Reports

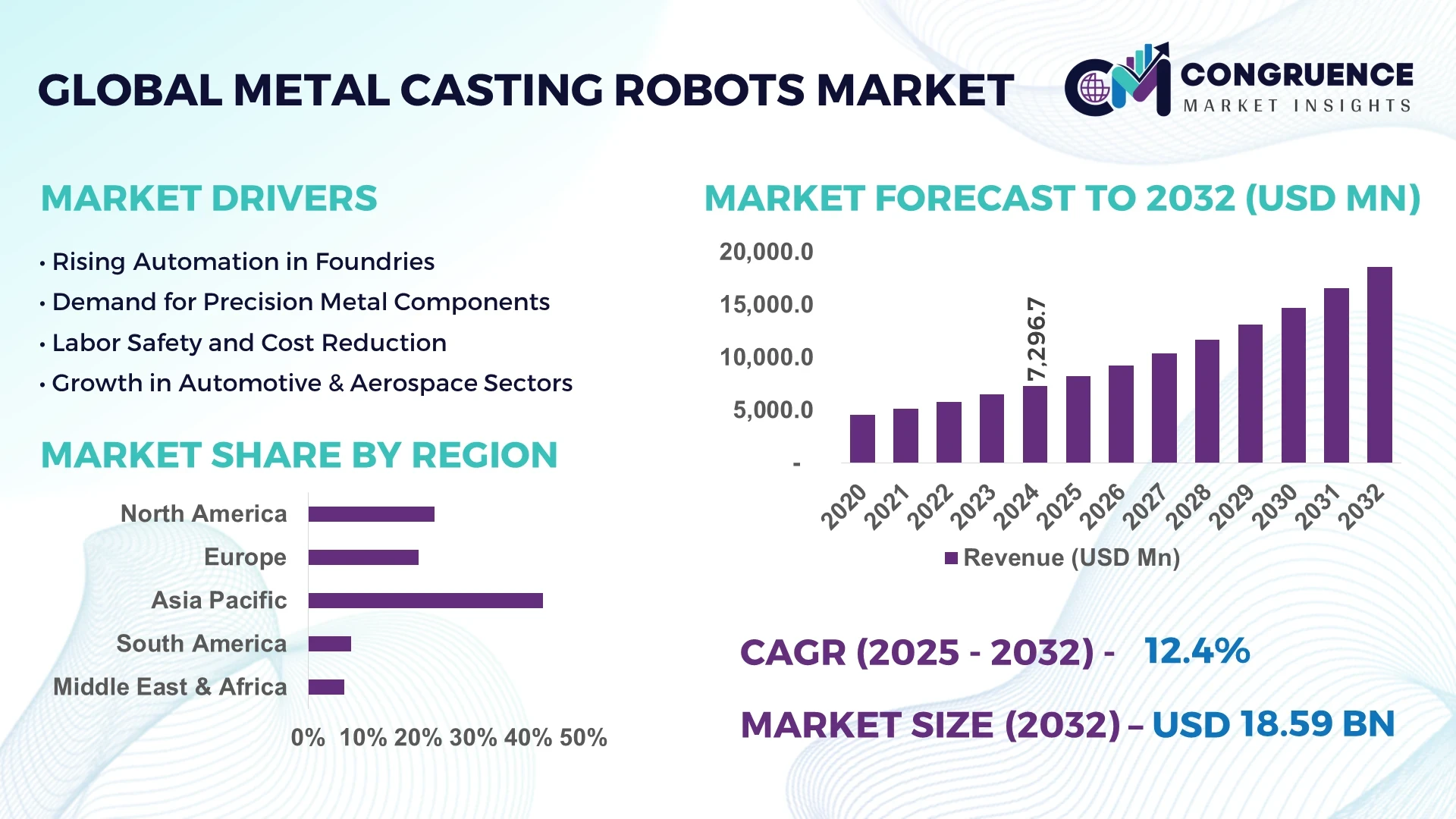

The Global Metal Casting Robots Market was valued at USD 7,296.67 Million in 2024 and is anticipated to reach a value of USD 18,588.96 Million by 2032 expanding at a CAGR of 12.4% between 2025 and 2032.

Japan, a leading force in industrial automation, has significantly advanced its metal casting robot production with several robotics manufacturers expanding facilities and integrating cutting-edge AI controls into their foundry applications, notably across automotive and heavy machinery sectors.

The Metal Casting Robots Market is witnessing a robust surge due to the increasing demand for high-precision and cost-effective manufacturing in industries such as automotive, aerospace, and industrial equipment. Innovations such as 6-axis robotic arms, real-time defect detection systems, and adaptive motion control have revolutionized casting precision and reliability. Regulatory pressure for safer work environments and energy-efficient operations is driving industries to adopt robotic automation. Foundries in Asia-Pacific and North America have seen increased adoption rates due to regional labor cost concerns and skill shortages. Environmental standards for emission reduction are pushing for cleaner and automated metal casting processes. Moreover, hybrid robotic systems with IoT integration are improving real-time monitoring and predictive maintenance. The market is poised for expansion as advanced robotics, sensor integration, and AI analytics continue transforming traditional casting lines into smart, efficient manufacturing hubs.

AI is transforming the Metal Casting Robots Market by enhancing the intelligence, adaptability, and precision of robotic operations across casting processes. Industrial robots now utilize machine learning algorithms to optimize pouring angles, monitor thermal behavior, and minimize metal waste during mold filling. These capabilities have significantly improved casting accuracy and consistency in high-volume production environments. Manufacturers are integrating AI-powered computer vision systems that detect casting defects such as shrinkage, porosity, and misruns in real time, reducing quality assurance costs by over 30%.

AI also enables adaptive process controls that adjust robotic performance based on variations in mold materials or environmental conditions, ensuring stable output without manual intervention. The Metal Casting Robots Market is also benefiting from predictive maintenance technologies, where AI algorithms analyze vibration, temperature, and load data to forecast mechanical failures before downtime occurs. In heavy industry applications like steel and aluminum casting, AI-integrated robots now manage hazardous operations with precision, enhancing both productivity and operator safety. Furthermore, AI-driven digital twins are being deployed to simulate entire casting cells, reducing the lead time for system reconfiguration by up to 40%. As industries embrace smart manufacturing, AI is becoming a strategic pillar in optimizing performance, reducing costs, and driving innovation in the Metal Casting Robots Market.

“In March 2024, a leading industrial robotics firm introduced an AI-integrated robotic casting cell that achieved a 25% increase in throughput by using predictive pouring control and thermal imaging to prevent casting defects in high-temperature aluminum applications.”

The Metal Casting Robots Market is undergoing significant transformation, driven by automation trends, safety concerns, and the increasing demand for high-volume precision casting. As industries seek to improve operational efficiency and reduce manual labor exposure to extreme heat and molten metals, metal casting robots are becoming integral to modern foundries. Adoption is particularly strong in automotive, aerospace, and industrial machinery manufacturing, where casting quality and repeatability are critical. Technological enhancements such as AI integration, advanced motion control, and real-time defect detection are strengthening market traction. Additionally, the shift toward Industry 4.0 is pushing companies to digitize and automate traditional casting workflows. Environmental regulations and labor shortages further influence the global expansion of robotic casting systems. The market is characterized by rapid advancements in robot flexibility, payload capabilities, and adaptive learning systems tailored for complex casting geometries and multi-metal operations.

The need to reduce workplace accidents and improve production consistency is significantly boosting the deployment of robots in the casting sector. Foundry operations involve hazardous environments with high temperatures, heavy loads, and exposure to toxic fumes. Metal casting robots eliminate these risks by automating tasks such as mold pouring, ladle handling, and post-casting trimming. According to industry assessments, foundries that implement robotic automation report up to a 45% reduction in workplace injuries and a 35% increase in operational throughput. This driver is especially critical in economies with stringent occupational safety regulations. In addition, robotic automation allows for continuous operation without fatigue, which results in improved production cycles and cost-efficiency across industries, including automotive and heavy industrial machinery. The scalability and precision offered by modern casting robots are further reinforcing their importance in meeting growing manufacturing demands.

One of the primary restraints in the Metal Casting Robots Market is the high upfront capital required for procurement, system integration, and operator training. Mid-sized foundries, especially in emerging economies, face difficulty justifying the return on investment due to limited production volumes or lack of technical expertise. Installing robotic casting systems demands infrastructure upgrades, including reinforced work cells, safety cages, and integration with existing PLC systems. Moreover, skilled personnel are needed to program, maintain, and troubleshoot robotic systems, adding to the operational burden. For small and medium enterprises (SMEs), these requirements may lead to delayed adoption or reliance on conventional semi-automated machinery. Additionally, when production needs shift or molds are changed frequently, reprogramming robots can cause extended downtime, further discouraging adoption in dynamic production environments.

The rise of smart foundry concepts presents a significant opportunity for growth in the Metal Casting Robots Market. Advanced robotic systems now come equipped with IoT sensors, AI-enabled controllers, and cloud-based data analytics that enhance real-time decision-making and process optimization. These smart technologies allow robots to self-adjust for variable inputs such as temperature, mold conditions, or metal composition, improving accuracy and reducing waste. The growing trend of digital twins—virtual replicas of casting cells—helps in simulating processes before deployment, minimizing production risks. Industrial manufacturers, particularly in Germany, Japan, and South Korea, are investing in smart factory models that prioritize robotic integration to meet zero-defect goals. Additionally, increased government funding in automation R&D and digital infrastructure is opening doors for new market entrants offering modular, scalable casting robots tailored for Industry 4.0 applications.

Despite technological advances, robots still face challenges in managing intricate casting processes involving multiple alloys, varying mold shapes, or extreme environmental conditions. Complex casting geometries, such as thin-walled turbine components or asymmetrical automotive parts, require high-precision manipulation and real-time process adjustments that some conventional robotic systems struggle to accommodate. In addition, maintaining consistent metal flow and preventing defects like air entrapment or misrun during pouring requires advanced coordination between robots and auxiliary equipment. These limitations can result in quality issues, rework, or scrap, especially in high-specification industries like aerospace and defense. Moreover, robotic systems exposed to excessive heat and particulate matter during molten metal handling experience accelerated wear, increasing the frequency and cost of maintenance. Overcoming these challenges demands continuous innovation in materials, cooling systems, and sensor technology tailored for extreme casting environments.

• Surge in 6-Axis Robotic Arm Deployments: The Metal Casting Robots market is experiencing a sharp increase in the deployment of 6-axis robotic arms, particularly in complex foundry environments. These multi-jointed robots offer greater flexibility and precision, enabling them to perform intricate pouring and trimming tasks previously managed manually. Adoption of 6-axis systems grew by over 38% in 2024, driven by demand in automotive and aerospace sectors where irregular geometries and multi-metal casting processes are common.

• Integration of AI-Powered Quality Control Systems: AI-based vision and thermal imaging systems are being widely integrated into casting robots to improve product quality and reduce defects. These technologies automatically detect casting anomalies such as voids or cracks with up to 95% accuracy, significantly reducing rework and scrap rates. The inclusion of real-time analytics and adaptive machine learning has transformed quality assurance into a predictive and proactive function across major foundries.

• Expansion of Robotic Use in Non-Ferrous Metal Applications: Robotic systems are increasingly used in the handling and casting of non-ferrous metals like aluminum and magnesium due to their lightweight and heat-sensitive properties. These metals require high-precision control and minimal thermal disturbance, which robots equipped with advanced cooling and temperature sensors can deliver. Adoption has accelerated across EV component manufacturing and lightweight aerospace structures.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Metal Casting Robots market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

The Metal Casting Robots market is segmented into three primary categories: type, application, and end-user. In terms of type, robot systems include various configurations such as 4-axis, 6-axis, and SCARA robots, each suited for specific foundry needs. Applications range from mold handling and metal pouring to trimming and post-casting operations. Automotive and aerospace industries dominate usage, while other sectors like defense and construction materials are emerging rapidly. End-user analysis reveals that large-scale manufacturing facilities currently lead the adoption curve due to high-volume demands and capital readiness. However, mid-sized enterprises are entering the space faster than anticipated, driven by automation incentives and modular robot availability. This segmentation illustrates how demand for speed, accuracy, and safety is steering robot usage across diverse manufacturing environments.

In the Metal Casting Robots market, 6-axis robots represent the leading segment due to their enhanced flexibility, reach, and multi-directional movement, making them ideal for intricate and high-precision casting operations. These robots dominate foundries producing complex parts like engine blocks and turbine components. The fastest-growing type is collaborative robots (cobots), which are increasingly being introduced in mid-sized casting operations due to their ease of integration, safety features, and ability to work alongside human workers. Cobots are seeing a notable surge in smaller metal fabrication shops where space and budget constraints exist. 4-axis robots continue to be used for repetitive, high-speed tasks in less complex pouring operations, especially in bulk metal part production. Meanwhile, SCARA robots maintain a niche presence for horizontal casting applications where space constraints and fast cycle times are critical. Hybrid robotic solutions that combine mobility with precision are also emerging in pilot-scale deployments across Europe and Asia.

Among all application areas, molten metal pouring leads the Metal Casting Robots market due to its inherent danger, precision requirements, and the critical nature of metal flow consistency in casting quality. Automated pouring systems have reduced defect rates by over 30% in automotive production lines. Trimming and deburring is the fastest-growing application segment, fueled by the rise in demand for post-casting finishing accuracy and labor shortage in manual finishing jobs. Robotic trimming ensures consistent surface quality, particularly for aluminum and magnesium alloy castings. Core handling is gaining attention in advanced foundries dealing with complex mold assemblies that require careful placement and orientation. Robots are also being used in die spraying and mold coating processes to maintain cycle uniformity and reduce human exposure to hazardous chemicals. Across applications, the convergence of automation with sensor data has made robots integral in achieving zero-defect production goals.

The automotive industry remains the leading end-user segment for metal casting robots, owing to its large-scale component production needs and a high degree of automation maturity. Foundries producing engine blocks, transmission housings, and brake components extensively rely on robotic systems to maintain throughput and quality. The aerospace sector is the fastest-growing end-user due to its stringent component tolerances, lightweight material usage, and increasing demand for precision casting in turbine blades and structural components. Aerospace foundries are investing in robotic automation to meet production scalability while adhering to quality certifications. Heavy machinery and industrial equipment manufacturers also utilize metal casting robots, especially for producing large components with consistent dimensional accuracy. Emerging sectors such as renewable energy and defense are beginning to deploy robotic casting cells for prototype and limited-scale production, focusing on parts like wind turbine hubs and structural mounts. These diverse end-user demands are propelling specialized robot innovations tailored to unique operational needs.

Asia-Pacific accounted for the largest market share at 42.7% in 2024 however, Region North America is expected to register the fastest growth, expanding at a CAGR of 13.5% between 2025 and 2032.

The Asia-Pacific region leads due to its dominant manufacturing ecosystem, advanced robotic infrastructure, and high-volume automotive production facilities, especially in China, Japan, and South Korea.

The Metal Casting Robots Market exhibits strong regional diversity driven by differing levels of automation, industrial base maturity, and regulatory environments. Asia-Pacific remains the key contributor due to its expansive foundry infrastructure and heavy adoption of robotic automation in automotive and aerospace manufacturing. North America is rapidly gaining momentum with increased investment in smart foundries and AI-integrated robotic systems. Europe follows closely, supported by sustainability initiatives and a strong push for digitized production across Germany, France, and the UK. Meanwhile, South America is gradually expanding with growing demand in Brazil’s industrial and automotive sectors, while the Middle East & Africa market is being shaped by construction and energy-related developments. Across all regions, supportive government policies, digital transformation initiatives, and skilled labor shortages are fueling the uptake of metal casting robots across diverse end-use industries.

Smart Automation Driving Efficiency Across Advanced Foundries

The Metal Casting Robots Market in this region secured a market share of 21.3% in 2024, driven by the strong presence of automotive and aerospace industries. Manufacturers across the U.S. and Canada are rapidly automating foundry processes to reduce labor exposure to hazardous conditions and enhance casting precision. Government programs supporting industrial modernization, including tax credits for robotic automation, are accelerating investments in robotic cells for casting operations. Technological innovations such as AI-integrated robotic arms, predictive maintenance systems, and cloud-based performance monitoring are becoming standard in Tier-1 supplier foundries. The market is also influenced by stricter workplace safety regulations and sustainability standards that favor robotic integration. As the demand for EVs grows, so does the requirement for precision-cast aluminum parts, further amplifying regional adoption.

Green Manufacturing Standards Fueling Robotic Transformation

Holding 18.6% of the global market share in 2024, this region is driven by strong automation adoption across key nations like Germany, the UK, and France. Foundries are investing heavily in advanced robotics to meet EU emission norms and labor safety directives. Germany leads in robot deployment across automotive casting operations, while France and the UK show growing uptake in defense and industrial component manufacturing. The European Union's green transition policies, including energy efficiency targets and waste minimization strategies, are directly impacting the robotization of metal casting lines. Digital twins, AI vision systems, and cobots are becoming more common in European smart foundries. Collaborative efforts among governments, research institutions, and robotics firms continue to foster cutting-edge innovations in this region.

Manufacturing Powerhouse Accelerating Robotic Integration

Asia-Pacific recorded the highest market volume in 2024, accounting for 42.7% of the global Metal Casting Robots Market. China, India, and Japan are the top consumers, with significant investments in manufacturing infrastructure and digital transformation. China's automotive and heavy machinery industries are leveraging robotic casting systems for mass production scalability and safety enhancement. India is seeing rising demand from mid-sized foundries seeking to reduce defects and labor costs, while Japan continues to lead in technology-driven automation with proprietary robotics innovations. Government support for Industry 4.0 and increased funding for smart factory initiatives across Southeast Asia is further propelling adoption. Regional innovation hubs such as Shenzhen, Tokyo, and Bengaluru are fostering advancements in robot precision, thermal sensing, and adaptive AI learning models.

Industrial Growth and Foundry Upgrades Driving Adoption

Brazil and Argentina are the primary contributors to this region’s Metal Casting Robots Market, which captured 5.9% of the global share in 2024. The region is witnessing gradual but steady growth driven by expanding automotive, mining, and construction industries. Brazil’s steel and aluminum casting operations are undergoing modernization through the integration of automated pouring systems and robotic trimming cells. Argentina is leveraging public-private partnerships to improve industrial competitiveness through robotic automation. Infrastructure development and energy sector expansion are further fueling demand for cast components produced with robotic accuracy. Government incentives in Brazil to promote Industry 4.0 adoption are expected to further drive the integration of AI-enhanced robotic systems in mid-sized and large foundries.

Energy and Construction Demands Powering Robotic Evolution

With a market share of 3.8% in 2024, this region is showing promising growth in the Metal Casting Robots Market. UAE and South Africa lead in demand due to their expanding construction and oil & gas sectors. These industries require precision metal parts, often produced under high-heat and high-risk conditions, making robotics a logical investment. UAE’s push towards smart city development and advanced manufacturing has led to increased automation in local foundries. South Africa is upgrading its foundry base with assistance from international automation firms to improve production efficiency and worker safety. Regional growth is also supported by trade partnerships and national policies aimed at reducing industrial downtime and improving output quality through robotic integration.

China – 28.4% market share

High production capacity and significant investments in automotive and industrial robotics infrastructure.

United States – 19.7% market share

Strong end-user demand in aerospace and automotive foundries combined with advanced technological capabilities in AI and automation.

The Metal Casting Robots market is characterized by intense competition among over 40 active global and regional players offering diverse robotic solutions tailored to foundry operations. Leading robotics manufacturers are competing through innovations in precision pouring, thermal regulation, and AI-integrated defect detection systems. Strategic initiatives such as collaborations with casting system integrators and partnerships with automotive OEMs are reshaping the market structure. In 2024 alone, several companies launched next-generation robotic casting arms with enhanced payload capabilities, faster cycle times, and smart control interfaces, reinforcing the innovation race.

Product differentiation through AI, IoT integration, and energy efficiency enhancements is a core strategy among top-tier competitors. Companies are also expanding into emerging markets in Asia-Pacific and South America by offering modular robotic systems and post-sale service ecosystems. Mergers and acquisitions are on the rise, with players seeking to strengthen their automation portfolios and expand geographic reach. Mid-sized manufacturers are gaining traction by focusing on niche applications such as non-ferrous metal casting and hybrid automation systems. The competitive landscape remains dynamic, shaped by digital transformation trends, labor cost dynamics, and evolving regulatory standards across industrial sectors.

FANUC Corporation

Yaskawa Electric Corporation

KUKA AG

ABB Ltd.

Kawasaki Heavy Industries, Ltd.

Comau S.p.A

Staubli International AG

Hyundai Robotics

Nachi-Fujikoshi Corp.

DENSO Robotics

The Metal Casting Robots Market is evolving rapidly with the integration of advanced technologies that improve precision, safety, and process efficiency. One of the most notable innovations is the use of AI-driven robotic control systems, which enable real-time decision-making and adaptive process adjustments. These systems are capable of optimizing metal flow, monitoring temperature gradients, and minimizing casting defects such as porosity or shrinkage.

Smart sensors are now being embedded in robotic arms to track vibration, thermal levels, and alignment parameters during the casting process. This data is utilized by predictive maintenance algorithms to identify potential equipment failures before they disrupt operations, reducing downtime by over 25%. Additionally, robotics manufacturers are integrating 3D vision systems that facilitate automatic mold recognition and enable accurate positioning during core handling and pouring stages.

Collaborative robots (cobots) are emerging as a viable solution for mid-sized foundries due to their ease of integration, space efficiency, and ability to operate alongside human workers safely. Moreover, digital twin technology is being adopted to simulate casting operations, optimize cell layout, and shorten the commissioning time of robotic systems. Enhanced mobility, thermal insulation materials, and modular robot designs are further enabling their use in complex and high-temperature casting environments. These advancements are setting new performance benchmarks across high-demand industries.

• In March 2023, ABB launched its IRB 5710 series tailored for foundry applications, featuring expanded payload capacity and a reinforced arm structure, enabling enhanced precision for high-volume aluminum casting operations in automotive plants across Europe and Asia.

• In September 2023, KUKA introduced a next-generation robotic casting cell at a global expo, incorporating AI-based adaptive pouring control and thermal monitoring systems that reportedly improved casting quality consistency by 32% in pilot installations.

• In February 2024, FANUC upgraded its industrial robot software with a new AI algorithm that reduced trimming cycle time by 18% and increased detection accuracy of casting defects through enhanced image recognition capabilities.

• In May 2024, Hyundai Robotics collaborated with a South Korean automotive OEM to deploy a fully automated, sensor-integrated foundry line using metal casting robots capable of continuous operation under extreme heat, achieving a 27% improvement in production throughput.

The Metal Casting Robots Market Report offers an in-depth analysis of the global industry landscape, covering various technology types, application domains, and end-user sectors. It includes comprehensive segmentation by robot types such as 4-axis, 6-axis, SCARA, and collaborative robots, each suited for specific casting tasks including mold handling, pouring, trimming, and post-casting inspection. The report also examines applications across key industries such as automotive, aerospace, heavy machinery, and industrial manufacturing, with emphasis on evolving use cases in energy, defense, and renewable infrastructure.

Geographically, the report encompasses Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, outlining regional trends, adoption rates, and regulatory influences. It also highlights emerging markets and mid-tier manufacturers entering the automation landscape with modular and AI-enhanced robotic solutions. Technological insights include the adoption of machine learning, real-time thermal monitoring, predictive maintenance, IoT-enabled sensors, and digital twins for virtual simulation.

Furthermore, the report provides a strategic overview of competitive dynamics, investment trends, government initiatives, and workforce automation patterns. It serves as a critical resource for stakeholders looking to assess market readiness, innovation trends, and opportunities for strategic expansion within the metal casting robotics domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7296.67 Million |

|

Market Revenue in 2032 |

USD 18588.96 Million |

|

CAGR (2025 - 2032) |

12.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, ABB Ltd., Kawasaki Heavy Industries, Ltd., Comau S.p.A, Staubli International AG, Hyundai Robotics, Nachi-Fujikoshi Corp., DENSO Robotics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |