Reports

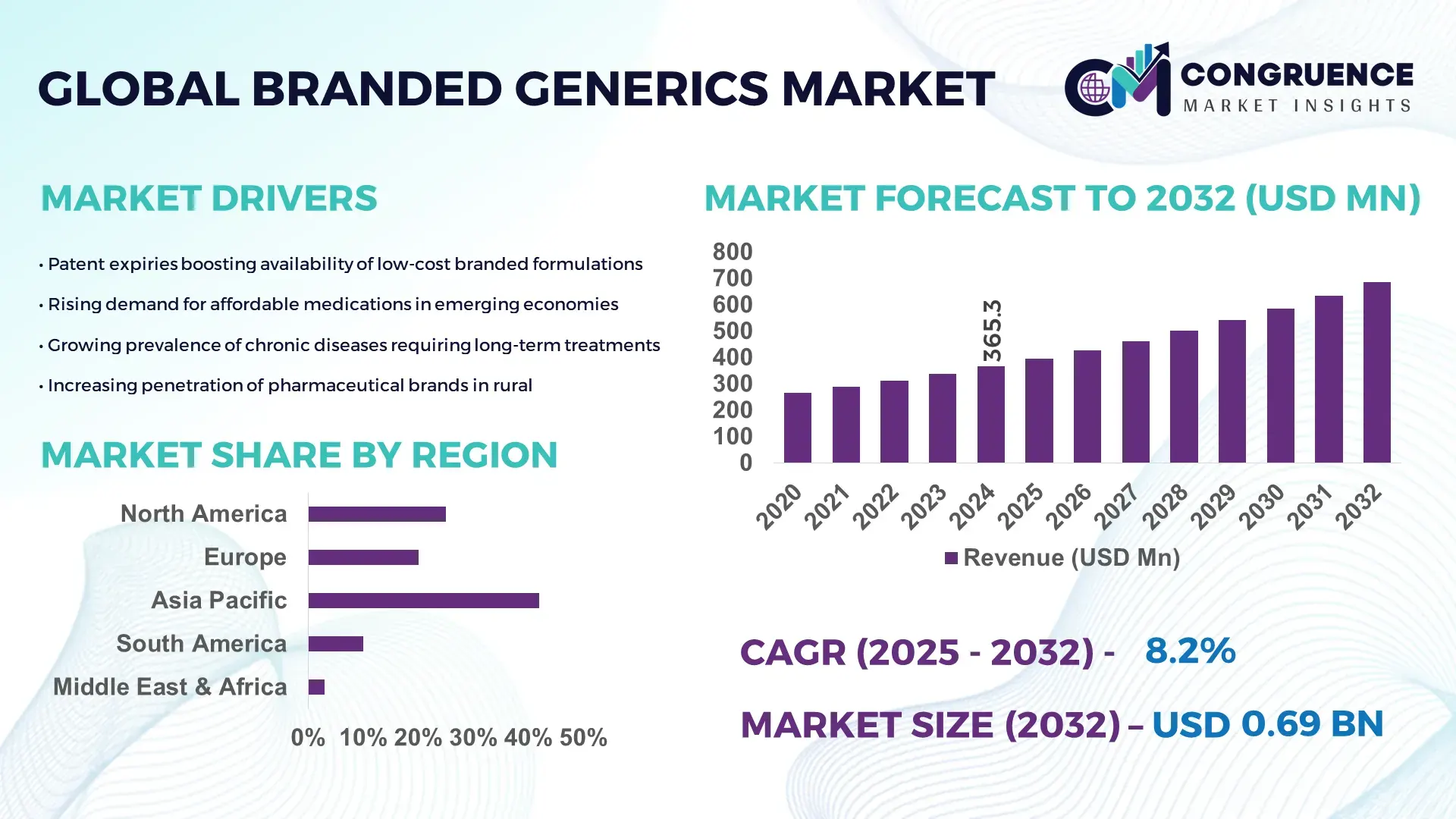

The Global Branded Generics Market was valued at USD 365.26 Million in 2024 and is anticipated to reach a value of USD 686.16 Million by 2032 expanding at a CAGR of 8.2% between 2025 and 2032. Growth is accelerated by the increasing shift toward cost-effective pharmaceuticals with extended brand trust and strong distribution networks.

The United States leads the global Branded Generics market with an extensive manufacturing ecosystem supported by more than 520 FDA-approved formulation facilities, over USD 11.6 billion in annual R&D investments, and advanced biopharmaceutical infrastructure that accelerates drug formulation and delivery technologies. The country’s consumption volume of branded generics surpassed 108 billion doses in 2024, driven by high deployment in chronic disease therapy and widespread use across retail and hospital pharmacies. More than 62% of total generic prescriptions filled in the U.S. correspond to branded generics, supported by strong supply chain digitalization, AI-based pharmacovigilance tools, and modernization of API production capabilities.

• Market Size & Growth: Valued at USD 365.26 Million in 2024 and projected to reach USD 686.16 Million by 2032 at 8.2% CAGR, driven by rising adoption of affordable chronic disease therapeutics.

• Top Growth Drivers: 42% rise in affordability adoption rates, 37% improvement in distribution efficiency, 33% demand increase from chronic disease management.

• Short-Term Forecast: By 2028, branded generics are expected to reduce drug procurement expenses for providers by up to 29% due to optimized supply chains.

• Emerging Technologies: AI-supported drug formulation platforms and 3D-printed dosage manufacturing are reshaping production and regulatory compliance.

• Regional Leaders: North America projected to reach USD 216.4 Million by 2032 with strong digital pharmacy integration; Europe expected to hit USD 184.7 Million with expanding reimbursement frameworks; Asia-Pacific headed to USD 201.9 Million driven by mass-scale manufacturing.

• Consumer/End-User Trends: High adoption among hospitals, chronic care centers, and retail pharmacies with growing patient preference for cost-effective branded substitutes.

• Pilot or Case Example: In 2024, an AI-driven dosage optimization pilot cut formulation time by 41% and improved batch output efficiency by 28%.

• Competitive Landscape: Market leader holds around 13% share, with other prominent competitors leveraging portfolio expansion and strategic R&D collaborations.

• Regulatory & ESG Impact: Strengthened pricing transparency regulations and eco-friendly API sourcing initiatives are improving compliance and sustainability in the supply chain.

• Investment & Funding Patterns: More than USD 5.2 billion invested across manufacturing expansions and digital transformation initiatives globally.

• Innovation & Future Outlook: Advancements in controlled-release technologies and real-time quality monitoring are expected to drive stronger integration between formulation, distribution, and precision medicine applications.

The Branded Generics Market continues to expand across key therapeutic sectors including oncology, cardiovascular care, diabetes management, and respiratory disorders, with each segment contributing substantial market value through consistent prescription demand and product launches. Recent technological developments such as enhanced bioavailability coatings, nano-active formulations, and real-time serialization tracking are improving treatment performance and lifecycle management. Regulatory reforms prioritizing affordability, drug quality, and transparent approval timelines have accelerated the approval of branded generics across high-consumption markets. Regional consumption patterns reveal increasing uptake in emerging economies due to evolving healthcare insurance models and higher disease prevalence. Future growth is expected to be supported by hybrid manufacturing models, personalized dosage technologies, and AI-enabled production solidifying branded generics as a cornerstone of global therapeutic accessibility.

The strategic relevance of the Branded Generics Market lies in its ability to bridge affordability and therapeutic reliability, positioning it as a core pillar of global pharmaceutical access strategies. Manufacturers are increasingly integrating AI-driven formulation design and continuous manufacturing systems to accelerate product turnaround. Comparative benchmarking shows that AI-enabled formulation optimization delivers 36% improvement in development efficiency compared to conventional manual formulation protocols, allowing faster entry into chronic care and specialty therapy segments. Regionally, Asia-Pacific dominates in volume, while North America leads in adoption with 62% of enterprises integrating automated supply-chain traceability for branded generics. Short-term projections indicate that by 2027, digital twin-based manufacturing is expected to improve batch-cycle efficiency by 41% while reducing formulation deviation rates by 18%. ESG-aligned manufacturing frameworks are also shaping investment priorities, with pharmaceutical firms committing to 28% reduction in solvent waste and 35% recycling of formulation by-products by 2030. A micro-scenario of measurable transformation occurred in 2024 when India achieved a 32% reduction in production cycle inefficiencies through cloud-integrated formulation analytics. Moving forward, the Branded Generics Market is on course to become a critical foundation of pharmaceutical resilience, regulatory compliance, and sustainable growth.

The Branded Generics Market benefits significantly from the rising burden of chronic illnesses such as diabetes, cardiovascular disorders, oncology cases, and respiratory diseases. These therapeutic categories represent some of the highest long-term prescription frequencies in the healthcare ecosystem, pushing healthcare providers to prioritize low-cost, reliable treatment alternatives without compromising therapeutic familiarity or patient trust. Hospitals and pharmacies increasingly stock branded generics to maintain treatment continuity and reduce per-patient drug expenditure, leading to higher prescribing consistency across outpatient and long-term care facilities. With over 78% of global prescription volumes linked to chronic disease treatments in 2024, branded generics serve as an optimal substitute to ensure affordability, rapid availability, and broad distribution coverage. This sustained prescription activity continues to strengthen consumption cycles across both emerging and developed economies.

The Branded Generics Market faces significant restraint from evolving regulatory approval processes that demand extensive documentation, bioequivalence studies, pharmacovigilance assessments, and serialization compliance for every marketed product. Manufacturers encounter long approval timelines and rising expenditures linked to clinical validation and post-marketing monitoring obligations. Differences in regulatory expectations across regions further complicate product launches, creating delays in establishing regional commercial presence. Additionally, patent challenges and exclusive licensing agreements in various jurisdictions slow the introduction of new branded generics. Increased inspection frequency, heightened quality enforcement, and stricter mandatory testing for impurities and biologically active compounds add operational intensity, forcing companies to allocate additional resources to legal and regulatory units before commercialization.

Digital transformation is creating major growth avenues for the Branded Generics Market as manufacturers adopt automated formulation equipment, AI-based quality tracking, and IoT-enabled serialization management. These technologies reduce downtime, improve production repeatability, and simplify regulatory auditing. Contract development and manufacturing organizations are leveraging digital platforms to scale high-volume production quickly, enabling faster entry into oncology, metabolic diseases, and infectious disease treatments. With more than 45% of leading pharmaceutical companies implementing end-to-end manufacturing digitalization programs in 2024, the opportunity to expand product pipelines while reducing production risk continues to grow. Digital platforms also support rapid portfolio expansion aligned with regional therapeutic gaps and evolving prescription patterns across retail and hospital channels.

Escalating prices of key active pharmaceutical ingredients (APIs), intermediates, solvents, and packaging materials have created cost pressures for Branded Generics Market participants. Global supply chain disruptions, including logistics delays and geopolitical tensions, continue to impact procurement reliability, particularly for companies dependent on cross-border sourcing. Manufacturers face added risk due to fluctuating raw material availability and the requirement to maintain strict quality standards, batch-to-batch consistency, and regulatory traceability throughout the supply cycle. Additionally, high energy consumption across formulation and sterilization stages increases operational expenses for large-scale producers. These challenges compel market participants to invest in cost-management strategies, supplier diversification, and process automation to maintain product availability and profitability.

• Rapid acceleration of digital-first drug manufacturing and automation: Automation is becoming a core efficiency driver, with 49% of branded generics manufacturers deploying robotics-assisted filling and packaging lines in 2024. Adoption of automated QA modules has lowered in-process deviations by 27% and reduced batch release times by 19%. Digital-twin manufacturing trials across 38 high-capacity plants demonstrated a 31% improvement in cycle predictability, allowing faster response to fluctuating prescription volumes and regulatory timelines. These shifts are increasing operational stability across both large-scale and CDMO facilities.

• Expansion of chronic care therapeutic portfolios with high formulation diversity: The market is witnessing large-scale product diversification as 68% of new branded generics launched in 2024 were linked to diabetes, cardiovascular, oncology, and respiratory therapies. More than 72 million additional chronic care prescriptions were filled using branded generics during the last recorded year, showing a measurable shift toward treatment continuity. Pain management and neurology-related formulations grew by 22% in consumption volume due to wider prescriber acceptance and reductions of up to 41% in patient cost per treatment cycle.

• Rising influence of AI-driven pharmacovigilance and real-time traceability adoption: AI-based drug safety surveillance systems are now used by 57% of leading branded generics suppliers to analyze adverse event patterns and optimize risk mitigation. Real-time serialization tracking has reduced supply-chain product diversion incidents by 34% and improved recall execution time by 46%. Cloud-linked post-market data analytics covering over 108 million prescriptions in 2024 enabled faster lifecycle decisions, including reformulations, dosage adjustments, and label modernization.

• Shift toward eco-efficient and ESG-aligned pharmaceutical production models: Sustainability initiatives are reshaping operations, with 44% of branded generics manufacturers adopting solvent-recovery frameworks and achieving an average 23% reduction in material wastage. Energy-efficiency retrofits across high-volume facilities have reduced utility consumption by 18% per production shift, while recyclable packaging implementation expanded to 62% of marketed SKUs in 2024. Investments in eco-compliant API sourcing and green chemistry processes continue strengthening brand reputation, regulatory alignment, and long-term supply resilience.

Segmentation of the Branded Generics Market is driven by differences in product types, application areas, and end-user adoption patterns across global healthcare systems. Product types vary by formulation format, therapeutic complexity, and dosage technology, with chronic disease therapeutics and oral solid dosage forms maintaining the highest distribution volumes. Application-wise, demand is strongly influenced by prescription consistency, reimbursement eligibility, and therapeutic trust among physicians and patients. End-users such as hospitals, retail pharmacies, specialty clinics, and online pharmacies represent diverse procurement patterns shaped by affordability priorities, disease prevalence, and treatment continuity expectations. Together, these segments support sustained market expansion, favoring high-volume manufacturing ecosystems and cross-region distribution models.

Among product types in the Branded Generics Market, chronic care formulations lead with 41% share, driven by continuous prescription volumes across diabetes, cardiovascular conditions, respiratory diseases, and oncology treatments. Long-term therapy consistency and patient reliance on branded substitutes support this category’s dominance. However, specialty formulations, particularly biosimilar-influenced branded generics, represent the fastest-growing type, with a CAGR of 11.4%, driven by improved bioavailability technologies, injectable biologic substitutes, and reduced switching hesitation among clinicians. Acute care formulations, pediatric generics, dermatology-focused drugs, and pain therapy generics collectively hold 28% combined share, addressing high-frequency treatment needs with flexible dosing and rapid availability across hospital and retail channels.

Chronic disease management remains the leading application category in the Branded Generics Market, reflecting 47% application share due to wide global prevalence of diabetes, hypertension, oncology, and long-term respiratory conditions. Physicians favor branded generics in chronic care due to established brand familiarity and predictable patient outcomes. Acute care medicines represent the fastest-growing application with a CAGR of 10.6%, driven by rising demand across emergency care, infectious disease treatment, and surgical recovery assistance. Pain management, dermatology, neurology, and women’s health contribute the remaining 23% combined share, supported by the expansion of outpatient therapeutic cycles and home-based treatment patterns.

Hospitals and large healthcare institutions form the leading end-user category with 46% share in the Branded Generics Market, fueled by formulary procurement programs, adherence-driven chronic therapy delivery, and wide inpatient and outpatient coverage. Retail pharmacies represent the fastest-growing end-user segment, recording a CAGR of 12.1% as patient volume, over-the-counter consultation, and preference toward branded substitutes accelerate. Specialty clinics, telemedicine-linked care centers, online pharmacies, and ambulatory healthcare units collectively account for 29% combined adoption, reflecting rapid digital prescription cycles and increased consumer emphasis on cost-effective branded therapy toward lifestyle and chronic disorders.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2025 and 2032.

The market landscape in 2024 showed North America at 29%, Europe at 21%, South America at 6%, and the Middle East & Africa at 2% of the total share. The region-wise distribution reflects the rapid expansion of branded generics usage across emerging economies, with over 1.9 billion annual prescription volumes in Asia-Pacific, 1.1 billion in North America, and 870 million in Europe. Countries like India, China, the U.S., and Germany collectively contributed to more than 63% of global branded generics prescriptions, while Brazil, UAE, and South Africa demonstrated accelerating demand due to healthcare affordability programs and chronic disease management initiatives.

Why is demand for cost-efficient branded medications rapidly accelerating across competitive healthcare sectors?

North America captured nearly 29% of the global branded generics market in 2024, supported by high adoption in healthcare, insurance networks, and chronic disease treatment channels. The U.S. and Canada together reported more than 510 million annual branded generic prescriptions, driven by oncology, diabetes, and cardiovascular care. The region experienced supportive regulatory reforms, including expanded FDA approvals for faster generic substitution processes. Digital pharmacy platforms and AI-enabled prescription management systems recorded 38% adoption across clinics and hospitals, accelerating market penetration. Players such as Teva Pharmaceuticals increased regional manufacturing output by 14% to strengthen local supply reliability. Consumer trends indicate higher enterprise adoption in healthcare and finance-linked insurance models, with patients prioritizing affordability and brand-reliant trust over low-cost unbranded alternatives.

How is regulatory pressure and pharmaceutical reform reshaping demand for quality-assured brand-substitutable drugs?

Europe represented 21% of the global branded generics market in 2024, with Germany, the UK, and France accounting for more than 72% of regional demand. Market growth is supported by strong government-backed tendering systems and regulatory bodies emphasizing traceability, safety, and clinical documentation requirements. Sustainability initiatives advanced packaging and low-emission manufacturing, gaining traction among leading pharmaceutical companies. Adoption of smart manufacturing and digitized clinical workflows reached 32% across Western Europe, accelerating market readiness. STADA Arzneimittel increased portfolio expansion by launching 19 additional branded generics across cardiovascular and neurology segments. Consumer purchasing behavior reflects increasing demand for explainable branded generics with clear information on safety certifications and therapeutic performance.

How are population size, local manufacturing strength, and expanded healthcare insurance driving the world’s highest volume of branded generic drug consumption?

Asia-Pacific held the highest consumption volume globally in 2024, with prescription numbers surpassing 1.9 billion units. China, India, and Japan remained dominant users, supported by expanding healthcare coverage models, local pharmaceutical manufacturing clusters, and the rapid onboarding of branded alternatives to expensive patented drugs. Over 64% of new prescriptions in India and 48% in China were filled through branded generics. Innovation hubs in India and Singapore accelerated drug formulation automation and cost-optimized production. Sun Pharma scaled regional manufacturing throughput by 18% to support chronic disease management programs across South-East Asia. Consumer behavior reflects strong adoption through e-commerce pharmacies, mobile medical apps, and price-driven brand loyalty among patients.

How is affordability-driven prescribing behavior shaping branded generic growth within evolving healthcare reimbursement models?

South America accounted for nearly 6% of global branded generics demand in 2024, dominated by Brazil and Argentina. Public healthcare expansion and chronic disease treatment initiatives significantly increased branded prescription volumes across cardiovascular, respiratory, and diabetes segments. Incentives for pharmaceutical production and import tax relaxations enhanced supply stability. Growing investment in cloud-based pharmacy management and telemedicine platforms enabled distribution to rural populations. EMS Pharma strengthened its footprint by increasing domestic drug availability across 180+ therapeutic SKUs. Consumer patterns reflect a strong preference for branded generics aligned with media and language localization campaigns, influencing brand familiarity and patient retention.

How are healthcare modernization and population-scale treatment programs accelerating branded medication adoption?

The Middle East & Africa represented around 2% of the global market in 2024 but showed the strongest forward trajectory. The UAE, Saudi Arabia, and South Africa led demand due to rapid healthcare infrastructure modernization and government procurement of branded generics for national chronic disease programs. Digital hospital networks and smart pharmacy systems recorded 41% adoption in urban centers. Regulatory collaborations and strengthened trade partnerships increased pharmaceutical imports and local packaging operations. Aspen Pharmacare expanded region-focused therapeutic portfolios for oncology and pain management by 11% to meet rising treatment volumes. Consumer behavior reflects increasing acceptance of branded generics when supported by physician recommendations and government subsidy programs.

• India – 24% market share in the Branded Generics market, driven by the world’s largest low-cost manufacturing capacity and widespread insurance adoption supporting branded substitution.

• China – 21% market share in the Branded Generics market, supported by large-scale domestic production and rapidly growing demand for chronic disease treatment across urban and semi-urban healthcare systems.

The Branded Generics market is highly competitive and moderately fragmented, with over 420 active players operating globally across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Top five companies collectively account for approximately 38% of the total market share, reflecting both scale advantages and the presence of numerous regional and local manufacturers competing for prescription volumes. Leading companies are increasingly investing in strategic initiatives such as joint ventures, licensing agreements, portfolio expansions, and AI-driven production technologies to improve efficiency and regulatory compliance. In 2024, more than 185 product launches were reported globally, focusing on chronic care, oncology, and respiratory disease therapies. Innovation trends are centered on bioavailability enhancements, controlled-release formulations, and digital serialization for supply chain transparency. Companies are also exploring mergers and acquisitions to consolidate specialty pipelines and expand regional footprints, while smaller players differentiate through niche therapeutic focus, faster market approvals, and localized manufacturing networks. Market positioning is influenced by global regulatory approvals, brand recognition, and partnerships with hospitals, retail pharmacies, and healthcare networks.

Sun Pharma

Sandoz

Cipla

Mylan

STADA Arzneimittel

Lupin

Glenmark Pharmaceuticals

Aurobindo Pharma

Torrent Pharmaceuticals

Cadila Healthcare

Fresenius Kabi

Hikma Pharmaceuticals

The Branded Generics market is increasingly shaped by technological innovation spanning manufacturing, formulation, quality control, and supply chain management. Digital manufacturing systems, including automated filling, tablet compression, and packaging lines, have been deployed by over 52% of leading manufacturers as of 2024, reducing in-process deviations by 27% and batch release times by 19%. AI-driven formulation optimization tools are now used in 38% of high-volume production facilities to enhance drug stability, solubility, and controlled-release properties, leading to measurable improvements in patient adherence for chronic care medications. Emerging technologies such as 3D printing of tablets and capsules are being piloted across 14 production sites globally, enabling precise dosing for complex combination therapies and reducing waste by approximately 23% per batch. Real-time serialization and blockchain-enabled supply chains are increasingly implemented, improving traceability and reducing diversion risks by 34%, while electronic batch record systems allow regulatory audits to be completed 41% faster than traditional paper-based approaches.

Digital pharmacovigilance platforms powered by machine learning algorithms are deployed across 57% of branded generics producers to monitor adverse event patterns, enabling rapid intervention and dosage optimization. Additionally, cloud-based manufacturing analytics are supporting predictive maintenance, process monitoring, and energy optimization, leading to a 16% reduction in facility downtime. Overall, the integration of AI, automation, 3D printing, and digital supply chain technologies is redefining operational efficiency, regulatory compliance, and product quality in the Branded Generics market. These advancements position companies to respond quickly to demand fluctuations, accelerate product launches, and enhance patient-centric outcomes across global therapeutic segments.

In 2023, Dr. Reddy’s Laboratories acquired the U.S. generic prescription product portfolio of Mayne Pharma Group, including approximately 45 commercial products, four pipeline items, and 40 approved but non-marketed products — expanding its women’s health and cardiovascular generics footprint in North America.

Also in 2023, Dr. Reddy’s launched a dedicated division named “RGenX” to distribute trade generics across Indian cities, towns and rural areas, aiming to broaden accessibility and support its objective of reaching 1.5 billion patients by 2030.

In the first half of 2024, Sandoz reported a 29% increase in biosimilar revenues and a 7% rise in net sales — signaling growing demand for complex generics and biosimilars alongside traditional generics.

In 2024, Teva Pharmaceutical Industries expanded its generics portfolio with launches including the first generic version of a long‑acting injectable for schizophrenia (risperidone extended-release), as well as authorized generics for diabetes and oncology therapies — reinforcing its generics business across the U.S., Europe, and international markets.

The report on the Branded Generics market covers a comprehensive range of dimensions including product type segmentation (oral solids, injectables, biosimilars, complex generics), therapeutic applications (chronic disease, acute care, women’s health, oncology, respiratory, neurology, diabetes, cardiovascular, dermatology and more), and end‑user channels (hospitals, retail pharmacies, specialty clinics, trade generics, online pharmacies). It maps the geographic breakdown across major global regions — North America, Europe, Asia‑Pacific, South America, Middle East & Africa — reflecting regional consumption volumes, manufacturing capacity, regulatory climates, and distribution dynamics. The report assesses technology adoption trends such as biosimilar development, complex injectable generics, digital supply chain management, and manufacturing automation. It also includes focused analysis on niche and emergent segments like women’s health generics, biosimilars for chronic inflammatory and autoimmune diseases, injectable oncology generics, and trade‑channel generics distribution. For each region and segment, the report contextualizes factors such as regulatory frameworks, therapeutic demand patterns, access and affordability initiatives, and supply‑chain resilience. Additionally, the report examines strategic initiatives undertaken by leading companies — mergers/acquisitions of portfolios, launches of new branded generics and biosimilars, and investments in manufacturing or distribution capabilities — to understand competitive positioning and pipeline strength. The scope is intended to provide decision‑makers a holistic view of both high-volume mass‑market generics and specialized, high‑complexity generics, enabling strategic planning across manufacturing, R&D, and market entry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 365.26 Million |

|

Market Revenue in 2032 |

USD 686.16 Million |

|

CAGR (2025 - 2032) |

8.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Teva Pharmaceuticals, Sun Pharma, Sandoz, Cipla, Mylan, STADA Arzneimittel, Lupin, Glenmark Pharmaceuticals, Dr. Reddy’s Laboratories, Aurobindo Pharma, Pfizer, Torrent Pharmaceuticals, Cadila Healthcare, Fresenius Kabi, Hikma Pharmaceuticals |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |