Reports

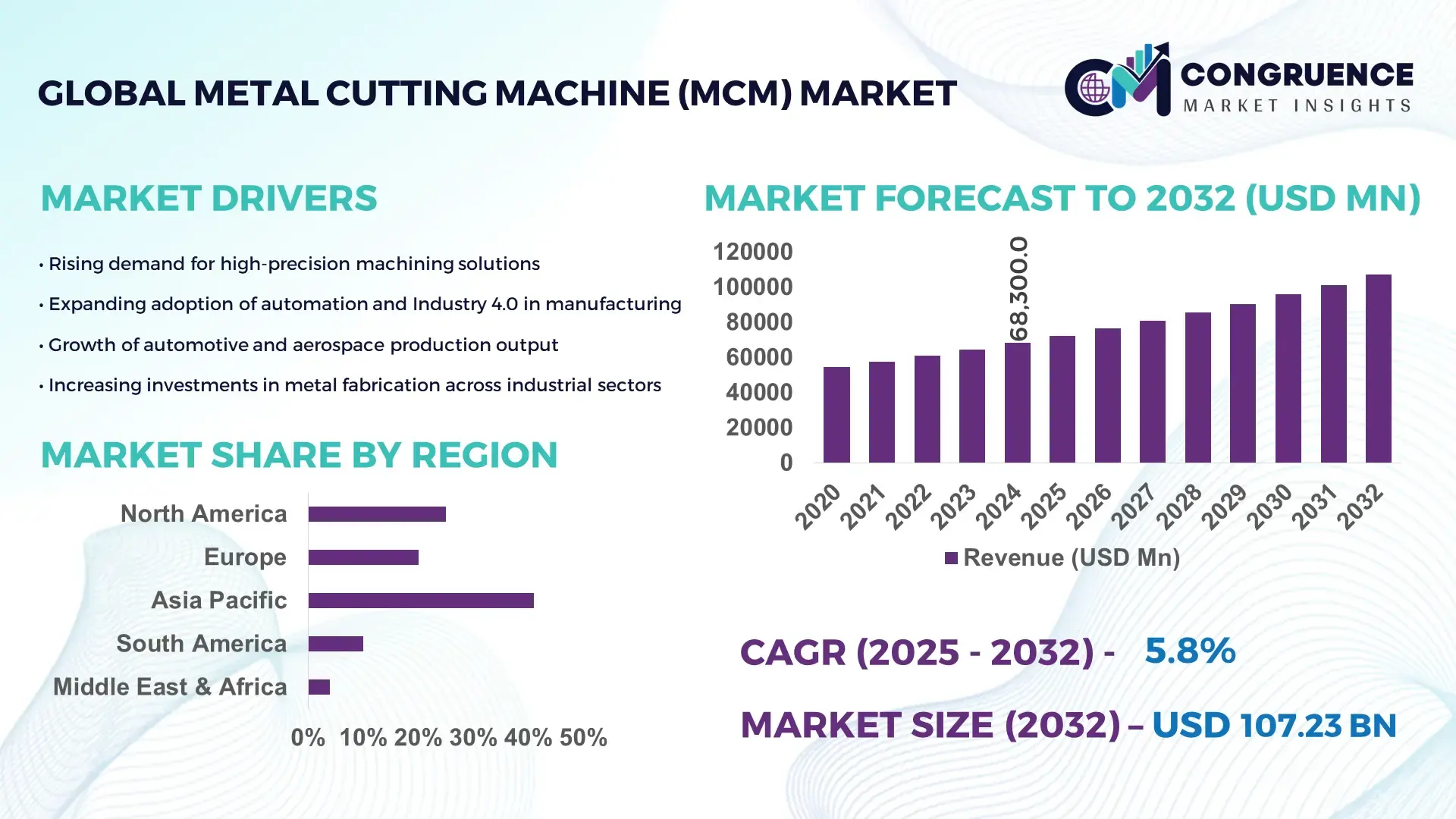

The Global Metal Cutting Machine (MCM) Market was valued at USD 68,300 Million in 2024 and is anticipated to reach a value of USD 113,446.65 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032. The growth is being driven by increasing industrial automation and demand for precision manufacturing worldwide.

In China, production capacity for metal-cutting machine tools exceeded 900,000 units by 2017, supported by strong investment in medium- and high-end systems to strengthen the domestic manufacturing base. Imports of advanced machine tools crossed USD 8 billion in 2021 to support high-precision industrial requirements. Automotive suppliers account for close to 40% of metal-cutting machine usage in the country, followed by aerospace, mold production, and construction machinery industries, contributing nearly half of the remaining demand. Rapid adoption of CNC machining centres, laser-cutting platforms, and digitally networked manufacturing systems has expanded machine capability clusters across China’s major industrial hubs, reinforcing its leadership in the metal cutting machine technology landscape.

Market Size & Growth: Valued at USD 68,300 Million in 2024, projected to reach USD 113,446.65 Million by 2032 at a CAGR of 5.8%, powered by expanding precision-manufacturing and automated production lines.

Top Growth Drivers: Automation adoption (~33%), efficiency improvement in cutting operations (~28%), demand from lightweight automotive & aerospace components (~22%).

Short-Term Forecast: By 2028, operational cost reduction estimated at ~12% with productivity improvement of ~15% through modern cutting systems and digitalized workflows.

Emerging Technologies: Fiber-laser and hybrid laser/plasma systems, IoT-enabled predictive maintenance, AI-based cutting optimization for variable materials.

Regional Leaders: Asia-Pacific projected at USD 45 000 Million by 2032, North America USD 30 000 Million, and Europe USD 20 000 Million, each driven by unique industrial modernization trends.

Consumer/End-User Trends: Highest adoption among automotive, aerospace, electronics, and metal fabrication sectors, with a shift toward automated metal-cut-shape-finish integrated systems.

Pilot or Case Example: A 2023 aerospace deployment recorded 17% downtime reduction and 22% productivity improvement via AI-enhanced laser-cutting lines.

Competitive Landscape: Market leader holds approximately ~25% share, alongside TRUMPF Group, Amada Holdings Co. Ltd., Bystronic AG, and Flow International Corporation.

Regulatory & ESG Impact: Global policies emphasize energy-efficient industrial equipment, sustainability-compliant heavy machinery operations, and recyclable components to reduce environmental footprint.

Investment & Funding Patterns: Over USD 1.2 billion recently invested in smart metal-cutting innovations, with increasing funding for automation upgrades and performance-based machinery models.

Innovation & Future Outlook: Advancements in modular cutting cells, remote diagnostics via cloud platforms, and autonomous zero-setup production lines shaping long-term market progression.

The Metal Cutting Machine (MCM) market serves core sectors including automotive, aerospace, electronics, industrial machinery, and construction, with the automotive sector commanding the highest consumption share due to high-volume component manufacturing requirements. Continuous product innovation—particularly in fiber-laser cutting, CNC multi-axis machining, hybrid additive–subtractive capabilities, and AI-driven predictive systems—is accelerating productivity and reducing scrap generation. Regulatory and environmental priorities are encouraging low-energy, high-efficiency cutting solutions, pushing manufacturers to upgrade equipment fleets globally. Consumption growth remains strongest in Asia-Pacific due to large-scale industrial automation, while North America and Europe prioritize high-precision digital retrofits and flexible manufacturing for short production cycles. Emerging trends show increasing preference for performance-contract business models, robotics-linked cutting platforms, and next-generation smart factories integrating CNC cutting with real-time workflow control and automated finishing systems.

The strategic relevance of the Metal Cutting Machine (MCM) Market lies in its integral role across key manufacturing ecosystems—including automotive, aerospace, industrial machinery, electronics, and precision engineering—where productivity, material accuracy, and operational agility are becoming decisive competitive advantages. CNC-driven fiber-laser technology delivers up to 35% higher cutting precision and 28% faster throughput compared to traditional CO₂-based systems, creating transformative efficiency gains for high-volume component manufacturing. Regionally, Asia-Pacific dominates in volume, while North America leads in enterprise adoption with more than 62% of manufacturers using digitally integrated MCM platforms. Strategic capital allocation by fabricators is increasingly centered on predictive-maintenance systems, automated tool-path optimization, and integrated robotics for continuous metal-processing lines. By 2027, AI-optimized machining and digital-twin simulation are expected to reduce material wastage and unplanned downtime by nearly 18% across metal-fabrication facilities worldwide. In parallel, ESG commitments are reshaping investment criteria, with firms targeting a 22% reduction in energy consumption and recyclability improvements in cutting consumables by 2030. In 2024, a manufacturing cluster in Germany achieved a 19% cycle-time reduction through autonomous laser-cut processing supported by edge-AI analytics, illustrating measurable value creation. Overall, the Metal Cutting Machine (MCM) Market is on a future trajectory defined by automation, sustainable operations, lifecycle productivity, and strategic technology modernization—positioning it firmly as a pillar of resilience, compliance, and long-term industrial growth.

Automation in industrial manufacturing has become a major catalyst for accelerating adoption of Metal Cutting Machine (MCM) platforms as companies aim to achieve high-volume component production with minimal labor intensity. Automated CNC and fiber-laser systems provide continuous cutting capability, multi-axis processing, reduced cycle time, and stable accuracy even in complex geometries. Industrial facilities adopting automated cutting lines report productivity improvements between 15% and 25% following integration of closed-loop control and robotic loading mechanisms. With automotive and aerospace manufacturers transitioning to scalable fabrication standards, modern MCM systems enable multi-material cutting—including high-strength steel, aluminum, and titanium—at significantly lower lead times. Added benefits such as enhanced repeatability, improved shop-floor safety, and real-time cutting diagnostics continue to strengthen automation’s influence on demand for MCM solutions globally.

Despite strong growth potential, high acquisition and lifecycle maintenance costs remain substantial barriers for many manufacturers seeking to adopt Metal Cutting Machine (MCM) systems. Advanced CNC and laser-cutting machines require significant upfront investment, continuous calibration, dedicated skilled technicians, and regular upgrades to maintain efficiency and material compatibility. Additionally, replacement of consumables, optics, and auxiliary equipment increases total cost of ownership for users operating in cost-sensitive production sectors. Many small- and medium-scale fabricators delay equipment modernization due to these financial constraints, choosing to extend the operating life of legacy systems rather than replacing them. The expense associated with integrating digital analytics, automation software, and predictive maintenance solutions further intensifies the investment burden, slowing the pace of modernization among manufacturers with limited capital allocation.

The rapid advancement of Industry 4.0 and smart-factory infrastructure is creating significant opportunities for technology-driven growth in the Metal Cutting Machine (MCM) market. Digital connectivity, remote monitoring, and sensor-driven predictive maintenance allow cutting systems to deliver higher uptime, reduced tool wear, and more consistent quality. Machine-learning-based optimization enables dynamic adjustment of feed rates, tool paths, and heat profiles based on real-time data, enhancing throughput and minimizing scrap. Manufacturers adopting digital-twin simulation and automated scheduling tools can optimize cutting tasks across multiple workstations and achieve efficiency improvements ranging from 10% to 20%. This opens large-scale opportunities for MCM suppliers to offer integrated automation software, connected robotics, and cloud-based production management platforms to industries striving for traceability, continuous processing, and zero-defect manufacturing targets.

As Metal Cutting Machine (MCM) systems evolve toward highly digital and automated architectures, proficiency requirements for machine operators and maintenance personnel are increasing rapidly. Fiber-laser, CNC, and hybrid-multiprocess cutting platforms require advanced skill sets in programming, digital control interpretation, safety compliance, and troubleshooting. However, a widening gap exists between industrial technology advancement and workforce upskilling, particularly in emerging economies. Training periods for technicians can extend from several months to more than a year, contributing to slower adoption cycles. Technical complexity also increases the risk of operational disruptions when qualified specialists are not readily available, which can lead to productivity losses during calibration, software updates, or machine realignment. These constraints make workforce development and skill certification essential yet challenging components of the market’s continued evolution.

Accelerated Shift Toward Modular and Prefabricated Construction: The rapid rise of modular and prefabricated buildings is reshaping demand patterns for Metal Cutting Machine (MCM) systems, with 55% of new construction projects reporting measurable cost benefits from modular execution. Automated cutting of beams, brackets, and steel framing components has reduced on-site labor requirements by 32% and shortened project timelines by nearly 20%. Europe and North America are seeing the highest traction for high-precision MCM equipment to support structural consistency and repeatability across prefabricated units, reinforcing a sustained upgrade cycle within fabrication workshops.

High-Speed Laser Systems Replacing Conventional Machinery: Laser-based cutting solutions are increasingly substituting plasma and mechanical cutting machines due to performance and efficiency gains. Fiber-laser systems have demonstrated up to 28% faster cutting speeds and 35% greater precision tolerance compared to older standards. Manufacturers deploying automated laser lines report a 16% reduction in material scrap and a 21% improvement in throughput within the first year of transition. Adoption is strongest in automotive and aerospace fabrication, where reduced thermal distortion and superior finish quality are critical to achieving consistent production metrics.

Expansion of Fully Connected Smart-Factory Cutting Cells: Global manufacturers are integrating Metal Cutting Machine (MCM) systems into smart-factory environments using sensors, digital monitoring, and data-driven process control. Plants adopting interconnected cutting cells have achieved an average 18% reduction in unplanned downtime and a 14% increase in asset utilization. Remote diagnostics and predictive maintenance now account for more than 40% of digital services linked to cutting operations. The shift allows real-time adjustments on feed rates, nozzle settings, and power calibration to maintain accuracy even during high-volume production cycles.

Rise of Flexible Multi-Material Processing for Lightweight Manufacturing: Demand for lightweight automotive and aerospace components is driving rapid expansion of multi-material MCM capabilities, enabling seamless cutting of aluminum, titanium, composite alloys, and high-strength steel within a single digital workflow. Manufacturers using multi-material machines have recorded a 23% reduction in changeover time and up to 19% faster prototype-to-production transitions. Approximately 48% of new industrial equipment purchases in 2024 prioritized multi-material compatibility to reduce operational fragmentation and accelerate fabrication agility in high-mix, short-run production environments.

The market is segmented based on type, application, and end-user categories, each shaping adoption patterns and competitive alignment. Type-based segmentation highlights how technological capabilities influence deployment across industries, while application-based segmentation demonstrates the functional needs driving selection in real-world use cases. End-user segmentation shows varying adoption maturity across technology-intensive verticals versus emerging sectors. Growing integration of AI automation, data analytics, and digital transformation initiatives is pushing higher adoption across multiple segments simultaneously rather than a single dominant use case. Adoption momentum is supported by increasing investments in advanced multimodal systems, user-experience optimization, and scalable AI infrastructure. Collectively, these segmentation clusters reveal a rapidly maturing ecosystem with differentiated demand profiles, accelerating innovation cycles, and expanding commercial viability across global markets.

Vision-language models represent the largest type category, accounting for 42% of adoption, supported by their ability to process multimodal content—images, documents, and text—making them widely used in retail analytics, autonomous systems, and content automation. Audio-text systems hold 25% of adoption due to strong uptake in customer support, conversational AI, and transcription workflows. However, adoption in video-language models is rising fastest and is expected to surpass 30% by 2032, driven by increasing requirements for contextual video understanding, enhanced streaming experiences, and automated media workflows. The fastest-growing type segment is video-language models, growing at 18.7% CAGR due to rising integration across entertainment platforms, smart surveillance systems, and virtual training environments. Other types including haptic-language, 3D-language, and biometric-language models collectively account for 33% share, offering niche advantages in immersive simulation, spatial computing, and security-centric ecosystems.

Customer experience intelligence stands as the leading application area, commanding 38% share, driven by enterprise-wide demand for automated service delivery, real-time sentiment understanding, and personalized customer engagement. Operational automation currently accounts for 27% of adoption, supporting large-scale content processing, workflow enhancement, and productivity optimization. However, adoption in healthcare diagnostics is rising fastest and is projected to surpass 29% by 2032, supported by clinical imaging insights, symptom-to-text mapping, and AI-based treatment recommendation systems. Healthcare diagnostics is the fastest-growing application segment, advancing at 19.2% CAGR due to growing global emphasis on precision healthcare and digital patient management. Other applications including cybersecurity intelligence, smart mobility, and education technology collectively represent 35% share and continue to benefit from policy support, digital learning demand, and intelligent risk detection systems.

The enterprise sector is the leading end-user group, representing 41% share with widespread use of AI-enabled automation, customer analytics, and content management. Technology companies currently account for 26% of adoption due to continuous product innovation and strategic integration of AI modules into commercial offerings. However, adoption in healthcare organizations is accelerating fastest and is expected to exceed 31% penetration by 2032, propelled by electronic medical record optimization, AI-assisted screening workflows, and automated reporting systems. Healthcare organizations represent the fastest-growing segment with a CAGR of 20.5%, fueled by rising demand for cost-efficient and scalable diagnostic support solutions. Other end-users including education institutions, government agencies, and media organizations contribute a combined share of 33%, supported by digital learning requirements, smart governance initiatives, and automated media production.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 11.9% between 2025 and 2032.

Asia-Pacific’s scale advantage is driven by high-volume manufacturing in China, Japan, and India, where CNC and automated machining are integrated heavily into automotive, electronics, and heavy engineering. Europe followed with 27% share due to strong engineering export capacity and sustainability-driven upgrades to machining precision. North America captured 21% supported by Industry 4.0 retrofits and automation in aerospace, defense, and automotive. South America represented 6% with machinery uptake in energy and mining equipment production, while the Middle East & Africa held 5% share driven by infrastructure investment. Increasing precision engineering, digital machining networks, and capital equipment modernization are reshaping consumption patterns across regions.

Is automation the main factor accelerating next-gen Metal Cutting Machine investments?

The region held a 21% share of the market in 2024, driven by large-scale demand from aerospace, automotive, medical component fabrication, and heavy engineering. Government programs supporting reshoring of manufacturing and digital infrastructure adoption are accelerating CNC, laser cutting, and robotic machining deployment. The U.S. remains the dominant contributor with more than 68% of the region’s consumption, supported by high-value production lines. Local players such as Haas Automation continue to expand high-precision vertical machining centers tailored for SMEs and enterprise manufacturers. North American buyers demonstrate higher preference for AI-integrated cutting systems, real-time quality assurance sensors, and smart production scheduling—showing stronger enterprise adoption in healthcare and finance-linked fabrication operations compared to other regions.

Are sustainability initiatives reshaping Metal Cutting Machine investments for long-term efficiency?

Europe accounted for a 27% share in 2024, led by Germany, France, and the UK, where high-precision engineering and automotive production remain key drivers. Stringent regulatory frameworks supporting carbon-efficient manufacturing and energy-optimized machining are influencing equipment choices. Sustainability programs and EU industrial modernization incentives have accelerated adoption of fiber-laser, 5-axis, and hybrid cutting technologies. Germany alone represented 39% of regional consumption due to its large automotive and machinery export footprint. Players like DMG Mori continue introducing eco-efficiency machining lines with reduced power loads and higher throughput. Consumer behavior in Europe shows strong demand for explainable and traceable performance of Metal Cutting Machines, driven by compliance pressure and a preference for certified production output.

Is high-volume industrialization driving the largest Metal Cutting Machine consumption worldwide?

Asia-Pacific remained the top-consuming region with a 41% market share in 2024, with China accounting for 48% of the region’s volume followed by Japan and India. Expansive automotive, industrial equipment, and electronics manufacturing bases continue to drive investments in CNC, plasma, and laser cutting machinery. Rapid development of industrial automation parks and smart factories in China and India is intensifying demand for connected machining systems and robotic cutting arms. Japan’s precision engineering sector is increasingly integrating sensor-driven and software-optimized machining workflows. Local players such as Yamazaki Mazak are scaling advanced multi-tasking systems addressing productivity increases across micro-to-large component fabrication. Consumer behavior in the region reflects strong demand from e-commerce distribution equipment manufacturing and mobile device supply chains.

Is the demand for Metal Cutting Machines rising due to expanding energy and heavy equipment production?

South America held a 6% share in 2024, led by Brazil and Argentina, where infrastructure, mining equipment, and agricultural machinery production are primary demand drivers. Increasing investments in steel, power, and pipeline projects are pushing the need for laser, plasma, and heavy-duty cutting systems. Government import duty relaxations on production equipment continue to support machine acquisition in Brazil. Local manufacturers in Brazil are upgrading machining workshops to incorporate mid-range CNC capabilities for domestic industrial vehicle fabrication. Consumer trends show growing interest in Metal Cutting Machine solutions that support language-local manufacturing workflows, especially across media, industrial fabrication, and localized hardware production.

Are construction and oil & gas projects driving modernization of Metal Cutting Machine technology?

The region captured 5% of the market in 2024, driven by manufacturing growth in the UAE, Saudi Arabia, and South Africa. Infrastructure development, oil & gas equipment fabrication, and large-scale construction machinery assembly remain core demand channels. Adoption of advanced cutting solutions—robotic machining, plasma cutting for pipeline fabrication, and CNC for heavy steel components—is accelerating modernization. Trade partnerships and free-zone policies supporting capital equipment procurement have strengthened purchasing capacity. Local companies in the UAE have begun deploying digitally monitored machining stations for precision steel fabrication. Regional consumer behavior shows preference toward durable, high-power cutting systems suited for industrial-grade demands rather than SME-centric configurations.

• China – 28% market share – Dominance supported by large-scale industrial machinery and automotive production capacity, high precision-tool consumption, and mature equipment export ecosystem.

• Germany – 17% market share – Leadership driven by strong engineering infrastructure, global automotive exports, and early adoption of advanced CNC and hybrid cutting machines.

The Metal Cutting Machine (MCM) market is highly competitive, with more than 120 active global manufacturers and regional suppliers collectively shaping the industry. The market is moderately consolidated, with the top five companies accounting for approximately 46% of total share, led by strong portfolios in CNC, fiber-laser, and multi-axis machining technologies. Competition is driven by performance optimization, automation integration, and modular equipment architecture designed to reduce production time and improve machining precision. More than 37% of companies introduced new product lines between 2023 and 2024, signaling intensified innovation cycles. Partnerships between machine builders, software integrators, and robotics suppliers increased by nearly 22% in the same period, supporting the transition to smart factory-compatible cutting systems. Mergers and acquisitions remain strategic, particularly among mid-size manufacturers seeking stronger global footprints and access to automated machining IP. AI-driven toolpath optimization, predictive diagnostics, and multi-material capabilities are emerging as differentiating features. Demand for customization and reduced lead-time manufacturing further intensifies competition, particularly in automotive, aerospace, and industrial components where precision tolerances and throughput are critical selection criteria.

Amada Co., Ltd.

Yamazaki Mazak

Bystronic Group

Okuma Corporation

Mitsubishi Electric Corporation

Hypertherm Associates

Lincoln Electric Holdings Inc.

FANUC Corporation

Hurco Companies Inc.

Technological advancement in the Metal Cutting Machine (MCM) market is accelerating the transformation of industrial production, driven by automation, precision control, and smart factory adoption. CNC-based cutting systems now account for over 62% of installations worldwide, offering sub-micron tolerance, digital toolpath programming, and real-time speed–torque adjustments. The rising shift toward fiber-laser cutting technology has improved processing speed by up to 3× compared to CO₂ systems, while simultaneously lowering energy consumption by nearly 28%, enabling high-volume cutting in automotive, aerospace, and general manufacturing sectors.

Hybrid machining platforms that integrate additive and subtractive processes are becoming a major innovation catalyst. More than 19% of new high-end installations in 2024 included hybrid configurations, enabling manufacturers to build base geometries additively and complete precision finishing via metal cutting in the same workstation. Multi-axis machining (5- and 9-axis) continues to gain traction, reducing part setup time by 45% and decreasing machining errors by 32%, especially in industries requiring complex geometries such as turbines, EV components, and medical implants.

Digitalization and AI-driven automation are reshaping MCM deployment strategies. Predictive maintenance systems based on sensor analytics have reduced unplanned downtimes by up to 40%, while adaptive cutting algorithms optimize feedrate and spindle speed autonomously, achieving up to 22% performance gains. Industrial IoT integration enables centralized machine monitoring across distributed facilities, with remote optimization adopted by more than 54% of large-scale manufacturers. Robotics-integrated cutting cells with automated part loading/unloading are scaling rapidly, improving throughput by 35% in fabrication and metalworking plants. Collectively, these technological developments position the Metal Cutting Machine (MCM) market for long-term growth through higher efficiency, reduced production cycles, and smart manufacturing compatibility.

In October 2023, TRUMPF Group announced the launch of its TruMatic 5000 automated punch-laser manufacturing cell, featuring the new SheetMaster material-handling system. The solution delivers fully automated loading, cutting, punching and unloading, enabling reduction of manual intervention and a 30% energy savings through the DeltaDrive electric drive.

In September 2024, TRUMPF introduced the TruLaser Series 3000 Bevel Cut Edition, which generates bevels up to 50° during metal cutting—enabling welded-edge preparation and eliminating separate downstream operations. It supports sheet materials up to 1 inch thick and expands edge-geometry capability beyond previous standards.

In February 2024, Haas Automation unveiled its participation at MACH 2024 showing the TM-0P Toolroom Mill and the ST-15Y Y-axis lathe, both aimed at high-mix/low-volume and lights-out machining scenarios. These machines feature 4th/5th axis options, automatic pallet pools and improved rapid traverse speeds.

In February 2023, TRUMPF’s TruLaser 8000 Coil Edition was launched—a laser blanking system capable of processing up to 25 metric tons of coiled steel automatically, delivering savings of 1,700 metric tons of steel and approximately 4,000 metric tons of CO₂ annually when compared to traditional press-blanking operations.

This Metal Cutting Machine (MCM) Market Report provides a comprehensive overview of equipment types covering laser-cutting systems, plasma cutters, EDM, water-jet cutting, milling machines, turning centres and hybrid multi-process systems. It tracks application verticals including automotive, aerospace, electronics, heavy machinery, energy infrastructure, construction steel fabrication and precision engineering. The report spans key geographic regions—North America, Europe, Asia-Pacific, South America and Middle East & Africa—covering country-level insights where relevant. Type segmentation is explored via machine architecture (2-axis to 9-axis), material focus (ferrous, non-ferrous, composite) and automation layer (manual, semi-automated, fully-automated). Application segmentation assesses production volumes, batch-sizes, and shift from conventional to digital-integrated workflows. End-user profiling identifies automotive OEMs, aerospace component suppliers, metal-fabrication shops, electronics contract manufacturers, and construction equipment makers. Emerging niches such as additive-subtractive hybrid machining cells, multi-material cutting platforms, and “lights-out” unmanned fabrication lines are included. Technology insights evaluate connectivity, IoT-based monitoring, AI-driven process control, and sustainability-driven energy / material-waste metrics. The competitive landscape section reviews market structure, number of active players, alliances, merger activity, regional supply-chains and product-launch frequency. The report culminates in decision-oriented strategic recommendations and market-entry frameworks for stakeholders including machine builders, system integrators, end-users and investors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 68300 Million |

|

Market Revenue in 2032 |

USD 113446.65 Million |

|

CAGR (2025 - 2032) |

5.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TRUMPF Group, DMG MORI, Haas Automation, Amada Co., Ltd., Yamazaki Mazak, Bystronic Group, Okuma Corporation, Mitsubishi Electric Corporation, Hypertherm Associates, Lincoln Electric Holdings Inc., FANUC Corporation, Hurco Companies Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |