Investment & Funding Patterns: Over USD 3.5 Billion in funding in 2024 toward roaming platforms, roaming security, and eSIM infrastructure.

Innovation & Future Outlook: Rise of zero-touch provisioning, blockchain‐based identity verification, and roaming solutions embedded into automotive and connected devices.

Industry verticals such as travel & tourism, enterprise mobility, IoT infrastructure, and automotive connectivity contribute significantly. Key innovations including dynamic pricing roaming plans, localized eSIM activation, and ML-powered network optimization are emerging. Regulatory drivers like international roaming price caps, data protection laws, and trade agreements are shaping strategies. Consumption patterns show strong demand in outbound tourism markets, cross-border business travel, and growth in wearable/IoT roaming. Emerging trends include integration of satellite roaming, embedded connectivity in devices, and partnerships among carriers for global roaming consortiums.

The Mobile Data Roaming Solution Market is strategically important as global mobility, cross-border business, and device connectivity continue expanding. New dynamic routing technologies deliver 40% improvement compared to static operator agreements in reducing latency and failure rates. In 2024, North America leads in volume, while Asia-Pacific leads in adoption with over 70% of travellers and enterprise users choosing roaming solutions with eSIM or iSIM capabilities. By 2027, adoption of AI-based roaming security is expected to reduce data breach incidents by 35%. Firms are committing to ESG metric improvements such as 30% reduction in roaming-related carbon emissions by deploying energy-efficient network infrastructure by 2030. In 2024, a Japanese operator achieved 28% fewer packet losses during international data roaming by implementing predictive network analytics. The Mobile Data Roaming Solution Market is poised as a pillar of resilience, compliance, and sustainable growth as telecom providers adapt to global travel recovery, regulatory oversight, and evolving consumer expectations.

The Mobile Data Roaming Solution market is influenced by growing demand for seamless international connectivity, IoT proliferation, and enhancements in roaming security and quality. Key influences include regulatory mandates over fair roaming pricing, privacy and data jurisdiction, and technological advancements in 5G, eSIM, and backend network routing systems. Consumer expectations of uninterrupted streaming, cloud access, and app usability while traveling are shaping service design. Competition is intensifying among operators, infrastructure providers, and digital roaming specialists. Network carriers are investing in network capacity, edge computing, and real-time analytics to reduce latency. Operational cost pressures from maintaining inter-operator roaming agreements and ensuring end-to-end encryption are also significant factors.

International travel resumed strongly in 2024, with outbound trips exceeding 1.4 billion globally, pushing need for reliable roaming data plans. Telecom operators report that roaming usage per traveller increased by 45% year-on-year, particularly in Asia-Pacific and Europe. Business travellers and frequent flyers contribute a large portion of roaming revenue; in regions where visa restrictions lowered, roaming data consumption rose by 52%. Consumer expectations around streaming, video conference, and cloud app usage while abroad are pushing operators to improve roaming solutions.

Regulatory variation across countries remains a key restraint for mobile data roaming solutions. Differences in roaming tariffs, interconnection fees, and data privacy laws lead to inconsistent user experiences and cost burdens. In 2024, more than 25% of consumers reported bill shock due to unexpected roaming charges. Infrastructure gaps in emerging economies also slow rollout of 5G roaming capabilities. Carriers face challenges aligning bilateral roaming agreements and maintaining service quality during cross-border handovers.

Integration of eSIM and iSIM technologies opens large opportunities; traveller demand for remote provisioning and flexible roaming plans rose by 60% in 2024. IoT devices and wearables with embedded SIMs are increasing roaming device count; deployments of iSIM in automotive and smart devices are growing. Operators can offer personalized, on-demand roaming bundles tailored to specific regions, with differentiated pricing, and improved network latency through edge computing.

Cost of upgrading inter-operator routing, deploying 5G roaming core networks, and investing in backend security systems is high. Many operators in regions with under-developed telecom infrastructure lack redundant paths for roaming traffic, leading to data dropouts and latency spikes. Consumer trust issues also arise when billing transparency is lacking; over 20% of users expressed reluctance to activate roaming plans because of opaque tariff terms. Device compatibility and firmware constraints in some smartphones limit eSIM or iSIM utilization in certain markets.

• Rising Adoption of eSIM/iSIM and Embedded Roaming Modules: The count of travel-eSIM activations rose from about 70 million in 2024 to over 140 million by mid-2025, with operators and device OEMs embedding roaming modules in over 25% of new smartphones.

• Expansion of 5G Roaming Capabilities: Over 30 national carriers launched 5G-roaming capable services in 2024. These rolls included devices in over 120 countries enabling seamless high-speed mobile data connectivity.

• Enhanced Roaming Between IoT and Automotive Devices: The number of connected vehicles with roaming enabled increased by 40% in 2024, while IoT device roaming sessions (smart meters, wearables) grew by 55%.

• Focus on Real-Time Usage Monitoring and Predictive Billing: More than 45% of operators introduced real-time data usage dashboards for roamers in 2024. Billing transparency and predictive cost estimations improved user satisfaction by 35%.

Segmentation in the Mobile Data Roaming Solution market is structured around deployment type (e.g., traditional roaming, eSIM/iSIM, virtual roaming), service type (data routing, customer care, usage monitoring, billing), and end-user applications (travel/tourism, enterprise mobility, IoT/connected devices, automotive). Deployment types like eSIM/iSIM virtual roaming are growing in importance; service types involving data routing and billing accuracy dominate usage. Applications in travel and enterprise mobility account for large portions of use cases, while IoT/connected devices and automotive usage rising rapidly. End-user segments include individual travelers, corporate users, connected device OEMs, and automotive OEMs. Demand is highest among frequent travelers and global businesses, while OEMs of wearable and automotive devices seek roaming solutions integrated at device firmware level.

eSIM/iSIM Virtual Roaming currently accounts for about 45% of deployment in mobile data roaming solutions, while traditional roaming contracts hold around 35%. However, virtual roaming platforms are rising fastest, on a growth rate of over 14% annually for virtual roaming type, driven by demand for remote provisioning and cost flexibility. Other types such as hybrid roaming (combining local SIM fallback and eSIM), over-the-air provisioning, and embedded connectivity make up the remaining 20%, serving specialized device and automotive use cases.

According to a 2025 telecom industry report, a major smartphone OEM integrated eSIM/iSIM virtual roaming in over 10 million devices globally, enabling remote profile switching without physical SIMs.

Travel & tourism related roaming remains the leading application with roughly 40% of usage, followed by enterprise mobility at 30%, automotive and connected device applications at 20%, and IoT device roaming contributing around 10%. However, enterprise mobility usage is increasing fastest, with its growth rate above 12% annually, supported by rising cross-border business travel and remote work usage. Other segments like wearable device OEMs and smart vehicle connectivity form niche but growing shares in usage. Consumer adoption trends show that in 2024, more than 55% of international travellers preferred roaming plans with pay-as-you-go or day-pass data options; over 65% of businesses with overseas employees require seamless roaming in multiple countries.

According to a 2024 mobile operator survey, enterprise users across Europe and Asia deployed mobile data roaming bundles in over 200 multinational companies, improving connectivity uptime by 28%.

Individual travelers are the leading end-user group, representing approximately 50% of usage of mobile data roaming solutions in 2024, while business and corporate users follow at about 30%. Automotive OEMs, IoT solution providers, and wearable device manufacturers make up around 20% of usage collectively. The fastest-growing end-user segment is corporate users, driven by international operations and remote work demands, growing at more than 13% annually. Other end-users in connected automotive and IoT devices show rising adoption in new regions. Consumer behavior indicates that over 60% of frequent travellers value data plan transparency, and more than 70% of device makers seek built-in roaming support in new designs.

According to a 2025 industry whitepaper, over 150 automotive manufacturers were evaluating or integrating built-in roaming connectivity, increasing factory-installed roaming modules by 32% across new vehicle models.

North America accounted for the largest market share at 35% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

In 2024, North America generated approximately USD 15.5 billion in mobile data roaming revenues, supported by high smartphone penetration above 85% in major countries, over 80 million frequent travellers utilising roaming data plans, and more than 120 telecom operators deploying 5G roaming infrastructure. Europe followed with about USD 14.2 billion market size in 2024, driven by regulatory measures, the “Roam Like at Home” policy, and strong intra-regional travel exceeding 500 million people annually. Asia-Pacific achieved around USD 18.7 billion in 2024 in data roaming market value, led by countries such as China, India, Japan, and South Korea with outbound roaming subscriber volumes exceeding 200 million. Latin America and Middle East & Africa collectively accounted for nearly USD 18–20 billion in 2024, supported by rising international travel, expanding mobile device adoption, and increasing investment in cross-border connectivity infrastructure.

How Are Enhanced Roaming Solutions Shaping Enterprise and Consumer Demand?

North America holds about 35% of the global mobile data roaming solution market share in 2024, reflecting its leadership in roaming infrastructure, regulatory maturity, and advanced service offerings. Major industries driving demand include travel & tourism, enterprise mobility (corporate travel), and IoT/connected devices sectors such as automotive and wearables. Regulatory changes in the United States and Canada have introduced clearer rules on roaming tariffs, data privacy, and international roaming agreements, encouraging operators to offer transparent roaming pricing and bundled data plans. Technological trends include rollout of eSIM/iSIM platforms, deployment of dynamic routing, network edge caching, and real-time roaming traffic analytics. A local player, AT&T, has expanded its international roaming plans with embedded eSIM for travellers, offering over 80 countries of coverage with simplified on-boarding. Consumer behavior varies: enterprise users in finance, healthcare, and professional services often demand SLA-backed roaming solutions, while leisure travellers prioritize flexible short-term roaming passes.

Why Are Regulatory and Roaming Harmonization Efforts Central to Innovation?

Europe commands close to 30% share of the mobile data roaming solution market in 2024, driven by markets such as Germany, UK, and France where regulatory bodies enforce transparency and network interoperability. Key regulatory frameworks like the European Union’s policies on roaming, data protection (GDPR), and “Roam Like at Home” regulations have removed additional intra-regional charges and encouraged unified roaming service standards. Adoption of technologies such as eSIM, VoLTE roaming, and real-time billing reconciliation is increasing. A local operator, Vodafone European operations, has upgraded roaming platforms to support VoLTE and HD voice across more than 50 destination countries, enhancing voice quality while abroad. Consumer behavior tends to favor explainable roaming solutions, i.e., users want clarity on rates, data consumption alerts, and minimal latency, especially among high-frequency travellers and cross-border commuters.

What Drives Rising Demand Among Travellers and Device Ecosystems?

Asia-Pacific accounted for approximately USD 17.8 billion in mobile data roaming market value in 2024, ranking third behind North America and Europe. Top consuming countries include China, India, Japan, and South Korea, with aggregate outbound roaming subscribers exceeding 200 million. Infrastructure trends involve accelerated 5G/6G deployments, growth in cloud-based roaming solutions, and investment in regional roaming consortiums like Bridge Alliance covering multiple networks. Local players, such as major Chinese telecom operators, are launching eSIM-based roaming plans integrated into consumer devices and travel packages. Consumer behavior shows strong demand from travellers and youth segments: more than 70% of travellers in India and Southeast Asia prefer roaming plans that can be activated remotely, and mobile apps for roaming management are heavily used.

How Are Localization and Government Incentives Shaping Adoption?

South America held about 8% share of the global mobile data roaming solution market in 2024, with Brazil and Argentina being the most significant contributors. Infrastructure enhancements in telecommunications are on the rise, with increasing investment into fiber-optic backhaul and upgrade of roaming interconnections. Government incentives and trade policy reforms in Brazil and Mercosur are encouraging cross-border roaming agreements. A local telecom firm in Brazil has deployed roaming management tools with multilingual customer support and localized billing to serve both Portuguese and Spanish speaking travellers. Consumer behavior is influenced by demand tied to language localization, budget-friendly roaming bundles, and preference for travel promotions paired with roaming benefits.

What Role Does Digital Transformation Play in Remote Connectivity Zones?

Middle East & Africa accounted for around 6% of the global mobile data roaming solution market in 2024. Major growth countries include UAE, Saudi Arabia, and South Africa, where demand is rising among business travellers, expatriate communities, and connected device users. Technological modernization trends involve deployment of roaming agreements supporting 5G/4G handovers, investment in satellite backhaul in remote areas, and deployment of secure roaming platforms. Local players such as telecom operators in UAE have begun offering bundled roaming data plans for tourists and remote workers. Consumer behavior in the region shows preference for mobile-first, pay-as-you-go roaming options, with over 50% of users selecting short-term roaming packs rather than long-term contracts.

United States – 28% market share

Dominance due to high outbound and inbound roaming connections, well-developed telecom infrastructure, and aggressive deployment of 5G and eSIM technologies.

China – 16% market share

Leadership driven by rapid growth in outbound travellers, government support for roaming infrastructure, and large mobile user base including use of eSIM/iSIM in devices.

The mobile data roaming solution market is relatively consolidated among major telecom operators, roaming solution vendors, eSIM platform providers, and network infrastructure firms. In 2024, more than 90 active competitors are operating globally, with the top 5 players holding approximately 40-45% of the market. Key strategic initiatives include alliances between carriers (for example roaming agreement networks), partnerships with device OEMs for built-in roaming support, and launches of roaming management platforms emphasizing latency, dynamic routing, and security. Innovation trends are centered on real-time data usage monitoring, eSIM/iSIM remote provisioning, AI-based fraud detection in roaming traffic, and over-the-air profile switching. Operators are investing in seamless customer experience, push-notifications for data consumption abroad, and simplified cross-border billing. New product launches in 2023-2024 include unlimited roaming bundles, multipurpose roaming for IoT devices, and tailored solutions for business travellers. The market remains competitive, with differentiation largely based on interface quality, roaming destination breadth, regulatory compliance, and backend network routing performance.

T-Mobile USA

China Mobile

SoftBank Group

Telefónica

MTN Group

Telstra Corporation

Bharti Airtel

Emerging technologies are reshaping the mobile data roaming solution market through increased automation, intelligent network routing, secure identity management, and seamless connectivity across platforms. eSIM and iSIM are enabling remote provisioning and profile switching, removing dependence on physical SIM distribution; in 2024 over 25% of new devices shipped have built-in eSIM profiles enabling roaming activation. 5G roaming is expanding, with more than 30 countries supporting full inter-network and interoperator 5G roaming handovers. Roaming management platforms are incorporating AI/ML to detect anomalous roaming traffic, reduce fraud, and optimize cost by routing traffic through least-cost transit paths. Edge computing and network slicing are being tested to reduce latency for roaming users, particularly in video streaming and gaming use-cases. Blockchain and secure ledger technologies are being piloted in certain markets to ensure tamper-proof roaming agreements and transparent billing. Real-time usage dashboards, roaming usage alerts, and localized pricing interfaces are becoming standard in app-based user journey designs.

In September 2025, Kenya Airways launched KQSafari Data, a global roaming service in partnership with RoamBuddy. The service gives travellers access to more than 2,250 roaming plans in over 180 countries, aiming to reduce the cost of mobile data abroad. Source: www.techafricanews.com

In September 2024, a major European operator launched an eSIM-based roaming activation service in over 70 countries, enabling travellers to activate data roaming robustly without physical SIMs.

In December 2023, a North American telecom group introduced AI-powered roaming fraud detection reducing unauthorized usage by 27%.

In July 2024, a South American provider rolled out unlimited roaming data bundles for travellers in Brazil and Argentina, increasing adoption for travel-heavy users by 34%.

The report covers global market segmentation by deployment type (traditional roaming, eSIM/iSIM virtual roaming, hybrid roaming), service type (data routing, billing & usage monitoring, roaming customer care, security & fraud protection), and end-user verticals (travel & tourism, enterprise mobility, automotive connectivity, IoT/wearables, device OEMs). Geographic regions analysed include North America, Europe, Asia-Pacific, South America, Middle East & Africa, with country-level breakdowns for US, China, India, Brazil, Germany, UK, Japan, South Africa, UAE. Technology focus includes network routing optimization, eSIM/iSIM integration, AI/ML analytics, edge computing, blockchain in roaming contracts. Industry focus areas include regulatory compliance, cross-border interconnection agreements, user experience optimization, cost transparency, and sustainable infrastructure investment. Product innovation areas such as unlimited roaming bundles, IoT/automotive embedded roaming, and mixed reality/streaming friendly roaming experiences are also examined to support emerging demand.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 84,786.6 Million |

|

Market Revenue in 2032 |

USD 136,160.2 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Deployment Type

By Service Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Vodafone Group, AT&T Inc., Orange S.A., T-Mobile USA, China Mobile, SoftBank Group, Telefónica, MTN Group, Telstra Corporation, Bharti Airtel |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |