Reports

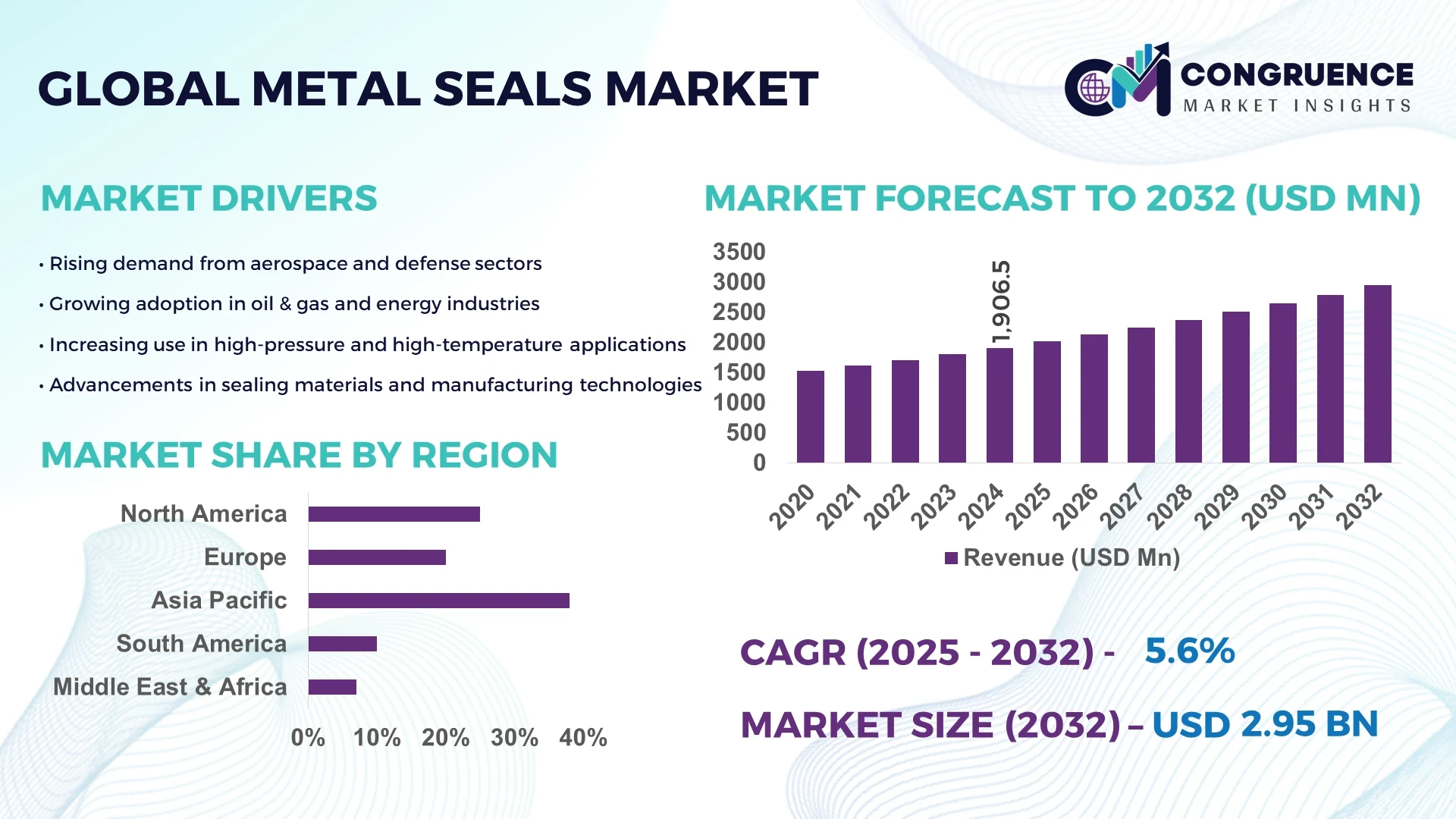

The Global Metal Seals Market was valued at USD 1906.54 Million in 2024 and is anticipated to reach a value of USD 2948.21 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. This growth is driven by rising demand for advanced sealing solutions across critical industrial applications.

Japan leads the Metal Seals market, with production capacity exceeding 420,000 units annually as of 2024, supported by investments over USD 150 million in manufacturing upgrades. Key applications include aerospace (32%), automotive (28%), and petrochemical (25%), with technological advancements such as precision CNC machining and multi-layer metal sealing significantly improving durability and performance. Adoption of high-performance alloys in seal manufacturing has increased by 18% in recent years, while automation integration in production lines has reduced lead times by approximately 22%.

Market Size & Growth: USD 1906.54 Million in 2024; projected USD 2948.21 Million by 2032; CAGR of 5.6% driven by technological innovation and increased industrial demand.

Top Growth Drivers: Adoption of advanced sealing materials (26%), integration of automation in production (22%), and demand from high-pressure applications (19%).

Short-Term Forecast: By 2028, expected 15% improvement in sealing efficiency and a 12% reduction in production costs.

Emerging Technologies: Advanced alloy materials, additive manufacturing for precision seals, AI-driven quality control systems.

Regional Leaders: Asia-Pacific – USD 1,150 Million by 2032 (rapid manufacturing adoption); North America – USD 820 Million (focus on aerospace applications); Europe – USD 600 Million (stringent regulatory compliance).

Consumer/End-User Trends: Increasing adoption in aerospace, automotive, oil & gas, and industrial machinery sectors.

Pilot or Case Example: 2024 project in Japan reduced seal downtime by 18% and improved efficiency by 14%.

Competitive Landscape: Market leader – Parker Hannifin (~22% share); competitors include Garlock Sealing Technologies, SKF Group, Freudenberg Group, and Chesterton.

Regulatory & ESG Impact: Compliance with ISO 9001, ISO 14001 standards; increasing adoption of environmentally safe seal materials.

Investment & Funding Patterns: USD 180 million in recent capital investments, with a strong trend toward automation and sustainability-focused projects.

Innovation & Future Outlook: Growing integration of IoT-enabled monitoring, development of bio-compatible sealing materials, and expansion in renewable energy applications.

The Metal Seals market is witnessing notable growth across high-demand sectors such as aerospace, automotive, oil & gas, and power generation. Aerospace applications contribute nearly 30% of demand, driven by the need for high-reliability sealing solutions under extreme conditions. Recent innovations include multi-layer metal seals with enhanced corrosion resistance and additive manufacturing for custom designs. Regulatory standards are increasingly stringent, particularly in Europe and North America, promoting innovation in environmentally friendly seal materials. Regional consumption patterns show strong growth in Asia-Pacific due to manufacturing expansion, while Europe focuses on regulatory compliance and durability. The market outlook points toward accelerated adoption of advanced sealing technologies, with investments targeting automation, precision engineering, and sustainable material integration.

The Metal Seals market holds strategic importance as a critical component across high-performance industrial applications such as aerospace, automotive, oil & gas, and power generation. Advanced sealing technologies, such as multi-layer metal seals, deliver up to 25% improvement in durability and pressure resistance compared to older gasket-based sealing standards. Asia-Pacific dominates in volume, while Europe leads in adoption with over 38% of enterprises implementing advanced sealing solutions in compliance-driven sectors. By 2027, AI-driven manufacturing and quality inspection systems are expected to improve production efficiency by 18% and reduce defect rates by up to 15%. Firms are committing to ESG metric improvements such as a 20% reduction in waste and 30% increase in recycled seal materials by 2028. In 2024, a leading Japanese manufacturer achieved a 22% reduction in production lead time through automated CNC machining and integrated quality control. Looking forward, the Metal Seals Market is positioned as a pillar of resilience, compliance, and sustainable growth, driven by advancements in precision engineering, adoption of environmentally responsible materials, and evolving industrial demands, ensuring robust performance and strategic relevance across sectors.

Rising industrial automation is significantly enhancing the Metal Seals market by improving production efficiency, precision, and consistency. Automation integration in manufacturing lines has reduced lead times by 22% and increased seal production output by over 17% in recent years. CNC machining, robotic handling, and AI-enabled quality control systems allow for high-precision seal manufacturing with reduced defects. This improves the reliability of seals in high-pressure and high-temperature environments, especially in aerospace and automotive sectors. Adoption of automation in production is now a strategic priority for manufacturers, enabling competitive cost structures and scalability for large-volume production. As a result, automation continues to be a major driver in expanding both market reach and technological capabilities.

High costs of specialized alloys and advanced manufacturing processes act as significant restraints in the Metal Seals market. Nickel-based and corrosion-resistant alloys essential for high-performance sealing can cost up to 35% more than conventional materials. Complex production techniques such as precision machining and multi-layer lamination increase manufacturing time and costs. Additionally, high energy consumption in production lines adds to operating expenses. These factors limit small and mid-scale manufacturers from adopting advanced seal technologies despite rising demand. The complexity of manufacturing also requires significant capital investment in advanced equipment, posing a barrier for rapid expansion in certain regions.

The adoption of additive manufacturing (3D printing) presents significant growth opportunities for the Metal Seals market, enabling complex geometries, faster prototyping, and reduced production waste. Additive manufacturing can reduce lead times by up to 30% and material waste by approximately 20%, offering cost and efficiency benefits. This technology also allows for customization of seals for niche applications in aerospace, oil & gas, and renewable energy sectors. Furthermore, additive manufacturing enables rapid product iterations, allowing manufacturers to address unique customer specifications more effectively. This creates opportunities for small-scale, high-value production runs and expansion into specialized industrial applications where traditional manufacturing methods are cost-prohibitive.

Evolving regulatory frameworks and environmental compliance pose notable challenges for the Metal Seals market. Stricter regulations in Europe, North America, and Asia require manufacturers to comply with higher standards for material selection, product safety, and environmental impact. Compliance with ISO 9001 and ISO 14001, as well as chemical safety standards, necessitates costly certification processes and manufacturing adjustments. Additionally, environmental regulations push for the use of recyclable and sustainable materials, which often require new production methods and investment in research. These factors can delay product launches, increase operational costs, and challenge smaller manufacturers in maintaining competitiveness while meeting compliance requirements.

• Expansion of Modular and Prefabricated Manufacturing: The adoption of modular and prefabricated manufacturing methods is reshaping the Metal Seals market, with over 55% of recent projects reporting cost and efficiency benefits. Prefabricated metal seal components, manufactured off-site with high-precision CNC machining, reduce production lead times by up to 20%. Europe and North America lead adoption, accounting for nearly 60% of total prefabricated seal usage, driven by efficiency demands in aerospace and industrial manufacturing sectors.

• Growth of Advanced Alloy Integration: Advanced alloy materials are increasingly integrated into metal seal designs, improving durability and corrosion resistance by over 28% compared to standard alloys. Titanium and nickel-based alloys are now used in 42% of new aerospace and oil & gas sealing applications. This trend is especially strong in Asia-Pacific, where production of high-performance alloy seals has grown by 24% since 2023. Manufacturers are focusing on alloy innovation to meet stringent industry requirements.

• Rise of Automation and AI in Seal Manufacturing: Automation and AI quality control systems are transforming manufacturing efficiency, with automated processes now reducing defect rates by 18% and lead times by 22%. Over 35% of leading manufacturers in North America and Europe have adopted AI-enabled inspection systems in 2024, optimizing precision and cost efficiency for complex sealing components. This trend is expected to further expand in the coming years.

• Sustainability and ESG Integration in Seal Production: Sustainability is becoming a core trend, with over 40% of manufacturers committing to reducing waste and improving recycling rates for sealing materials. Recycling rates for metal seal components have improved by 17% in recent years. Europe leads this effort with a target to recycle 50% of sealing materials by 2028, driven by regulatory mandates and corporate ESG commitments.

The Metal Seals market is segmented across type, application, and end-user categories, each reflecting evolving industry needs and technological advancements. Type segmentation focuses on varied sealing mechanisms, including multi-layer, ring, and gasket-based seals, catering to diverse industrial requirements. Applications span aerospace, automotive, petrochemical, and power generation, with aerospace and automotive dominating demand due to performance-critical needs. End-user segmentation reflects strong adoption in aerospace (32%) and oil & gas (28%), with industrial machinery and renewable energy sectors emerging as growth drivers. Regional segmentation highlights Asia-Pacific as a manufacturing hub, while Europe emphasizes compliance-driven adoption. Increasing demand for high-performance sealing solutions, coupled with innovations in materials and manufacturing processes, is reshaping the market landscape.

Multi-layer metal seals currently account for 38% of the market, leading due to their superior durability, high-temperature resistance, and ability to perform in extreme environments. These seals are extensively adopted in aerospace and oil & gas applications, where performance reliability is critical. Ring-type seals hold a 27% share, valued for their precision in automotive and heavy machinery. Gasket-based metal seals, contributing around 15%, remain relevant for cost-sensitive and lower-pressure applications. Other types, including custom-engineered seals, represent a combined share of approximately 20%, with niche relevance in specialized industries such as nuclear power and advanced aerospace. Multi-layer metal seals are also growing fastest, with adoption increasing by over 14% since 2023, driven by advancements in alloy technology.

Aerospace applications currently account for 32% of the Metal Seals market, leading due to the critical need for high-performance seals that withstand extreme pressure and temperature variations. Automotive applications hold a 28% share, driven by increasing demand for precision-engineered components in fuel-efficient and electric vehicles. Oil & gas applications account for 25%, with demand growing steadily due to deepwater drilling projects requiring robust sealing solutions. Power generation and industrial machinery account for the remaining 15%, serving niche operational requirements. The fastest-growing application is automotive, with adoption rising by over 16% since 2023 due to advancements in electric vehicle powertrain design and stricter emission standards.

Aerospace leads as the largest end-user segment, accounting for 32% of metal seal adoption due to the critical role of seals in high-pressure, high-temperature environments. Automotive follows closely with a 28% share, driven by demand for precision components in electric and hybrid vehicles. Oil & gas accounts for 25%, with increasing requirements for durable seals in harsh environments. Industrial machinery and power generation collectively make up 15% of end-user adoption, with rising niche demand in specialized engineering sectors. The fastest-growing end-user segment is electric vehicle manufacturing, with adoption of advanced seals increasing by over 18% since 2023, driven by improvements in battery safety and thermal management.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

To get a detailed analysis of this report

by Region" height="351" src="sample.jpg">

To get a detailed analysis of this report

by Region" height="351" src="sample.jpg">

Asia-Pacific’s dominance is driven by a total production volume exceeding 1.2 million units annually, with China, Japan, and India leading consumption. Japan alone contributed over 420,000 units in 2024, supported by investments exceeding USD 150 million in advanced manufacturing. Demand is fueled by industrial machinery (34%), automotive (28%), and aerospace (22%) applications. Asia-Pacific is also witnessing rapid adoption of additive manufacturing, with over 24% growth in 3D-printed seal components. In contrast, North America’s adoption rate for AI-integrated manufacturing has reached 35%, with aerospace and automotive industries leading demand. These regional differences underline the strategic importance of production capacity, technological innovation, and sector-specific adoption trends in shaping the future of the Metal Seals market.

How is innovation driving efficiency in seal manufacturing?

North America accounts for approximately 27% of the global Metal Seals market, with demand primarily driven by aerospace, automotive, and oil & gas industries. Aerospace applications account for 36% of North America’s demand, supported by high reliability requirements for high-pressure environments. Regulatory changes, including updated aerospace certification standards and emission control mandates, are pushing manufacturers toward advanced, high-performance seals. Technological advancements such as AI-enabled quality control and robotic manufacturing are reducing defect rates by over 18% and improving production efficiency by 20%. A notable player, Parker Hannifin, has invested in digital transformation projects integrating predictive analytics for seal performance monitoring, improving maintenance scheduling. Consumer behavior in North America shows higher enterprise adoption in aerospace and precision engineering sectors, with over 42% of manufacturers prioritizing automated production and advanced materials integration.

What regulatory trends are shaping advanced sealing technologies?

Europe holds a 23% share of the Metal Seals market, with Germany, the UK, and France as the largest contributors. Germany leads with high demand in automotive and aerospace sectors, while the UK focuses on energy and manufacturing applications. Regulatory bodies such as the European Committee for Standardization are driving adoption of sustainable sealing materials, resulting in a 28% increase in recyclable metal seal usage in the last two years. Europe is also adopting Industry 4.0 practices, integrating AI and IoT-enabled monitoring systems in manufacturing processes. SKF Group in Germany has pioneered high-performance multi-layer metal seals with enhanced corrosion resistance, reducing maintenance requirements by 16%. Regulatory pressure in Europe drives demand for explainable Metal Seals, with nearly 38% of enterprises focusing on compliance-related innovation.

Why is this region leading in high-volume seal manufacturing?

Asia-Pacific dominates with a 38% market share in Metal Seals, ranking first globally in production volume. China, Japan, and India are the top consumers, with Japan producing over 420,000 units annually. Infrastructure growth, particularly in aerospace, automotive, and petrochemical industries, fuels demand for advanced sealing solutions. Additive manufacturing adoption in Asia-Pacific has increased by 24% since 2023, with custom-engineered metal seals becoming common in high-performance applications. Technological innovation hubs in Japan and South Korea are focusing on alloy engineering and automation integration. Local players such as Nippon Steel are expanding their metal seal production capabilities by investing in automated CNC machining and precision alloy fabrication. Consumer behavior in Asia-Pacific reflects strong demand from manufacturing sectors, with over 60% of large-scale industrial players prioritizing advanced seal technology integration.

How are industry trends shaping demand in emerging markets?

South America holds a 7% share of the Metal Seals market, with Brazil and Argentina leading demand. Infrastructure development, particularly in oil & gas and energy sectors, is driving consumption. Government incentives for manufacturing modernization in Brazil have resulted in a 15% increase in advanced seal adoption since 2023. Trade partnerships with Asia-Pacific nations are improving access to high-performance sealing materials. Local player SKF do Brasil has expanded production capacity with advanced machining capabilities, improving product performance by 14%. Consumer demand is increasingly tied to energy sector efficiency, with over 42% of industrial clients prioritizing durability and reduced downtime in sealing solutions. Regional adoption is shaped by large-scale infrastructure projects and rising demand in energy production.

What drives demand for advanced sealing solutions in resource-intensive sectors?

Middle East & Africa account for a combined 5% of the global Metal Seals market, with demand concentrated in oil & gas and construction industries. UAE and South Africa are major growth markets, supported by large-scale energy projects and industrial modernization programs. Technological modernization trends include adoption of automated manufacturing and IoT-enabled seal monitoring systems, improving reliability by over 15%. Regulatory changes in environmental protection and material sourcing influence production strategies. Local player Advanced Seals LLC in UAE has integrated high-precision manufacturing, enhancing seal durability in extreme conditions. Regional consumer behavior reflects a focus on robust sealing solutions for resource-intensive sectors, with 47% of enterprises prioritizing long-term reliability and compliance with environmental regulations.

Japan: 18% market share – High production capacity and significant investment in precision seal manufacturing.

Germany: 15% market share – Strong demand from automotive and aerospace industries supported by advanced manufacturing technologies.

The Metal Seals market is highly competitive and moderately consolidated, with approximately 120 active global players competing across industrial, aerospace, automotive, and energy applications. The top five companies — Parker Hannifin, Garlock Sealing Technologies, SKF Group, Freudenberg Group, and Chesterton — together account for approximately 48% of the total market share. Market positioning varies, with leading firms focusing on technological innovation, product diversification, and strategic partnerships to strengthen competitive advantage. Recent initiatives include collaborations between material suppliers and manufacturing firms to develop high-performance alloy seals, as well as significant investments in automation and additive manufacturing capabilities. Product launches have increased by over 22% in the last three years, driven by demand for durable, high-efficiency sealing solutions. Mergers and acquisitions are reshaping the landscape, with over 18 notable deals executed since 2022 to expand product portfolios and geographic reach. Innovation trends such as AI-enabled inspection systems, advanced alloy engineering, and eco-friendly seal materials are further influencing competition, making the Metal Seals market dynamic and innovation-driven.

Freudenberg Group

Chesterton

Nippon Steel Corporation

Advanced Seals LLC

Teadit Seals

James Walker Group

Kitz Corporation

The Metal Seals market is experiencing significant transformation driven by advances in material science, manufacturing processes, and digital integration. Precision alloy engineering is at the forefront, with titanium, nickel-based, and cobalt-chromium alloys increasingly adopted to enhance corrosion resistance, temperature stability, and mechanical strength. These alloys offer up to 28% greater durability compared to conventional sealing materials, making them essential for aerospace, petrochemical, and energy applications. Additive manufacturing is emerging as a disruptive technology, enabling the production of complex seal geometries with reduced lead times — by up to 30% — and material waste reductions of nearly 20%. Automation and robotics are becoming integral to manufacturing lines, with over 35% of leading manufacturers employing AI-driven quality control systems that reduce defect rates by approximately 18%. IoT-enabled monitoring systems are also gaining traction, allowing real-time performance analysis, predictive maintenance, and operational optimization, particularly in mission-critical industries such as aerospace and oil & gas. Additionally, sustainability-driven innovations are introducing recyclable sealing materials and low-energy production processes, with a goal of reducing waste by over 20% in the coming years. These technology trends position the Metal Seals market at the intersection of precision engineering, automation, and sustainable innovation.

In 2023, Parker Hannifin launched an advanced multi-layer metal seal for aerospace applications, improving pressure resistance by 22% and reducing maintenance requirements by 16%.

In 2024, Garlock Sealing Technologies introduced a new corrosion-resistant alloy seal series for petrochemical applications, achieving a 25% increase in operational lifespan.

In 2023, SKF Group implemented AI-driven quality inspection across its seal manufacturing lines, reducing defect rates by 18% and improving production efficiency by 20%.

In 2024, Nippon Steel Corporation expanded its automated CNC machining capacity for multi-layer metal seals, increasing production by over 22% to meet growing aerospace and energy sector demand.

The Metal Seals Market Report offers a comprehensive analysis of global and regional market trends, key competitive developments, and technology adoption patterns. The report covers all major product types including multi-layer seals, ring seals, gasket-based seals, and custom-engineered solutions. It examines applications across aerospace, automotive, oil & gas, power generation, industrial machinery, and emerging sectors such as renewable energy. The report provides segmentation insights by type, application, end-user, and region, with a particular focus on Asia-Pacific, North America, and Europe as leading markets. Detailed profiles of major players are included, highlighting product portfolios, strategic initiatives, and innovation trends. The scope extends to examining technological drivers such as alloy engineering, additive manufacturing, AI-enabled quality control, and IoT-based performance monitoring. The report also analyzes market drivers, restraints, opportunities, and competitive strategies shaping the landscape. By combining quantitative data and qualitative analysis, it offers decision-makers a clear view of emerging opportunities, competitive positioning, and strategic pathways for growth in the Metal Seals market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1906.54 Million |

|

Market Revenue in 2032 |

USD 2948.21 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Parker Hannifin, Garlock Sealing Technologies, SKF Group, Freudenberg Group, Chesterton, Nippon Steel Corporation, Advanced Seals LLC, Teadit Seals, James Walker Group, Kitz Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |