Reports

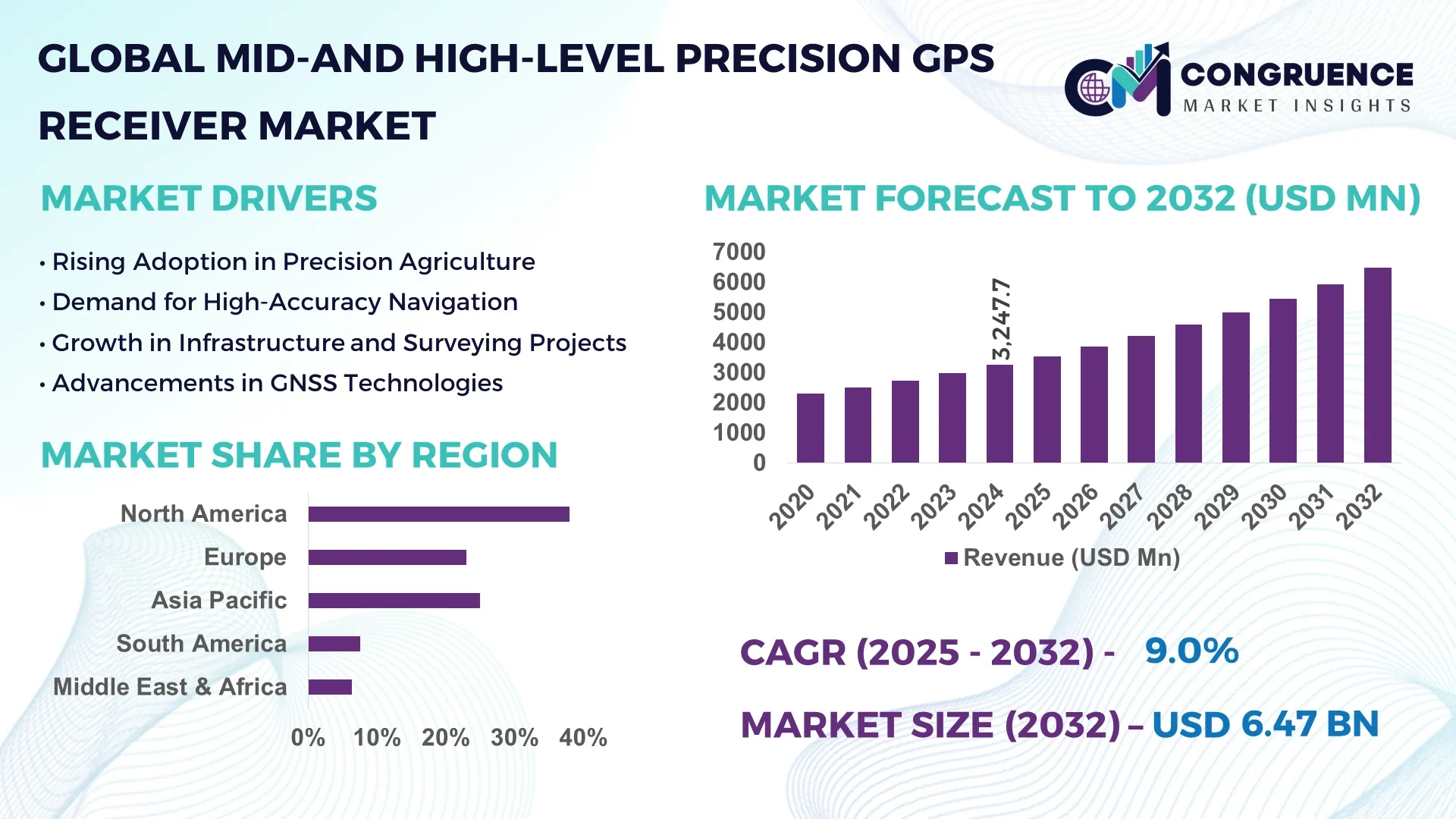

The Global Mid-and High-Level Precision GPS Receiver Market was valued at USD 3247.67 Million in 2024 and is anticipated to reach a value of USD 6471.18 Million by 2032 expanding at a CAGR of 9.0% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States leads the global market in mid-and high-level precision GPS receivers, boasting advanced production facilities and significant investment in R&D. The country is known for integrating cutting-edge technology into GPS receiver manufacturing, particularly for applications in aerospace, defense, and autonomous vehicles, supported by stringent regulatory frameworks and robust technological infrastructure.

The Mid-and High-Level Precision GPS Receiver Market spans key industry sectors including agriculture, construction, transportation, and surveying. The agriculture sector utilizes precision GPS technology to enable smart farming techniques, significantly enhancing crop yields through accurate field mapping and automated machinery. In construction, these receivers are integral to site surveying and machine control, improving project accuracy and reducing operational costs. Technological innovations such as multi-frequency signal processing and real-time kinematic (RTK) positioning are shaping the market by improving receiver accuracy and reducing latency. Environmental and regulatory factors, including global emissions reduction initiatives and government mandates on location accuracy, are driving adoption across regions. Emerging trends such as integration with IoT systems and increasing demand for autonomous drones highlight a promising future outlook, with regional consumption patterns showing accelerated growth in North America and Asia-Pacific.

Artificial Intelligence (AI) is revolutionizing the Mid-and High-Level Precision GPS Receiver Market by enhancing data processing capabilities, operational efficiency, and accuracy. AI algorithms enable GPS receivers to filter noise, predict satellite visibility, and improve signal reliability in challenging environments such as urban canyons or dense forests. This leads to more precise positioning data critical for industries like autonomous transportation, surveying, and precision agriculture. AI-powered receivers can analyze large volumes of geospatial data in real-time, facilitating dynamic route optimization and adaptive navigation systems.

In the Mid-and High-Level Precision GPS Receiver Market, AI integration has led to improvements in receiver firmware that self-learns to adjust to satellite constellation changes, enhancing positional accuracy without manual recalibration. Additionally, AI-driven anomaly detection identifies and corrects GPS errors caused by atmospheric interference, multipath effects, or signal jamming, which improves reliability for mission-critical applications. AI also accelerates the processing speed of correction signals from augmentation systems such as WAAS or EGNOS, enabling faster and more stable positioning outputs. These advancements support operational performance across transportation fleets, construction equipment, and unmanned aerial vehicles (UAVs). The synergy between AI and precision GPS receivers continues to foster innovation, enabling smarter, more autonomous systems that meet growing demands for location accuracy and system resilience.

“In 2024, a leading GPS technology company implemented AI-based adaptive filtering algorithms within their mid-and high-level precision GPS receivers, resulting in a 25% improvement in signal stability under urban canyon conditions and a 15% reduction in positioning errors during real-time operations.”

The rising integration of autonomous vehicles and precision agriculture technologies is a critical driver for the Mid-and High-Level Precision GPS Receiver market. Precision GPS receivers enable automated machinery to operate with centimeter-level accuracy, significantly improving crop management and reducing resource wastage. The transportation sector’s growing reliance on advanced navigation systems to support autonomous driving and fleet management further boosts demand. Industry data reveals that agriculture equipment manufacturers have incorporated precision GPS receivers in over 70% of new machinery shipments globally. This increasing adoption accelerates technological innovation and expands applications, underpinning robust growth in the Mid-and High-Level Precision GPS Receiver market.

One of the major restraints in the Mid-and High-Level Precision GPS Receiver market is the substantial cost associated with developing and deploying advanced receiver technologies. High-precision components, such as multi-frequency antennas and enhanced signal processors, significantly increase manufacturing expenses. These costs often limit the adoption of mid-and high-level GPS receivers, particularly among small and medium-sized enterprises and emerging markets. Moreover, maintenance and calibration requirements add to the overall operational expenses, deterring wider usage. Budget constraints in sectors like construction and agriculture can slow market penetration, creating challenges for manufacturers aiming to expand their customer base.

The growing utilization of unmanned aerial vehicles (UAVs) and drones across commercial, agricultural, and defense sectors presents a significant opportunity for the Mid-and High-Level Precision GPS Receiver market. High-level precision GPS receivers are essential for reliable navigation and positioning of drones in complex environments, facilitating applications such as aerial surveying, mapping, and delivery services. Forecasts indicate a surge in drone deployments worldwide, with precision GPS technology becoming a critical component. This trend opens avenues for product innovation and customization tailored to UAV-specific requirements, driving new market segments and revenue streams within the Mid-and High-Level Precision GPS Receiver industry.

Regulatory challenges and spectrum management complexities pose significant obstacles to the Mid-and High-Level Precision GPS Receiver market. Different countries enforce varied standards for frequency allocation and interference mitigation, complicating product development and cross-border deployments. Ensuring compliance with stringent government regulations regarding signal security and electromagnetic interference requires continuous adaptation and investment. Additionally, congestion in GPS frequency bands due to increasing satellite constellations and competing technologies creates technical difficulties that can degrade receiver performance. These regulatory and spectrum-related challenges increase operational risks and development costs, impacting market growth and innovation pace.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is significantly influencing the Mid-and High-Level Precision GPS Receiver market. Automated manufacturing of pre-bent and cut components off-site requires highly precise GPS receivers to ensure exact placement and alignment. This trend is particularly pronounced in Europe and North America, where the focus on reducing labor costs and accelerating project completion is driving demand for advanced positioning technologies. Precision GPS receivers are critical for coordinating machinery and verifying dimensional accuracy during assembly, supporting the shift toward faster, more efficient building processes.

• Enhanced Multi-Constellation Support: Increasing incorporation of multi-constellation capabilities, including GPS, GLONASS, Galileo, and BeiDou, is transforming receiver performance in the Mid-and High-Level Precision GPS Receiver market. Devices with multi-constellation support provide superior signal availability and redundancy, minimizing downtime in urban or obstructed environments. This feature improves operational reliability for sectors such as autonomous transportation, surveying, and maritime navigation, where consistent accuracy is non-negotiable.

• Integration with Edge Computing Platforms: The integration of Mid-and High-Level Precision GPS Receivers with edge computing is emerging as a pivotal trend. Real-time data processing at the edge reduces latency and enables faster decision-making for applications like precision farming, construction site monitoring, and drone navigation. This shift allows organizations to optimize workflows, enhance operational safety, and reduce reliance on centralized cloud infrastructure.

• Growing Use in Smart City Infrastructure: The deployment of precision GPS receivers within smart city projects is accelerating, driven by increasing urbanization and demand for connected infrastructure. Applications include traffic management systems, public transportation tracking, and emergency response coordination. These receivers provide critical data that supports real-time location tracking and spatial analytics, helping municipalities improve service delivery and resource allocation.

The Mid-and High-Level Precision GPS Receiver market is segmented based on product types, applications, and end-user categories, offering detailed insights into diverse demand drivers. By type, the market is classified into differential GPS receivers, RTK (Real-Time Kinematic) GPS receivers, and GNSS (Global Navigation Satellite System) receivers, each serving distinct accuracy and functionality requirements. Application segmentation includes agriculture, construction, transportation, surveying and mapping, and UAV/drone navigation, reflecting broad industry adoption. End-user segmentation focuses on sectors such as agriculture, construction, transportation, defense, and UAV operations. Understanding these segments enables decision-makers to identify strategic investment opportunities and tailor product offerings according to evolving market demands.

Among product types, RTK GPS receivers lead the Mid-and High-Level Precision GPS Receiver market due to their superior accuracy, often achieving centimeter-level precision, which is essential for construction and surveying operations requiring exact positioning. The fast-paced growth of GNSS receivers is driven by their capability to access multiple satellite constellations simultaneously, enhancing signal availability and reliability in complex environments such as urban canyons or dense foliage. Differential GPS receivers continue to play a vital role in agricultural applications where moderately high accuracy suffices for field mapping and machine guidance. Each type caters to specific industry needs, with RTK devices dominating high-precision tasks, GNSS gaining traction for robustness, and differential GPS maintaining niche relevance due to cost-effectiveness.

In the Mid-and High-Level Precision GPS Receiver market, agriculture stands out as the leading application, driven by widespread adoption of precision farming techniques that rely on accurate positioning for automated planting, fertilizing, and harvesting. The fastest-growing application area is UAV and drone navigation, where precise GPS receivers enable safe flight paths, real-time mapping, and delivery services, meeting the rising demand across commercial, industrial, and defense sectors. Construction also remains a significant application, utilizing precision GPS for site surveying, machine control, and infrastructure development. Other applications such as transportation and surveying benefit from improved location accuracy, facilitating fleet management and geospatial data collection. These diverse uses underscore the versatility of mid-and high-level GPS technology.

The agriculture sector is the dominant end-user in the Mid-and High-Level Precision GPS Receiver market, extensively leveraging GPS technology for enhancing crop yields, optimizing input usage, and supporting sustainable farming practices. The fastest-growing end-user segment is the UAV and drone industry, propelled by expanding commercial drone deployments for aerial inspection, surveillance, and delivery applications, requiring highly accurate GPS receivers for reliable operations. Construction firms constitute another key user base, employing GPS receivers for precise site layout and machine guidance to improve efficiency and safety. Defense and transportation sectors also contribute notably by integrating mid-and high-level GPS receivers into navigation and tracking systems to meet stringent operational requirements. This end-user diversity reflects broad market adoption and growth potential.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America continues to dominate due to extensive adoption of advanced positioning technologies across construction, agriculture, and transportation sectors. Meanwhile, Asia-Pacific’s expanding infrastructure projects, growing manufacturing capabilities, and rising adoption of smart technologies are driving significant demand for mid-and high-level precision GPS receivers. Europe and South America also maintain steady consumption patterns, influenced by regulatory frameworks and sustainable development initiatives. Emerging trends like integration with AI and edge computing further bolster regional growth prospects, making the market dynamic and competitive across geographies.

Accelerating Precision in Key Industrial Applications

North America holds approximately 38% of the Mid-and High-Level Precision GPS Receiver market volume, driven by robust demand from the agriculture, construction, and autonomous vehicle sectors. The region benefits from stringent government regulations supporting precision agriculture and smart infrastructure development, encouraging adoption of high-accuracy GPS technologies. Recent technological advancements include integration with IoT platforms and AI-enabled data analytics, enhancing operational efficiency. Digital transformation initiatives in manufacturing and logistics have increased reliance on GPS receivers for real-time asset tracking and process automation. These factors contribute to North America’s leadership in the precision GPS receiver landscape, with ongoing innovation fueling sustained market activity.

Pioneering Sustainable and Smart Location Solutions

Europe accounts for about 24% of the Mid-and High-Level Precision GPS Receiver market share, with Germany, the UK, and France being the key contributors. The region is influenced by stringent environmental regulations and sustainability mandates from bodies like the European Union, which promote precision technologies to reduce carbon footprints in construction and agriculture. European industries are rapidly adopting GNSS multi-constellation receivers to enhance reliability and accuracy. Additionally, the integration of GPS technology with smart city initiatives and renewable energy projects is expanding market demand. Innovation hubs in countries like Germany foster ongoing development of high-precision GPS technologies, supporting Europe’s strong market presence.

Driving Infrastructure Expansion with Advanced Positioning

Asia-Pacific ranks as the fastest-growing region with a significant market volume, largely fueled by China, India, and Japan. These countries are experiencing rapid industrialization and urbanization, resulting in increased investments in infrastructure and precision agriculture. The manufacturing sector’s shift towards Industry 4.0 standards is driving adoption of high-accuracy GPS receivers to improve automation and quality control. Regional tech innovation hubs are pioneering integration of GPS with AI and cloud computing to enhance operational precision. Government initiatives to modernize infrastructure and promote smart farming also contribute to the rising demand, solidifying Asia-Pacific’s pivotal role in the global market.

Emerging Markets Focused on Energy and Infrastructure Growth

South America holds around 8% market share, with Brazil and Argentina leading regional consumption of Mid-and High-Level Precision GPS Receivers. Growing infrastructure development projects, especially in transportation and energy sectors, are primary drivers. The region’s oil and gas industries increasingly utilize precision GPS technology for enhanced exploration and drilling accuracy. Government incentives and trade policies aimed at improving technological adoption support the market expansion. Despite slower digital transformation compared to developed regions, increasing awareness of precision positioning benefits is encouraging steady growth, particularly in urban planning and agricultural mechanization.

Modernizing Critical Sectors with Precision Technology

Middle East & Africa contribute roughly 6% to the Mid-and High-Level Precision GPS Receiver market, driven mainly by demand in oil & gas exploration, construction, and mining activities. The UAE and South Africa are the key growth countries benefiting from infrastructure modernization and smart city projects. Technological upgrades include deployment of ruggedized GPS receivers capable of operating in harsh environments. Regional regulations promoting industrial efficiency and enhanced safety standards encourage adoption. Furthermore, increasing trade partnerships facilitate access to cutting-edge GPS technologies, positioning the region as an emerging market for mid-and high-level precision GPS devices.

United States: Holds 32% market share due to strong production capacity and advanced technological infrastructure supporting agriculture and construction sectors.

China: Captures 25% market share driven by rapidly growing infrastructure investments and increasing industrial automation requiring precision positioning solutions.

The Mid-and High-Level Precision GPS Receiver market is characterized by a moderately concentrated competitive environment, with approximately 25 to 30 active global players vying for market share. Leading companies focus heavily on innovation, consistently launching advanced GPS technologies that enhance accuracy, durability, and integration with emerging digital platforms such as IoT and AI. Strategic partnerships and collaborations with technology firms and end-user industries are prevalent, enabling companies to expand their market presence and improve product offerings. Additionally, mergers and acquisitions have become key tactics for broadening geographic reach and acquiring complementary capabilities. The competition also revolves around developing ruggedized and multi-frequency receivers to meet diverse industrial applications. Market leaders differentiate themselves through investments in R&D, customization capabilities, and after-sales support, creating strong brand loyalty among enterprise clients. Overall, the competitive landscape is shaped by technological innovation, strategic expansion, and a focus on specialized applications to maintain and grow market positioning.

Trimble Inc.

Topcon Corporation

Leica Geosystems (part of Hexagon AB)

NovAtel Inc. (a Hexagon company)

Septentrio NV

Hemisphere GNSS Inc.

Navcom Technology Inc.

South Survey Instruments Co., Ltd.

CHC Navigation

Ashtech (a division of Trimble Inc.)

The Mid-and High-Level Precision GPS Receiver market is experiencing significant technological evolution driven by advances in multi-constellation GNSS integration, real-time kinematic (RTK) positioning, and enhanced signal processing algorithms. Modern receivers now support simultaneous tracking of GPS, GLONASS, Galileo, and BeiDou satellite systems, which improves positional accuracy and reliability across diverse environments. Integration of RTK technology enables centimeter-level precision, critical for applications in surveying, agriculture, and autonomous vehicles. Emerging technologies such as multi-frequency reception reduce signal interference and enhance performance in urban canyons or dense foliage, addressing longstanding challenges in GPS accuracy. Furthermore, developments in low-power GNSS chipsets are enabling extended field operations for portable and battery-dependent devices.

Digital transformation trends also incorporate AI and machine learning algorithms to optimize satellite signal acquisition and error correction in real-time, increasing operational efficiency. Additionally, ruggedized receiver designs with enhanced environmental resistance are gaining traction, especially for industrial and military use cases. Enhanced connectivity options, including integration with 5G networks and cloud-based data services, allow seamless data transmission and remote monitoring. These technological innovations collectively drive market growth by expanding the applicability and performance of Mid-and High-Level Precision GPS Receivers across multiple high-value sectors.

In January 2024, Trimble launched the Trimble R12i GNSS receiver, featuring advanced inertial technology for improved tilt compensation and enhanced accuracy in challenging environments, targeting surveying and construction applications globally.

In September 2023, Leica Geosystems unveiled the GS18 T GNSS RTK rover, integrating a high-performance GNSS receiver with a unique tilt compensation sensor, simplifying complex data collection workflows in geospatial projects.

In March 2024, Hemisphere GNSS introduced the A326 GNSS smart antenna, designed with multi-frequency capabilities and compact form factor, supporting precision agriculture and unmanned vehicle navigation demands in North America and Europe.

In November 2023, NovAtel released its SMART6-L GNSS receiver, combining multi-constellation support with advanced interference mitigation technology, improving operational reliability in military and defense applications worldwide.

The Mid-and High-Level Precision GPS Receiver Market Report provides a comprehensive analysis of the market’s broad spectrum, encompassing product types, applications, end-user industries, and geographic regions. The report covers key product segments including single-frequency, dual-frequency, and multi-frequency receivers, with particular emphasis on the growing adoption of multi-constellation GNSS-enabled devices. It further analyzes applications spanning surveying and mapping, agriculture, construction, transportation, and defense, highlighting diverse use cases that drive market demand. Geographically, the report examines major markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional market shares, technological penetration, and infrastructure developments that influence growth dynamics. The geographic focus includes both mature markets with established precision GPS receiver deployments and emerging markets with expanding infrastructure and industrial activities.

Technological insights extend to innovations in RTK, GNSS augmentation systems, low-power chipsets, and AI-driven positioning enhancements, underlining the report’s commitment to tracking cutting-edge trends. Additionally, the report explores niche and emerging segments such as UAV (unmanned aerial vehicle) applications, autonomous vehicles, and smart city projects that increasingly rely on high-precision GPS technology. By delivering detailed market segmentation and comprehensive coverage of competitive, technological, and regional factors, the report offers critical intelligence for stakeholders seeking strategic opportunities and informed decision-making in the Mid-and High-Level Precision GPS Receiver market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3247.67 Million |

|

Market Revenue in 2032 |

USD 6471.18 Million |

|

CAGR (2025 - 2032) |

9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Trimble Inc., Topcon Corporation, Leica Geosystems (part of Hexagon AB), NovAtel Inc. (a Hexagon company), Septentrio NV, Hemisphere GNSS Inc., Navcom Technology Inc., South Survey Instruments Co., Ltd., CHC Navigation, Ashtech (a division of Trimble Inc.) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |