Reports

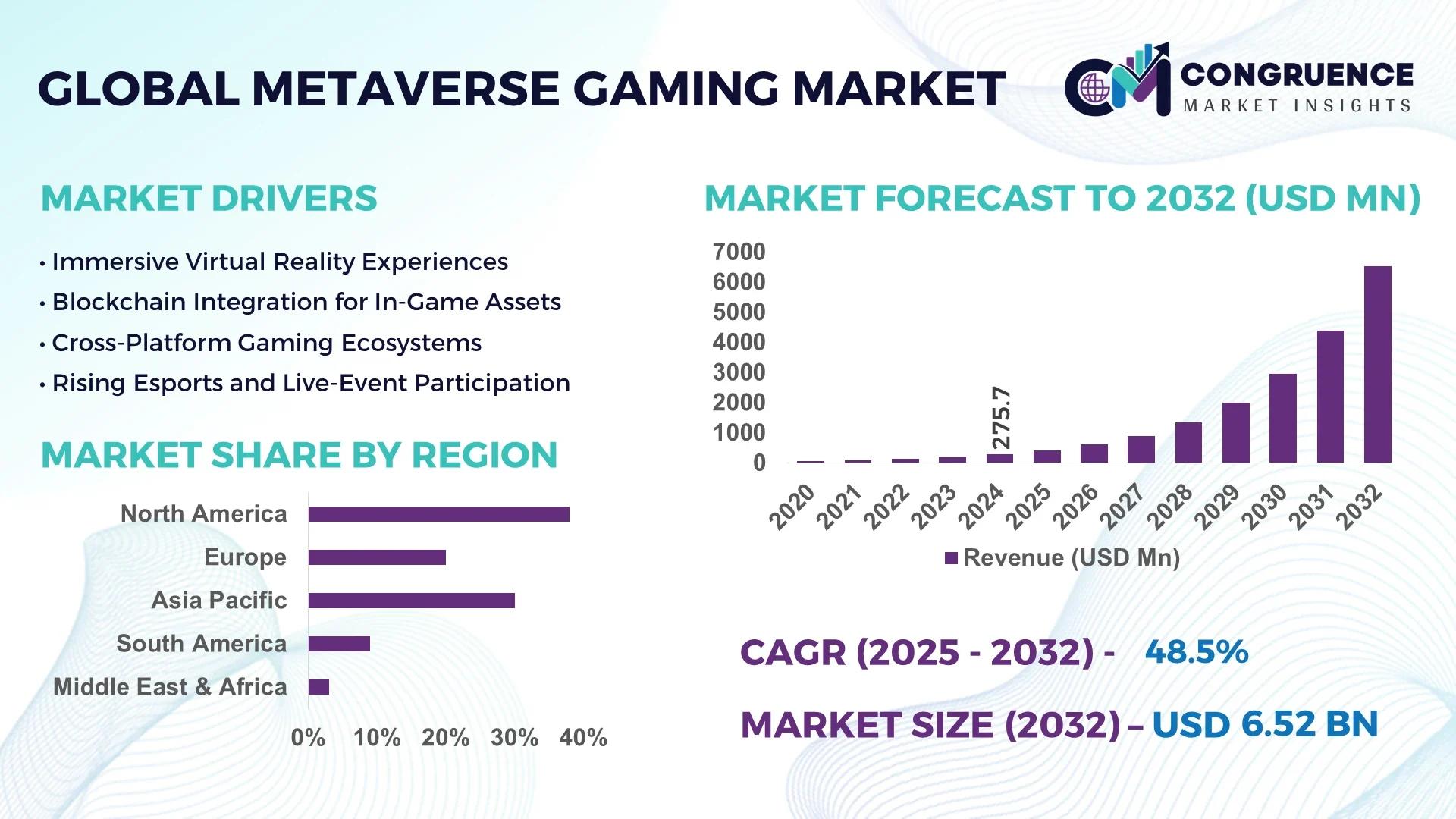

The Global Metaverse Gaming Market was valued at USD 275.65 Million in 2024 and is anticipated to reach a value of USD 6,518.9 Million by 2032 expanding at a CAGR of 48.5% between 2025 and 2032. This rapid growth is driven by accelerating demand for immersive technologies such as virtual reality, augmented reality, blockchain, and cloud gaming that enable rich, persistent virtual worlds.

China invests heavily in metaverse gaming, with over USD 12.1 Billion in annual domestic revenue from the broader metaverse sector in 2024 and expected to exceed USD 117.6 Billion by 2030, reflecting aggressive infrastructure expansion in AR/VR hardware production, massive R&D spending in spatial computing, and deployment of gaming metaverse pilots by major tech firms. Consumer adoption in China shows more than 300 million active metaverse gamers engaging with multiplayer virtual environments and in-game digital economies, while production of AR/VR headsets has scaled by more than 50% year-on-year across domestic factories.

Market Size & Growth: Valued at USD 275.65M in 2024, projected at USD 6,518.9M by 2032 with a CAGR of 48.5%; growth fueled by accelerated adoption of immersive gaming platforms.

Top Growth Drivers: Adoption of AR/VR devices rising ~60%, increase in high-speed 5G infrastructure by ~45%, blockchain/NFT-economy integration trending up ~30%.

Short-Term Forecast: By 2028, hardware cost per user expected to reduce by ~25%, and latency in networked VR gaming projected to improve (reduce) by ~40%.

Emerging Technologies: Generative AI for content creation; cloud-rendering and edge computing; cross-platform interoperability with blockchain and tokenized assets.

Regional Leaders: North America projected to reach around USD 2,000M by 2032, Asia-Pacific expected to hit ~USD 3,500M by 2032 showing fastest uptake, Europe projected ~USD 1,200M by 2032 with increasing regulatory clarity.

Consumer/End-User Trends: Young gamers (age 18-35) driving 70%+ of usage; shift from pure play to integrated metaverse behaviors (socializing, trade, virtual goods); frequent usage in mobile and wearable platforms.

Pilot or Case Example: In 2026, a major studio achieved ~35% increase in user retention via integrating real-time voice chat + spatial audio in VR metaverse game; downtime in AR/VR servers cut by ~20% through edge server deployment.

Competitive Landscape: Leading company holds approx. 30-35% hardware/software combined share; major competitors include Epic Games, Unity Technologies, Meta, Tencent, and NetEase.

Regulatory & ESG Impact: Several governments are enforcing digital asset ownership laws, data privacy protections; incentives for green data centers reducing device carbon footprint by 15-20% by 2030.

Investment & Funding Patterns: Billions in recent venture funding toward XR platforms; large alliances (tech + entertainment IP holders); increasing project finance models with revenue-sharing in virtual economies.

Innovation & Future Outlook: Motion capture, full-body avatars, haptic feedback innovations; immersive live events inside metaverse; growth in decentralized metaverse platforms enabling user control and monetization.

Key genres like adventure and role-play contribute over 50% of gameplay hours; recent product innovations include blockchain-enabled virtual land, AI-driven NPCs, and cloud streaming; economic drivers include rising disposable income in APAC, regulatory support in Asia, and tax incentives for immersive tech; future trends point to interoperability, sustainability in hardware, and deeper integration of AI in content generation.

Strategic relevance of the Metaverse Gaming Market lies in its capacity to merge entertainment, social interaction, and commerce into immersive virtual environments, offering businesses new revenue streams and competitive differentiation. By adopting cross-platform XR systems, firms can deliver up to 60% improvement in user engagement metrics compared to older standard online games. North America dominates in volume, while Asia-Pacific leads in adoption with over 40% of global user base actively using metaverse gaming platforms.

Future pathways include integration of edge computing and AI-driven personalization: by 2027, these technologies are expected to improve frame-rate stability and reduce latency by at least 30%, enhancing user experience in VR worlds. Firms are committing to ESG metric improvements such as 50% reduction in energy consumption of VR headsets by 2030 via advances in display efficiency and sustainable materials.

In 2025, in China, a leading VR game developer achieved 25% reduction in server costs through deployment of cloud-edge hybrid infrastructure. In the same year, a U.S. studio improved avatar fidelity by 40% using generative AI authoring tools compared to earlier procedural methods. Strategic partnerships are forming between IP holders and tech platform providers to leverage virtual real estate, tokenization, and live DM-driven events. The Metaverse Gaming Market is thus positioned to be a pillar of resilience, compliance, and sustainable growth as immersive digital ecosystems scale across borders and industries.

The Metaverse Gaming Market is experiencing rapid transformation driven by technological convergence of virtual reality, augmented reality, blockchain, and artificial intelligence. Widespread deployment of high-speed 5G networks and cloud infrastructure enables seamless multiplayer experiences and persistent digital worlds. Consumer behavior is shifting toward immersive entertainment, with more than 45% of global gamers engaging in metaverse platforms for social interaction, commerce, and virtual events. Strategic partnerships between gaming studios and hardware manufacturers are accelerating product innovation, while venture capital investments continue to support platform scalability and content diversity. Regulatory frameworks are evolving to address digital asset ownership, privacy, and cybersecurity, shaping the operational landscape for industry stakeholders.

Rapid adoption of immersive technologies such as advanced VR headsets, haptic feedback devices, and spatial audio systems significantly enhances player engagement in the Metaverse Gaming Market. Global shipments of standalone VR devices grew over 38% in 2024, while the number of active AR/VR users surpassed 210 million worldwide. These advancements provide highly realistic gameplay environments, boosting user retention rates by up to 55% compared to traditional gaming platforms. Integration of AI-powered content creation further streamlines the development of expansive virtual worlds, enabling faster release cycles and richer experiences. As consumers seek deeper social connectivity and interactive storytelling, these innovations continue to propel market expansion across both developed and emerging economies.

Data privacy risks and cybersecurity threats present significant barriers to growth in the Metaverse Gaming Market. Players routinely exchange sensitive personal information and digital assets within virtual environments, creating attractive targets for cyberattacks. In 2024 alone, global gaming platforms reported a 25% increase in breaches involving digital wallet theft and identity fraud. Complex international data protection regulations, such as varying regional compliance requirements, increase operational costs for developers and platform providers. Additionally, maintaining robust encryption and real-time threat detection systems requires substantial investment and skilled personnel, slowing platform scalability. These challenges may reduce consumer confidence and limit adoption unless addressed through stringent security protocols and transparent user data policies.

Decentralized economies built on blockchain technology present major opportunities for the Metaverse Gaming Market. Non-fungible tokens (NFTs) and decentralized marketplaces allow players to own, trade, and monetize in-game assets, creating sustainable revenue streams and user engagement. In 2024, NFT-related gaming transactions exceeded USD 5 billion globally, reflecting robust demand for player-owned digital goods. Smart contract functionality enables secure peer-to-peer transactions, reducing reliance on centralized intermediaries and fostering creative ecosystems. Brands and entertainment franchises are increasingly leveraging these mechanics to launch branded virtual merchandise and unique experiences. This evolution expands monetization pathways for developers and empowers gamers with true asset ownership, reinforcing long-term market growth.

High hardware costs and infrastructure demands remain critical challenges for the Metaverse Gaming Market. Advanced VR headsets with full-motion tracking and high-resolution displays often exceed USD 500, creating affordability barriers in price-sensitive regions. Additionally, delivering smooth, low-latency gameplay requires stable broadband exceeding 100 Mbps and robust cloud computing resources, which are still limited in many developing countries. Data centers supporting real-time rendering must invest in energy-efficient cooling systems and high-performance GPUs, adding to capital expenditures. Supply chain disruptions for semiconductor components further exacerbate cost pressures, delaying hardware availability. These factors collectively hinder widespread adoption, particularly in regions lacking strong digital infrastructure or facing currency fluctuations that inflate device pricing.

Expanded Cross-Platform Play Integration: Cross-platform capability is accelerating user engagement, with over 68% of active metaverse gamers in 2025 playing seamlessly across console, PC, and mobile. Unified matchmaking systems have increased average playtime per user by 35%, while cross-device purchases rose 28% year-on-year, highlighting demand for flexible access and persistent digital identities.

AI-Driven Content Personalization: Artificial intelligence is enabling dynamic, player-specific experiences. In 2024, approximately 42% of leading metaverse games adopted AI algorithms to adapt storylines in real time, raising session retention by 31%. Personalized virtual events generated a 25% uplift in microtransaction purchases, demonstrating measurable monetization opportunities for developers and publishers.

Growth in Haptic and Sensory Feedback Hardware: Advanced haptic suits and gloves recorded a 47% surge in shipments during 2024, delivering full-body feedback that deepens immersion. Gamers using these devices reported a 40% increase in perceived realism, while e-sports tournaments integrating haptic tech observed a 22% rise in competitive participation, supporting broader hardware adoption.

Blockchain-Enabled Asset Ownership: Integration of blockchain-based digital assets is reshaping in-game economies. By 2025, more than 55% of major metaverse titles offered NFT-backed items, with user-to-user transactions growing 60% annually. Tokenized ownership led to a 33% jump in secondary market trading, creating sustainable revenue streams and enhancing player loyalty.

The Metaverse Gaming Market is segmented by type, application, and end-user demographics, reflecting diverse technological approaches and usage patterns. Types include immersive hardware, gaming platforms, and blockchain-based environments, each attracting unique developer and consumer bases. Applications span entertainment, education, retail marketing, and professional collaboration, revealing a shift from purely recreational gaming to multifunctional virtual ecosystems. End-user adoption ranges from individual gamers to large enterprises and educational institutions, with increasing participation from retail brands and social media companies. This varied segmentation illustrates a dynamic landscape where immersive technologies and decentralized economies intersect, offering stakeholders multiple pathways to capture and sustain engagement.

Hardware-based platforms currently account for approximately 46% of global adoption, driven by rising demand for high-fidelity VR headsets and motion-tracking systems that elevate gameplay realism. Software-driven ecosystems follow with around 32% share, fueled by rapid development of immersive game engines and AI-enhanced worlds. Blockchain-integrated platforms, though at 22% share, are the fastest-growing type, with an estimated 29% CAGR as NFTs and decentralized ownership redefine value creation in virtual gaming. Emerging formats such as mixed-reality systems contribute a combined 8% niche share, appealing to specialized enterprise applications.

Entertainment dominates with about 58% share, supported by high user demand for interactive storytelling and large-scale multiplayer environments. Education and training applications represent 20%, integrating immersive simulations for skill-building and remote learning. Virtual retail marketing holds 15%, while professional collaboration tools make up the remaining 7%. Education is the fastest-growing segment with a projected 26% CAGR as universities adopt immersive classrooms and corporations expand VR-based employee training. In 2024, more than 38% of enterprises globally reported piloting Metaverse Gaming systems for customer engagement platforms, while 64% of Gen Z consumers indicated preference for brands utilizing virtual worlds for product discovery.

Individual gamers represent the leading end-user segment with roughly 55% adoption, driven by continuous hardware innovation and accessible subscription models. Enterprise adoption stands at 25%, reflecting strong interest from entertainment studios, retailers, and event organizers seeking immersive marketing and customer engagement tools. Educational institutions hold a 12% share, while government and non-profit organizations collectively contribute 8%. Enterprises are the fastest-growing end-user group with an anticipated 28% CAGR as brands integrate metaverse storefronts and host virtual events to boost customer loyalty. In 2024, over 40% of retail companies reported experimenting with metaverse-enabled product launches, while 60% of Gen Z consumers expressed higher trust in brands incorporating immersive experiences.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 49% between 2025 and 2032.

North America led with more than 120 million active metaverse gamers and strong enterprise adoption in finance, healthcare, and entertainment. Asia-Pacific followed with a 32% share, driven by rapid AR/VR device production and over 300 million active players across China, India, and Japan. Europe secured 20% of global volume, supported by stringent data-privacy regulations and rising esports investments. South America captured 6% with Brazil holding 3% alone, while the Middle East & Africa held 4% amid accelerating digital transformation and 5G deployments in the UAE and South Africa.

North America holds approximately 38% of the global Metaverse Gaming Market, supported by high enterprise adoption across healthcare, finance, and media. Strong federal and state incentives encourage 5G expansion and cloud gaming platforms, enabling low-latency immersive experiences. Notable player Meta Platforms invests heavily in VR hardware manufacturing and AI-driven gaming ecosystems, while U.S. consumers show a 60% preference for multiplayer VR games over traditional online formats. Regional consumer behavior highlights higher enterprise demand for virtual training solutions and large-scale e-sports events, making North America a central hub for premium content development and cross-platform gaming innovation.

Europe commands about 20% market share, with Germany, the UK, and France as primary contributors to metaverse gaming adoption. The European Union’s strict GDPR regulations drive demand for privacy-compliant virtual platforms and explainable AI features. Regional initiatives emphasize sustainability, with green data-center operations reducing energy use by nearly 18% in key markets. Companies such as Ubisoft are integrating blockchain-based in-game assets and launching immersive multiplayer events. Consumer trends indicate a 35% rise in subscription-based VR gaming, driven by regulatory confidence and government-backed digital innovation programs that support cross-border virtual economies.

Asia-Pacific accounts for around 32% of global volume and ranks first in growth pace, fueled by over 300 million active gamers across China, India, Japan, and South Korea. Advanced manufacturing hubs in China produce more than 55% of global VR headsets, while India shows a 40% annual increase in mobile-based VR gaming users. Regional innovation clusters in Tokyo and Shenzhen are pioneering AI-driven NPC technology and large-scale e-sports tournaments. Consumer behavior demonstrates high adoption of e-commerce-linked gaming platforms and mobile payment integration, with over 65% of players purchasing virtual goods directly through mobile wallets.

South America captures about 6% market share, with Brazil representing nearly 3% alone through rapidly growing e-sports and streaming communities. Government incentives for tech startups and improved broadband access have enabled broader VR platform deployment. Local developers in Brazil are creating language-localized content and culturally tailored virtual events, increasing user retention by 25%. Consumer preferences lean toward community-based multiplayer experiences and localized payment systems, while Argentina shows strong uptake of mobile gaming platforms integrated with metaverse features.

The Middle East & Africa collectively hold approximately 4% market share, led by the UAE and South Africa. Large-scale 5G network rollouts and smart city initiatives are catalyzing adoption of immersive gaming platforms. Dubai-based gaming firms are launching VR arcades and metaverse-linked e-commerce experiences, while local regulations encourage blockchain-based digital economies. Regional consumers show high interest in social VR gatherings and competitive gaming, with a 28% year-on-year increase in multiplayer participation, especially in Gulf countries investing in entertainment diversification.

United States – 25% market share: Dominates due to advanced digital infrastructure, extensive content creation, and strong enterprise adoption in healthcare and entertainment.

China – 21% market share: Leads in large-scale VR headset manufacturing and massive gamer base exceeding 200 million active metaverse users, supported by robust investment in AI-driven immersive platforms.

The Metaverse Gaming Market is moderately consolidated, with the top five companies collectively holding about 42% of global market share in 2024. Over 120 active competitors operate worldwide, ranging from major technology conglomerates to specialized AR/VR startups. Industry leaders focus on strategic mergers, content partnerships, and platform interoperability to strengthen their market positions. In 2024 alone, more than 50 notable product launches were recorded, including next-generation VR headsets with 8K resolution and AI-driven real-time rendering engines. Competitive strategies emphasize blockchain integration, cross-platform ecosystems, and proprietary avatar-creation tools to differentiate user experiences. Innovation remains a key battleground, with nearly 60% of leading firms investing in generative AI for dynamic world-building and adaptive gameplay. Emerging entrants are leveraging niche offerings such as haptic-feedback accessories and decentralized metaverse marketplaces to capture early adopters. Continuous capital inflows from venture funds—estimated at over USD 8 billion globally—underscore the sector’s robust growth trajectory and heighten competitive intensity across regions.

Roblox Corporation

Tencent Holdings

NetEase Inc.

Sony Interactive Entertainment

Microsoft Corporation

Decentraland

The Sandbox

The Metaverse Gaming Market is being reshaped by a convergence of advanced technologies that enhance immersion, scalability, and interactivity. Cloud-based GPU rendering enables real-time 3D graphics at ultra-high frame rates, supporting multiplayer environments with up to 100,000 concurrent users per server. Augmented Reality (AR) and Virtual Reality (VR) headsets now feature 8K resolution displays with 120 Hz refresh rates, reducing motion sickness and delivering lifelike visuals. Artificial Intelligence drives adaptive gameplay through procedural content generation, while natural language processing allows seamless voice-based interactions between players and non-player characters. Blockchain technology supports decentralized economies, with more than 25 million active blockchain-based gaming wallets recorded globally in 2024. Haptic feedback suits and gloves, capable of simulating temperature changes and pressure variations, enhance physical engagement within virtual worlds. Spatial audio technology with 360-degree sound mapping provides realistic acoustic experiences critical for competitive gaming. Edge computing minimizes latency to under 20 milliseconds, essential for fast-paced action genres. Additionally, cross-platform engines such as Unreal Engine 5 and Unity’s HDRP facilitate the creation of photorealistic environments and multi-device compatibility. These innovations collectively drive market growth, enabling enterprises to deliver richer, more interactive, and scalable metaverse gaming experiences for a global audience.

• In February 2024, Epic Games announced a new Unreal Engine upgrade with real-time path tracing, enabling photorealistic environments and supporting simultaneous gameplay for over 80,000 users in persistent metaverse worlds. Source: www.epicgames.com

• In September 2023, Meta Platforms launched Quest 3 VR headsets featuring pancake optics and full-color passthrough, improving visual fidelity by 30% and reducing headset weight by 15% compared to Quest 2. Source: www.meta.com

• In March 2024, Microsoft integrated generative AI into Xbox Cloud Gaming, allowing dynamic NPC dialogue creation and real-time world-building for large-scale multiplayer environments. Source: www.microsoft.com

• In July 2023, Roblox introduced layered clothing technology for avatars, enabling customizable multi-layer outfits and recording a 40% increase in user-generated content within three months of release. Source: www.roblox.com

The Metaverse Gaming Market Report provides a comprehensive analysis of the industry’s structure, covering technology, application, and geographic segmentation to guide strategic decision-making. It examines core components such as AR/VR hardware, game engines, blockchain frameworks, and AI-driven analytics that underpin immersive metaverse environments. Key application areas include social gaming, esports tournaments, virtual real estate development, and enterprise training simulations, with market dynamics assessed across consumer, commercial, and industrial use cases.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional adoption patterns, infrastructure readiness, and regulatory landscapes. It explores platform-specific insights for PC, console, and mobile ecosystems, noting their contribution to active player bases exceeding 400 million globally in 2024.

The scope extends to emerging niches such as decentralized autonomous organizations (DAOs) managing virtual economies, AI-powered world-building tools, and haptic-feedback peripherals enhancing user immersion. Competitive analysis covers market concentration, innovation pipelines, and strategic collaborations, with attention to startups driving unique monetization models like play-to-earn. By integrating quantitative data and qualitative trends, the report offers a holistic perspective for investors, developers, and policymakers aiming to capitalize on the rapid evolution of metaverse gaming worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 275.65 Million |

|

Market Revenue in 2032 |

USD 6518.9 Million |

|

CAGR (2025 - 2032) |

48.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Meta Platforms, Epic Games, Unity Technologies, Roblox Corporation, Tencent Holdings, NetEase Inc., Sony Interactive Entertainment, Microsoft Corporation, Decentraland, The Sandbox |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |