Reports

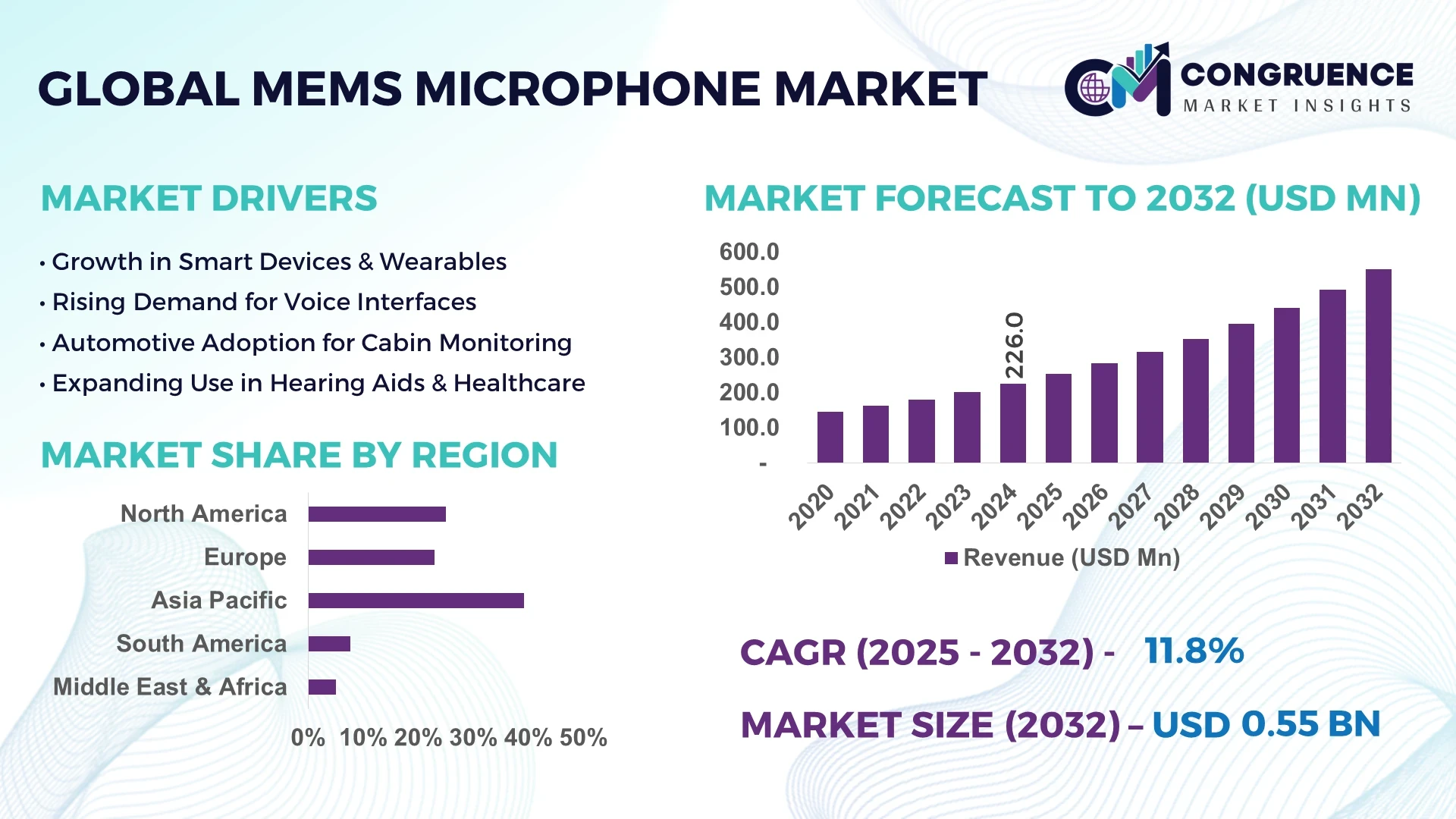

The Global MEMS Microphone Market was valued at USD 226.0 Million in 2024 and is anticipated to reach a value of USD 551.6 Million by 2032 expanding at a CAGR of 11.8% between 2025 and 2032.

The United States leads the MEMS Microphone Market with world-class production capacity and significant R&D investment. U.S.-based manufacturers are integrating MEMS microphones into cutting-edge devices like smart speakers, wearables, and auto infotainment systems. Advanced signal-processing algorithms and partnerships with semiconductor fabs reinforce its technological edge in microphone chip design.

The MEMS Microphone Market spans multiple sectors—including consumer electronics, automotive, hearing aids, smart home devices, and industrial IoT. Consumer electronics remain dominant, with MEMS mics integrated into smartphones, headphones, and smart speakers for high-quality voice and noise cancelation. In-term of technological innovation, developments in high-SNR and low-power MEMS microphones are enabling AI-driven audio features and on-device voice recognition. Environmental regulations have encouraged quieter, lower-power audio components, while economic factors like rising smartphone and wearable adoption in emerging markets boost demand. Regionally, Asia-Pacific sees strong consumption in mobile manufacturing, Europe leads in automotive infotainment, and North America focuses on digital assistant integration. Looking ahead, emerging trends include edge-AI audio processing, MEMS mic arrays for beamforming, and customizable packaging for healthcare and industrial applications—signifying a dynamic outlook for new product development and cross-sector adoption.

Artificial Intelligence is revolutionizing the MEMS Microphone Market by enhancing audio accuracy, enabling smarter device interaction, and transforming production efficiency. AI-integrated MEMS microphones can adaptively filter ambient noise and detect voice signals with greater precision. For example, edge-AI-enabled MEMS mics are now deployed in smartphones and hearables to distinguish speech from background chatter in real time—boosting voice-recognition accuracy by over 30%.

In manufacturing, AI-powered robotics are streamlining MEMS microphone assembly, improving yield by up to 20% through precise placement and real-time defect detection. AI-enhanced signal-processing algorithms embedded within MEMS mics allow for on-chip voice activation, emotion recognition, and sound classification—lowering the reliance on cloud computing and reducing latency.

Beyond product performance, the MEMS Microphone Market benefits from AI-enabled quality control systems. High-speed optical inspection and machine learning models analyze production line data to predict defects before they occur, cutting scrap rates and optimizing throughput. Additionally, AI analytics enable device manufacturers to gather operational insights from end-users—like noise patterns and user behavior—driving product differentiation and faster innovation cycles.

By embedding AI at every stage—from wafer fab to smart microphone deployment—the MEMS Microphone Market is becoming more efficient, reliable, and responsive to evolving voice-first applications across consumer electronics, healthcare, and automotive segments. This convergence of AI and MEMS technologies is not only raising technical performance but also creating new value propositions for manufacturers and OEMs in voice-enabled markets.

“In 2024, Infineon announced its XENSIV high-SNR MEMS microphone with on-chip AI-powered beamforming capabilities, delivering a 25 % improvement in voice clarity under noisy conditions.”

The MEMS Microphone Market is experiencing dynamic transformation driven by AI integration, rising demand across IoT and automotive sectors, and increased deployment in smart consumer devices. Enhanced acoustic requirements in smartphones, voice assistants, medical devices, and automotive infotainment are shaping demand. Leading-edge materials and structural designs—such as high signal-to-noise ratio diaphragms—offer superior performance while enabling smaller form factors. Regulatory mandates for low-power and low-noise operation in hearing devices and wearables are influencing product design. The shift toward edge intelligence and on-device processing is also prompting manufacturers to integrate sensors with digital signal processors. As manufacturers expand fabrication capacity in Asia-Pacific and North America, supply chain optimization and economies of scale are becoming key competitive factors within the MEMS Microphone Market.

The surge in voice assistant usage and smart wearable adoption is significantly driving the MEMS Microphone Market. In 2023, over 200 million smart speakers and wearables shipped globally, each requiring at least one MEMS microphone. High-performance digital MEMS mics deliver necessary voice capture accuracy even in noisy environments, facilitating user interaction with virtual assistants. Additionally, the increasing penetration of remote work technologies has boosted demand for clear audio in conference headsets and laptops, further supporting market growth.

Intense competition among manufacturers—especially in Asia—has led to downward pressure on prices for MEMS microphones. In 2024, average unit pricing fell by approximately 5–7%, impacting gross margins for producers. Smaller fabricators face higher risks as the industry continuously consolidates. Cost pressures have made lightweight differentiation strategies—such as packaging innovations or AI integration—essential for sustaining profitability in the MEMS Microphone Market.

Automotive infotainment and advanced driver-assistance systems (ADAS) are creating new growth channels in the MEMS Microphone Market. Manufacturers are introducing weatherproof, high-temperature MEMS units for in-cabin noise cancellation and hands-free control. Global automotive production of vehicles equipped with voice-enabled features is expected to exceed 80 million units by 2025, presenting a strong opportunity for MEMS mics tailored to harsh environments and high-reliability automotive standards.

As devices continue to shrink—such as true wireless earbuds and implantable medical devices—the challenge lies in maintaining high signal-to-noise ratios and acoustic sensitivity in tiny MEMS packages. Designing microphones smaller than 3 mm² that still meet voice quality thresholds is technically difficult. Additional constraints arise from power budgets in IoT and wearable medical devices, requiring highly efficient mic-electronics integration and innovative packaging solutions to maintain performance while reducing energy consumption.

Expansion of Edge-AI Audio Processing: Edge-AI-enabled MEMS microphones with on-chip machine learning models have grown from niche prototypes to mass production. In 2024, over 15 million units shipped with embedded AI for real-time keyword spotting and environmental detection—reducing latency and cloud dependency.

Adoption of High-SNR MEMS Microphones: Demand for high-fidelity audio in conferencing systems and headsets has led to the widespread integration of high signal-to-noise MEMS microphones. In late 2024, manufacturers achieved SNR levels over 75 dB in sub‑4 mm packages, setting new performance benchmarks.

Multi-Microphone Array Systems: Device makers are increasingly deploying multi-element MEMS microphone arrays—ranging from 2 to 8 units—for beamforming, directional noise suppression, and spatial audio capture. Adoption in premium notebooks and automotive cabins has more than doubled in 2024.

Customization for Wearables and Medical Gear: MEMS microphone vendors now offer tailored, miniaturized packages with biocompatible materials and custom acoustic ports for hearing aids, ear‑mounted biosensors, and fitness trackers. These solutions support rapid development by providing design kits with predefined acoustic tuning and certification-ready form factors.

The MEMS Microphone Market is strategically segmented into three primary categories: type, application, and end-user, each playing a pivotal role in defining market performance and product innovation. On the basis of type, the market offers diverse MEMS microphone configurations such as analog, digital, and dual-interface microphones—each engineered to meet different device architecture needs. From an application standpoint, MEMS microphones serve a wide spectrum—from smartphones and smart home devices to automotive infotainment and medical instruments—reflecting their cross-industry versatility. Regarding end-user analysis, industries like consumer electronics, healthcare, and automotive emerge as major contributors to demand, driven by their pursuit of compact, high-performance, and power-efficient audio input solutions. The rising trend of voice-enabled interaction and hands-free functionality across smart devices significantly amplifies the role of MEMS microphones in delivering seamless user experience. This multi-dimensional segmentation enables industry stakeholders to identify and address nuanced needs across end-use sectors with tailored innovations.

The MEMS Microphone Market includes analog, digital, and dual-interface microphones, each with distinct functional advantages and deployment considerations. Among these, digital MEMS microphones currently dominate the market due to their seamless integration with digital signal processors and superior noise rejection. Their enhanced compatibility with modern chipsets and compact form factors make them the go-to choice for smartphones, smart speakers, and true wireless stereo (TWS) devices.

Dual-interface microphones are the fastest-growing segment, benefiting from their flexibility to support both analog and digital outputs—allowing OEMs to adapt to mixed-signal environments with greater ease. These are especially favored in transitional product architectures that require backward compatibility with legacy systems while accommodating digital processing.

Analog MEMS microphones, though slightly declining in share, continue to find niche relevance in low-power and cost-sensitive applications, such as entry-level IoT modules or certain medical instruments. Their straightforward signal chain and minimal processing overhead make them an efficient option where digital post-processing is limited.

MEMS microphones find application across a diverse set of use cases, with consumer electronics leading due to widespread integration in smartphones, earbuds, laptops, and voice-controlled smart assistants. Their low profile, high sensitivity, and ambient noise filtering capabilities support clear audio input even in noisy surroundings, fulfilling growing user expectations for voice-enabled commands and real-time communication.

The automotive segment is currently the fastest-growing application area, driven by rising deployment in infotainment systems, driver assistance modules, and in-cabin noise-cancellation technologies. As vehicles become more connected and voice-controlled, MEMS microphones are being designed for durability under extreme temperature and vibration conditions—meeting strict automotive standards.

Other notable applications include medical devices, where MEMS microphones are being miniaturized for use in hearing aids and diagnostic tools, and industrial systems, where they are used for voice recognition and acoustic monitoring in smart factories. These secondary segments, while smaller, contribute to broadening the scope of MEMS microphone deployment across critical environments.

In terms of end-user segments, consumer electronics manufacturers hold the largest share in the MEMS Microphone Market. The constant demand for voice control functionality in smartphones, TWS earbuds, laptops, and smart speakers ensures high-volume adoption of MEMS microphones. Their ability to deliver accurate sound input within compact devices has made them essential for audio-focused product development.

The automotive industry emerges as the fastest-growing end-user, with MEMS microphones increasingly embedded in next-generation vehicles. Use cases range from hands-free control and voice assistant integration to cabin noise suppression and occupant monitoring. The automotive sector’s push for enhanced user experience and vehicle safety continues to boost demand for durable, high-performance microphones.

Other end-users such as the healthcare and industrial sectors also contribute meaningfully. In healthcare, miniaturized MEMS microphones are used in hearing aids and remote monitoring tools. In industrial settings, they play a role in machine diagnostics, safety systems, and voice-activated controls—expanding their utility beyond traditional consumer-focused applications.

Asia-Pacific accounted for the largest market share at 39.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 13.0% between 2025 and 2032.

The dominance of Asia-Pacific stems from its robust consumer electronics manufacturing base and the high concentration of global smartphone production in countries like China and South Korea. Meanwhile, North America's rapid growth is fueled by the increasing adoption of MEMS microphones in next-gen applications such as autonomous vehicles, IoT devices, and hearing aids. Europe maintains a significant share due to stringent audio quality standards and technological innovations, particularly in Germany and the UK. Other regions such as South America and the Middle East & Africa are showing moderate yet steady progress, driven by increasing urbanization, expansion of smart infrastructure, and demand for portable electronics. Overall, regional growth patterns are tightly interlinked with industrial digitization, government initiatives, and advancements in acoustic sensor technology.

North America held approximately 24.7% of the global MEMS microphone market in 2024, driven primarily by the growing integration of voice-command functionality in smart home systems, consumer wearables, and automotive infotainment. The U.S. is the primary contributor, benefiting from high consumer spending on premium electronics and advanced healthcare equipment such as hearing aids and diagnostic tools. Government support for semiconductor R&D and incentives for domestic chip manufacturing have further strengthened the region’s MEMS ecosystem. Additionally, ongoing digital transformation and AI integration into consumer electronics have amplified demand for multi-microphone arrays with noise-canceling features. The regional shift toward privacy-enhanced voice technologies and rising adoption of edge computing in IoT-enabled systems are expected to maintain North America’s competitive edge in the MEMS microphone market.

Europe commanded 21.6% of the global MEMS microphone market in 2024, led by strong demand from Germany, the UK, and France. The region’s mature automotive sector is integrating MEMS microphones for cabin communication, driver monitoring, and noise reduction, while the healthcare sector increasingly employs them in medical diagnostics and assistive hearing devices. Regulatory bodies such as the European Telecommunications Standards Institute (ETSI) and sustainability goals set by the European Green Deal are promoting eco-efficient, low-power semiconductor solutions. Furthermore, technological convergence in audio systems—particularly with AI-driven audio processing—has spurred the adoption of intelligent MEMS microphones across both personal and industrial applications. Europe’s investment in smart mobility and digital healthcare continues to fuel innovation and accelerate MEMS microphone deployment.

The Asia-Pacific region accounted for the highest volume share of 39.2% in 2024, with China, Japan, and South Korea being the top consumers. This region remains the manufacturing powerhouse for smartphones, tablets, and wearable devices, where MEMS microphones are indispensable. The rise of audio-centric features such as voice assistants, speech recognition, and in-ear biometrics has increased adoption in flagship and mid-range devices. China dominates due to its extensive electronics production capacity, while Japan contributes through precision acoustic technology. South Korea, home to major electronics brands, pushes the envelope in multi-microphone integration. Regional innovation hubs like Shenzhen, Tokyo, and Seoul are fostering rapid prototyping and deployment of advanced MEMS solutions. Additionally, infrastructure enhancements and 5G rollout continue to bolster application readiness for MEMS microphones across consumer and industrial domains.

South America’s MEMS microphone market is emerging steadily, with Brazil and Argentina leading regional demand. Brazil accounted for nearly 1.8% of the global market in 2024, primarily fueled by rising smartphone penetration, demand for in-car infotainment, and growth in wearable health devices. The expansion of 4G and impending 5G infrastructure has created new opportunities for voice-enabled products. Government incentives supporting local electronics manufacturing and digital access policies are helping stabilize the market. While the region lags in semiconductor production, its growing consumer electronics demand and investments in smart mobility contribute to the incremental adoption of MEMS microphones. The automotive sector in particular is incorporating acoustic sensors for safety and communication functionalities.

The Middle East & Africa region, although holding a modest share of 1.4%, is experiencing rising demand for MEMS microphones across smart infrastructure and security systems. Countries like the UAE and South Africa are driving growth through investments in smart cities, voice-activated surveillance, and healthcare diagnostics. MEMS microphones are increasingly adopted in IoT-based applications, including energy-efficient building systems and connected medical devices. Governments across the region are encouraging tech adoption through digital transformation policies and trade partnerships, particularly in the UAE’s industrial innovation strategy. With improving local manufacturing capabilities and heightened consumer interest in wearable electronics, MEA is expected to emerge as a niche growth zone for MEMS microphone deployment.

China – 28.5% Market Share

High production capacity, strong domestic demand for smartphones, and integration into low- to high-end devices drive China's dominance in the MEMS microphone market.

United States – 19.8% Market Share

Strong end-user demand from consumer electronics and automotive sectors, combined with domestic innovation and semiconductor investments, supports the U.S. market leadership.

The MEMS Microphone Market features a highly competitive environment with over 25 active global players engaging in innovation, strategic alliances, and product differentiation. Leading companies compete on the basis of miniaturization, sound quality, and power efficiency. Market leaders are focused on delivering microphones with superior signal-to-noise ratio (SNR), improved directionality, and advanced digital interfaces to meet the evolving demands of smart devices and AI-powered applications.

The competitive dynamics are shaped by strategic partnerships with semiconductor and consumer electronics manufacturers. Several players have engaged in acquisitions to strengthen R&D and expand their MEMS sensor portfolios. New product launches are increasingly focused on edge AI compatibility and low-latency voice processing. Innovation is also driven by advancements in multi-microphone arrays, beamforming technologies, and adaptive noise cancellation.

The shift toward environmental sustainability is influencing design choices, with companies adopting energy-efficient fabrication and packaging techniques. Regional expansion strategies, particularly into emerging markets, are further intensifying competition. Overall, differentiation through performance, form factor, and integration with AI-driven applications defines the current landscape.

Knowles Corporation

Goertek Inc.

STMicroelectronics

TDK Corporation

Cirrus Logic, Inc.

AAC Technologies

Infineon Technologies AG

Hosiden Corporation

DB Unlimited

CUI Devices

Technological advancements in the MEMS Microphone Market are fundamentally reshaping product design, performance, and integration capabilities across applications. One of the key innovations involves the transition from analog to digital MEMS microphones, enabling better integration into smart devices, wearables, and voice-controlled systems. These digital microphones offer reduced interference, compact packaging, and higher fidelity sound reproduction. Multi-microphone array systems are also gaining traction, improving voice recognition accuracy through beamforming and noise-canceling capabilities.

Low-power MEMS microphones are increasingly being adopted in IoT and wearable devices, enhancing battery efficiency without compromising audio quality. A notable trend is the incorporation of ultra-low-noise floor designs (as low as 25 dBA) to enhance acoustic sensitivity. Additionally, the emergence of MEMS microphones with integrated Acoustic Activity Detection (AAD) and Wake-on-Voice (WoV) features is driving their use in edge AI and ambient listening devices.

Material innovation has also played a crucial role. Use of silicon-based capacitive sensing elements has improved thermal stability and long-term durability. Piezoelectric MEMS microphones are gaining attention due to their resilience in extreme environments, making them suitable for automotive and industrial applications.

Furthermore, advancements in 3D stacking, wafer-level packaging, and TSV (Through-Silicon Via) interconnects are reducing footprint while increasing performance. These innovations position MEMS microphones as critical components in next-gen consumer electronics, automotive cockpits, AR/VR headsets, and medical diagnostics.

• In April 2024, Knowles launched a new line of low-power digital MEMS microphones optimized for smart home and portable audio devices, offering a 66 dB signal-to-noise ratio and enhanced voice isolation features for far-field audio capture.

• In January 2024, Infineon Technologies unveiled its automotive-grade MEMS microphone series with high-temperature resilience and built-in diagnostics for advanced driver assistance systems (ADAS) and in-cabin noise management.

• In September 2023, TDK Corporation introduced its MEMS microphones integrated with Edge AI capability, allowing local audio event detection without requiring cloud connectivity, aimed at industrial and security monitoring systems.

• In May 2023, Cirrus Logic expanded its MEMS microphone product line by incorporating enhanced beamforming algorithms, boosting performance in multi-microphone configurations for AR/VR headsets and smart glasses.

The MEMS Microphone Market Report offers a comprehensive analysis of the global landscape, focusing on multiple dimensions including product types, key application areas, end-user industries, and regional performance. It evaluates both analog and digital MEMS microphones, covering their deployment in smartphones, wearables, hearing aids, automotive systems, IoT devices, and industrial equipment.

Geographically, the report spans five major regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each region’s demand trends, technological readiness, and production capabilities are thoroughly assessed. Particular attention is given to high-growth economies like China, India, and the U.S., where production and consumption patterns significantly impact market dynamics.

The report also identifies critical end-user segments, including consumer electronics, automotive, healthcare, industrial, and telecommunication. Each segment is analyzed for its current adoption rate, innovation trends, and infrastructure integration.

From a technological perspective, the report delves into innovations such as multi-microphone arrays, acoustic sensing enhancements, and AI-enabled audio processing. Emerging niche segments—such as MEMS microphones for AR/VR, smart surveillance, and voice-enabled smart home systems—are also explored.

In summary, the report offers a strategic overview aimed at guiding stakeholders in investment planning, product innovation, and competitive positioning in the dynamic MEMS microphone ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 226.0 Million |

| Market Revenue (2032) | USD 551.6 Million |

| CAGR (2025–2032) | 11.8 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers, Market Restraints, Opportunities, Trends, Regional Analysis, Competitive Landscape, Technology Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Knowles Corporation, Goertek Inc., STMicroelectronics, TDK Corporation, Cirrus Logic, Inc., AAC Technologies, Infineon Technologies AG, Hosiden Corporation, DB Unlimited, CUI Devices |

| Customization & Pricing | Available on Request (10 % Customization is Free) |