Reports

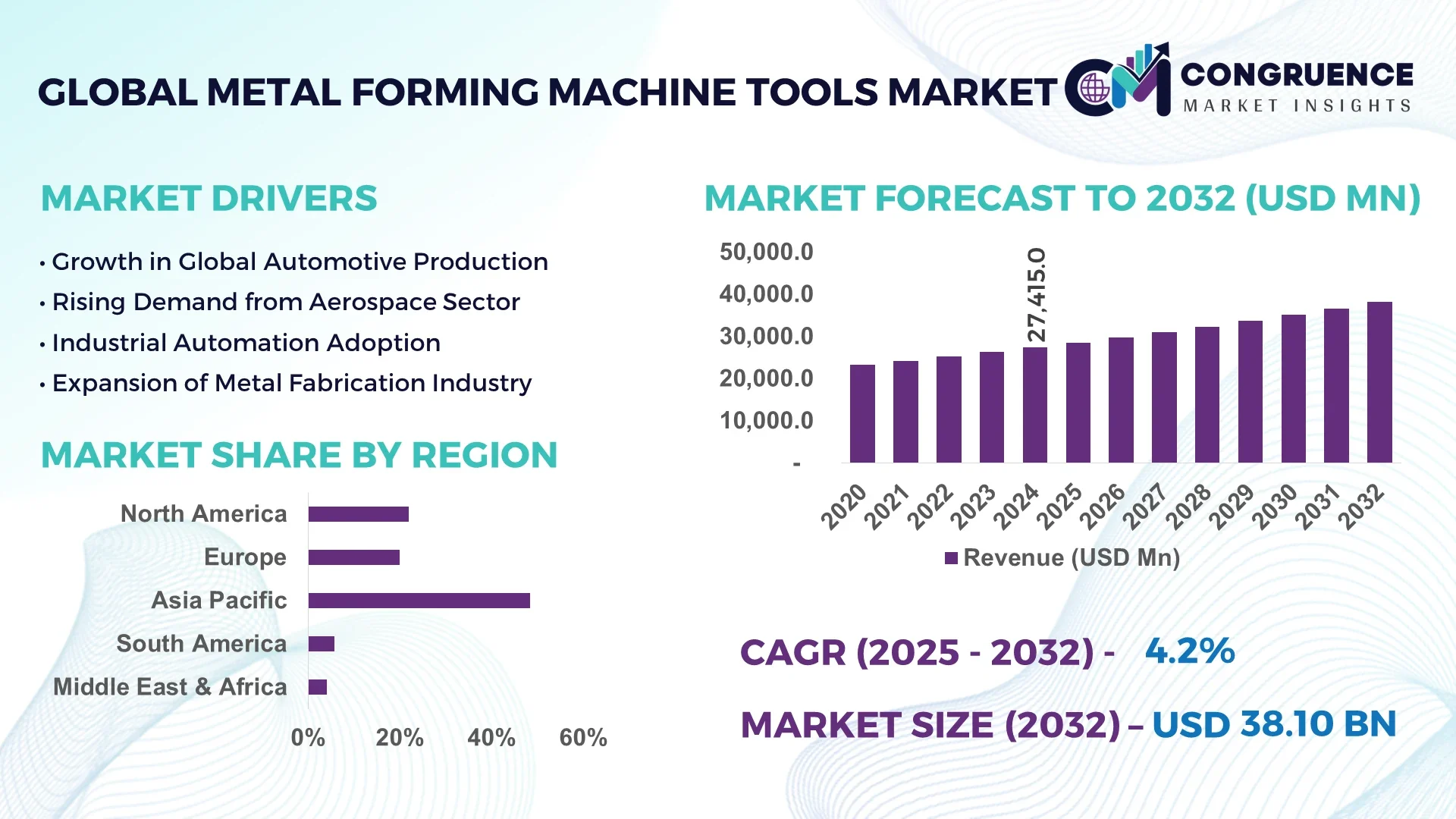

The Global Metal Forming Machine Tools Market was valued at USD 27,415.02 Million in 2024 and is anticipated to reach a value of USD 38,100.46 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032.

Japan, known for its advanced manufacturing ecosystem, maintains high production capacity in the Metal Forming Machine Tools market with consistent investments in precision forging and stamping technologies for automotive and aerospace sectors, integrating IoT-enabled systems within modern machining centers.

The Metal Forming Machine Tools market is witnessing robust momentum driven by expanding demand from key sectors such as automotive, aerospace, and heavy machinery, which collectively contribute significantly to the market structure. Technological advancements including servo press technology, hybrid machine integration, and precision die innovations are reshaping operational landscapes, increasing output quality while reducing waste and downtime. The market is influenced by strict environmental and safety regulations that encourage the adoption of energy-efficient and low-emission forming equipment. Regional consumption trends reflect rising demand in Asia-Pacific for high-speed metal forming machines, while Europe is focusing on smart factory integrations within the metal forming ecosystem. Future trends indicate the rise of fully automated metal forming lines equipped with real-time monitoring and predictive maintenance capabilities to enhance operational reliability and manufacturing consistency, shaping the next decade for the Metal Forming Machine Tools market.

Artificial Intelligence is accelerating the evolution of the Metal Forming Machine Tools Market by enabling predictive maintenance, real-time quality monitoring, and production optimization across complex forming operations. By leveraging machine learning algorithms and advanced analytics, manufacturers can now predict die wear, optimize toolpath strategies, and automate adjustments in press operations to reduce cycle times and scrap rates. AI-powered inspection systems are integrated into metal forming lines to detect micro-defects during forging and stamping, ensuring higher consistency in output and reducing the manual inspection workload. Additionally, AI-driven energy management systems in the Metal Forming Machine Tools Market are helping manufacturers lower operational costs and environmental impact by optimizing energy consumption during high-load forming processes.

In the Metal Forming Machine Tools Market, AI is also enhancing adaptive control systems in CNC forming equipment, where data from sensors guide real-time parameter adjustments to improve dimensional accuracy and surface quality during forming. This has proven especially beneficial in high-strength steel and aluminum forming operations in the automotive sector. Manufacturers are utilizing AI to enhance simulation models for metal flow, heat distribution, and material springback, thus reducing trial-and-error in die design and speeding up time-to-market for new components. AI’s role in optimizing supply chain planning, demand forecasting, and production scheduling is further supporting market participants to manage high-mix, low-volume production runs while maintaining profitability and operational efficiency within the Metal Forming Machine Tools Market.

“In 2024, an AI-integrated servo press system was deployed by a leading Japanese manufacturer within the Metal Forming Machine Tools Market, achieving a 25% reduction in downtime and a 30% improvement in die life through predictive wear monitoring and automatic load adjustments during high-speed forming operations.”

The Metal Forming Machine Tools Market is experiencing continuous evolution driven by technological integration, growing demand from high-precision industries, and regional advancements in manufacturing capabilities. Increasing focus on lightweight vehicle production and the rising use of high-strength materials in the automotive and aerospace sectors are influencing equipment upgrades and advanced tooling adoption within the Metal Forming Machine Tools Market. Environmental policies are accelerating the demand for energy-efficient forming machines, while the integration of automation and robotics enhances production consistency and throughput. Additionally, the emergence of smart factory initiatives is propelling the adoption of IoT-connected forming machines, supporting predictive maintenance and operational transparency. The dynamic shifts in the Metal Forming Machine Tools Market are further influenced by supply chain developments, increasing demand for high-speed forming operations, and continuous innovations in servo press technology, forging systems, and die management, creating a competitive yet growth-driven environment for manufacturers and stakeholders globally.

Technological advancements are significantly propelling the Metal Forming Machine Tools Market by enabling manufacturers to increase production efficiency while maintaining product quality. The integration of servo press technology has led to higher accuracy in forming operations, reducing waste and downtime across production lines. Automation, coupled with advanced CNC systems, has enabled real-time process control, providing consistent dimensional accuracy during complex forming processes, particularly in the automotive and heavy machinery sectors. The deployment of IoT sensors within metal forming machines is supporting predictive maintenance strategies, thereby minimizing unplanned downtimes. These technological improvements are fostering the adoption of advanced forming equipment globally, allowing companies to scale their operations while addressing labor shortages and quality challenges in high-volume production environments.

High initial capital investment associated with advanced machinery and technology integration remains a restraint in the Metal Forming Machine Tools Market. The implementation of modern servo presses, CNC-enabled forming machines, and AI-integrated inspection systems requires substantial upfront investment, posing financial challenges for small and medium-sized manufacturers. Additionally, the costs related to skilled workforce training and system integration increase the total ownership cost of such advanced equipment. This restraint limits market penetration in developing regions, where manufacturers continue to rely on conventional forming machinery to manage operational costs. Consequently, despite long-term benefits, the high initial expenditure remains a significant consideration impacting the adoption pace of new technologies within the Metal Forming Machine Tools Market.

The increasing demand for lightweight components in the automotive and aerospace industries presents a significant opportunity within the Metal Forming Machine Tools Market. As manufacturers aim to enhance fuel efficiency and reduce emissions, the need for high-precision forming of lightweight materials like aluminum and advanced high-strength steels is rising rapidly. This trend drives the requirement for technologically advanced forming machines capable of handling complex geometries with high repeatability and surface quality. Additionally, with the global shift towards electric vehicles, the production of battery housings, structural components, and lightweight body parts is expanding, providing a clear growth opportunity for machine tool manufacturers to develop specialized forming solutions aligned with these industry needs.

Fluctuating raw material prices continue to pose a challenge to the Metal Forming Machine Tools Market by affecting production planning and operational costs. Steel, aluminum, and specialized alloys essential for metal forming processes often experience price volatility due to geopolitical tensions, supply chain disruptions, and shifting global demand patterns. These fluctuations complicate cost estimations and profit margin management for manufacturers investing in metal forming machine tools, especially when planning for long-term contracts and high-volume production. The unpredictability in raw material costs also impacts the procurement of tool steels and die materials necessary for consistent forming operations, adding complexity to operational strategies within the Metal Forming Machine Tools Market.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is reshaping demand dynamics in the Metal Forming Machine Tools market. Pre-bent and pre-cut elements are produced off-site using automated forming machines, reducing labor requirements while enhancing consistency and safety standards in project delivery. Europe and North America are witnessing increased demand for high-precision machines to meet construction timelines, with contractors requiring consistent component quality for modular housing, healthcare facilities, and industrial warehouses.

• Growth in Electric Vehicle Production: Expansion in electric vehicle manufacturing is driving significant demand within the Metal Forming Machine Tools market, particularly for forming lightweight aluminum and high-strength steel components. Precision forming machines are utilized for battery tray housings, motor casings, and structural lightweight components essential for reducing EV weight while maintaining crash safety standards. Countries like Germany and China have seen a sharp increase in orders for advanced forming equipment aligned with expanding EV production capacities.

• Integration of Servo Press Technology: Servo press technology adoption is accelerating in the Metal Forming Machine Tools market, with manufacturers seeking flexible control over stroke profiles and force application for complex geometries. Servo presses are enabling higher forming precision while reducing energy consumption compared to traditional mechanical presses. This trend is especially evident in the aerospace and automotive sectors, where advanced material forming and process repeatability are critical for operational efficiency.

• Increased Adoption of Automated Inspection Systems: Automated inspection systems integrated within forming lines are becoming a measurable trend in the Metal Forming Machine Tools market. These systems utilize vision sensors and AI algorithms to detect dimensional inaccuracies and micro-defects during forming operations, reducing reliance on manual inspection and minimizing rework. This trend is particularly impactful in the production of high-precision components where quality assurance is central to maintaining manufacturing standards in global supply chains.

The Metal Forming Machine Tools market is segmented based on types, applications, and end-user sectors, aligning with the evolving demands of advanced manufacturing industries. Type segmentation includes mechanical presses, hydraulic presses, servo presses, and others, with each catering to distinct forming needs in industrial applications. Application segmentation covers automotive, aerospace, construction, heavy machinery, and electronics manufacturing, where the demand for high-strength, lightweight formed components is rising. End-user segmentation focuses on automotive OEMs, aerospace component manufacturers, construction contractors, and industrial equipment manufacturers, each driving demand for advanced forming capabilities to improve operational efficiency, product quality, and sustainability in their processes within the Metal Forming Machine Tools market.

Mechanical presses lead the Metal Forming Machine Tools market due to their suitability for high-volume stamping operations in automotive and appliance manufacturing, offering consistent performance and cost-effective production cycles. Servo presses are the fastest-growing type within the segment, driven by their programmable control capabilities that enable high-precision forming and material handling flexibility while reducing energy consumption. Hydraulic presses maintain a strong presence in applications requiring deep drawing and complex shaping, providing controlled force application across varying material thicknesses. Other types, including pneumatic presses and hybrid forming machines, contribute to niche segments such as electronics and small-scale component forming, where specialized forming tasks demand compact and adaptable machinery. The evolving technological landscape in forming processes, emphasizing energy efficiency and automation, is expected to enhance the operational capabilities of these machine types, influencing their adoption across regional markets.

Automotive manufacturing remains the leading application segment in the Metal Forming Machine Tools market, with forming machines extensively used for chassis components, body panels, and structural reinforcements. This leadership is supported by the rising global vehicle production and lightweighting initiatives to improve fuel efficiency. The aerospace sector is the fastest-growing application area, driven by the demand for precision-formed high-strength alloys for structural and engine components to enhance aircraft performance and fuel efficiency. Construction applications are gaining traction due to the surge in modular construction projects requiring preformed steel and aluminum components. Additionally, the electronics sector utilizes precision forming for casing and frame components, while heavy machinery manufacturing employs forming machines for robust component production. These application areas collectively contribute to the robust demand for metal forming solutions, emphasizing quality, repeatability, and operational productivity.

Automotive OEMs are the leading end-user segment within the Metal Forming Machine Tools market, consistently investing in advanced forming solutions to meet lightweighting targets and high-volume production requirements for body and chassis components. Aerospace component manufacturers are emerging as the fastest-growing end-user group, driven by the rising demand for lightweight and high-strength parts, necessitating precision forming technologies to maintain strict tolerances and material integrity. Construction contractors increasingly adopt metal forming solutions for pre-engineered structures, while industrial equipment manufacturers utilize forming machines for parts requiring robust construction and dimensional accuracy. These end-user groups, focusing on automation, precision, and sustainability, continue to shape the demand landscape of the Metal Forming Machine Tools market globally, driving manufacturers to innovate in forming technologies and integrated production systems.

Asia-Pacific accounted for the largest market share at 48.3% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.7% between 2025 and 2032.

The Asia-Pacific Metal Forming Machine Tools market benefits from extensive automotive and electronics production hubs, with China, Japan, and India driving significant demand for high-precision stamping and forging equipment. Meanwhile, Europe’s rapid growth is supported by automotive lightweighting trends, EV production expansion, and strong sustainability initiatives influencing the adoption of energy-efficient forming machines. Across both regions, the integration of digital manufacturing and smart factory principles is shaping the operational frameworks of end-users, enhancing throughput and quality in forming operations within the Metal Forming Machine Tools market.

Precision Automation Driving Advanced Component Manufacturing

The Metal Forming Machine Tools market in this region held a market share of 21.6% in 2024, driven by high demand from the automotive, aerospace, and heavy machinery industries. The region’s industry dynamics are shaped by the rising need for lightweight structural components and advanced manufacturing capabilities in aerospace and defense sectors. Government initiatives focusing on reshoring manufacturing and modernizing industrial infrastructure are encouraging investments in energy-efficient forming equipment. Technological advancements such as AI-enabled quality monitoring and servo press automation are driving operational productivity, while regulatory focus on workplace safety and emissions reduction supports the accelerated replacement of outdated machinery with advanced forming solutions within the Metal Forming Machine Tools market.

Smart Manufacturing Trends Powering Precision Engineering Growth

Holding a market share of 24.9% in 2024, the Metal Forming Machine Tools market in this region benefits from Germany, the UK, and France driving investments in EV production and lightweight automotive component manufacturing. European Union directives on carbon reduction and sustainability are encouraging manufacturers to adopt energy-efficient and low-emission forming machinery. The region is witnessing increased implementation of Industry 4.0 technologies, with real-time data monitoring and predictive maintenance systems enhancing operational efficiency. The growing aerospace sector and the expansion of modular construction projects further support the uptake of advanced forming equipment across key industries, positioning the region as a leader in precision forming solutions within the Metal Forming Machine Tools market.

High-Volume Production Demands Advancing Industrial Forming Solutions

Asia-Pacific dominated the Metal Forming Machine Tools market by volume in 2024, driven by strong consumption from China, Japan, and India. China’s large-scale automotive and electronics manufacturing capabilities are supported by investments in high-speed stamping and forging lines. Japan’s advanced technological infrastructure and high-precision forming equipment deployment continue to influence operational trends across the region. India’s manufacturing growth, supported by infrastructure development and domestic automotive expansion, is increasing the demand for forming machines. The integration of smart manufacturing and industrial automation, including AI-enabled forming solutions and digital twins, is gaining traction in regional manufacturing hubs, reshaping operational efficiencies within the Metal Forming Machine Tools market.

Industrial Upgrades Supporting Forming Equipment Modernization

The Metal Forming Machine Tools market in this region is influenced by key countries including Brazil and Argentina, with the region accounting for 4.2% of the global market share in 2024. Brazil’s automotive and agricultural equipment sectors are major drivers of forming machine demand, while Argentina’s industrial modernization initiatives support incremental market growth. Investments in infrastructure and energy projects are creating opportunities for forming equipment manufacturers, particularly in producing structural and pipeline components. Trade policies promoting industrial machinery imports and government incentives for modernizing production capabilities are encouraging the adoption of advanced forming machines, with manufacturers prioritizing durable and high-throughput equipment in the Metal Forming Machine Tools market.

Infrastructure Expansion Fuelling Forming Equipment Demand

The Metal Forming Machine Tools market in this region is supported by the construction, oil and gas, and transportation sectors, with major growth noted in the UAE, Saudi Arabia, and South Africa. The region’s demand is driven by large-scale infrastructure projects and industrial diversification strategies seeking to reduce economic dependency on oil. Technological modernization trends, including the gradual adoption of CNC and servo press forming machines, are evident across industrial hubs, aiming to enhance operational precision and reduce energy consumption. Local regulations supporting industrial equipment upgrades and international trade partnerships are facilitating the import and deployment of advanced forming equipment, strengthening the operational landscape within the Metal Forming Machine Tools market.

China – 34.7% Market Share

High production capacity, robust automotive and electronics manufacturing, and continuous technological upgrades sustain China’s dominance in the Metal Forming Machine Tools market.

Germany – 14.8% Market Share

Strong end-user demand across automotive and aerospace industries, combined with advanced engineering and digital transformation, positions Germany as a leader in the Metal Forming Machine Tools market.

The Metal Forming Machine Tools market features a competitive environment with over 200 active manufacturers globally, each strategically enhancing their technological capabilities to maintain market positioning. Leading players are focusing on expanding their forming equipment portfolios with servo press technology, CNC-integrated systems, and AI-enabled forming lines to address increasing demands for precision and high-volume production. Strategic initiatives such as partnerships with automation companies, technology licensing agreements, and the establishment of smart manufacturing plants are shaping the competitive dynamics. Product launches featuring energy-efficient forming machines and modular forming systems are gaining traction as manufacturers aim to align with global sustainability goals and reduce operational costs for end-users. Mergers and acquisitions are evident across the industry, with key players targeting regional market expansion and technological synergies to enhance competitiveness. Innovation trends, including the integration of digital twins for predictive maintenance and forming process optimization, are becoming critical differentiators among competitors in the Metal Forming Machine Tools market, driving operational efficiency and customer value within a rapidly evolving manufacturing landscape.

TRUMPF Group

Amada Co., Ltd.

Schuler AG

DMG Mori Co., Ltd.

JTEKT Corporation

Komatsu Ltd.

Makino Milling Machine Co., Ltd.

Hyundai WIA Corporation

Haas Automation, Inc.

MAG IAS GmbH

The Metal Forming Machine Tools market is witnessing rapid technological transformation with the integration of servo press systems, AI-enabled inspection, and IoT-connected forming lines to enhance production precision and operational efficiency. Servo press technology is enabling customizable stroke profiles, reducing energy consumption by up to 30% while maintaining high forming accuracy, making it increasingly adopted for complex automotive and aerospace parts. CNC-enabled forming machines are now integrated with adaptive control systems, allowing real-time parameter adjustments based on in-process sensor data, which reduces defect rates and tool wear. AI-powered vision systems are automating quality inspections during stamping and forging operations, identifying micro-defects that previously required manual checks, thereby increasing throughput. Digital twin technology is emerging in forming machine maintenance, allowing manufacturers to simulate forming operations, monitor machine health, and optimize tool changeover processes to reduce downtime. In addition, hybrid forming machines that combine hydraulic and mechanical press features are being introduced to handle high-strength materials while improving operational flexibility. Automation in material handling and robotic part transfer systems are further streamlining workflows in forming lines, enabling consistent production quality and reducing labor dependence. These technological advancements collectively support sustainable manufacturing while aligning with industry goals for precision and productivity within the Metal Forming Machine Tools market.

• In February 2023, Schuler launched a new servo press line equipped with a Smart Assist system, enabling automated tool setup and real-time monitoring, reducing setup times by 40% in high-volume automotive component production while improving operational safety during forming processes.

• In July 2023, Amada introduced an updated fiber laser blanking system integrated with metal forming machines, increasing cutting and forming speed by 35% while supporting automated material handling for automotive and heavy machinery applications across key Asian markets.

• In March 2024, DMG Mori unveiled its eco-friendly forming machine series with energy-efficient drives and regenerative braking technology, reducing energy consumption by 25% during forming operations, targeting precision component production in the European automotive sector.

• In May 2024, Komatsu installed AI-driven predictive maintenance systems on its metal forming equipment in North American facilities, achieving a 20% reduction in unplanned downtime and extending the die lifespan in continuous forming operations for the aerospace sector.

The Metal Forming Machine Tools Market Report provides an in-depth analysis of the diverse market segments, technological trends, and regional insights shaping the industry landscape. The report covers mechanical presses, servo presses, hydraulic presses, and hybrid forming machines, analyzing their adoption across high-volume production, precision forming, and niche component manufacturing. Applications assessed include automotive, aerospace, construction, heavy machinery, and electronics, with focused analysis on lightweight material forming and high-strength alloy applications. The geographic scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional manufacturing capabilities, industrial policies, and technological adoption influencing forming equipment demand.

Additionally, the report investigates emerging segments such as AI-integrated forming machines, automated inspection systems, and digital twin-enabled predictive maintenance technologies, which are transforming operational practices in the market. It also assesses sustainability trends in forming equipment, including energy-efficient drives, regenerative systems, and smart factory integrations. Supply chain analysis, industry challenges such as raw material price fluctuations, and competitive strategies including partnerships and product innovations are examined to support business decisions. This comprehensive scope positions the report as a strategic resource for industry professionals, investors, and decision-makers seeking actionable insights into the evolving Metal Forming Machine Tools market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 27415.02 Million |

|

Market Revenue in 2032 |

USD 38100.46 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TRUMPF Group, Amada Co., Ltd., Schuler AG, DMG Mori Co., Ltd., JTEKT Corporation, Komatsu Ltd., Makino Milling Machine Co., Ltd., Hyundai WIA Corporation, Haas Automation, Inc., MAG IAS GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |