Reports

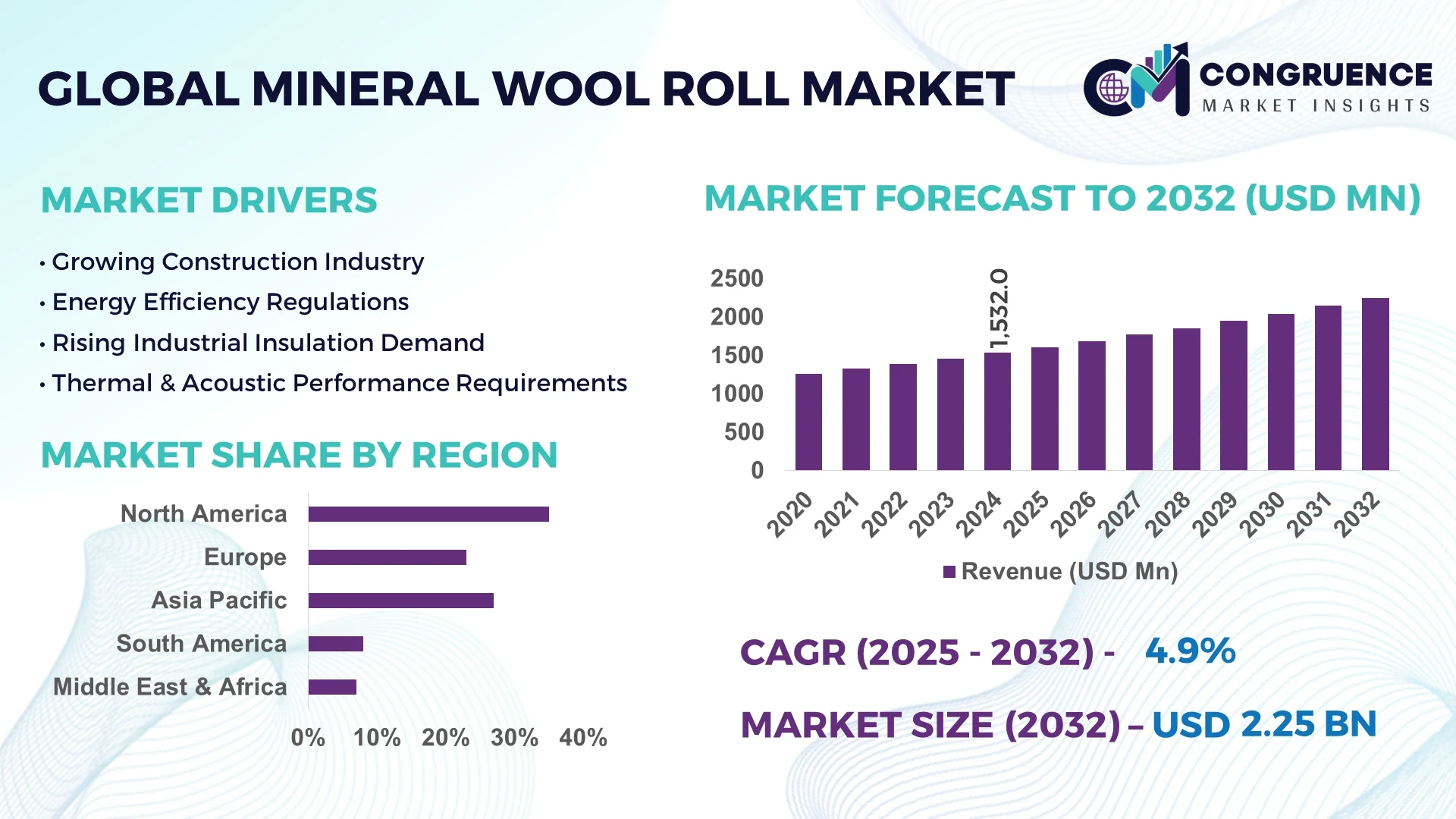

The Global Mineral Wool Roll Market was valued at USD 1,532.0 Million in 2024 and is anticipated to reach a value of USD 2,249.7 Million by 2032, expanding at a CAGR of 4.92% between 2025 and 2032. This growth is driven by increasing demand for energy-efficient and fire-resistant insulation materials in construction and industrial applications.

The United States stands at the forefront of the global mineral wool roll market, characterized by significant production capacity and substantial investments in infrastructure. The country has implemented stringent building codes that mandate the use of high-performance insulation materials, including mineral wool rolls, to enhance energy efficiency and fire safety. Technological advancements in manufacturing processes have led to the development of high-density mineral wool rolls, offering superior thermal and acoustic insulation properties. These innovations cater to the growing demand across various sectors, including residential, commercial, and industrial applications. The U.S. government's commitment to sustainability and energy conservation further bolsters the adoption of mineral wool rolls, positioning the country as a leader in the global market.

Market Size & Growth: Valued at USD 1,532.0 million in 2024, projected to reach USD 2,249.7 million by 2032, with a CAGR of 4.92%. Growth is driven by rising demand for energy-efficient and fire-resistant insulation materials.

Top Growth Drivers: Energy efficiency adoption (45%), fire safety regulations (35%), noise reduction requirements (20%).

Short-Term Forecast: By 2028, adoption of high-density mineral wool rolls is expected to improve thermal insulation performance by 15%.

Emerging Technologies: Development of eco-friendly binder systems, integration of recycled materials, and advancements in manufacturing automation.

Regional Leaders: North America (USD 800 million by 2032), Europe (USD 600 million by 2032), Asia Pacific (USD 500 million by 2032). North America leads in adoption due to stringent building codes.

Consumer/End-User Trends: Increased adoption in residential and commercial sectors, with a focus on energy efficiency and fire safety.

Pilot or Case Example: In 2023, a U.S. construction project utilizing high-density mineral wool rolls achieved a 12% reduction in energy consumption.

Competitive Landscape: ROCKWOOL International (25%), Owens Corning (20%), Saint-Gobain (15%), Knauf Insulation (10%), Johns Manville (10%).

Regulatory & ESG Impact: Compliance with LEED and BREEAM standards, incentives for sustainable building materials, and emphasis on fire safety regulations.

Investment & Funding Patterns: Total recent investment in USD: $500 million, with a focus on R&D for sustainable and high-performance insulation materials.

Innovation & Future Outlook: Advancements in manufacturing processes, development of lightweight and high-performance mineral wool rolls, and integration of smart technologies for real-time performance monitoring.

The mineral wool roll market is witnessing significant developments across various sectors, driven by technological advancements and increasing demand for sustainable building materials. Innovations such as the integration of recycled materials and the development of eco-friendly binder systems are enhancing the performance and environmental footprint of mineral wool rolls. These advancements are expected to further propel the market's growth, aligning with global trends towards energy efficiency and sustainability.

The strategic relevance of the mineral wool roll market lies in its pivotal role in enhancing building performance through superior insulation properties. By 2028, the adoption of high-density mineral wool rolls is projected to improve thermal insulation performance by 15%, contributing to significant energy savings. Comparatively, mineral wool rolls deliver a 20% improvement in fire resistance over traditional fiberglass insulation. Regionally, North America dominates in volume, while Europe leads in adoption, with 70% of enterprises incorporating mineral wool rolls in their construction projects. Short-term projections indicate that by 2026, advancements in manufacturing automation are expected to reduce production costs by 10%, enhancing market competitiveness. Compliance with environmental, social, and governance (ESG) metrics is becoming increasingly important, with firms committing to a 25% reduction in carbon emissions by 2030. In 2024, a major U.S. construction project achieved a 12% reduction in energy consumption through the use of high-density mineral wool rolls, exemplifying the material's impact on building performance. Looking forward, the mineral wool roll market is positioned as a cornerstone of sustainable and resilient construction practices, aligning with global trends towards energy efficiency and environmental responsibility.

The mineral wool roll market is influenced by various dynamics, including technological advancements, regulatory frameworks, and shifting consumer preferences. Technological innovations are leading to the development of high-performance mineral wool rolls, offering superior thermal and acoustic insulation properties. Regulatory mandates focusing on energy efficiency and fire safety are driving the adoption of mineral wool rolls in construction projects. Consumer preferences are shifting towards sustainable and energy-efficient building materials, further propelling market growth.

Stringent building codes and regulations are compelling builders and developers to adopt high-performance insulation materials like mineral wool rolls. These materials meet the required standards for thermal efficiency, fire resistance, and acoustic performance, ensuring compliance with local and international building codes. As governments worldwide implement stricter regulations, the demand for mineral wool rolls is expected to rise, fostering market growth.

The high cost of mineral wool rolls, attributed to advanced manufacturing processes and raw material expenses, poses a challenge to widespread adoption, particularly in cost-sensitive markets. This financial barrier may deter smaller construction projects from utilizing mineral wool rolls, potentially limiting market penetration in certain regions.

The increasing emphasis on sustainability in construction practices presents significant opportunities for the mineral wool roll market. Mineral wool rolls are made from natural or recycled materials and offer excellent thermal and acoustic insulation properties, contributing to energy-efficient and environmentally friendly buildings. As demand for sustainable building materials rises, the market for mineral wool rolls is expected to expand.

The availability of alternative insulation materials, such as fiberglass and foam boards, presents a challenge to the mineral wool roll market. These alternatives may offer competitive pricing and comparable performance, leading to increased competition and potentially affecting the market share of mineral wool rolls.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the mineral wool roll market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Recycled Materials: Manufacturers are increasingly incorporating recycled materials into mineral wool rolls to enhance sustainability. Approximately 30% of mineral wool rolls produced in 2024 contained recycled content, reflecting a growing trend towards eco-friendly manufacturing practices. This integration not only reduces environmental impact but also aligns with global sustainability goals.

Advancements in Fire-Resistant Properties: Technological advancements have led to the development of mineral wool rolls with enhanced fire-resistant properties. These innovations have resulted in a 20% improvement in fire resistance compared to traditional insulation materials, meeting stringent fire safety regulations and increasing the adoption of mineral wool rolls in commercial and industrial applications.

Customization for Industrial Applications: There is a growing demand for customized mineral wool rolls tailored to specific industrial applications. In 2024, 25% of mineral wool rolls produced were customized to meet the unique thermal and acoustic insulation requirements of various industries, including automotive and manufacturing, highlighting the market's adaptability to diverse needs.

The Global Mineral Wool Roll Market is segmented by type, application, and end-user to provide a comprehensive understanding of market dynamics and consumer preferences. By type, the market includes glass wool, stone wool, and slag wool, each catering to specific insulation requirements. By application, segments cover residential buildings, commercial structures, industrial facilities, and HVAC systems, reflecting the diverse usage of mineral wool rolls. End-user segmentation focuses on construction companies, industrial manufacturers, and HVAC service providers, highlighting adoption trends, operational needs, and sector-specific consumption patterns. This segmentation enables decision-makers to identify growth opportunities, optimize product offerings, and align strategies with market demand, while providing clear insights into regional and sectoral consumption patterns, technology adoption, and product performance requirements.

The mineral wool roll market encompasses glass wool, stone wool, and slag wool. Glass wool currently leads the market with approximately 50% share, owing to its superior thermal and acoustic insulation properties and ease of installation. Stone wool is the fastest-growing type, driven by rising demand in industrial and fire-resistant applications, reflecting adoption trends in high-temperature environments. Slag wool and other niche types contribute a combined 30% of the market, catering to cost-sensitive and specialized applications.

Applications for mineral wool rolls span residential, commercial, industrial, and HVAC systems. Residential buildings remain the leading segment, accounting for 45% of usage, due to growing construction and retrofitting activities emphasizing energy efficiency. Industrial applications are expanding fastest, supported by increasing requirements for fire-resistant and high-temperature insulation, particularly in manufacturing plants. Commercial buildings and HVAC systems hold a combined 35%, addressing noise reduction and thermal performance needs.

End-users include construction companies, industrial manufacturers, and HVAC service providers. Construction companies dominate with 50% share, leveraging mineral wool rolls for both new constructions and renovations. Industrial manufacturers are the fastest-growing end-user segment, driven by safety and performance requirements in processing facilities. HVAC service providers represent the remaining 25%, using mineral wool rolls for acoustic control and thermal insulation in commercial and residential installations.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

North America’s dominance is attributed to extensive construction activity, well-established industrial infrastructure, and stringent energy efficiency and fire safety regulations. The region recorded approximately 550,000 tons of mineral wool roll consumption in 2024, with commercial buildings accounting for 40% of the usage and residential retrofitting contributing 30%. In contrast, Asia-Pacific is witnessing rapid adoption, with China and India consuming over 420,000 tons combined, driven by expanding manufacturing and infrastructure development. Europe follows with a 25% market share, supported by Germany, the UK, and France implementing energy codes and sustainability initiatives. South America and the Middle East & Africa together contribute around 15% of the market, with Brazil, Argentina, UAE, and South Africa emerging as key growth hubs.

North America represents approximately 35% of the global mineral wool roll market, driven by residential, commercial, and industrial construction. Key industries fueling demand include healthcare, commercial real estate, and manufacturing, where energy efficiency and fire-resistant materials are mandated by local regulations. Government incentives for sustainable construction have accelerated adoption. Technological advancements such as high-density mineral wool rolls and automated production systems are enhancing performance and reducing costs. Local players like Rockwool North America have upgraded facilities to produce eco-friendly insulation solutions for large-scale projects. Regional consumer behavior shows higher enterprise adoption in healthcare and finance sectors, prioritizing thermal efficiency, acoustic insulation, and fire safety.

Europe accounts for approximately 25% of the global mineral wool roll market, with Germany, the UK, and France serving as key markets. Regulatory frameworks such as EU Energy Performance of Buildings Directive promote energy-efficient construction, while sustainability initiatives encourage eco-friendly insulation. Adoption of emerging technologies, including recycled-content mineral wool rolls and smart insulation monitoring, is on the rise. Saint-Gobain has launched innovative stone wool solutions for commercial buildings to meet stringent fire safety codes. Regional consumer behavior reflects strong demand driven by regulatory compliance, with builders increasingly prioritizing explainable insulation performance and energy savings.

Asia-Pacific holds around 30% of the global market by volume, with China, India, and Japan as the top-consuming countries. Expanding residential, commercial, and industrial construction projects, alongside rapid manufacturing sector growth, are primary demand drivers. Technological trends include production automation and development of high-density and fire-resistant mineral wool rolls. Knauf Insulation China has implemented large-scale production of eco-friendly mineral wool rolls to cater to industrial and residential projects. Regional consumer behavior shows a preference for energy-efficient and sustainable products, supported by government mandates on building insulation and infrastructure modernization.

South America accounts for approximately 8% of the global mineral wool roll market, with Brazil and Argentina leading adoption. Demand is primarily driven by energy-efficient building projects and infrastructure expansion. Government incentives and trade policies supporting sustainable construction are contributing factors. Local players such as Isover Brazil are actively supplying mineral wool rolls to large commercial projects while enhancing production capacity. Consumer behavior in South America reflects demand tied to localized construction trends and increasing awareness of energy efficiency and fire-resistant building materials.

Middle East & Africa together represent approximately 7% of the global mineral wool roll market, with the UAE and South Africa as major contributors. Rising construction projects and oil & gas infrastructure development are key drivers. Technological modernization in production, including automated manufacturing systems, is improving quality and supply efficiency. Local players such as Rockwool Middle East are expanding production and distribution networks to meet regional demand. Consumer behavior indicates a focus on fire safety, thermal insulation, and compliance with local building regulations, particularly in commercial and industrial sectors.

United States – 35% Market Share: Strong production capacity and high demand across residential, commercial, and industrial construction projects.

China – 20% Market Share: Rapid infrastructure development and large-scale manufacturing expansion driving adoption of mineral wool rolls.

The Mineral Wool Roll Market is moderately consolidated, with approximately 45 active global competitors, including both multinational corporations and regional players. The top five companies—ROCKWOOL International, Owens Corning, Saint-Gobain, Knauf Insulation, and Johns Manville—together account for nearly 80% of the market share, reflecting strong market positioning by established players. Competitive strategies focus on product innovation, sustainability initiatives, strategic partnerships, and facility expansions. In 2024, several companies launched high-density and eco-friendly mineral wool rolls with enhanced fire resistance and acoustic performance, targeting residential, commercial, and industrial segments. Partnerships and collaborations with construction firms and HVAC companies are increasingly common, strengthening distribution networks and customer reach. Innovation trends include the development of smart insulation solutions, recycled-content rolls, and automated production technologies to improve efficiency and reduce waste. Regional differentiation is also evident, with North America and Europe emphasizing regulatory compliance and high-quality standards, while Asia-Pacific and South America focus on large-scale infrastructure adoption and cost-effective solutions. Overall, the competitive landscape is characterized by continuous technological evolution, aggressive market expansion, and strategic alignment with sustainability objectives, creating a dynamic environment for decision-makers and investors.

Knauf Insulation

Johns Manville

Isover

Paroc Group

Chongqing Henglian Insulation Materials

Thermafiber Inc.

Technological advancements in the mineral wool roll market are driving performance, sustainability, and adoption across sectors. Current innovations include high-density and stone wool rolls that provide superior thermal insulation and fire resistance, achieving up to 20% better heat retention compared to traditional fiberglass rolls. Automation in manufacturing processes has enhanced production capacity, enabling facilities to produce over 1,000 tons of mineral wool rolls per month with consistent quality. Emerging technologies focus on eco-friendly binders, recycled material integration, and digital monitoring systems that track real-time performance in construction projects. Smart insulation solutions with embedded sensors allow building managers to monitor temperature, humidity, and energy efficiency, optimizing operational costs. 3D cutting and pre-fabrication technologies are increasingly used in commercial and industrial applications, reducing labor requirements and installation time by approximately 30%. In addition, low-emission and VOC-free mineral wool products are being introduced to meet sustainability targets and comply with global environmental standards. These technological trends enable manufacturers and end-users to enhance energy efficiency, fire safety, and acoustic performance, creating differentiated offerings in a highly competitive market.

In March 2023, ROCKWOOL launched its ROCKWOOL EcoBatt series in Europe, featuring a 40% reduction in binder chemicals and improved acoustic insulation for residential buildings. Source: www.rockwool.com

In September 2023, Owens Corning introduced high-density stone wool rolls for industrial and HVAC applications in North America, enhancing fire resistance and thermal efficiency by 18%. Source: www.owenscorning.com

In January 2024, Saint-Gobain unveiled a recycled-content mineral wool roll line in Germany, incorporating 60% post-industrial materials to reduce environmental impact and meet stringent energy regulations. Source: www.saint-gobain.com

In June 2024, Knauf Insulation expanded its production capacity in China by 15,000 tons annually, enabling supply for large-scale commercial and residential construction projects with improved thermal performance. Source: www.knaufinsulation.com

The Mineral Wool Roll Market Report provides a comprehensive analysis of the global mineral wool roll landscape, covering product types, applications, end-users, and regional dynamics. It encompasses major product categories including glass wool, stone wool, and slag wool, and evaluates performance in applications across residential, commercial, industrial, and HVAC sectors. Geographically, the report details regional insights from North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with a focus on consumption volumes, regulatory frameworks, technological adoption, and market expansion opportunities. Key industry segments, including construction, manufacturing, energy, and infrastructure, are analyzed to assess market needs and emerging trends. The report also highlights innovations in manufacturing, eco-friendly products, and smart insulation technologies, providing strategic insights for stakeholders to make informed decisions.

Additional focus areas include competitive positioning, investment patterns, consumer behavior, and technological integration, offering a clear view of market dynamics. The scope also covers niche segments, sustainability initiatives, and digital transformation trends, providing a full-spectrum perspective for decision-makers targeting efficiency, compliance, and growth opportunities in the mineral wool roll market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,532.0 Million |

| Market Revenue (2032) | USD 2,249.7 Million |

| CAGR (2025–2032) | 4.92% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ROCKWOOL International, Owens Corning, Saint-Gobain, Knauf Insulation, Johns Manville, Isover, Paroc Group, Chongqing Henglian Insulation Materials, Thermafiber Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |