Reports

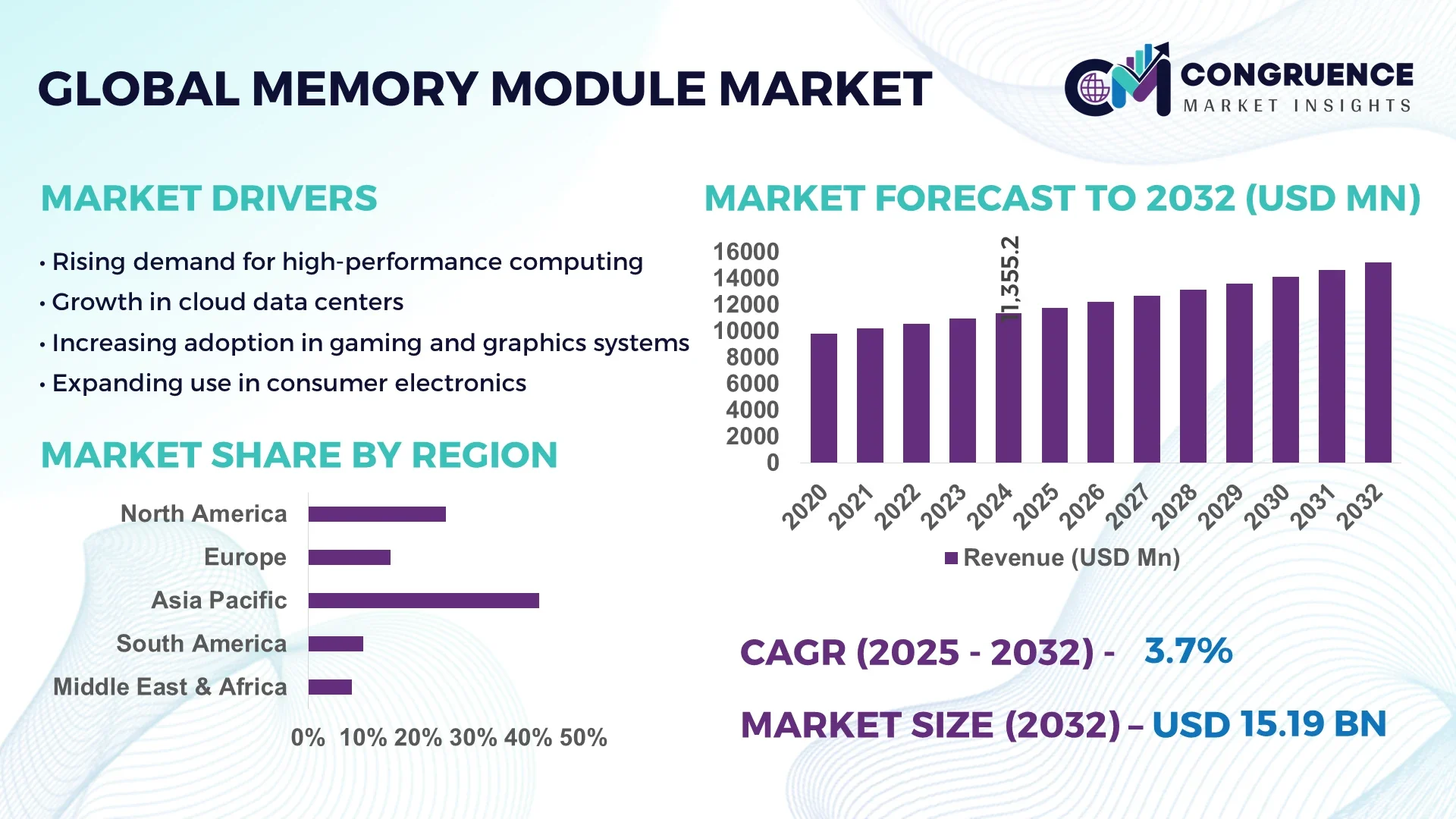

The Global Memory Module Market was valued at USD 11355.15 Million in 2024 and is anticipated to reach a value of USD 15185.28 Million by 2032 expanding at a CAGR of 3.7% between 2025 and 2032. The growth is driven by increasing demand for high-performance computing, cloud data centers, and AI-driven applications requiring faster memory solutions.

In South Korea, the Memory Module market benefits from world-class semiconductor manufacturing infrastructure, backed by over USD 45 billion in annual investments across fabrication facilities and R&D. The country’s advanced capabilities in DRAM and NAND technologies support production at scales exceeding 600 million memory units annually. Integration into key industries such as automotive electronics, 5G, and enterprise servers is accelerating, with AI-enabled memory modules improving energy efficiency by 18% in high-density data applications.

Market Size & Growth: Valued at USD 11355.15 Million in 2024, projected to reach USD 15185.28 Million by 2032, with a CAGR of 3.7% driven by demand for advanced computing and AI integration.

Top Growth Drivers: 65% adoption in data centers, 42% efficiency improvement in DDR5 systems, and 38% enterprise demand from cloud expansion.

Short-Term Forecast: By 2028, DDR5 modules are expected to achieve 25% lower latency and 30% improved performance compared to DDR4.

Emerging Technologies: DDR5 and LPDDR5X modules, AI-optimized memory, and 3D-stacked memory solutions.

Regional Leaders: Asia-Pacific projected at USD 7000 Million by 2032 with strong manufacturing, North America at USD 4500 Million driven by data centers, Europe at USD 2500 Million with high adoption in automotive systems.

Consumer/End-User Trends: Strong adoption in enterprise cloud computing, rising gaming PC demand, and integration into smart automotive systems.

Pilot or Case Example: In 2024, a major U.S. data center pilot achieved 22% energy savings using LPDDR5X modules in server upgrades.

Competitive Landscape: Samsung Electronics leads with 29% share, followed by SK Hynix, Micron Technology, Kingston Technology, and Corsair.

Regulatory & ESG Impact: Governments pushing green semiconductor policies with targets of 20% carbon reduction in memory fabs by 2030.

Investment & Funding Patterns: Over USD 18 billion invested globally in advanced semiconductor fabs during 2023–2024, focusing on memory module innovation.

Innovation & Future Outlook: Growth in AI-accelerated memory, quantum computing readiness, and edge computing integration shaping future demand.

The Memory Module market is being transformed by strong adoption in sectors such as data centers, gaming, and enterprise IT infrastructure. Automotive memory demand is rising rapidly, with connected vehicles and ADAS systems projected to account for 18% of usage by 2030. Technological advances like DDR5 and high-bandwidth memory are fueling breakthroughs in server performance and AI workloads. Environmental regulations are driving investment into low-power memory modules, while regional consumption trends show Asia-Pacific leading in manufacturing, North America in AI and enterprise adoption, and Europe in automotive integration. The future outlook emphasizes sustainable production, innovation in 3D-stacked architectures, and stronger penetration in next-generation computing environments.

The Memory Module Market holds strategic significance as it underpins advancements in computing, data storage, and AI-driven applications across industries. With the rise of digital transformation, cloud computing, and high-performance gaming, demand for advanced modules continues to expand. DDR5 technology delivers up to 30% improvement in speed and bandwidth compared to DDR4, enabling servers and data centers to achieve higher efficiency. Asia-Pacific dominates in production volume, while North America leads in enterprise adoption with 62% of data centers integrating advanced memory modules in 2024.

By 2027, AI-optimized memory architectures are expected to cut latency in server applications by 28%, enhancing throughput in mission-critical systems. Firms are committing to ESG improvements such as achieving 25% energy reduction in fabrication plants and expanding recycling of electronic components by 2030. In 2024, a major U.S. cloud service provider implemented LPDDR5X modules in its server clusters, achieving a 20% reduction in energy consumption while increasing performance output by 18%.

The strategic pathways of the market involve expanding integration in autonomous vehicles, AI workloads, and next-generation 5G networks. With innovation in 3D-stacked memory and hybrid modules, the Memory Module Market is positioned as a pillar of resilience, compliance, and sustainable growth for global industries.

The Memory Module Market is shaped by strong technological innovation, rising demand from enterprise IT, and rapid expansion in consumer electronics. Growing adoption of AI, IoT, and cloud services is pushing requirements for higher-speed and low-latency memory systems. DDR5 and LPDDR5X modules are reshaping industry standards, while AI-driven workloads demand greater energy efficiency. Regional growth is driven by Asia-Pacific’s manufacturing dominance, North America’s heavy reliance on advanced data centers, and Europe’s integration into automotive and industrial applications. Challenges such as fluctuating raw material prices, supply chain disruptions, and environmental regulations continue to influence the dynamics, yet long-term opportunities remain strong due to the integration of memory modules into emerging industries such as autonomous systems, 6G networks, and green data centers.

The surge in global data traffic has led to massive demand from hyperscale data centers, driving the Memory Module Market forward. With over 8,000 data centers operating worldwide in 2024, operators are upgrading to DDR5 and high-bandwidth modules to achieve higher efficiency and scalability. Cloud providers reported a 40% increase in demand for memory modules optimized for AI and machine learning workloads. The push toward virtualization, big data analytics, and 5G networks has increased reliance on low-latency and high-performance memory, ensuring stable growth. As enterprises adopt edge computing, demand for compact yet powerful modules is rising, further consolidating the role of data centers as a critical driver.

Supply chain constraints remain one of the biggest restraints in the Memory Module Market. The semiconductor shortage that began in 2020 still impacts production capacity, with lead times for advanced modules stretching beyond 26 weeks in 2023–2024. Rising costs of raw materials such as silicon wafers and rare earth elements have added an average of 12% to overall production costs. Additionally, geopolitical trade tensions, particularly involving Asia-Pacific manufacturing hubs, disrupt continuity in supply. Smaller manufacturers are especially vulnerable, facing difficulties in securing components at competitive pricing. These bottlenecks delay large-scale adoption in industries such as automotive electronics and consumer devices, where consistent supply is essential.

The expansion of AI-driven applications and autonomous technologies offers significant opportunities for the Memory Module Market. Autonomous vehicles, which require real-time data processing exceeding 4 TB per day, rely heavily on high-speed, low-power memory systems. Similarly, AI accelerators demand advanced memory architectures that can handle massive datasets with minimal latency. Projections indicate that by 2026, nearly 35% of automotive electronic systems will integrate advanced DDR5 or LPDDR memory modules. In addition, industrial automation and smart manufacturing are expanding demand for ruggedized and high-performance memory solutions. This untapped segment provides scope for innovation, particularly in energy-efficient modules designed for AI workloads.

Although DDR5 and LPDDR5X offer superior performance, they also present challenges related to power consumption and heat dissipation. High-performance modules can consume up to 20% more energy compared to older generations under peak workloads, posing difficulties for data centers already struggling with sustainability targets. The growing emphasis on ESG compliance puts additional pressure on manufacturers to design low-power modules without sacrificing performance. Thermal management also becomes a critical issue, with cooling systems contributing to nearly 30% of operational costs in high-density server environments. Balancing performance with sustainability remains a major challenge for stakeholders in the Memory Module Market.

• Growing Adoption of DDR5 Modules: DDR5 memory adoption is accelerating across enterprise and consumer markets, with DDR5 accounting for 48% of all memory module shipments in 2024. These modules deliver up to 30% higher bandwidth compared to DDR4, driving performance improvements in AI workloads and high-performance computing systems. Asia-Pacific and North America lead adoption, with enterprise-level upgrades accounting for over 60% of installations. This trend is expected to significantly influence system design standards across industries.

• Expansion of AI-Optimized Memory Solutions: AI workloads are driving demand for specialized memory modules. In 2024, over 35% of server-based AI applications integrated LPDDR5X or DDR5 memory optimized for low latency. This trend is particularly strong in North America, where enterprise adoption of AI-driven analytics rose by 28% in 2024, requiring high-speed memory for real-time processing. This shift encourages manufacturers to develop memory with AI-specific architectures.

• Surge in Edge Computing Deployments: Edge computing growth is reshaping memory requirements, with demand for compact, high-speed modules increasing by 42% in 2024. Regions such as Europe are integrating advanced memory into edge devices for manufacturing and automotive systems, improving latency by up to 25%. This trend supports distributed data processing and decentralization strategies in various industries.

• Focus on Energy-Efficient Memory Solutions: Sustainability trends are driving interest in low-power memory technologies. In 2024, 38% of memory module production incorporated energy-saving designs, with modules achieving up to 20% less power consumption compared to previous generations. This shift is significant for data centers, where energy costs comprise nearly 30% of operational expenses, and is fostering investment in sustainable memory production practices.

The Memory Module Market is segmented by type, application, and end-user, reflecting diverse demand drivers and growth opportunities. By type, DDR4 and DDR5 dominate, while emerging LPDDR5X and HBM solutions are gaining traction. Applications range from enterprise servers and data centers to consumer electronics and automotive systems, with enterprise and cloud computing leading adoption. End-users include IT service providers, gaming industries, automotive manufacturers, and cloud infrastructure firms, with enterprise applications accounting for over 50% of demand. Growing trends such as AI adoption, edge computing, and sustainability measures are influencing segmentation patterns and driving innovation in memory module technology.

DDR5 modules currently account for 48% of adoption, driven by their higher bandwidth and lower latency, making them the leading segment in the Memory Module Market. DDR4 still holds a 30% share due to cost efficiency and established compatibility. LPDDR5X modules are the fastest-growing type, with a 27% increase in adoption in 2024, driven by mobile devices and AI applications. HBM solutions, while niche, contribute 12% of the market, particularly in high-performance computing and GPU applications. Together, these other types hold about 10% of the market.

Enterprise servers and cloud infrastructure are the leading applications, representing 52% of the Memory Module Market due to surging demand for virtualization and AI computing. Consumer electronics account for 25%, driven by high-performance PCs and gaming systems. Automotive applications, at 13%, are expanding rapidly, integrating memory modules into autonomous driving and infotainment systems. Edge computing contributes the remaining 10%, with demand rising due to low-latency requirements. The fastest-growing application is AI data processing, which increased 29% in module demand in 2024, supported by advances in LPDDR5X.

IT service providers dominate the Memory Module Market, accounting for 45% of adoption due to growth in cloud computing and data analytics. The consumer electronics sector holds 28%, driven by gaming PCs, laptops, and mobile devices. The automotive industry, contributing 15%, is rapidly adopting high-performance memory for advanced driver-assistance systems and infotainment. Industrial automation accounts for 7%, while edge computing devices represent 5% of end-user demand. The fastest-growing end-user segment is autonomous vehicle manufacturing, where memory demand rose 31% in 2024, driven by real-time data processing needs.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Asia-Pacific’s dominance is driven by strong manufacturing bases in China, Japan, and South Korea, contributing over 60% of global memory module production capacity. In 2024, China alone produced more than 1.8 billion memory modules, with technological upgrades driving performance improvements by up to 28%. North America’s rapid adoption is supported by AI and cloud computing expansions, with enterprise data center upgrades increasing by 33% in 2024. Europe contributed about 21% of global memory module consumption, with Germany and the UK leading in integration for enterprise and automotive sectors. South America and the Middle East & Africa together accounted for 12%, supported by targeted infrastructure investments and digital transformation initiatives.

How is advanced enterprise computing shaping memory module demand?

North America holds a 28% share of the Memory Module Market, driven by demand in cloud computing, AI, and enterprise IT infrastructure. Key industries include healthcare, finance, and aerospace, adopting high-speed DDR5 and LPDDR5X modules to support data-intensive applications. Regulatory frameworks such as the CHIPS and Science Act encourage domestic production, leading to a 19% increase in local manufacturing investments in 2024. Digital transformation is driving demand for modular memory solutions with higher bandwidth, supporting enterprise data analytics and AI-driven workloads. Micron Technology, a leading U.S.-based player, introduced DDR5 solutions optimized for AI in 2024, reducing latency by 18%. North American consumers demonstrate a preference for high-performance memory, with enterprise adoption in AI-driven healthcare and finance increasing by over 25% in 2024.

How is regulatory pressure influencing memory module adoption?

Europe holds a 21% market share, with Germany, the UK, and France leading demand. Regulatory frameworks such as the EU Green Deal encourage energy-efficient memory designs, boosting adoption of LPDDR5X and low-power DDR5 modules by 31% in 2024. Emerging technologies like AI-optimized memory are increasingly integrated into industrial automation, automotive, and data center applications. Sustainability initiatives are influencing production, with 35% of memory modules now manufactured under energy-efficient processes. A leading German memory manufacturer launched a DDR5 series in 2024 optimized for automotive AI applications, reducing energy use by 22%. European buyers prioritize explainable and sustainable memory solutions, particularly in enterprise, government, and automotive sectors, aligning with regional ESG requirements.

What factors drive Asia-Pacific’s dominance in memory modules?

Asia-Pacific is the largest market, contributing 42% of global consumption. China, Japan, and South Korea are the top consuming countries, with China accounting for 28% of total regional demand. The region leads in manufacturing, producing over 1.8 billion modules in 2024. Infrastructure trends include expanding smart manufacturing hubs and automotive electronics, while innovation clusters focus on DDR5 and HBM technologies. Samsung and SK Hynix have expanded production capacities with advanced fabrication lines in South Korea and China. In 2024, Asia-Pacific memory module shipments grew by 21%, driven by strong demand from mobile AI applications and cloud infrastructure. Regional behavior reflects high adoption rates in electronics manufacturing and technology-driven industrial sectors.

How is digital transformation shaping memory module growth in South America?

South America accounted for 6% of the global Memory Module Market in 2024, with Brazil and Argentina leading demand. Infrastructure growth in telecommunications and renewable energy is driving memory integration. Government incentives for technology upgrades have stimulated enterprise investments in cloud-based and edge computing solutions. Memory module adoption rose by 17% in 2024, with significant contributions from automotive and manufacturing industries. Local player TecMemory launched DDR5-based solutions for enterprise applications, improving data access speeds by 15%. Regional consumer behavior reflects high interest in language localization technologies, gaming systems, and digital transformation in public and private sectors.

How are infrastructure upgrades shaping memory module demand in the Middle East & Africa?

The Middle East & Africa contributed about 6% of the global Memory Module Market in 2024. Key growth countries include the UAE and South Africa, with investments in smart city projects and renewable energy infrastructure driving demand. Technological modernization, particularly in oil & gas and construction, has prompted memory module adoption in edge computing and industrial automation. Government incentives for digital infrastructure upgrades increased local demand by 14% in 2024. A UAE-based player deployed DDR5 solutions for smart energy grids, improving processing efficiency by 20%. Consumer trends reflect adoption in high-performance computing, industrial automation, and urban infrastructure projects.

China: 28% — Strong production capacity and extensive manufacturing infrastructure for DDR5 and LPDDR5X modules.

United States: 22% — Robust demand from enterprise IT, cloud computing, and AI-driven workloads supported by regulatory incentives and innovation.

The Memory Module market is moderately consolidated, with the top five companies accounting for approximately 58% of global market share. The competitive environment includes more than 150 active players globally, with key participants focusing on high-performance DDR5, LPDDR5X, and HBM memory technologies. Strategic initiatives include product launches, R&D investments, strategic alliances, and mergers to strengthen portfolios and enhance manufacturing capacities. In 2024, Samsung Electronics expanded its production line by 20% to meet demand for AI-optimized memory modules, while Micron Technology launched advanced DDR5 modules with a 15% improvement in bandwidth performance. SK Hynix invested USD 1.2 billion in a new fabrication facility in South Korea, enhancing its memory output capacity. Kingston Technology partnered with leading cloud computing firms to integrate specialized memory solutions for enterprise servers. G.Skill introduced high-density DDR5 modules targeting gaming and professional workstations, increasing adoption by 17% in 2024. Competitive innovation focuses heavily on energy efficiency, low-latency architectures, and scalable memory systems, with global competition intensifying as demand for high-speed memory in AI, cloud computing, and data centers grows.

Kingston Technology

Corsair Components

G.Skill International

Patriot Memory

ADATA Technology

Transcend Information

Team Group Inc.

The Memory Module market is being transformed by advancements in DDR5, LPDDR5X, and High Bandwidth Memory (HBM) technologies, enabling significantly higher speeds, lower latency, and improved energy efficiency. DDR5 modules now achieve speeds of up to 8400 MT/s, compared to DDR4’s 3200 MT/s, delivering more than 160% improvement in data transfer rates. LPDDR5X technology, adopted widely in mobile and edge computing, offers up to 50% better power efficiency and a bandwidth increase of 30% over its predecessor. HBM advancements are driving high-performance computing, with stack densities reaching 24 GB per stack, enhancing performance for AI and data center applications. Emerging technologies like 3D stacking, Chip-on-Wafer-on-Substrate (CoWoS) integration, and advanced error-correcting codes (ECC) are improving reliability, scalability, and integration density. AI-driven memory optimization tools are also being deployed, enabling dynamic allocation of memory resources to improve workload efficiency by up to 20%. The integration of photonic interconnects for memory modules is under development, aiming to reduce latency by up to 40% for large-scale computing systems. These innovations position the memory module market as a critical enabler for next-generation AI, cloud, and IoT ecosystems.

• In March 2023, Micron Technology launched its DDR5 DRAM modules with advanced AI memory management, improving performance by 18% for enterprise computing workloads. Source: www.micron.com

• In July 2023, Samsung Electronics unveiled a new line of LPDDR5X modules for mobile devices, offering up to 50% lower power consumption and enabling enhanced battery life for smartphones and tablets. Source: www.samsung.com

• In January 2024, SK Hynix announced the completion of a USD 1.2 billion upgrade to its memory fabrication plant in Icheon, South Korea, increasing production capacity by 22% for high-performance modules. Source: www.skhynix.com

• In September 2024, Kingston Technology introduced a new series of high-density DDR5 modules with over 30% improvement in read/write speeds, specifically optimized for gaming and workstation applications. Source: www.kingston.com

The Memory Module Market Report provides a comprehensive analysis of the global memory module ecosystem, covering a broad spectrum of product types, applications, and end-user industries. It examines DDR, DDR2, DDR3, DDR4, DDR5, LPDDR, and HBM modules, emphasizing their role in enhancing system performance across computing platforms. The report addresses key applications such as personal computing, servers, data centers, mobile devices, embedded systems, and gaming, with measurable insights into adoption patterns and performance requirements. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, each with detailed analyses of regional demand drivers, infrastructure trends, manufacturing capabilities, and innovation hubs. It assesses technological innovations including high-bandwidth memory architectures, 3D stacking, low-power designs, and photonic interconnect integration. The report also explores emerging segments such as AI-driven memory optimization and application-specific modules, along with industry-specific adoption trends. Regulatory frameworks, environmental policies, and sustainability initiatives impacting the memory module market are addressed, along with a forward-looking view on growth pathways and future technological advancements, providing strategic insights for stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 11355.15 Million |

|

Market Revenue in 2032 |

USD 15185.28 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Electronics, Micron Technology, SK Hynix, Kingston Technology, Corsair Components, G.Skill International, Patriot Memory, ADATA Technology, Transcend Information, Team Group Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |