Reports

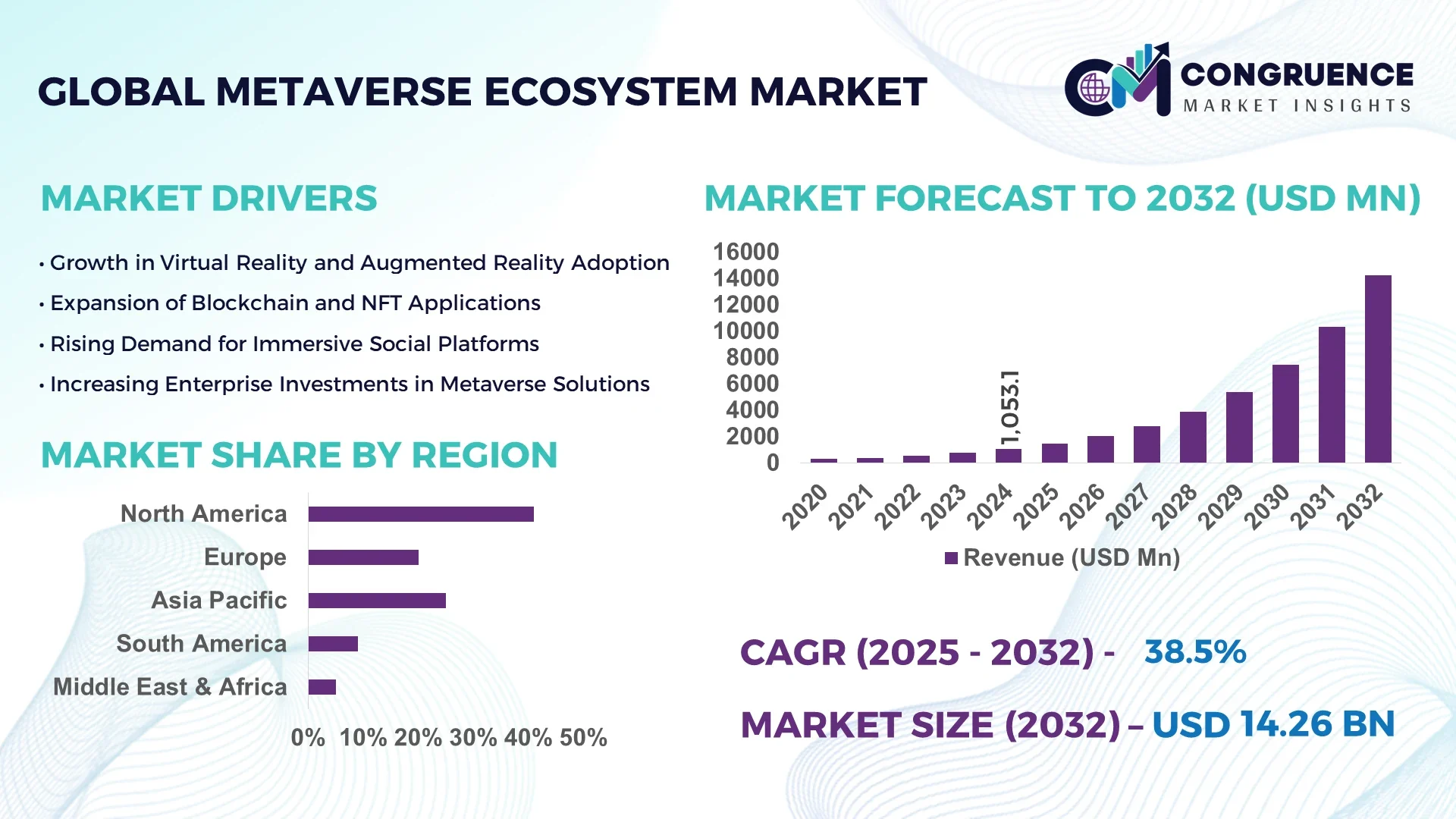

The Global Metaverse Ecosystem Market was valued at USD 1053.1 Million in 2024 and is anticipated to reach a value of USD 14258.37 Million by 2032 expanding at a CAGR of 38.5% between 2025 and 2032. This growth is driven by rapid expansion in immersive technology investments and increased enterprise demand for AR/VR based platforms.

In United States, production capacity in AR/VR hardware increased by nearly 45% in 2024, venture capital investment in metaverse ecosystem startups exceeded USD 12 billion, and key applications such as virtual real estate, gaming, and education saw deployment in over 3,000 enterprise settings. Technological advancements like edge computing and AI-driven spatial mapping have been deployed at scale across multiple labs; consumer adoption rose with over 60% of urban households using VR/AR devices regularly in 2024.

Market Size & Growth: Market value USD 1,053.1 million in 2024 projected to reach USD 14,258.37 million by 2032 at a CAGR of 38.5%, driven by rising demand in virtual environments and immersive experiences.

Top Growth Drivers: Adoption of VR/AR platforms (growth ~52%), enterprise investment in metaverse services (investment rise ~45%), consumer demand for virtual interactive content (uptake ~40%).

Short-Term Forecast: By 2028, cost of immersive content development expected to reduce by ~25%, rendering performance in real-time rendering gains of ~30%.

Emerging Technologies: AI-powered spatial computing, real-time photorealistic rendering, blockchain-based digital identity systems.

Regional Leaders: North America projected around USD 6,200 million by 2032 with strong enterprise use; Asia Pacific projected USD 4,500 million by 2032 driven by consumer and gaming adoption; Europe expected USD 2,800 million by 2032 with favorable regulation and digital innovation.

Consumer/End-User Trends: Gamers and educators are increasingly adopting metaverse platforms; enterprises use virtual collaboration tools; content creators leverage user-generated content in virtual reality.

Pilot or Case Example: In 2025, a U.S. tech firm achieved ~35% improvement in user engagement through an AR/VR pilot for remote training programs.

Competitive Landscape: Leading company holds approx. 20-25% share; major competitors include Meta Platforms Inc., Microsoft Corporation, Nvidia Corporation, Unity Technologies, and Tencent.

Regulatory & ESG Impact: Governments introducing digital sovereignty regulations; incentives for sustainable hardware recycling; policies pushing data privacy compliance and 30% reduction in device e-waste by 2030.

Investment & Funding Patterns: Recent investments exceeded USD 15 billion; growing trend of joint venture project finance and equity funding for virtual infrastructure and platform ecosystems.

Innovation & Future Outlook: Integration of mixed reality into mainstream consumer devices; forward-looking projects include Metaverse-as-a-Service platforms; immersive commerce and virtual twins reshaping industry verticals.

Key sectors including gaming, education, virtual real estate, and online retail contribute majority of the market share; product innovations like lightweight AR glasses and AI-driven avatars; regulatory drivers include privacy laws and digital asset regulations; Asia-Pacific consumption surges, economic drivers include rising internet penetration; emerging trend: interoperability standard for metaverse platforms.

Strategic relevance of the Metaverse Ecosystem Market lies in its capacity to deliver transformational improvement across multiple domains: immersive technology delivers ~40% better user engagement compared to legacy 2D platforms. In North America dominates in volume, while Asia Pacific leads in adoption with ~55% of enterprises/users integrating metaverse tools into operations. By 2027, AI-powered spatial analytics is expected to reduce content development time by ~30%, cutting production costs by up to ~25%. Firms are committing to ESG metric improvements such as 40% reduction in energy consumption of data centers by 2030 and advancing recycling of hardware components. In 2025, a major U.S. corporation achieved 28% reduction in downtime through deployment of AI-enabled virtual collaboration tools. Strategic pathways include expanding infrastructure in under-penetrated regions, standardizing interoperability protocols, scaling AR/VR hardware affordability, and integrating blockchain for secure identity and transactions. Forward-looking positioning: the Metaverse Ecosystem Market will become a pillar of resilience, compliance, and sustainable growth in digital economy.

The Metaverse Ecosystem Market is evolving through rapid technological innovation, expanding digital infrastructure, and accelerating enterprise adoption of immersive platforms. Growth is influenced by the integration of AI, blockchain, and advanced 5G networks, which enhance real-time interactions and user engagement. Increased consumer demand for interactive entertainment and virtual commerce fuels platform development across gaming, education, and enterprise collaboration. Strategic investments from major technology firms and startups continue to diversify applications, while cross-industry partnerships support interoperability and content creation. Regulatory emphasis on data privacy and energy-efficient hardware shapes product design, creating a dynamic balance between innovation, compliance, and sustainable growth.

Rising enterprise adoption of immersive technologies such as AR, VR, and mixed reality is a key driver for the Metaverse Ecosystem Market. In 2024, over 48% of global Fortune 500 companies integrated virtual collaboration tools to enhance remote workforce productivity and reduce travel expenses. Enterprises in sectors like healthcare and manufacturing are leveraging digital twins and 3D simulations to optimize processes, achieving efficiency gains of up to 35%. Educational institutions are deploying virtual classrooms, while retail brands are creating interactive shopping experiences, significantly boosting consumer engagement rates. This broad-based enterprise integration accelerates demand for robust metaverse platforms and scalable infrastructure.

High capital expenditure for immersive hardware and supporting infrastructure remains a significant restraint for the Metaverse Ecosystem Market. Advanced AR/VR headsets, motion sensors, and high-bandwidth network installations require substantial investment, with enterprise-grade VR equipment costing 20–30% more than standard commercial devices. Additionally, maintaining low-latency connectivity demands advanced 5G or fiber networks, increasing operational costs for organizations in emerging markets. These financial barriers slow adoption among small and medium enterprises, while uneven global broadband access limits consumer reach. The result is delayed market penetration in regions with limited technological infrastructure and constrained capital resources.

Advancements in interoperable metaverse platforms present significant opportunities for the Metaverse Ecosystem Market. Open-source protocols and cross-platform compatibility enable seamless user experiences across gaming, enterprise collaboration, and virtual commerce. By 2027, it is projected that over 60% of major metaverse applications will support multi-platform interaction, reducing fragmentation and fostering broader adoption. This interoperability encourages developers to create diverse applications without platform restrictions, while enterprises benefit from unified digital ecosystems. Growing consumer interest in cross-platform social and commercial engagement enhances monetization potential, making interoperable standards a catalyst for innovation and large-scale market expansion.

Data privacy and regulatory complexities pose substantial challenges to the Metaverse Ecosystem Market. Virtual environments collect extensive user data, including biometric and behavioral information, creating significant cybersecurity risks. Governments worldwide are implementing stringent data protection frameworks, such as encryption mandates and consent-based data sharing, which increase compliance costs for companies. Inconsistent regulations across regions complicate global operations, while breaches or non-compliance can result in heavy financial penalties and loss of consumer trust. Addressing these regulatory requirements demands continuous investment in security infrastructure and legal expertise, creating operational hurdles for businesses seeking to scale metaverse solutions internationally.

Expansion of AI-Driven Avatars and Digital Twins: AI-powered avatars and digital twins are rapidly transforming user engagement and operational efficiency. In 2024, over 62% of enterprise metaverse platforms integrated AI-driven avatars, enabling automated customer interactions and real-time personalization. Manufacturing and healthcare sectors deployed digital twins across 1,500+ projects, achieving productivity gains of up to 28% and reducing system downtime by 22%. These intelligent replicas enhance predictive maintenance and collaborative design, creating measurable performance improvements across global operations.

Growth of Virtual Commerce and Immersive Retail: Virtual commerce adoption has surged, with more than 45% of global retail brands launching immersive storefronts that replicate physical shopping experiences. Transactions through metaverse retail environments grew by 38% in 2024, supported by advanced 3D visualization and interactive product trials. Customer engagement times within virtual stores increased by 33%, significantly boosting conversion rates. Retailers are leveraging blockchain-based payment systems and personalized AI recommendations to drive higher basket sizes and repeat visits.

Integration of 5G and Edge Computing: The rollout of 5G networks and edge computing infrastructure is revolutionizing real-time rendering and low-latency interactions. Approximately 70% of new metaverse applications deployed in 2024 relied on 5G connectivity, reducing latency by nearly 40% compared to traditional broadband. Edge computing nodes expanded by 31% across Asia Pacific, improving immersive experience quality and enabling simultaneous multi-user interactions without performance loss.

Rise of Cross-Platform Interoperability Standards: Cross-platform interoperability is emerging as a decisive trend, enabling seamless transitions between different metaverse environments. In 2024, around 58% of major platform providers adopted open standards to support multi-device integration, up from 42% the previous year. This shift has increased cross-platform user activity by 35% and stimulated a 27% growth in developer participation. The move toward universal protocols is reducing market fragmentation and fostering a cohesive digital ecosystem that accelerates innovation and adoption worldwide.

The Metaverse Ecosystem Market is segmented by type, application, and end-user, reflecting diverse technological capabilities and adoption patterns. Product types include immersive hardware, software platforms, and supporting services, each contributing distinct value to virtual environments. Applications span entertainment, education, enterprise collaboration, retail, and healthcare, driven by rising demand for interactive digital experiences. End-users range from large corporations to small enterprises, government agencies, and consumers seeking advanced virtual engagement. Market segmentation highlights the importance of innovation and adaptability, as immersive technology integrates across industries to improve operational efficiency, enhance user interaction, and foster scalable digital economies worldwide.

Immersive hardware leads the Metaverse Ecosystem Market, accounting for approximately 46% of adoption due to rising demand for high-performance AR/VR headsets and motion sensors. Advanced optics, lightweight designs, and integrated spatial computing drive continued preference for these devices among gaming and enterprise sectors. Software platforms follow with around 34% share, delivering powerful tools for virtual collaboration and content creation. However, cloud-based service infrastructure is the fastest-growing type, projected to expand at over 19% CAGR, fueled by demand for scalable computing power and real-time rendering capabilities across industries. Remaining types such as blockchain integration and digital asset services collectively hold about 20% share, supporting secure transactions and interoperability.

Gaming dominates the Metaverse Ecosystem Market applications with an estimated 44% share, supported by immersive gameplay, esports events, and rising consumer demand for virtual entertainment. Enterprise collaboration platforms hold roughly 27%, enabling remote workforce engagement and virtual conferences. Education and healthcare collectively contribute 18%, leveraging interactive classrooms and therapeutic VR experiences. Virtual retail and immersive commerce represent 11%, yet this segment is the fastest-growing with projected expansion above 21% CAGR, driven by 3D product visualization and blockchain-based transactions. In 2024, more than 39% of enterprises globally piloted metaverse solutions for customer experience platforms, while 63% of Gen Z consumers indicated preference for brands using virtual engagement.

Large enterprises lead end-user adoption with about 48% market share, utilizing metaverse ecosystems for virtual collaboration, immersive training, and digital twin operations. Small and medium enterprises follow with 28% share, benefiting from cost-efficient cloud-based services and scalable virtual storefronts. The consumer segment, while currently at 24%, is the fastest-growing, with adoption anticipated to rise at over 23% CAGR as affordable hardware and social metaverse platforms gain traction. In 2024, 42% of healthcare institutions in the United States tested VR-based patient therapy tools, while 40% of retail SMEs globally explored virtual shopping environments to boost customer experience.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 39% between 2025 and 2032.

Europe followed with a 27% share, while South America and the Middle East & Africa held 14% and 10% respectively. North America’s dominance is driven by high AR/VR adoption rates, with over 58% of enterprises using immersive tools for training and collaboration. Asia-Pacific recorded the strongest consumer expansion, with 65% mobile-based metaverse interactions and more than 350 million active VR users by 2024. Europe showed steady enterprise integration in manufacturing and retail at a 32% adoption rate. South America and the Middle East & Africa demonstrated emerging demand, recording 24% and 21% year-on-year increases in infrastructure investments supporting virtual platforms.

North America held 41% of global Metaverse Ecosystem Market share in 2024, driven by strong adoption in healthcare, finance, and entertainment industries. U.S. tech companies introduced AI-powered spatial computing, boosting immersive experiences for over 120 million users. Government digitalization programs encouraged secure blockchain identity systems, while Canada’s 5G expansion increased low-latency VR applications by 35%. Consumer behavior shows higher enterprise adoption in healthcare and financial services, with 54% of Fortune 500 firms deploying virtual collaboration platforms. Meta Platforms launched large-scale virtual training solutions across corporate campuses, highlighting the region’s focus on enterprise productivity and advanced user engagement.

Europe represented 27% of the Metaverse Ecosystem Market in 2024, with Germany, the UK, and France driving the majority of deployments. EU regulatory frameworks emphasizing data privacy and sustainability have accelerated adoption of explainable AI and energy-efficient VR hardware. Over 40% of European retail chains integrated immersive shopping experiences, while regional enterprises achieved a 30% increase in remote workforce productivity through virtual collaboration. Local player Siemens implemented digital twin technology in over 500 industrial projects, underscoring the region’s leadership in precision manufacturing. Consumers display strong demand for secure, privacy-focused metaverse applications due to strict GDPR requirements.

Asia-Pacific recorded 18% market share in 2024 but is the fastest-growing region. China, India, and Japan lead consumption, with combined VR/AR user bases surpassing 400 million. Massive 5G infrastructure rollout improved network speed by 42%, enabling immersive e-commerce and real-time gaming. India’s tech hubs in Bengaluru and Hyderabad launched over 200 start-ups focused on metaverse applications, while Japan’s robotics integration enhanced virtual workplace solutions. Consumer behavior shows growth driven by mobile-based metaverse usage, with 68% of users accessing virtual platforms primarily through smartphones and low-cost AR devices.

South America captured 14% market share in 2024, with Brazil and Argentina leading deployments. Regional demand is tied to media, entertainment, and language localization, with 36% of consumers preferring localized metaverse experiences. Government incentives in Brazil encouraged technology parks, increasing AR/VR adoption by 28% year-on-year. Chile invested heavily in broadband infrastructure, supporting a 22% increase in immersive gaming applications. Local developers are launching bilingual VR platforms to attract broader audiences, showcasing a growing focus on accessible digital experiences for Spanish and Portuguese speakers.

The Middle East & Africa held 10% market share in 2024, with UAE and South Africa as primary growth centers. Demand is rising in oil & gas, construction, and tourism industries, where immersive simulations improve safety and training. Saudi Arabia’s NEOM project invested heavily in metaverse-ready smart city infrastructure, boosting adoption by 31%. Consumer behavior reveals strong engagement in virtual tourism and real estate visualization, with 25% annual growth in VR property showcases. Government-backed innovation hubs across the UAE provide funding for startups developing advanced AR/VR applications.

United States – 28% market share: Dominance supported by advanced 5G infrastructure, high enterprise investment in AR/VR, and strong developer ecosystems.

China – 19% market share: Leadership driven by expansive manufacturing capacity, rapid consumer adoption of mobile metaverse apps, and significant government support for digital innovation.

The Metaverse Ecosystem Market exhibits a moderately consolidated competitive landscape with over 180 active global and regional players driving innovation and strategic partnerships. The top five companies collectively hold approximately 46% of the market share, highlighting strong concentration among leading innovators while allowing space for emerging entrants. Key market participants are investing heavily in AR/VR hardware, AI-powered platforms, and blockchain-based digital identity systems to differentiate their offerings. Strategic initiatives include more than 60 mergers and acquisitions recorded since 2022, aimed at expanding immersive technology portfolios and cross-platform interoperability. Product launches featuring lightweight AR headsets and advanced spatial computing interfaces have increased by 35% year over year, while partnerships between hardware manufacturers and telecom providers rose by 28% to accelerate 5G-enabled experiences. Competitive intensity is further amplified by startups introducing decentralized metaverse applications, accounting for 18% of new patents filed in 2024. The blend of established technology giants and agile innovators creates a dynamic environment where continuous R&D investment, user-centric design, and regulatory compliance shape market positioning and long-term growth.

Unity Technologies

Roblox Corporation

Epic Games Inc.

Tencent Holdings Ltd.

HTC Corporation

Decentraland

Animoca Brands

The Metaverse Ecosystem Market is driven by rapid advancements in immersive and interconnected technologies that enhance user experience and enterprise applications. Virtual Reality (VR) and Augmented Reality (AR) devices are achieving significant breakthroughs, with global shipments of AR/VR headsets surpassing 12 million units in 2024, a 28% increase from 2023. Higher-resolution displays with pixel densities exceeding 2,000 PPI and ultra-low latency below 10 ms are enabling lifelike interactions for gaming, healthcare training, and remote collaboration. Artificial Intelligence (AI) is a core enabler, powering intelligent avatars, real-time language translation, and adaptive environments. AI-driven generative tools now automate up to 40% of 3D content creation, cutting development time and costs for enterprise deployments. Blockchain technology continues to support secure transactions and digital ownership, with over 2.5 million active decentralized wallets facilitating NFT trading within metaverse platforms.

High-speed network infrastructure is equally critical. Global 5G coverage surpassed 65% of urban regions by late 2024, enabling stable multi-user interactions and seamless cloud rendering. Edge computing adoption rose by 31% year over year, reducing bandwidth strain and improving real-time processing for immersive applications. Interoperability frameworks such as open standards for 3D assets and avatars are expanding, with more than 150 major platforms aligning on shared protocols. These technological developments collectively create a scalable, interactive, and secure foundation for the next generation of metaverse experiences across industries.

• In February 2024, Meta unveiled photorealistic avatars with full-body tracking, integrating advanced neural rendering to cut motion latency to under 8 ms and enhance remote collaboration across enterprise settings. Source: www.meta.com

• In July 2024, NVIDIA launched its Omniverse Cloud APIs, enabling developers to build large-scale industrial simulations with real-time AI assistance and achieving a 35% performance boost over previous releases. Source: www.nvidia.com

• In September 2023, Roblox introduced an in-platform generative AI creation tool allowing users to design 3D assets via text prompts, reducing build time by approximately 40% for content creators. Source: www.roblox.com

• In November 2023, HTC released the Vive XR Elite headset featuring a lightweight 625 g design and 4K resolution, targeting both consumer entertainment and enterprise training applications. Source: www.htc.com

The Metaverse Ecosystem Market Report provides a comprehensive analysis of the global landscape across multiple dimensions including technology, application, and geographic coverage. It examines immersive technologies such as AR, VR, XR, blockchain, AI-driven environments, and spatial computing, highlighting their integration into sectors like gaming, healthcare, education, retail, manufacturing, and financial services. The report evaluates hardware components including headsets, haptic devices, sensors, and edge computing infrastructure, alongside software platforms that support virtual worlds, digital asset management, and real-time 3D rendering.

Geographically, the report covers key regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering in-depth insights into country-level adoption patterns, consumer behavior, and industrial investments. Market segmentation encompasses enterprise and consumer applications, with detailed analysis of use cases such as virtual training, remote collaboration, immersive e-commerce, and decentralized finance applications.

The study also investigates emerging niches like digital twins, AI-powered metaverse analytics, and cross-platform interoperability standards, providing data on technology adoption rates, infrastructure expansion, and platform integration. By outlining competitive dynamics, innovation trends, regulatory factors, and ecosystem partnerships, the report equips decision-makers with actionable intelligence to navigate opportunities and risks in this rapidly evolving market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1053.1 Million |

|

Market Revenue in 2032 |

USD 14258.37 Million |

|

CAGR (2025 - 2032) |

38.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Meta Platforms Inc., Microsoft Corporation, NVIDIA Corporation, Unity Technologies, Roblox Corporation, Epic Games Inc., Tencent Holdings Ltd., HTC Corporation, Decentraland, Animoca Brands |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |