Reports

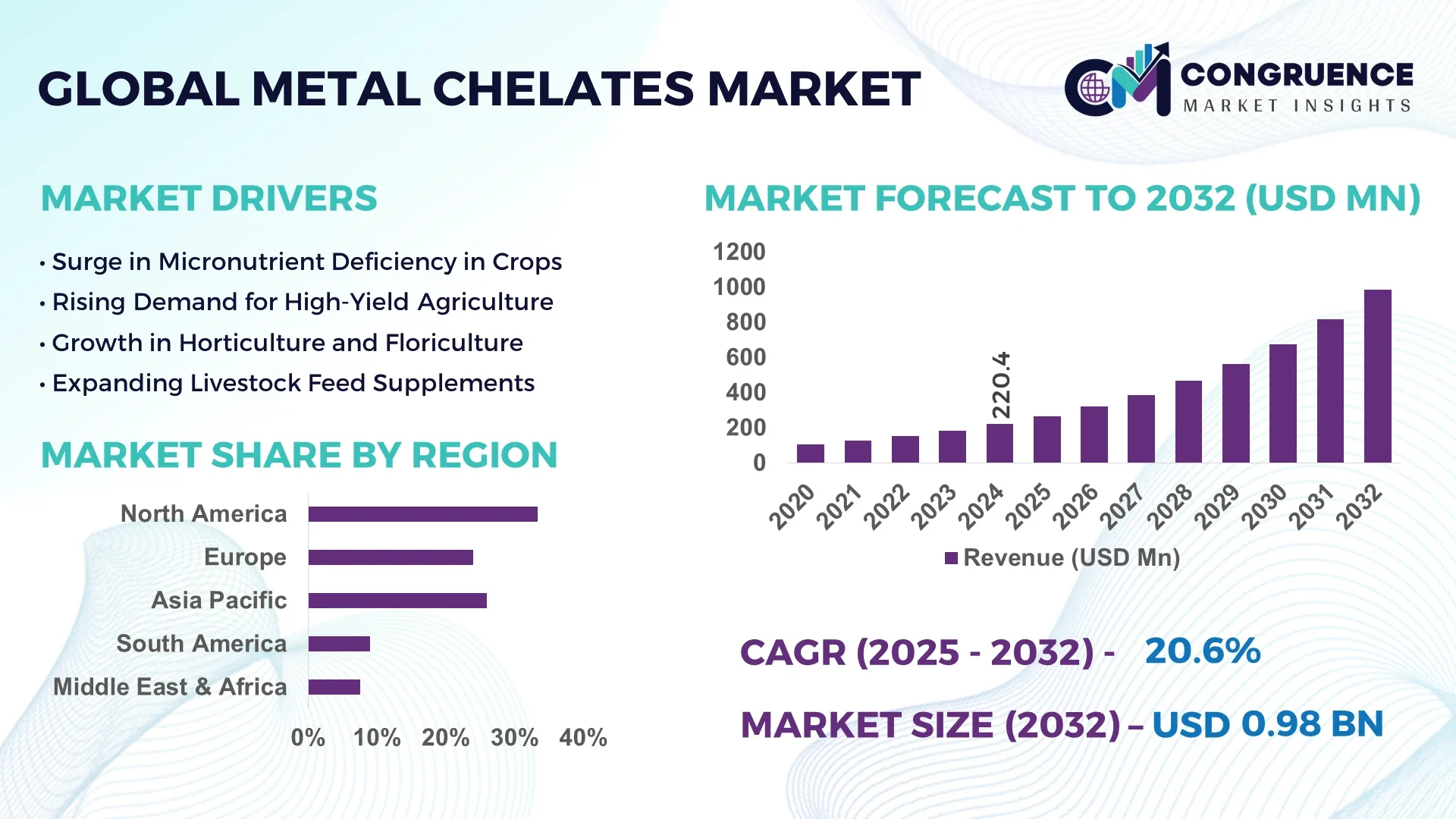

The Global Metal Chelates Market was valued at USD 220.35 Million in 2024 and is anticipated to reach a value of USD 984.07 Million by 2032 expanding at a CAGR of 20.57% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China continues to lead in the Metal Chelates Market, supported by large-scale investments in chelation technology infrastructure, advanced micronutrient application systems in agriculture, and a growing number of R&D centers focusing on enhanced chelate formulation. The country has also integrated metal chelates into its precision farming initiatives and high-efficiency irrigation projects.

The Metal Chelates Market is witnessing rapid transformation across multiple industries driven by environmental regulations, technological advancement, and rising demand for high-efficiency nutrient solutions. In agriculture, chelated micronutrients such as EDTA, DTPA, and EDDHA play a vital role in correcting trace element deficiencies, especially in high-pH and calcareous soils. The market is expanding into industrial segments including water treatment, where chelating agents like NTA and GLDA improve scale control and metal ion sequestration. Additionally, the food and beverage industry is incorporating metal chelates to enhance bioavailability of minerals in fortified products. The emergence of biodegradable and plant-based chelating agents is reshaping product development strategies in response to eco-regulatory trends. Regionally, growth is concentrated in Asia-Pacific and Latin America, where rising agricultural productivity and infrastructure upgrades are driving product uptake. The future outlook remains positive, bolstered by sustainability-focused innovation and increased integration of chelates in diverse end-user applications.

Artificial Intelligence is profoundly reshaping the Metal Chelates Market by driving enhanced decision-making, automation, and efficiency in production, application, and quality control. AI-powered platforms now assist manufacturers in optimizing chelation processes by analyzing real-time data to adjust pH levels, temperature, and ion concentration for maximum efficacy. Predictive algorithms help identify the most effective chelate compounds for specific crop types or industrial applications, reducing waste and improving output quality.

AI integration in agricultural operations utilizing metal chelates enables precision micronutrient delivery based on satellite imagery and soil analytics. This leads to higher yield efficiency and reduced environmental impact. Smart irrigation systems embedded with AI ensure optimal dispersion of chelated fertilizers, minimizing runoff and improving soil retention. In industrial water treatment applications, AI algorithms monitor metal ion concentrations and automatically dose chelating agents to maintain system integrity.

Moreover, AI-driven supply chain analytics offer insights into demand forecasting, logistics optimization, and inventory control for chelate manufacturers. These developments contribute to cost savings and improved customer satisfaction. As AI technologies become more accessible, small and mid-size enterprises in the Metal Chelates Market are also adopting automation solutions to enhance competitiveness, thereby accelerating overall industry digitization and sustainability initiatives.

“In 2024, a leading specialty chemical firm implemented an AI-enabled real-time monitoring system in its metal chelate production facility, which resulted in a 23% increase in process efficiency and a 17% reduction in chemical waste through predictive batch optimization and automated pH control.”

The growing emphasis on sustainable agriculture practices is significantly accelerating the adoption of chelated micronutrients across global farming operations. Metal chelates enhance nutrient efficiency by preventing micronutrient precipitation in alkaline and calcareous soils, a common challenge in large agricultural regions of Asia and Africa. Governments and agri-tech firms are promoting their use through precision farming programs and nutrient management initiatives. For example, the widespread application of iron and zinc chelates has been linked to a 30% increase in crop yield in micronutrient-deficient regions. Additionally, the compatibility of chelated fertilizers with drip and foliar application systems supports sustainable water and resource use, aligning with global climate-resilient agriculture strategies. As food demand rises with population growth, the need for productive yet eco-friendly agricultural inputs will continue to drive the Metal Chelates Market forward.

Despite the growing demand, high production costs and complex manufacturing processes continue to restrict the widespread adoption of metal chelates. The synthesis of stable chelating compounds, particularly those suitable for environmentally sensitive applications, requires advanced technology, specialized equipment, and costly raw materials like EDTA and DTPA. These costs are often transferred to end-users, making metal chelates less attractive compared to conventional fertilizers and water treatment chemicals, especially in price-sensitive markets. Moreover, the need for controlled conditions during manufacturing—such as precise pH levels, temperature regulation, and ion balance—adds to operational expenditure. In industries where cost-efficiency is critical, such as smallholder farming or municipal water treatment, these restraints may delay or limit uptake. Until production scalability improves and input costs are optimized, this factor will remain a barrier to full-scale market penetration.

Beyond traditional agricultural use, the Metal Chelates Market is discovering promising opportunities in industrial and cosmetic sectors. In industrial water treatment, chelating agents are increasingly adopted for their ability to prevent scale buildup, corrosion, and heavy metal contamination in boilers and cooling systems. With industrial output expanding globally, especially in developing countries, demand for efficient and environmentally safe water treatment solutions is growing. Simultaneously, the cosmetics and personal care industry is integrating metal chelates like EDTA to enhance product stability, improve shelf life, and neutralize metallic impurities in formulations. For example, skincare brands are leveraging chelated ingredients to stabilize vitamin C serums, which are highly susceptible to oxidation. This diversification of application areas opens up substantial opportunities for manufacturers to innovate and cater to premium, regulation-compliant market segments.

The Metal Chelates Market faces ongoing challenges from increasingly stringent regulatory standards aimed at curbing environmental pollution and enhancing chemical safety. Chelating agents such as EDTA and DTPA, while effective, are non-biodegradable and can persist in ecosystems, raising concerns about aquatic toxicity and long-term soil health. Regulatory agencies in Europe and North America have imposed usage restrictions or are considering bans on specific formulations, compelling manufacturers to reformulate products or invest in eco-friendly alternatives. This transition increases R&D and compliance costs, particularly for smaller market players. Additionally, obtaining certifications for new formulations under REACH or EPA regulations requires extensive documentation and testing, which can delay product launches and reduce market agility. These regulatory pressures demand strategic investment and innovation, but they also impose significant challenges to maintaining competitiveness and sustainability.

• Surge in Bio-Based Chelating Agents:

Environmental concerns and rising restrictions on traditional chelating compounds like EDTA are fueling the demand for biodegradable, plant-based alternatives. Bio-based chelates derived from natural acids and fermentation processes are gaining popularity due to their lower toxicity and compatibility with organic agriculture. Several manufacturers have launched sustainable product lines utilizing these alternatives, with adoption rates increasing by over 35% in European agricultural sectors in 2024. This shift aligns with eco-labeling demands and regulatory incentives promoting green chemistry across the food production and water treatment industries.

• Technological Advancements in Chelation Stability:

Innovations in chelation chemistry are driving the development of more stable compounds capable of withstanding extreme pH ranges and high salinity. Advanced formulations now allow micronutrients like zinc, copper, and iron to remain soluble longer, increasing nutrient uptake efficiency in poor soil conditions. In 2024, companies reported a 28% improvement in nutrient delivery efficiency using next-gen synthetic chelates compared to legacy products, contributing to increased agricultural productivity and cost-effectiveness.

• Expanding Use in Pharmaceutical and Nutraceutical Formulations:

Chelated minerals are being increasingly integrated into pharmaceutical and dietary supplement formulations to enhance bioavailability. Iron chelates and magnesium chelates, in particular, have shown higher absorption rates in clinical studies, leading to more effective treatments for anemia and metabolic disorders. The pharmaceutical industry in North America and Japan has notably expanded its use of chelated ingredients, with production volumes doubling between 2022 and 2024.

• Integration into Circular Water Management Systems:

Municipal and industrial water treatment sectors are deploying metal chelates to manage heavy metal contamination and scale buildup. With stricter discharge standards, there is a growing demand for chelating agents that enable the reuse of processed water. In 2024, several Asian wastewater facilities integrated chelation systems into their operations, resulting in a 42% reduction in metal ion concentration in treated water. This advancement supports long-term sustainability goals and compliance with environmental norms.

The Metal Chelates Market is segmented into three key dimensions: type, application, and end-user. Each segment reflects unique growth dynamics shaped by evolving technological, environmental, and industrial requirements. In terms of type, synthetic and bio-based chelating agents are central to addressing diverse industry demands ranging from agriculture to personal care. Application areas such as soil treatment, industrial processing, and pharmaceuticals show high variation in adoption and innovation levels. From an end-user perspective, sectors including agriculture, healthcare, and water treatment exhibit strong, differentiated consumption patterns. The interplay between these segments offers insights into the market’s complexity and expansion trajectory, with manufacturers tailoring solutions to meet increasingly specific technical and regulatory standards across regions.

Synthetic chelates, particularly those based on EDTA and DTPA, currently dominate the Metal Chelates Market due to their proven effectiveness in micronutrient stabilization and broad industrial compatibility. These types have shown strong performance across soil treatment and water purification processes. However, bio-based chelating agents are the fastest-growing segment, propelled by regulatory pressures to reduce chemical persistence and promote environmental sustainability. Products such as IDHA and GLDA are gaining favor for their biodegradability and compatibility with organic agriculture. Meanwhile, amino acid chelates are carving a niche in the pharmaceutical and nutraceutical industries due to superior absorption rates and minimal side effects. Polyaminocarboxylic acids and phosphonate-based chelates also contribute to specialized applications, such as scale inhibition in industrial settings. Each type offers unique benefits and constraints, shaping its relevance across sectors.

Agricultural micronutrient management remains the leading application of metal chelates, with widespread use in fertilizers to combat soil nutrient deficiencies. Chelates of iron, zinc, and copper are extensively used to improve crop yields in alkaline and calcareous soils. The fastest-growing application is in water treatment systems, where chelating agents assist in metal ion control and scale prevention, especially in industrial boilers and cooling towers. Pharmaceutical and nutraceutical uses are also expanding as chelated minerals gain attention for their higher bioavailability and therapeutic efficacy. Additionally, metal chelates are being explored in cosmetics to enhance product stability and in food fortification processes. The diversity of application areas continues to grow as research introduces more refined and targeted chelation technologies.

The agriculture sector is the leading end-user of metal chelates, driven by the increasing demand for high-yield, nutrient-rich crops in regions with micronutrient-deficient soils. Farmers and agrochemical companies continue to adopt chelated micronutrient solutions to enhance efficiency and reduce environmental impact. The fastest-growing end-user segment is the pharmaceutical and nutraceutical industry, which is incorporating chelated minerals into therapeutic formulations due to their improved absorption and patient compliance. Industrial users, especially in water treatment and manufacturing, are leveraging chelates for metal ion control and operational efficiency. Cosmetics and personal care manufacturers also utilize chelating agents to maintain product integrity and compliance with regulatory standards. This broad end-user spectrum underscores the versatility and essential role of metal chelates in modern industrial and consumer applications.

North America accounted for the largest market share at 33.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The North American market is characterized by robust demand from the agriculture and pharmaceutical sectors, supported by established manufacturing infrastructure and technological integration. In contrast, Asia-Pacific is experiencing rapid industrial expansion, increasing investments in sustainable agriculture, and growing pharmaceutical production—especially in China, India, and Southeast Asia. Europe holds a significant share as well, driven by stringent environmental regulations promoting bio-based chelating agents. Meanwhile, South America and the Middle East & Africa are emerging as opportunity-rich markets due to agricultural modernization efforts and infrastructural growth. This regional diversity reflects a competitive yet fragmented market landscape for metal chelates, with tailored strategies needed for each geography.

Sustainable Agriculture and Healthcare Innovation Driving Growth

The Metal Chelates market in this region commanded a 33.4% market share in 2024, fueled by strong adoption across agricultural and pharmaceutical sectors. Key drivers include widespread use of chelated micronutrients in precision farming and the high integration of chelated minerals in nutraceutical and pharmaceutical formulations. Government support through subsidies and sustainable farming programs further propels adoption. The United States remains the dominant contributor, with advanced R&D infrastructure enabling high-performance formulations. Canada is following suit with increasing adoption in organic farming and water treatment. Additionally, technological innovations such as bio-based chelating compounds and AI-enabled nutrient delivery systems are gaining momentum, contributing to enhanced market penetration and long-term sustainability.

Sustainability Mandates and Technological Adoption Shape the Market

Holding a 27.6% share in 2024, the European market is driven by sustainability-focused regulations and the widespread use of metal chelates in advanced agriculture and industrial wastewater management. Germany, the UK, and France are the top contributors, owing to large-scale adoption of organic farming practices and increasing restrictions on conventional chemical use. Organizations such as the European Chemicals Agency (ECHA) are enforcing strict environmental guidelines, encouraging the use of biodegradable chelating agents. Additionally, technological advancements in chelation chemistry and automation in agriculture further enhance market potential. The transition toward circular economies is also encouraging the use of metal chelates in environmental remediation applications across the region.

Rapid Industrialization and Agrochemical Demand Fuel Market Surge

Asia-Pacific ranks as the fastest-growing region for the Metal Chelates market, with countries like China, India, and Japan driving demand through expansive agriculture, industrialization, and pharmaceutical development. The region accounted for 21.9% of global volume in 2024 and is poised for significant growth due to increasing awareness of micronutrient deficiencies in crops and human nutrition. Infrastructure development, including the expansion of irrigation systems and precision farming tools, is boosting chelate usage in agriculture. Additionally, Japan’s innovation in healthcare and China's large-scale pharmaceutical production enhance product penetration. Emerging manufacturing hubs and supportive government policies across Southeast Asia also contribute to regional competitiveness and technological advancement.

Agricultural Expansion and Government Incentives Catalyze Growth

With a market share of 8.7% in 2024, this region is gradually emerging as a strategic hub for Metal Chelates, led by Brazil and Argentina. Brazil’s significant investments in modernizing agriculture and increasing awareness of soil micronutrient deficiencies are key growth drivers. Argentina’s export-oriented crop production further supports sustained demand. Government-led initiatives encouraging the use of micronutrient-enriched fertilizers and trade policies favoring agrochemical imports contribute to market advancement. Infrastructure improvements in irrigation and farm management, combined with the introduction of digital agriculture technologies, are accelerating the adoption of chelated micronutrients in both small and large-scale farming operations.

Industrial Modernization and Water Management Drive Uptake

In 2024, the region contributed 8.4% to the global Metal Chelates market. Demand is being driven by the oil & gas industry’s increasing focus on environmentally friendly water treatment solutions and the construction sector's growth across the UAE, Saudi Arabia, and South Africa. With growing urbanization and desert agriculture initiatives, countries are adopting advanced soil and water management systems that leverage chelating technologies. South Africa’s pharmaceutical sector is also rising, incorporating chelated minerals in health supplements. Furthermore, regional partnerships and trade agreements are boosting imports of chelating products, while localized R&D initiatives aim to address specific environmental and agricultural challenges through customized solutions.

United States – 29.1% market share

Strong end-user demand in agriculture and pharmaceuticals, supported by technological leadership and infrastructure.

China – 18.7% market share

High production capacity and rapid industrial adoption of metal chelates across agrochemical and water treatment sectors.

The Metal Chelates market is characterized by a moderately fragmented yet intensifying competitive environment, with over 75 active players operating globally. Leading companies are differentiating themselves through specialization in chelation technology, eco-friendly formulations, and product innovation targeting specific applications such as agriculture, pharmaceuticals, and industrial water treatment. Market leaders are focusing on the development of biodegradable and non-toxic chelating agents to comply with evolving regulatory standards, particularly in Europe and North America.

Strategic partnerships and collaborations are playing a pivotal role in market positioning, as companies aim to expand distribution networks and co-develop tailored solutions for end-users. Several key players have launched advanced micronutrient delivery systems for agriculture and mineral-enriched formulations for health supplements. Mergers and acquisitions have also shaped the competitive landscape, enabling firms to enhance their R&D capabilities and global reach. Additionally, regional players are leveraging low-cost manufacturing and local distribution strength to challenge multinational brands, especially in Asia-Pacific and Latin America. The pace of innovation, particularly in nanotechnology-enhanced chelates and AI-driven formulation processes, is a defining factor that is reshaping competitive dynamics.

BASF SE

AkzoNobel N.V.

Haifa Chemicals Ltd.

Syngenta AG

Nufarm Ltd.

Valagro S.p.A.

Van Iperen International

Aries Agro Limited

Deretil Agronutritional

Shandong IRO Chelating Chemical Co., Ltd.

ATP Nutrition

Grupa Azoty Zakłady Chemiczne "Police" S.A.

Agroplasma SL

The Metal Chelates market is experiencing significant technological advancements, particularly in the development of eco-friendly and efficient chelating agents. One notable innovation is the introduction of biodegradable chelating agents, such as GLDA (glutamic acid diacetic acid) and MGDA (methylglycine diacetic acid), which offer effective metal ion binding while minimizing environmental impact. These agents are gaining traction in agriculture and industrial applications due to their high biodegradability and low toxicity. Nanotechnology is also playing a pivotal role in enhancing the performance of metal chelates. Nanoscale chelates exhibit improved solubility and stability, enabling more efficient nutrient delivery in agricultural practices. For instance, nano-chelated fertilizers are being developed to facilitate targeted nutrient release, reducing waste and improving crop yields. Additionally, the integration of nanomaterials in chelating agents is expanding their applications in water treatment and pharmaceuticals, where precise metal ion control is crucial.

Furthermore, advancements in synthesis methods, such as microwave-assisted and ultrasonic techniques, are streamlining the production of metal chelates. These methods offer faster reaction times and higher yields, contributing to cost-effective manufacturing processes. The adoption of green chemistry principles in synthesis is also promoting the development of sustainable chelating agents, aligning with global environmental regulations. In the realm of industrial applications, metal chelates are being tailored for specific processes, such as catalysis and metal plating. Customized chelating agents are being designed to enhance selectivity and efficiency in these processes, leading to improved product quality and reduced environmental impact. Overall, the continuous technological evolution in the Metal Chelates market is driving innovation across various sectors, offering sustainable and efficient solutions for metal ion management.

In April 2024, Inolex, Inc. launched Spectrastat CHA, a natural, palm-free powdered chelating agent derived from coconut. This product offers a sustainable alternative for formulators seeking effective preservation solutions in personal care applications.

In October 2023, Nouryon introduced Berol Nexxt and Dissolvine GL Premium at the SEPAWA Congress in Berlin. Dissolvine GL Premium is noted as the most concentrated GLDA-based chelating agent available, enhancing performance in cleaning and personal care products.

In February 2023, Aries Agro Limited's flagship brand, Aries Chelamin, received the ISI mark for chelated zinc from the Bureau of Indian Standards. This recognition underscores the product's quality and compliance with national standards in India.

In March 2023, BASF announced the successful commercial-scale production of metal-organic frameworks (MOFs) for carbon capture applications. This development marks a significant step in utilizing advanced materials for environmental sustainability initiatives.

The Metal Chelates Market Report provides an in-depth analysis of the global landscape, examining structural trends, segment performance, technological innovations, and geographic distribution. The report covers a wide array of chelating agents, including EDTA, DTPA, EDDHA, IDHA, GLDA, and others, across multiple applications. Each compound is analyzed based on its chemical stability, solubility, and efficacy across agriculture, pharmaceuticals, industrial cleaning, water treatment, and personal care industries. The report offers a detailed segmentation by type, application, and end-user. It investigates the leading market contributors such as EDTA, widely utilized in industrial water treatment, and EDDHA, which is gaining traction in agriculture for micronutrient management in alkaline soils. Applications across agriculture dominate market usage, particularly in micronutrient fertilizers, with substantial demand from developing nations. Industrial and pharmaceutical applications are also evaluated, particularly where high-purity chelation is essential.

Geographically, the market analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each region is assessed for consumption volume, industrial base, regulatory frameworks, and key growth drivers. The report highlights China, India, the U.S., and Germany as major country-level markets due to strong industrial and agricultural output. Additionally, the report explores emerging areas such as bio-based chelating agents and nano-chelated compounds, which are rapidly gaining acceptance due to environmental considerations and enhanced performance. The scope also includes technological trends in synthesis processes and applications in sustainability-driven sectors like renewable energy and green chemistry, providing a forward-looking view tailored for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 220.35 Million |

|

Market Revenue in 2032 |

USD 984.07 Million |

|

CAGR (2025 - 2032) |

20.57% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, AkzoNobel N.V., Haifa Chemicals Ltd., Syngenta AG, Nufarm Ltd., Valagro S.p.A., Van Iperen International, Aries Agro Limited, Deretil Agronutritional, Shandong IRO Chelating Chemical Co., Ltd., ATP Nutrition, Grupa Azoty Zakłady Chemiczne "Police" S.A., Agroplasma SL |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |