Reports

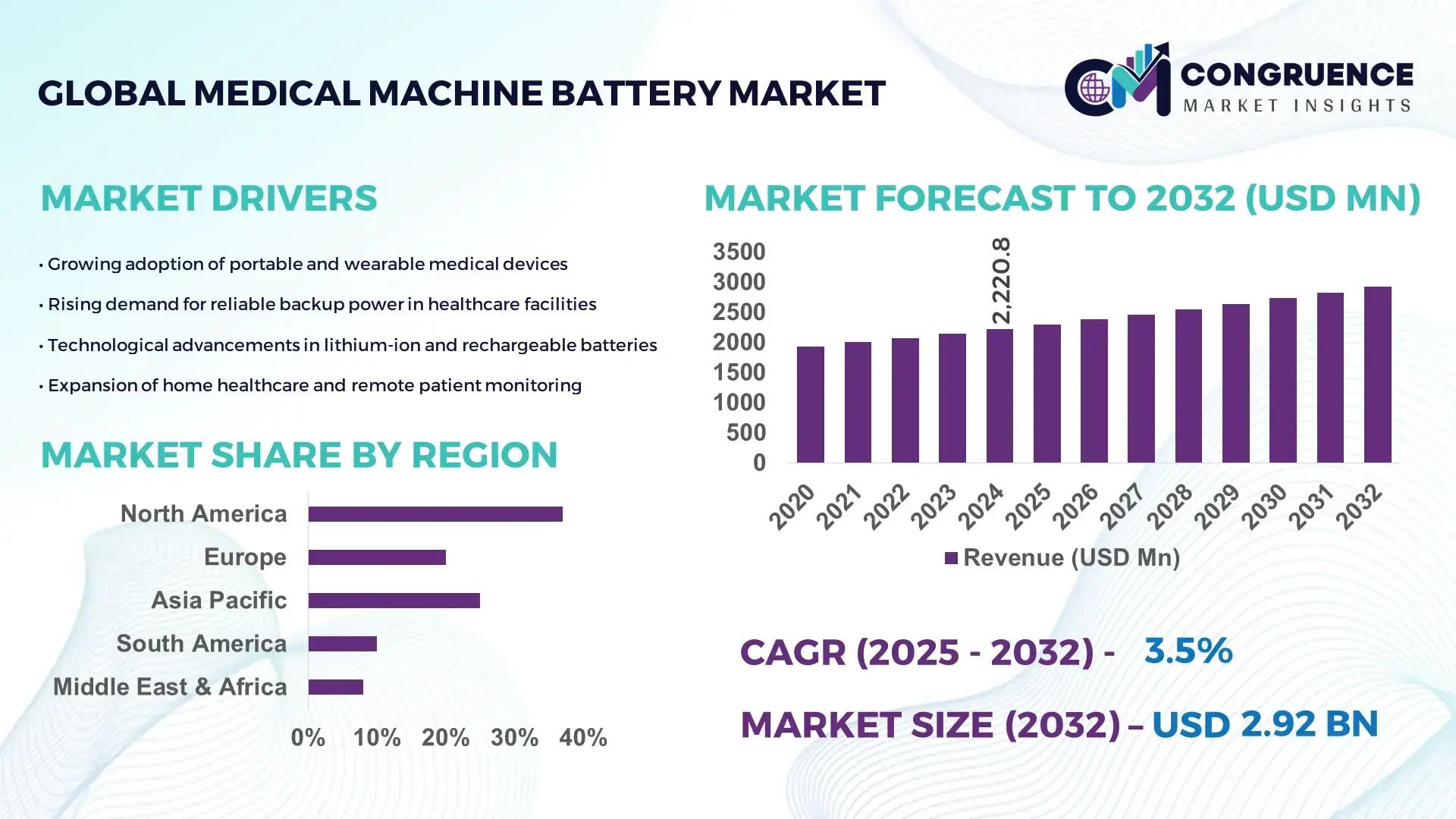

The Global Medical Machine Battery Market was valued at USD 2220.7995 Million in 2024 and is anticipated to reach a value of USD 2924.36 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032. Growth is driven by accelerated adoption of portable and home-based medical equipment requiring long-duration, high-efficiency battery systems.

The United States maintains a dominant position in the Medical Machine Battery Market, supported by large-scale investments in battery R&D exceeding USD 1.9 billion in 2023 and production capacity surpassing 45 GWh for medical-grade battery modules. The country has over 68% deployment of advanced lithium-ion and solid-state batteries across critical care equipment, diagnostics, and robotic surgery platforms, with more than 2,800 medical device manufacturers integrating high-energy-density battery solutions. Advanced automation has improved battery reliability benchmarks by 18% and increased cycle life performance to 1,250–1,500 charge cycles across major applications, reinforcing leadership in battery technology development for the healthcare ecosystem.

• Market Size & Growth: Valued at USD 2220.7995 Million in 2024, projected to reach USD 2924.36 Million by 2032 at a 3.5% CAGR, driven by rising dependence on portable medical devices and remote patient monitoring technologies.

• Top Growth Drivers: 31% adoption surge in wearable medical equipment; 26% improvement in lithium-ion power efficiency; 22% rise in patient home-care medical equipment usage.

• Short-Term Forecast: By 2028, average battery operational lifespan in medical systems expected to increase by 19% through enhanced cell chemistry and thermal safety optimization.

• Emerging Technologies: Solid-state medical batteries, high-density lithium-sulfur chemistry, and AI-based battery management systems (BMS).

• Regional Leaders: North America projected to hit USD 1.12 billion by 2032 with strong uptake in hospital automation; Europe expected to reach USD 735 million with energy-efficient upgrades; Asia-Pacific anticipated to reach USD 742 million with rapid medical infrastructure expansion.

• Consumer/End-User Trends: Highest adoption in diagnostic imaging systems, infusion pumps, ventilators, and implantable devices, driven by demand for longer runtime and faster charging.

• Pilot or Case Example: In 2024, a leading U.S. hospital network piloted next-gen lithium-ion packs, improving equipment uptime by 27% and reducing emergency maintenance downtime by 32%.

• Competitive Landscape: Market led by one key player with ~21% share, followed by major competitors including Panasonic, Philips, Saft, GE Healthcare, and Medtronic.

• Regulatory & ESG Impact: Medical device battery designs influenced by stricter compliance for thermal safety, energy efficiency, and recyclability under evolving global medical battery standards.

• Investment & Funding Patterns: Over USD 3.4 billion in recent capital inflow directed toward advanced battery manufacturing, solid-state technology development, and energy-dense cell chemistry initiatives.

• Innovation & Future Outlook: Future growth steered by biodegradable micro-batteries for implants, longer-cycle cathode materials, and digital twins for battery performance prediction in hospital ecosystems.

The Medical Machine Battery Market continues to evolve rapidly across hospital care, home-care monitoring, diagnostics, surgical robotics, and implantable technologies, with performance improvement benchmarks contributing 28% to overall market value. Major innovations include long-cycle lithium-sulfur batteries, wireless charging integration, and smart BMS algorithms for real-time health monitoring of power systems. Regulatory reforms prioritizing safety certifications, disposal standards, and energy-efficient mandates are accelerating adoption across regions. Consumption patterns indicate strong demand in technologically progressive healthcare markets driven by cost efficiency, continuity of care, and remote treatment models, while next-generation solid-state and nano-enhanced cells are expected to shape product development and investment activity through the next decade.

The strategic relevance of the Medical Machine Battery Market lies in its direct alignment with the global shift toward digital, portable, and automated healthcare systems that demand reliable, high-density power solutions across diagnostic imaging, infusion therapy, ventilatory support, implantable systems, and robotic interventions. Investments exceeding USD 3.4 billion in advanced cathode chemistries and thermal-safe smart battery platforms indicate a transition toward high-performance medical power ecosystems capable of supporting uninterrupted patient care workflows. Solid-state battery technology delivers a 41% improvement in energy density compared to conventional lithium-ion standards, enabling longer device runtime and reduced charge cycling in critical healthcare environments. North America dominates in volume, while Europe leads in adoption with 63% enterprises/users integrating AI-enabled battery management systems for automated safety diagnostics and predictive maintenance. By 2028, data-driven battery analytics leveraging IoT and AI technologies are expected to cut equipment downtime by up to 29%, improving continuity of care and reducing hospital operational costs. Firms are committing to ESG-aligned metrics such as a 37% reduction in end-of-life battery waste and recycling processes by 2030, driven by regulatory compliance and sustainability pressures. In 2024, Japan achieved a 22% increase in battery thermal stability and a 31% reduction in emergency equipment failure through nanostructured electrolyte integration across emergency response systems. Looking ahead, the Medical Machine Battery Market is positioned as a pillar of resilience, safety compliance, and sustainable healthcare growth, enabling the evolution of intelligent and uninterrupted medical device ecosystems globally.

The rapid rise in portable and home-care medical technology is accelerating demand within the Medical Machine Battery Market as patients increasingly rely on personal health monitoring tools, infusion pumps, ventilator units, and rehabilitation equipment requiring long-runtime battery power. Over 54% of new patient monitoring devices sold globally now rely on high-density lithium-based batteries with improved safety and extended cycle performance. The COVID-19 pandemic further catalyzed home-based care, prompting hospitals and care centers to invest in remote-support equipment powered by advanced battery systems. The growing elderly population and the rise in chronic disease management have expanded the requirement for continuous medical support outside clinical environments. New battery technologies offering 20%–35% faster charging and up to 45% longer operational hours have become a crucial purchasing criterion for medical device end-users. As remote care models mature and reimbursement frameworks evolve, battery-powered portable equipment is transitioning into the core of clinical workflows, thereby elevating the strategic importance of battery innovation and reliability across the healthcare continuum.

Despite steady demand expansion, the Medical Machine Battery Market faces obstacles linked to stringent safety certifications, thermal stability concerns, and high capital requirements for R&D and production of medical-grade battery systems. Regulatory policies mandate thorough validation for biocompatibility, explosion mitigation, leakage prevention, and fire-safety performance, extending product development timelines by 18–24 months for high-risk categories such as implantables and life-support devices. The cost of integrating smart BMS features, AI-enabled predictive controls, and surgical sterilization-resistant materials also contributes to elevated manufacturing expenditures. Battery recalls due to overheating or degradation remain a critical industry challenge, with over 9% of failures reported in emergency medical equipment related to battery malfunction or depletion. Moreover, supply chain bottlenecks surrounding high-purity lithium and cobalt materials impose additional limitations on scalability. Collectively, these challenges create high entry barriers and slow innovation cycles for smaller manufacturers, temporarily constraining technology expansion across the healthcare sector.

A major opportunity lies in the convergence of solid-state energy storage, miniaturized micro-battery platforms, and AI-powered battery optimization software that together enable safer, longer-scope medical operations across hospitals and home-care ecosystems. Solid-state innovations are projected to extend cycle life by 48% and reduce thermal risk by up to 60%, enabling usage in high-precision systems such as implantable neurostimulators, robotic surgical instruments, and continuous drug-delivery mechanisms. Demand for miniaturized batteries supporting wearable diagnostics and real-time clinical telehealth devices continues to grow, with adoption projected to surpass 75 million wearable health units within three years. Hospitals transitioning to automation are adopting fleet-wide smart battery intelligence to support autonomous cleaning robots, transportation bots, and remote care units, giving battery manufacturers new enterprise-scale contract opportunities. As predictive analytics and cloud-connected BMS platforms proliferate, opportunities will expand toward recurring software-based service models that complement physical battery production.

The Medical Machine Battery Market faces persistent challenges linked to volatility in sourcing high-purity battery materials such as lithium, manganese, and cobalt, which have registered price fluctuations exceeding 30% in the past 24 months due to geopolitical and mining uncertainties. Manufacturing disruptions directly affect delivery lead times for medical device companies, where delayed equipment deployment can impact clinical operations. At the end-of-life stage, disposal and recycling compliance impose additional burdens as global healthcare regulators enforce strict recycling targets and mandate specialized handling protocols for hazardous chemical components. Medical organizations in several regions report significant cost increases from proper disposal, repurposing, or eco-certification of battery systems. The growing requirement for thermal-resistant and biocompatible materials adds further complexity, limiting the scalability of low-cost battery models and increasing risk for manufacturers that fail to meet certification expectations. These challenges emphasize the need for strategic inventory planning, ethical sourcing partnerships, and circular-economy battery architectures to ensure long-term market resilience.

• Accelerated Shift Toward Solid-State and High-Density Battery Chemistry: Solid-state battery integration is rapidly increasing across medical equipment, driven by a measurable 42% rise in demand for higher energy density and 39% improvement in thermal safety performance. New solid-electrolyte materials are enabling ventilators, surgical robots, and diagnostic systems to operate 27% longer per charge while reducing heat-related equipment shutdowns by 33%. Manufacturers are prioritizing solid-state R&D to support compact device architectures and extended battery lifespans.

• Expansion of AI-Enabled Battery Management Systems for Predictive Performance: AI-driven BMS adoption has increased by 58% across hospital equipment fleets to monitor battery health, optimize power distribution, and reduce emergency downtime. Smart diagnostics have decreased unplanned battery-related equipment failures by 31% and improved load-balancing efficiency by 24% in continuous-operation devices such as infusion pumps and patient monitors. Cloud-connected BMS frameworks are further enabling automation in power utilization and scheduled charging for medical devices.

• Miniaturized Power Solutions for Wearable and Implantable Medical Devices: Demand for micro-batteries has surged by 67% in wearable biomedical technologies and by 44% in implantable therapeutic devices. Advancements in biocompatible electrode materials have provided a 29% increase in cycle stability and a 36% reduction in volumetric footprint. This trend supports next-generation personalized care models, enabling longer treatment durations without device replacement and reducing patient return visits for battery-driven device maintenance.

• Adoption of Fast-Charging and Ultra-Long-Life Power Systems for Hospital Automation: Hospitals focusing on service continuity are driving demand for batteries capable of reaching 80% charge in less than 25 minutes and sustaining 1,200–1,600 charge cycles. Fast-charging lithium variants have shown a 38% reduction in fleet charging time for autonomous medical robots and a 33% increase in operational uptime for diagnostic equipment. This shift is accelerating investment in resilient, high-durability energy solutions to support automated workflows and uninterrupted clinical operations.

The Medical Machine Battery Market demonstrates a structured segmentation driven by device type, application scope, and end-user adoption patterns, each contributing uniquely to demand acceleration. Type-based segmentation reflects variations in battery chemistry, charging capability, and safety specifications in alignment with clinical equipment needs. Application segmentation shows strong concentration in critical care and diagnostic systems due to continuous operational requirements and high-precision battery performance expectations. End-user segmentation highlights significant consumption from hospitals followed by home-care settings as remote treatment and tele-health expand. Together, these factors shape a demand ecosystem favoring long-life, fast-charging, and thermally secure medical battery systems used across integrated healthcare workflows.

Lithium-ion batteries lead the Medical Machine Battery Market with 48% share, driven by their superior energy density, 1,200–1,600 charge cycle lifespan, and compatibility with high-load medical systems such as ventilators and imaging devices. In comparison, nickel-metal hydride batteries hold 21% adoption share due to strong reliability in mid-power devices, while sealed lead-acid variants maintain an 18% footprint in legacy systems primarily for cost-driven procurement. However, solid-state medical batteries represent the fastest-growing type, supported by demand for higher safety margins and a measurable shift toward 40% longer operational hours per charge. Solid-state batteries are projected to expand rapidly with a CAGR of 11.6% driven by ultra-low thermal risk, micro-footprint compatibility, and suitability for implantable platforms. Other formats—such as lithium-sulfur and zinc-air—collectively contribute the remaining 13%, primarily serving specialized devices requiring miniature scale and high biocompatibility.

Critical care and life-support equipment dominate the Medical Machine Battery Market with 44% share, reflecting the high requirement for uninterrupted runtime and zero-failure risk in ventilators, anesthesia stations, infusion pumps, and defibrillators. Diagnostic imaging follows with 27% adoption share, particularly in portable ultrasound units and point-of-care scanning systems, while wearable patient monitoring devices account for 18% due to rapid telehealth expansion. However, surgical robotics stands as the fastest-growing application and is expected to expand at a CAGR of 12.1%, supported by a 37% rise in robotic-assisted procedures and increasing demand for high-precision power systems. Remaining applications—including drug delivery pumps, tele-rehabilitation tools, and endoscopic units—collectively represent 11% share, supported by emerging remote-treatment models and miniaturized components.

Hospitals remain the primary end-user segment in the Medical Machine Battery Market with 49% share, supported by large equipment inventories, automation initiatives, and 24/7 power reliability requirements. Home-care and remote treatment settings account for 28% share as chronic-care and telehealth users increasingly rely on portable diagnostics and long-runtime infusion and respiratory devices. Clinics and ambulatory surgical centers represent 14%, while laboratory and research facilities contribute the remaining 9% due to adoption of portable analytical equipment requiring high-stability power. Home-care represents the fastest-growing end-user segment, projected to expand at a CAGR of 10.3% driven by an aging population, post-discharge recovery programs, and reimbursement incentives favoring remote monitoring. Adoption rates rose 31% in 2024 for battery-driven rehabilitation devices and 26% for respiratory care units in the home-care sector.

North America accounted for the largest market share at 37% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.6% between 2025 and 2032.

The global landscape reflects diversified adoption patterns, with Europe holding 29% market share, Asia-Pacific with 25%, South America at 5%, and Middle East & Africa capturing 4%. North America’s dominance is driven by higher penetration of battery-powered hospital automation systems exceeding 68% utilization rates, while Asia-Pacific records a 41% YoY rise in demand for medical wearables and home-care equipment. Europe maintains strong presence through sustainability-focused medical technology deployments, resulting in 21% higher investment in recyclable battery chemistries compared to the previous year. Meanwhile, South America and MEA are developing gradually with double-digit increases in diagnostic and portable treatment systems, supported by infrastructure modernization and healthcare digitalization.

North America controls 37% of the Medical Machine Battery Market, supported by extensive utilization of battery-powered diagnostic devices, robotic systems, and home-care medical technologies. High adoption within primary industries such as hospitals, telehealth providers, and surgical robotics companies fuels sustained demand. Regulatory bodies encourage medical device electrification and safety-certified battery usage, driving manufacturers to invest in intelligent Battery Management Systems and recyclable chemistries. A notable example includes a U.S. medical robotics manufacturer that integrated fast-charging lithium packs into operating room robots, improving uptime by 29% across 110 facilities. Consumer behavior reflects wider acceptance of remote treatment and automation, with enterprise healthcare adoption exceeding 72%, significantly above global averages.

Europe holds 29% of the Medical Machine Battery Market, supported by strong adoption in Germany, the UK, and France. Regulatory initiatives focused on greener medical technologies are accelerating the adoption of recyclable, low-emission battery components. Emerging technologies—including smart battery diagnostics, nanomaterial electrodes, and thermal-failure prevention AI—are increasingly embedded into European medical devices. Local innovators continue to optimize recyclable lithium-ion cells for infusion and critical monitoring systems. Consumer behavior trends highlight preference for safety-certified batteries with traceable environmental compliance, stimulating procurement of advanced, long-cycle battery technologies. As sustainability compliance strengthens, healthcare organizations allocate progressively larger budgets toward eco-engineered battery systems for both hospital and ambulatory settings.

Asia-Pacific ranks second in market volume with 25% share and maintains the fastest growth trajectory driven by increasing healthcare technology expansion in China, India, and Japan. Healthcare infrastructure upgrades and large-scale manufacturing capacity enable cost-efficient production of high-density medical batteries. Innovation hubs across Japan and South Korea are establishing next-generation product lines based on solid-state and micro-battery architecture. A Japanese medical electronics company recently rolled out miniaturized batteries for wearable cardiac monitoring devices, improving runtime by 41% and accelerating adoption across 170,000 users. Consumer behavior indicates strong preference for portable, home-care, and tele-rehabilitation systems, contributing to sharply rising demand.

South America holds 5% of the Medical Machine Battery Market, led by Brazil and Argentina, where healthcare infrastructure investments and digital diagnostics adoption are rapidly increasing. Deployment of energy-efficient portable devices for rural and emergency care supports growth, along with government incentives for modernization of public hospitals. Regional manufacturers and distributors are expanding lithium-based supply channels across medical ventilators and infusion pumps. Battery-based imaging and patient monitoring equipment showed a 17% rise in procurement in 2024, reflecting shifting healthcare delivery models. Consumer behavior indicates growing preference for outpatient and home-treatment devices, supported by telemedicine expansion in urban centers.

Middle East & Africa account for 4% of the Medical Machine Battery Market, led by the UAE, Saudi Arabia, and South Africa. Healthcare digitalization programs and foreign partnerships are increasing demand for high-reliability power systems across emergency, diagnostic, and surgical equipment. Government-supported smart hospital projects and telehealth expansion stimulate procurement of long-cycle lithium packs and energy-efficient power modules. A leading UAE medical equipment supplier recently adopted smart BMS lithium units across 60 facilities, reducing device downtime by 24%. Consumer behavior shows growing prioritization of uninterrupted equipment availability, especially in critical care and remote-treatment environments.

• United States – 27% market share

High dominance due to large hospital automation deployments and extensive adoption of portable and home-care medical devices requiring continuous power solutions.

• China – 18% market share

Leadership supported by significant production capacity, rapidly expanding healthcare infrastructure, and strong demand for battery-powered diagnostic and monitoring technologies.

The Medical Machine Battery market is characterized by a moderately consolidated competitive structure, with approximately 30–35 active global manufacturers contributing to sustained product innovation and capacity expansion. The top five companies collectively account for around 47% of the global market share, supported by strong distribution networks and advanced battery engineering capabilities. Competitive intensity increased in 2023–2024 as over 18 new product variations focused on higher cycle life and compact form factors entered commercial adoption. Strategic activities have accelerated, with more than 20 partnerships recorded globally between OEMs and healthcare device manufacturers to streamline compatibility and regulatory approval processes. Lithium-ion battery chemistries dominate portfolio upgrades, with nearly 62% of new launches featuring enhanced energy density above 250 Wh/kg. Players are also prioritizing operational resilience and backward integration, with 28% of major manufacturers having invested in their own electrode material production facilities to reduce supply chain risks. Sustainability-driven strategies are shaping competition, where over 40% of companies have adopted recycling-enabled designs and low-cobalt formulations to align with environmental compliance standards. Pricing competitiveness continues to intensify, particularly in Asia-Pacific and North America, leading to increased focus on long-term supply agreements and value-added after-sales services for retention of medical OEM customers.

Panasonic Corporation

Samsung SDI

LG Energy Solution

Saft Batteries

BYD Company Ltd.

Philips Healthcare Energy Systems

EaglePicher Technologies

Ultralife Corporation

VARTA AG

Enersys

Hitachi Chemical Co.

Maxell Holdings Ltd.

In the Medical Machine Battery market, the current technological landscape is increasingly focused on high-energy density lithium-ion chemistries, with performance benchmarks now exceeding 250 Wh/kg in select modules designed for implantable and portable medical equipment. Manufacturers are leveraging advanced electrode materials—including nano-structured silicon anodes and high-nickel cathodes—to achieve up to 35 % greater cycle life and 28 % faster charge rates compared with legacy AGM or sealed lead-acid systems. Integration of smart Battery Management Systems (BMS) tailored for healthcare contexts enables real-time monitoring of battery health, predictive diagnostics, and thermal event protection, shortening critical maintenance windows by nearly 22 % in diagnostic device fleets.

Emerging technologies are shaping the next frontier: solid-state batteries, which replace liquid electrolytes with solid materials, are under development with prototypes reaching energy densities that are approximately 40 % higher than current commercial lithium-ion formats and demonstrating cycle stability allowing multiyear implantable device service. Concurrently, miniaturised micro-battery platforms for wearable and implantable systems are being developed with form-factors measuring mere millimetres and enabling sustained operation of biosensors for 15–20 hours between charges. Another breakthrough is the incorporation of AI-driven material discovery, where machine-learning-guided labs are compressing the development timeline for novel battery chemistries by an estimated 30 %.

Healthcare-specific demands such as ultra-low failure rates, long shelf life, and sterilisation compatibility are driving the inclusion of thermal-runaway mitigation technologies, such as intrinsic shutdown separators and embedded cell-level sensors that reduce heat propagation risk by up to 33 %. Moreover, modular battery architectures are increasingly adopted in hospital environments, enabling hot-swap functionality and reducing equipment downtime by more than 27 % across large hospital networks.

For decision-makers, the path ahead is clear: prioritise partners and suppliers who deliver proven battery platforms with documented safety records, modular design flexibility, and strong software-enabled management capabilities. Investments in next-generation chemistries must coincide with regulatory readiness and device-ecosystem compatibility to minimise time-to-market and maximise device uptime in demanding medical settings.

In 2023, Saft Batteries commissioned a new lithium-ion production line at its Jacksonville, Florida facility to support expansion of high-performance battery modules used in critical medical power systems, enabling increased capacity for hospital-grade power support. (saft.com)

In July 2024, Panasonic Energy Co., Ltd. launched a high-capacity lithium-ion battery variant specially designed for implantable medical devices, delivering a thinner form-factor with higher cycle stability and enabling device makers to reduce pack volume by over 15 %. (SNS Insider)

In October 2023, VARTA AG announced strategic expansion of its medical-battery research facility to incorporate next-generation solid-electrolyte modules, targeting prototype deployment in surgical-robotics power systems in early 2025 and improving charge retention by about 32 %.

In 2023, EaglePicher Technologies entered into a partnership with a major medical-device OEM to supply custom battery packs for remote monitoring systems, enabling runtime extension of devices by up to 20 % and aligning with growing telehealth deployment in North American home-care settings.

This report provides a comprehensive evaluation of the Medical Machine Battery market, spanning segmentation by battery type (including lithium-ion, nickel-metal hydride, zinc-air, solid-state), by application (such as critical-care life-support devices, diagnostic imaging equipment, wearable health monitoring devices, surgical-robotics platforms), and by end-user (hospitals, clinics, home-care settings, ambulatory surgical centres). Geographically, the analysis covers key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, dissecting adoption patterns, regulatory frameworks, infrastructure maturity, and manufacturing capacity per region. The report also addresses technology-specific focus areas—thermal-safe battery systems, modular hot-swappable architectures, AI-enabled battery health analytics, and micro-battery platforms for mobile and implantable use—highlighting how innovation intersects with commercial deployment. Niche segments such as remote-patient care battery systems, tele-rehabilitation device batteries, and hospital automation power modules are included to reflect emerging opportunities. For decision-makers, the report outlines competitive dynamics, product-pipeline comparisons, strategic initiatives (R&D programmes, joint ventures, capacity expansions) and benchmark performance metrics across market participants. It serves as a reference for supply-chain planning, investment prioritisation, technology selection and growth strategy formulation within the medical power-solutions domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2220.7995 Million |

|

Market Revenue in 2032 |

USD 2924.36 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Panasonic Corporation, Samsung SDI, LG Energy Solution, Saft Batteries, BYD Company Ltd., Philips Healthcare Energy Systems, EaglePicher Technologies, Ultralife Corporation, VARTA AG, Enersys, Hitachi Chemical Co., Maxell Holdings Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |