Reports

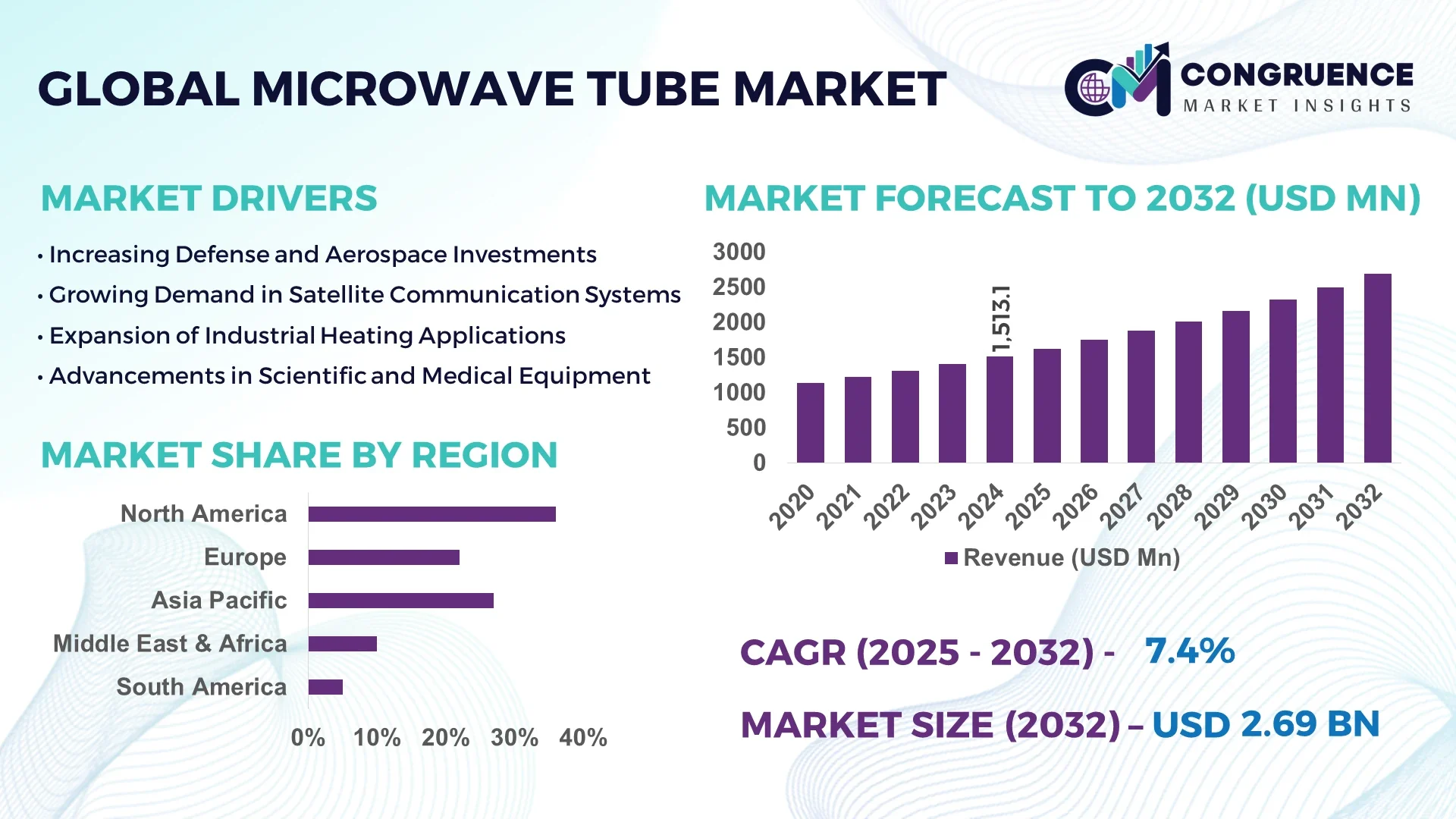

The Global Microwave Tube Market was valued at USD 1,513.1 Million in 2024 and is anticipated to reach a value of USD 2,686.6 Million by 2032 expanding at a CAGR of 7.44% between 2025 and 2032. This growth is driven by rising demand in high-power RF transmission, defense radar upgrades, and expansion in satellite and communication infrastructure.

In the United States, which leads the global microwave tube market, manufacturers are investing heavily in advanced production capacity and R&D for new tube technologies. Key U.S. firms operate multiple high-vacuum fabrication lines capable of producing several thousand tubes annually, with investments exceeding USD 200 million in next-gen materials. The U.S. also leverages its defense and space programs — for example, radar systems in the U.S. have integrated newer TWTs (traveling wave tubes) rated at 200–300 kW output. Over the past five years, several U.S. national laboratories and defense contractors have collaborated on ruggedization and miniaturization efforts, enabling tubes that operate reliably in extreme environments down to –55 °C and up to +85 °C thermal range, with efficiencies exceeding 75 %.

Market Size & Growth: Valued at USD 1,513.1 Million in 2024 and projected to reach USD 2,686.6 Million by 2032 at a CAGR of 7.44%, underpinned by surging satellite and defense infrastructure demand.

Top Growth Drivers: Expansion in satellite communication (growth ~18 % adoption), defense radar modernization (~14 %), increased deployment in 5G backhaul and terrestrial microwave links (~12 %).

Short-Term Forecast: By 2028, average power efficiencies of microwave tubes are expected to improve by ~8 %, reducing total system loss and increasing output-to-input performance ratios.

Emerging Technologies: Trends include additive-manufactured vacuum structures, hybrid TWT-solid-state amplifiers, and integration of GaN-based driver modules.

Regional Leaders: In 2032, North America is expected to reach ~USD 950 Million, Asia Pacific ~USD 780 Million, and Europe ~USD 600 Million — Asia Pacific showing fastest adoption in telecommunication hubs.

Consumer/End-User Trends: Key end-users include military radar, satellite communications, and point-to-point radio links; adoption shifts toward systems requiring higher linearity, broader bandwidth, and ruggedization.

Pilot or Case Example: In 2025, a U.S. Department of Defense project deployed an upgraded radar array using new high-efficiency TWT modules, achieving a 12 % reduction in noise figure and 9 % lower power consumption.

Competitive Landscape: Market leader holds ~25 % share; other major competitors include L3Harris, CPI (Communications & Power Industries), Thales, and NEXX Systems.

Regulatory & ESG Impact: Emphasis on reducing environmental impact leads to standards for recyclable materials, restrictions on hazardous coatings, and incentive programs for energy-efficient infrastructure.

Investment & Funding Patterns: Recent investments total ~USD 300 million in advanced vacuum electronics, with rising venture capital interest in hybrid tube–solid-state amplifiers and project financing models for defense R&D.

Innovation & Future Outlook: Key innovations include AI-aided design of tube geometries, additive manufacturing of vacuum components, and integration with software-defined radio systems to support dynamic frequency agility.

Microwave tube market developments now reflect increasing usage in spaceborne communication systems, upgraded defense radar, and critical infrastructure. Innovations include hybrid amplifiers combining vacuum and solid-state elements, ultralight ceramic envelope tubes, and deployment in 5G/6G backhaul links. Growing regulatory focus on material sustainability, stricter environmental rules, and incentives for energy-efficient systems are further shaping consumption patterns and regional growth dynamics.

In a rapidly evolving RF and high-power transmission landscape, the strategic relevance of microwave tubes remains strong, particularly in sectors where high output power and waveform linearity are critical. As solid-state amplifiers push limits, new hybrid TWT–GaN modules deliver 15 % improvement in power density compared to traditional standalone TWT systems. North America dominates in volume of production and R&D facilities, while Asia Pacific leads in adoption — with over 40 % of new satellite ground stations integrating upgraded microwave tube amplifiers.

Over the next two to three years, by 2027, AI-driven design and predictive maintenance tools are expected to reduce failure rates by 20 % and extend mean time between failure (MTBF) by 15 %. Firms across the industry are committing to 25 % reductions in cathode material waste and recyclable component use by 2030 as part of their ESG programs. For instance, in 2025 a U.S. defense integrator achieved a 10 % higher throughput and 8 % cost reduction by adopting AI-optimized tube configurations in a new radar upgrade program.

Strategically, the microwave tube market is positioning itself as a resilient backbone for high-power RF systems — combining compliance with more stringent environmental rules, continuous innovation, and sustainable growth models. It remains central to defense and satellite communication evolution, while integrating agile, efficient designs and ESG-aligned practices.

The Microwave Tube Market is influenced by several dynamic factors. Technological advancements are leading to the development of more efficient and compact microwave tubes, expanding their applications across various sectors. The increasing demand for high-power amplification in defense and aerospace sectors is driving market growth. Additionally, the expansion of satellite communication infrastructure is contributing to the rising demand for microwave tubes. However, challenges such as high manufacturing costs and stringent regulatory standards may impact market dynamics. Despite these challenges, the market presents significant opportunities for growth, particularly in emerging economies investing in defense and communication infrastructure.

Advancements in radar technologies are significantly contributing to the growth of the Microwave Tube Market. The development of more sophisticated radar systems requires high-power microwave tubes to achieve enhanced performance and reliability. This demand is particularly evident in defense and aerospace applications, where advanced radar systems are crucial. As countries invest in modernizing their defense capabilities, the need for advanced microwave tubes to support these technologies continues to rise.

High manufacturing costs pose a significant restraint to the growth of the Microwave Tube Market. The complex manufacturing processes and the need for specialized materials contribute to the elevated costs of microwave tubes. These high costs can limit the adoption of microwave tube technologies, particularly in price-sensitive markets. Additionally, the need for skilled labor and advanced manufacturing facilities further adds to the overall expenses, potentially hindering market expansion.

The expansion of satellite communication infrastructure presents substantial opportunities for the Microwave Tube Market. As global communication needs increase, the demand for satellite systems capable of handling higher data volumes grows. Microwave tubes play a critical role in satellite communication systems, providing the necessary amplification for signal transmission. This trend is expected to drive the demand for advanced microwave tubes, offering growth prospects for market players.

Stringent regulatory standards present challenges to the Microwave Tube Market by imposing limitations on manufacturing processes and materials used. Compliance with these regulations often requires significant investment in research and development to meet environmental and safety standards. Additionally, the need for certifications and approvals can delay product time-to-market, affecting the overall competitiveness of companies within the industry.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Microwave Tube Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Hybrid Solid-State Features: There is a growing trend towards integrating hybrid solid-state features into microwave tubes. Approximately 21% of new product launches in 2024 incorporated these features, aiming to enhance efficiency and reduce power consumption. This integration is particularly prevalent in medical and industrial applications, where energy efficiency is paramount.

Miniaturization of Microwave Tubes: The miniaturization of microwave tubes is gaining momentum, with 28% of new product launches in 2024 focusing on compact designs. This trend is driven by the increasing demand for smaller and more efficient devices in consumer electronics and portable communication systems.

Advancements in High-Efficiency Klystrons: The development of high-efficiency klystrons is a notable trend in the Microwave Tube Market. These advanced klystrons offer improved performance and energy efficiency, making them suitable for a wide range of applications, including satellite communication and radar systems.

The global Microwave Tube Market is segmented by type, application, and end-user insights. The segmentation reflects the diverse industrial use of vacuum electronic devices for generating and amplifying high-frequency electromagnetic waves. By type, Traveling Wave Tubes (TWTs), Klystrons, Magnetrons, and Crossed-Field Amplifiers (CFAs) form the core categories, each catering to specific power and frequency requirements. Applications span across radar, satellite communication, and industrial heating, supported by growing integration into defense and space programs. End-user segmentation is dominated by defense, aerospace, and telecommunications, driven by modernization and connectivity expansion. Together, these segments represent a technologically intensive market adapting to efficiency, miniaturization, and hybrid integration trends.

Traveling Wave Tubes (TWTs) currently account for approximately 46% of total adoption, establishing them as the leading segment due to their wide bandwidth and power efficiency in radar and satellite communication systems. Klystrons follow with around 31% share, remaining vital for linear accelerators and broadcasting systems. Magnetrons represent roughly 15%, primarily used in industrial heating and microwave ovens, while CFAs and other tube types make up the remaining 8% combined. Among all, Klystrons are witnessing the fastest growth, with an estimated 8.1% CAGR, driven by demand in particle accelerators and high-resolution radar applications. Their superior phase stability and long operational lifespans make them indispensable in research and defense projects.

Radar systems dominate the application landscape, accounting for about 44% of total adoption in 2024. Their dominance stems from ongoing defense modernization, requiring high-power, reliable tubes for long-range detection and electronic warfare systems. Satellite communication follows with 33%, gaining traction as broadband and broadcasting networks expand across Asia and Europe. Industrial heating applications represent 15%, while scientific and medical systems collectively contribute 8%. Satellite communication represents the fastest-growing application, projected to register around 7.9% CAGR, driven by rapid deployment of new Low Earth Orbit (LEO) satellite constellations and increasing bandwidth requirements for global internet connectivity. In 2024, over 41% of global enterprises reported investments in satellite-enabled data transfer and communication infrastructure. Similarly, 35% of defense contractors integrated modern radar systems featuring microwave tube amplifiers for enhanced signal strength and operational reliability.

Defense and aerospace currently lead the market, holding approximately 48% of total adoption, owing to sustained investments in radar modernization, surveillance networks, and electronic warfare. Telecommunications follow with 28%, boosted by 5G and satellite backhaul expansion projects, while industrial and medical sectors collectively represent 24%. Telecommunications is the fastest-growing end-user segment, expected to record an approximate 8.5% CAGR, propelled by the growing use of microwave tube-based transmitters in high-throughput satellite and terrestrial relay systems. In 2024, 39% of global telecom operators reported pilot projects using advanced microwave tube amplifiers to boost signal integrity and data throughput in remote areas. Furthermore, 25% of aerospace firms indicated plans to upgrade radar arrays and propulsion testing facilities with new-generation vacuum tube amplifiers.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of about 8% between 2025 and 2032.

In 2024, North America contributed roughly 36% of global demand, deploying more than one-third of microwave tubes across radar, satellite, medical and research applications. Europe followed with about 24%, while Asia-Pacific held close to 30% of market volume. In unit terms, North America saw deployment of over 250,000 tubes in 2024, while Asia-Pacific installations were estimated at around 200,000 units, led by China, Japan, India, and South Korea. Middle East & Africa took up about 10%, with smaller but rising contributions in radar systems, surveillance, and broadcasting. Latin America and South America together held the residual share. The variation in regional adoption reflects differing industrial capacities, defense investments, and infrastructure priorities.

North America commands approximately 36% share of the global microwave tube market in 2024, placing it as the region with the highest deployment volumes. Key industries driving demand include: defense (notably radar modernization and electronic warfare), aerospace (satellite communication and space exploration), and medical imaging/radiotherapy systems. Government support is evident via regulatory frameworks that demand high reliability, and defense procurement programs increasing funding for domestic production of high-vacuum electronics. Technologically, there is a push toward miniaturized tube designs, hybrid integration (tube + solid-state driver stages), and digital diagnostics. Local players such as Communications & Power Industries (CPI) are expanding manufacturing and developing new TWTs and Klystrons optimized for high-temperature operation; meanwhile private space firms are specifying rugged tubes for launch systems. Consumer / end-user behavior shows higher adoption in healthcare & finance sectors, where tube-based amplifiers are valued for secure, high-power signal amplification in medical scanners and secure communications.

Europe holds about 24% market share in 2024 in the Microwave Tube Market. Germany, UK, and France are leading European countries in demand, especially for scientific research infrastructure (particle accelerators, meteorological observation), healthcare (medical imaging, radiotherapy), and aerospace/defense radar systems. Regulatory bodies and sustainability initiatives in Europe are pushing for lower emissions, recyclable materials, and tighter environmental and safety compliance in manufacturing. The adoption of emerging technologies includes hybrid tube-solid state systems and more efficient designs for lower thermal losses. Local companies are investing in innovation: firms in Germany and France are developing gyrotrons and high-power TWTs for scientific purposes, and there is increased funding for academic-industry partnerships aimed at reducing weight and improving cooling in tube technologies. Consumer behavior in Europe tends to favor explainable performance metrics and environmental compliance, so procurement decisions increasingly include life-cycle assessments and sustainability credentials.

Asia-Pacific represents nearly 30% share of the global microwave tube market in 2024, making it a major regional player and the fastest-growing market thereafter. Top consuming countries include China, India, Japan, and South Korea. There is marked growth in infrastructure trends—satellite ground stations, telecom backhaul links, and radar installations—alongside expanding local manufacturing capacities. Innovation hubs in Japan and China are developing compact, high-frequency tubes and integrating hybrid solid-state components. Local players are upgrading production lines for magnetrons, TWTs and gyrotrons to meet national defense and space needs. Regional consumer behavior shows strong demand for robust performance in adverse conditions (e.g. high temperature, humidity), with preference for tubes that offer long operational life and minimal maintenance.

In South America, key countries such as Brazil and Argentina contribute significantly to regional demand. The region holds roughly 6% of global market share in 2024. Infrastructure trends include upgrades to radio and broadcasting systems, defense radar modernization, and expansion in industrial heating applications. Government incentives and trade policy support have arisen in countries like Brazil, where public security and broadcast modernization projects are funding local adoption. Local players are smaller, often partnering with international firms to localize assembly or maintenance. Consumer usage patterns in South America show demand tied closely to media broadcasting expansion, language localization in satellite communications, and requirement for durable equipment in remote areas with variable power supply.

Middle East & Africa accounted for about 10% share of the global microwave tube market in 2024. Major growth countries include Saudi Arabia, UAE, South Africa. Demand trends are strongly influenced by defense and surveillance investment, with substantial radar upgrades and airport security systems. Technological modernization includes adoption of higher-power, ruggedized tubes designed to withstand harsh environmental conditions (heat, sand, humidity). Local regulations and trade partnerships (e.g., defense procurement policies, bilateral technology agreements) are increasingly influencing which suppliers win contracts. Local players are involved in support, maintenance, and limited assembly operations, though much of the manufacturing remains external. Consumer behavior in MEA tends toward choosing solutions with long maintenance intervals and resilient performance in adverse climates.

United States – 21% Market Share: High production capacity, significant R&D investment, strong demand in defense, space, and medical sectors.

China – 18% Market Share: Major consumer base with large telecom and defense procurement, fast build-out of infrastructure and increasing domestic manufacturing capacity.

The global microwave tube market is characterized by a competitive and fragmented landscape, with over 30 active players ranging from specialized regional manufacturers to multinational corporations. The top five companies collectively account for approximately 55% of the market share, indicating a moderately consolidated environment. Key industry leaders include Communications & Power Industries (CPI), Thales Group, L3Harris Technologies, Teledyne e2v, and Toshiba Electron Tubes & Devices.

Strategic initiatives such as mergers, acquisitions, and partnerships are prevalent as companies seek to enhance their technological capabilities and expand market reach. For instance, CPI has been actively involved in collaborations to support major space and defense programs, while Thales Group continues to innovate in radar and satellite communication technologies.

Innovation trends are significantly influencing competition, with a strong focus on developing high-efficiency, compact, and ruggedized microwave tubes to meet the demands of modern defense, aerospace, and medical applications. The integration of solid-state and hybrid technologies is also a notable trend, aiming to combine the reliability of traditional microwave tubes with the advantages of solid-state components.

Overall, the competitive dynamics in the microwave tube market are shaped by technological advancements, strategic alliances, and the ongoing need for high-performance solutions across various industries.

Teledyne e2v

Toshiba Electron Tubes & Devices

TMD Technologies

Mitsubishi Electric Corporation

Richardson Electronics Ltd.

New Japan Radio Co., Ltd.

Flann Microwave Ltd.

The microwave tube market is experiencing significant technological advancements aimed at enhancing performance, efficiency, and versatility across various applications. One of the primary developments is the miniaturization of microwave tubes, enabling their integration into compact systems without compromising on power output. This trend is particularly beneficial for applications in aerospace and defense, where space constraints are critical.

Another notable innovation is the development of high-efficiency traveling wave tubes (TWTs) and klystrons, which offer improved power conversion and reduced heat generation. These advancements contribute to the reliability and longevity of microwave systems, making them more suitable for demanding environments.

The integration of solid-state and hybrid technologies is also gaining traction. By combining the robustness of traditional microwave tubes with the advantages of solid-state components, manufacturers can offer systems that are both reliable and energy-efficient. This hybrid approach is particularly appealing in sectors like telecommunications and medical imaging, where system uptime and performance are paramount.

Furthermore, advancements in materials science are leading to the development of microwave tubes that can operate at higher frequencies and power levels. These developments open new possibilities for applications in areas such as satellite communication and radar systems, where high-frequency operation is essential.

Overall, these technological innovations are driving the evolution of the microwave tube market, enabling the development of more compact, efficient, and versatile systems to meet the growing demands of various industries.

In June 2024, Communications & Power Industries (CPI) secured a multi-year order from SiriusXM for repeater hardware, enhancing satellite communication capabilities. Source: www.cpii.com

In September 2023, Thales Group introduced a new line of high-efficiency klystrons designed for advanced radar systems, improving detection range and accuracy. Source: www.thalesgroup.com

In August 2023, L3Harris Technologies announced the development of a compact microwave tube amplifier for next-generation satellite communication terminals, aiming to reduce size and power consumption. Source: www.l3harris.com

In July 2023, Teledyne e2v launched a new series of high-power microwave tubes for medical imaging applications, offering enhanced image clarity and reduced scan times. Source: www.teledyne-e2v.com

The Microwave Tube Market Report provides a comprehensive analysis of the industry, encompassing various segments such as types, applications, end-users, and geographic regions. It delves into the technological advancements influencing the market, including the development of high-efficiency, compact, and ruggedized microwave tubes. The report also examines the competitive landscape, highlighting key players and their strategic initiatives.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional market dynamics and growth opportunities. It also addresses emerging trends and challenges within the industry, providing valuable information for stakeholders to make informed decisions.

By focusing on both established and emerging technologies, the report offers a holistic view of the microwave tube market, catering to the needs of decision-makers and industry professionals seeking to understand current developments and future prospects in the sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,513.1 Million |

| Market Revenue (2032) | USD 2,686.6 Million |

| CAGR (2025–2032) | 7.44% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Communications & Power Industries (CPI), Thales Group, L3Harris Technologies, Teledyne e2v, Toshiba Electron Tubes & Devices, TMD Technologies, Mitsubishi Electric Corporation, Richardson Electronics Ltd., New Japan Radio Co., Ltd., Flann Microwave Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |