Reports

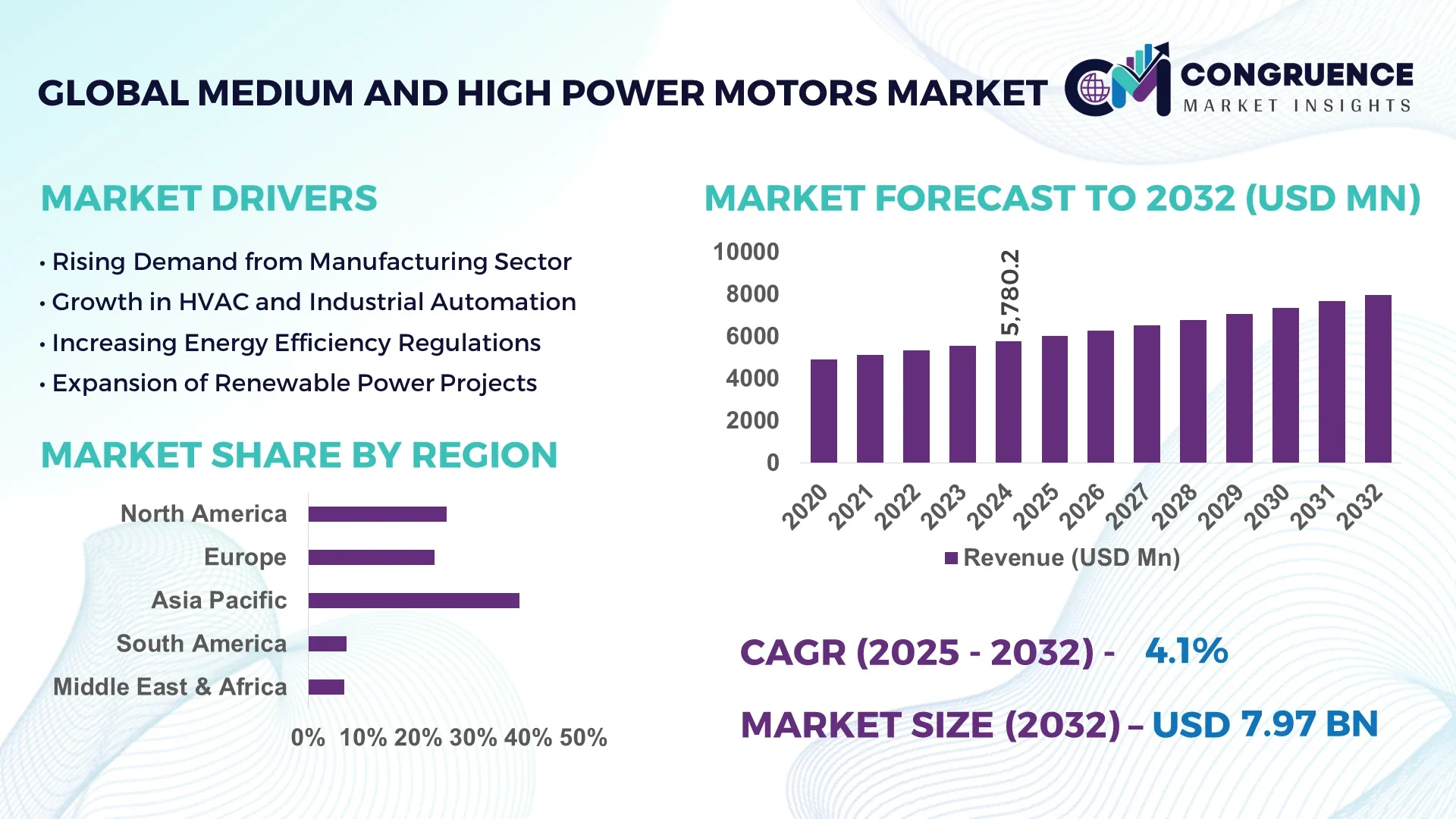

The Global Medium and High Power Motors Market was valued at USD 5,780.2 Million in 2024 and is anticipated to reach a value of USD 7,971.7 Million by 2032, expanding at a CAGR of 4.1% between 2025 and 2032.

China leads the global medium and high power motors market, driven by its extensive manufacturing and energy sectors. The country's focus on industrial automation and infrastructure development has significantly increased the demand for these motors, particularly in applications such as pumps, fans, and compressors. Additionally, China's investments in renewable energy projects have further propelled the market growth.

The Medium and High Power Motors Market is increasingly driven by the demand for energy-efficient solutions across various industries. These motors are crucial in applications where high torque and power are required, such as in large machinery, industrial automation, and electric vehicles. The adoption of these motors is particularly growing in sectors like manufacturing, oil & gas, automotive, and power generation. In 2024, the industrial segment accounted for the largest market share, with significant contributions from automation and robotics. Additionally, the rise in electric vehicle production is accelerating the demand for high-power motors, with key automotive manufacturers integrating these solutions into their EV models to enhance performance and efficiency. Advanced materials, such as high-strength magnets and optimized cooling technologies, are being used to improve the efficiency and durability of these motors.

Artificial Intelligence (AI) is revolutionizing the medium and high power motors market by enhancing efficiency, predictive maintenance, and design optimization. AI-driven predictive maintenance utilizes supervised learning models to monitor motor health, categorizing them as "Healthy," "Needs Preventive Maintenance," or "Broken." This approach minimizes unplanned downtimes and extends motor lifespan. Additionally, AI-based diagnostic systems, such as those employing ShuffleNetV2 models, have achieved classification accuracies of up to 98.856% in detecting faults like Broken Rotor Bar (BRB) in induction motors.

In design optimization, AI frameworks leverage data-driven approaches to generate preliminary designs for electrical machines. For instance, using a Metamodel of Optimal Prognosis (MOP)-based surrogate model, AI can produce thousands of scalable motor designs, significantly reducing the time required compared to traditional methods. These designs achieve higher power densities, exemplified by a 30kVA wound-rotor synchronous generator design attaining 2.21 kVA/kg in just 5 seconds.

Moreover, machine learning techniques are employed to estimate internal temperatures of induction motors, ensuring they operate within safe thresholds. Neural networks have demonstrated satisfactory performance in approximating stator winding and bearing temperatures, even under transient conditions. This capability is crucial for preventing failures and securing reliable operation in electrified powertrains.

Overall, AI integration in the medium and high power motors market leads to improved operational efficiency, reduced maintenance costs, and accelerated innovation in motor design and functionality.

"In 2024, ABB launched the MV Titanium, the world’s first medium-voltage speed-controlled motor in the 1–5 MW range, offering up to 40% energy savings in pumps, compressors, and fans, with integrated AI-driven control and diagnostics to reduce emissions and streamline industrial motor efficiency."

With the expansion of industrial automation globally, the demand for medium and high power motors is accelerating across sectors like automotive, oil and gas, mining, and utilities. Manufacturing plants are increasingly automating conveyor systems, pumps, compressors, and HVAC equipment, all of which require medium or high power motors for consistent and efficient operation. For instance, over 60% of equipment in heavy industries now relies on electric motors exceeding 1 MW. In addition, power plants and renewable energy projects are adopting medium voltage motors to handle fluctuating loads and maintain efficiency. The need to minimize energy losses and meet regulatory standards is further propelling the deployment of intelligent motor systems that enhance operational precision. These motors are critical to reducing downtime and maximizing output in high-demand environments.

Despite their advantages, medium and high power motors often involve significant capital investments, posing a restraint for small and mid-sized enterprises. The cost of acquiring a medium voltage motor ranges from thousands to hundreds of thousands of dollars depending on power rating, control systems, and industry application. Additionally, installation requires specialized infrastructure such as step-down transformers, ventilation systems, and vibration dampening, adding to overall costs. Maintenance complexity is another barrier, as large motors require skilled technicians for diagnostics and repairs, and unplanned downtime can incur substantial losses. These factors delay adoption in developing regions and limit retrofitting possibilities in older facilities. Companies often hesitate to invest unless assured of high load requirements and long-term operational continuity.

The shift toward sustainability and energy conservation has opened significant opportunities for the medium and high power motors market. Governments across North America, Europe, and Asia-Pacific have introduced stringent energy efficiency regulations such as IE3 and IE4 standards, encouraging industries to replace outdated motors. In India and China, large-scale electrification initiatives have further prompted the deployment of smart motors equipped with variable frequency drives (VFDs). These motors offer enhanced energy control and reduced CO₂ emissions, aligning with corporate ESG goals. Additionally, incentive programs, tax benefits, and grants for installing energy-efficient equipment make upgrading older motor systems financially viable. By transitioning to motors that deliver superior performance with reduced energy input, industries can achieve long-term cost savings while complying with global environmental norms.

The increasing sophistication of medium and high power motors poses a major challenge in terms of workforce preparedness. These motors often integrate AI, IoT, and condition monitoring systems that require highly trained personnel for operation and maintenance. However, a shortage of experienced motor technicians and engineers, particularly in emerging markets, hampers smooth adoption. According to recent industry data, over 45% of companies report delays in installation or diagnostics due to limited technical expertise. The lack of standardized training programs and certification pathways further widens the skills gap. Moreover, integrating smart motors with existing industrial control systems demands advanced knowledge in automation and electrical engineering. Without addressing the talent shortage, industries may experience increased downtimes, inefficiencies, and slow return on investment.

• Integration of Smart Sensors and IoT in Motor Systems: One of the most prominent trends in the medium and high power motors market is the integration of smart sensors and IoT-enabled technologies. These sensors provide real-time data on motor temperature, vibration, load, and energy usage, allowing predictive maintenance and improving operational efficiency. Industrial plants using IoT-integrated motors have reported up to 30% reduction in downtime and a 15% increase in energy efficiency. This trend is especially strong in regions with mature industrial automation infrastructures such as North America and Germany.

• Expansion of Renewable Energy Infrastructure: Medium and high power motors are increasingly being used in renewable energy applications, particularly in wind and hydropower sectors. These motors play a vital role in turbine operations, generators, and grid stabilization units. In 2024, over 25% of new motor installations above 1 MW were directed toward renewable energy projects. The focus on sustainable power generation and governmental mandates to shift away from fossil fuels is pushing the demand for durable and energy-efficient motor systems.

• Surge in Demand for Electric Vehicles (EV) Charging Infrastructure: With the growing adoption of electric vehicles globally, there is a parallel increase in the need for heavy-duty motors used in EV charging stations and power distribution systems. Medium power motors are critical for driving pumps and compressors in fast-charging stations and grid-level voltage regulators. Countries like China and the U.S. are investing billions in upgrading electrical infrastructure, thereby driving demand for medium voltage motor systems that offer high efficiency and stable performance.

• Rise in Heavy Industrial Automation in Emerging Markets: Emerging economies such as India, Brazil, and Southeast Asian countries are rapidly industrializing, leading to a higher demand for medium and high power motors. The manufacturing sector in these countries is witnessing massive growth, with more than 40% of new plant installations incorporating automated motor-driven systems. This shift is driven by low labor availability and the need for higher throughput and precision, making high-capacity motors an essential component in modern factories and processing units.

The medium and high power motors market is segmented based on type, application, and end-user, each contributing distinctly to overall market expansion. By type, the market spans AC motors, DC motors, and synchronous and asynchronous motors. By application, segments include industrial machinery, HVAC systems, water and wastewater treatment, power generation, and transportation. In terms of end-users, the primary segments are manufacturing, utilities, oil and gas, mining, and transportation. Each segment showcases unique growth trends driven by technological innovation, operational demands, and infrastructure development. The increased emphasis on energy efficiency and smart automation is pushing demand across all segments.

The medium and high power motors market by type is categorized into AC motors, DC motors, synchronous motors, and asynchronous motors. Among these, AC motors lead the market share, owing to their superior efficiency, low maintenance, and adaptability across industries. AC motors are commonly used in HVAC systems, industrial drives, and pumps. Synchronous motors, particularly high-voltage ones, are the fastest-growing segment due to their precise speed control and high torque capabilities in applications such as compressors, crushers, and conveyors. They are increasingly being deployed in energy-intensive sectors like oil & gas and mining, where efficiency and reliability are paramount. Meanwhile, DC motors, though widely used in smaller automation systems, are limited in high power applications due to commutation issues and higher maintenance needs. Asynchronous motors also maintain steady demand, especially in low-cost industrial environments where simple and rugged motors are preferred.

The application-based segmentation includes industrial machinery, HVAC systems, water and wastewater treatment, power generation, and transportation. Industrial machinery dominates this category, with over 35% share of medium and high power motors used in equipment like crushers, mixers, and presses. These motors ensure stable torque, energy savings, and higher throughput in manufacturing operations. Power generation is emerging as the fastest-growing segment, especially in renewable energy plants where large synchronous motors are used to drive turbines and generators. Water and wastewater treatment facilities also rely on medium voltage motors to operate large pumps and aerators. The HVAC segment continues to maintain moderate demand as commercial buildings and data centers increasingly adopt high-efficiency cooling systems. The transportation sector, especially rail and EV infrastructure, is creating niche but growing demand for medium voltage motors in traction and auxiliary systems.

By end-user, the market is segmented into manufacturing, utilities, oil and gas, mining, and transportation. Manufacturing holds the largest share, with extensive use of medium and high power motors in production lines, automated assembly, and heavy machinery operations. This segment accounts for nearly 40% of global installations. The utilities sector, particularly electric power and water treatment facilities, is the fastest-growing end-user segment due to the increasing need for smart and energy-efficient grid infrastructure. The oil and gas sector continues to demand explosion-proof, high-torque motors for downstream and upstream operations. Mining companies rely on rugged, high-horsepower motors for equipment like mills and excavators, especially in South America and Africa. Meanwhile, the transportation segment is seeing growth through infrastructure upgrades and railway electrification projects, creating a stable demand base for high-reliability motors used in power transmission and auxiliary services.

Asia-Pacific accounted for the largest market share at 38.4% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to large-scale industrialization, robust manufacturing activities, and the rise in renewable energy projects, particularly in China, India, and Japan. Rapid urbanization and government-led electrification programs have driven substantial installations of medium and high power motors across infrastructure and utilities sectors. Meanwhile, South America is witnessing accelerating demand for energy-efficient motor systems due to modernization in the mining and oil sectors, especially in Brazil and Chile. The increasing adoption of automation in these industries, coupled with government incentives for upgrading legacy motor systems, is fueling regional market expansion. Additionally, countries like Argentina are investing heavily in hydro and wind power, which require large-scale motor deployments. These dynamics are making South America the next growth hotspot for the medium and high power motors industry.

North America continues to show significant demand for medium and high power motors, driven by increased investments in industrial automation and sustainability initiatives. The U.S. leads the region with strong installations across sectors like manufacturing, utilities, and commercial HVAC systems. Over 60% of new motor systems installed in 2024 in North America were integrated with smart sensors for condition monitoring. Canada, meanwhile, is prioritizing high-efficiency motors in its public infrastructure upgrades, particularly for wastewater treatment and power transmission. The region’s focus on reducing carbon emissions and implementing the IE4 motor efficiency standards has accelerated the replacement of outdated motor systems. Additionally, the expansion of electric vehicle charging infrastructure and smart grid projects across North American cities is further boosting demand for high-capacity motors that ensure operational stability and low energy consumption.

Europe's medium and high power motors market is being shaped by strict environmental regulations and a push toward energy efficiency in industrial operations. Germany, the U.K., and France remain key contributors, with Germany accounting for nearly 28% of the regional market share. European industries are increasingly retrofitting legacy systems with IE4 and IE5 motors to align with the EU’s energy performance targets. Additionally, more than 45% of Europe’s newly installed motors in 2024 were deployed in sectors like power generation, water treatment, and heavy equipment manufacturing. The rise in wind energy and hydrogen fuel infrastructure has further driven the demand for high voltage motors capable of withstanding high loads and operating under challenging environmental conditions. Eastern European countries are also emerging as new hotspots due to rapid industrialization and EU-backed infrastructure funding initiatives.

Asia-Pacific remains the global leader in the medium and high power motors market, accounting for 38.4% of total share in 2024. China leads the pack, representing more than 52% of the regional share due to extensive deployment in cement, steel, and chemicals manufacturing sectors. India is rapidly catching up, with over 25% year-on-year growth in installations driven by infrastructure and metro rail projects. Japan and South Korea are focusing on automation-driven industries and renewable energy, particularly in wind and hydro sectors. Across the region, over 70% of high power motor installations in 2024 were for industrial machinery and utility operations. Investments in smart factories and green energy are transforming demand patterns, with countries prioritizing long-lifecycle motors with minimal energy losses. Asia-Pacific is also witnessing increased demand for explosion-proof motors in hazardous environments such as oil refineries and mining operations.

South America is emerging as the fastest-growing region in the medium and high power motors market. Brazil and Chile are at the forefront, with Brazil alone accounting for nearly 46% of the regional share. The rapid expansion of copper and lithium mining operations is fueling demand for rugged, high-capacity motors for crushers, conveyors, and mills. Chile, with its robust hydropower sector, has significantly increased installations of medium and high power motors for turbine and pump operations. The region is also seeing upgrades in power grid infrastructure and water management systems. In 2024, more than 60% of new motor installations in South America were in the utilities and mining sectors. Governments are also offering incentives for companies to adopt energy-efficient motors, creating momentum for IE3 and IE4 standard motors. This regulatory support combined with industrial growth is making South America a pivotal market over the coming years.

The Middle East & Africa region is experiencing robust growth in the medium and high power motors market, primarily driven by large-scale oil & gas operations and infrastructure development. Saudi Arabia and the UAE are the largest markets in this region, collectively contributing over 58% of total market share. The motors are extensively used in pipeline operations, drilling systems, and gas processing units requiring high torque and flameproof motor configurations. Meanwhile, African nations like South Africa and Nigeria are investing in water treatment plants and electric utilities, increasing demand for medium power motors. Over 50% of newly installed motors in 2024 across the region were directed toward industrial utilities and energy systems. As countries aim to diversify their energy portfolios with solar and wind projects, the deployment of efficient and robust motor systems is gaining momentum, especially in remote and high-temperature zones.

The medium and high power motors market is highly competitive, with several key players competing on the global stage. Major companies in the market invest heavily in R&D, innovation, and strategic partnerships to maintain their competitive edge. These companies are focused on improving energy efficiency, reducing the carbon footprint of their motors, and expanding their product portfolios to cater to a wide range of industries. The market is characterized by a mix of established global players and emerging regional players, leading to intense competition across different regions. Key players are also emphasizing the integration of advanced technologies such as AI and IoT to enhance motor performance and operational efficiency. Moreover, the growing demand from industries such as automotive, oil and gas, and renewable energy further intensifies the competitive landscape. With rapid advancements in motor technologies, companies are also focusing on improving the durability and scalability of their solutions to meet the changing demands of end-users.

Siemens AG

General Electric Company

ABB Ltd.

Toshiba Corporation

Nidec Corporation

Mitsubishi Electric Corporation

Schneider Electric SE

WEG S.A.

Hitachi Ltd.

Yaskawa Electric Corporation

The medium and high power motors market is witnessing significant technological advancements, driven by the need for greater efficiency, sustainability, and adaptability in industrial applications. One of the key innovations is the development of variable frequency drives (VFDs), which allow precise control over motor speed and torque, optimizing energy usage and reducing waste. VFDs are especially important in industries where variable loads are common, such as in HVAC systems and pump applications, leading to substantial energy savings. Another transformative technology is integrated motor controlsthat combine motors with sensors and microprocessors for better operational control. These smart motors are capable of real-time diagnostics, enabling predictive maintenance and reducing downtime. By integrating motor systems with IoT platforms, companies can remotely monitor performance, detect faults early, and schedule maintenance proactively, significantly improving the reliability of critical infrastructure.

Additionally, advances in material sciencehave enabled the development of lighter and more durable motor components. Innovations in permanent magnet technology, such as rare-earth magnets, have made motors more energy-efficient, particularly in high-demand applications like renewable energy generation. For example, high-efficiency induction motorsare being designed with improved winding technologies and optimized cooling methods to meet stringent energy standards and enhance long-term performance. The ongoing shift towards electric vehicles (EVs)and renewable energy sources, like wind and solar, has also pushed the demand for high-performance motors, driving further innovation in motor technologies. These developments help meet both the performance and environmental demands of industries, setting the stage for a more energy-efficient and sustainable future.

In May 2024, Mercedes-Benz began mass production of YASA's axial-flux motors, previously used in Ferrari, Lamborghini, and McLaren vehicles. These compact motors reduce vehicle weight by up to 200 kg, enhancing performance and efficiency.

In March 2024, Conifer, a Silicon Valley startup, introduced a cost-effective axial-flux motor that replaces rare-earth magnets with iron-based materials. This innovation offers 20% higher efficiency and is suitable for applications ranging from scooters to electric vehicles.

In November 2023, Evolito, a UK-based company, received Design Organisation Approval from the Civil Aviation Authority for its electric propulsion systems. This milestone validates its engineering capabilities and regulatory compliance in the aviation sector.

In August 2023, Rockwell Automation partnered with Infinitum, a company specializing in sustainable air-core motors, to jointly develop and distribute high-efficiency motor technology. This collaboration aims to reduce energy consumption and costs for customers.

The scope of the Medium and High Power Motors Market report includes a detailed analysis of the market trends, drivers, restraints, and opportunities shaping the industry. This report provides insights into the market size, segmentation by type, application, and end-user, along with regional market assessments. The report covers various types of motors, including permanent magnet motors, induction motors, and synchronous motors, providing in-depth insights into their demand and supply dynamics.

The report also explores key applications in industries such as automotive, industrial automation, HVAC, and renewable energy, identifying the leading sectors driving market growth. It highlights end-users like manufacturers, service providers, and energy producers who are adopting medium and high power motors to meet increasing demand for efficient energy solutions.

Regional insights include an analysis of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, focusing on how regional markets are evolving with technological advancements and rising investments in industries reliant on high-efficiency motors. Key players in the market are profiled to provide an understanding of competitive dynamics, including their strategies for market penetration and technological advancements.

This report helps stakeholders make informed decisions by providing a comprehensive understanding of the current market landscape, future trends, and growth prospects across various regions and sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5,780.2 Million |

|

Market Revenue in 2032 |

USD 7,971.7 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, General Electric Company, ABB Ltd., Toshiba Corporation, Nidec Corporation, Mitsubishi Electric Corporation, Schneider Electric SE, WEG S.A., Hitachi Ltd., Yaskawa Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |