Reports

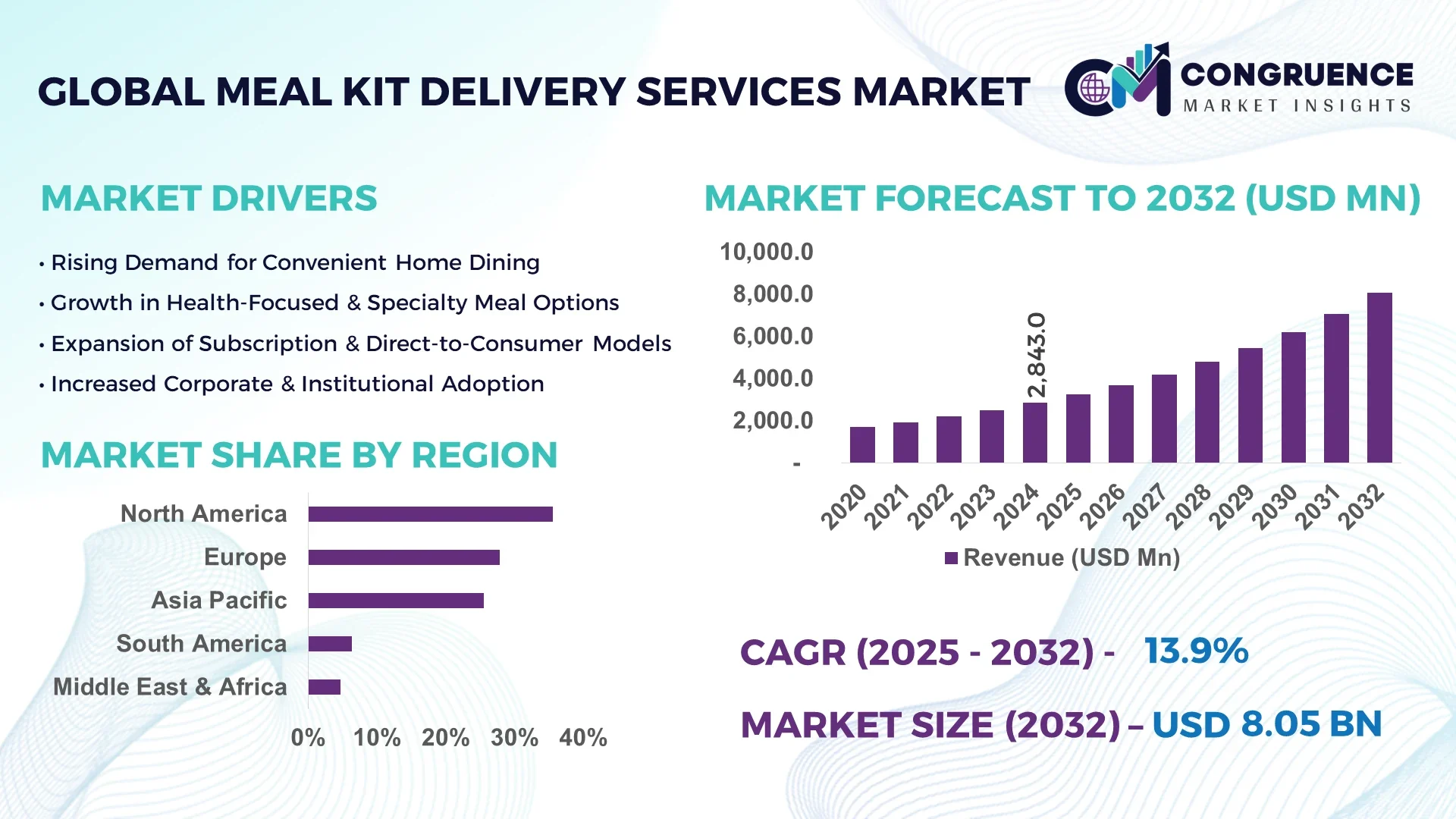

The Global Meal Kit Delivery Services Market was valued at USD 2,843.0 Million in 2024 and is anticipated to reach a value of USD 8,053.2 Million by 2032 expanding at a CAGR of 13.94% between 2025 and 2032.

In the United States, the Meal Kit Delivery Services Market benefits from substantial investments in cold‑chain logistics infrastructure, advanced last‑mile delivery networks, and powerful tech integration with predictive planning systems. Leading providers maintain high order volumes and scalable production capacity across multiple fulfillment centers, with strong focus on mobile app innovation, dietary personalization engines, and seamless subscription management workflows.

The Meal Kit Delivery Services Market spans key industry sectors such as health‑conscious consumer segments, corporate employee meal programs, and premium hospitality partnerships. Service‑type segmentation includes ready‑to‑cook and ready‑to‑eat delivery models with “cook & eat” options commanding higher utilization. Product innovations such as AI‑driven menu personalization, eco‑packaging solutions, and mobile planning tools are shaping service offerings. Regulatory and environmental drivers include stringent food safety standards, packaging waste mandates, and sustainability labeling requirements. Regional consumption patterns show high maturity in North America and Europe, while rapid urbanization and rising disposable income are fueling demand in Asia‑Pacific. Economic factors such as increasing digital purchasing and convenience preference are accelerating adoption. Emerging trends include meal kits integrated with wearable‑based nutritional feedback, on‑demand customizable plans, and partnerships with fitness and nutrition platforms, positioning the market for continued expansion through 2032.

Artificial Intelligence (AI) is redefining the efficiency, personalization, and operational precision within the Meal Kit Delivery Services Market. AI-enabled forecasting tools accurately predict demand by analyzing subscription patterns, reducing food waste and optimizing inventory levels. Providers report up to 30% improvement in demand-planning accuracy, minimizing surplus or shortage scenarios. Intelligent menu engines customize meal options based on dietary goals, prior orders, and flavor preferences, increasing customer retention while enhancing satisfaction. AI‑based logistics solutions optimize delivery routes, reducing last‑mile delivery times by up to 25% in urban zones. Meanwhile, packaging calculators powered by predictive analytics adjust insulation materials based on weather forecasts and shipment dimensions, improving on‑time delivery reliability and product freshness.

Within the Meal Kit Delivery Services Market, AI‑enhanced chatbots and customer service interfaces triage queries and address cancellations or substitutions 24/7, easing support loads and accelerating response resolution. Smart kitchen integrations allow seamless compatibility between recipe steps and voice assistants, offering a frictionless cooking experience. Furthermore, AI tools analyze feedback and rating trends to inform future menu planning and supplier sourcing strategy. These AI implementations contribute to operational cost reduction, elevated customer engagement, and streamlined workflow execution—elevating the strategic value of providers within the competitive Meal Kit Delivery Services Market.

“In mid‑2024, a leading meal kit provider deployed an AI logistics module that reduced delivery delays by 22% and increased weekly customer retention by 14% within three months of implementation.”

The Meal Kit Delivery Services Market dynamics are shaped by evolving consumer lifestyles, digital-first ordering trends, and a heightened focus on health and convenience. As time‑pressed consumers seek fresh, ready‑to‑cook options, providers are enhancing offerings with flexible bundle sizes, allergen-free recipes, and globally inspired menus. The integration of subscription models enables predictable recurring revenue and customer engagement through loyalty rewards and tailored meal plans. Supply partnerships with local farms and food brands are strengthening seasonal variety and ingredient transparency. New entrants are targeting niche segments such as vegan, keto, or family‑size meal kits. Competitive pressure encourages continuous innovation in packaging to meet sustainability mandates—like compostable materials and minimal-waste designs. Delivery model innovations include scheduled micro‑fulfillment centers, chilled lockers, and drone or e‑bike options in urban zones. The dynamics reflect a market responding to consumer needs via operational efficiency, customization, and environmental responsibility.

Consumer trends show strong preference for meal kits tailored to dietary needs—such as keto, vegan, gluten‑free, or low‑sugar plans. Providers offering customizable meal choices see higher engagement; for instance, platforms with high‑profile dietary filters often report a 40% increase in repeat subscriptions. Health-focused consumers are willing to pay premiums for balanced, portion-controlled, and nutrition-labeled kits, driving providers to expand such menu options and optimize ingredient sourcing to support wellness-oriented adoption.

Providers face logistical hurdles in managing perishable ingredients across seasons. Weather disruptions and variable harvest yields lead to packaging adjustments, restocking delays, and increased spoilage. Some providers report up to 12% weekly variance in inventory mismatch rates, leading to order adjustments or cancellations. Maintaining consistent quality and routing control across regions requires robust cold‑chain systems and contingency planning, elevating operational costs and complexity.

Expansion into corporate wellness and employee meal stipends presents unexploited opportunity in the Meal Kit Delivery Services Market. Companies are integrating meal kits into corporate benefits, boosting bulk order volumes and consistent demand. Partnerships with fitness, dietician, and healthcare platforms enable branded co‑developed kits, while bundling subscription services with employers and schools unlocks multi‑site deployment potential. Some corporate programs report up to 25% higher customer lifetime value compared to B2C channels.

Competitive pricing in densely populated markets is pressuring margins, especially with entry of value-based players offering simplified menus. Customer churn remains a challenge, as average retention intervals often dip below 6 months in absence of novelty. Providers must continually innovate menu diversity, loyalty incentives, and referral programs to maintain engagement. Additionally, rising shipping costs and health safety compliance add to pricing strain, demanding refined cost management and operational scaling strategies.

Growth of Ready‑to‑Eat (Heat‑and‑Serve) Subscriptions: Demand for fully prepared, heat-and-serve options is rising sharply, especially among urban professionals. Providers offering these kits report up to 35% higher week‑on‑week enrollment rates. These meals reduce prep time and deliver immediate convenience, making them ideal for time-constrained consumers seeking minimal-cook solutions.

Surge in AI‑Enabled Meal Personalization Tools: Advanced recommendation engines analyze customer eating patterns and dietary inputs to generate weekly menus tailored to individual tastes. In pilot programs, average upsell rate of add-on items increased by 28% when personalized options were presented via AI‑suggested selections.

Expansion of Eco‑Packaging and Sustainability Claims: Meal kit suppliers are increasingly adopting compostable containers, recyclable insulation liners, and renewable paper wraps. Some providers estimate a 20–22% reduction in packaging weight per box year-over-year, supporting both brand ESG goals and lower logistics costs.

Integration with Health and Fitness Platforms: Meal kit services partnering with fitness apps or wearable health devices deliver personalized nutrition plans tied to activity levels or biometric data. These strategic alliances have boosted cross-channel engagement by up to 18%, especially among health-conscious consumer segments.

The Global Meal Kit Delivery Services Market is segmented based on type, application, and end-user, reflecting the industry's evolving dynamics and consumer demands. Type segmentation includes ready-to-cook and ready-to-eat offerings, catering to varying levels of cooking involvement and convenience expectations. Applications span diverse use cases such as health-focused meal plans, time-saving weekday solutions, and family-oriented nutrition support. End-users range from individual households and working professionals to corporate wellness programs and hospitality service providers. This segmentation highlights how different consumer profiles and consumption behaviors influence the delivery model, packaging format, and subscription strategy. Notably, the rise in health awareness and increasing demand for dietary customization are shifting growth toward highly personalized kits. Each segment plays a critical role in shaping innovation, logistics planning, and digital engagement strategies for providers. As meal kits evolve into multifunctional solutions bridging nutrition, convenience, and sustainability, segmentation remains key to targeting and scaling effectively within a competitive landscape.

In terms of type, ready-to-cook meal kits dominate the market due to their blend of fresh ingredients and guided cooking instructions, which appeal to consumers seeking home-cooked quality with reduced meal prep time. These kits offer a balanced experience for health-conscious individuals who value culinary involvement but lack time for grocery shopping and meal planning. The consistency and customization of these kits contribute to their widespread adoption across urban households.

Ready-to-eat meal kits are the fastest-growing segment, driven by increasing demand from professionals, students, and the elderly who prioritize convenience. This format eliminates the need for preparation and offers instant consumption, making it ideal for busy lifestyles and single-person households. Providers have enhanced their ready-to-eat offerings by improving shelf stability, expanding cuisine variety, and ensuring premium taste, thereby increasing consumer retention.

Other types, such as hybrid models and gourmet meal kits, serve niche demographics. Hybrid kits that allow for optional cooking customization are gaining attention, while gourmet kits appeal to consumers seeking fine-dining experiences at home. Though these subtypes occupy smaller shares, they offer high-margin potential and brand differentiation opportunities.

Meal kit services are predominantly used for daily meal planning, especially among dual-income households seeking structured, nutritious, and time-efficient meal options. The predictability of pre-portioned meals and nutritional transparency supports weekly planning while reducing food waste. This application leads due to its broad relevance across demographics, including health-conscious individuals and families with school-age children.

The health and wellness segment is experiencing the fastest growth, with demand driven by the rising popularity of diets like keto, vegan, and gluten-free. Consumers are increasingly choosing kits that align with personal fitness goals, allergy restrictions, and sustainable lifestyles. Providers now offer biometric-integrated meal plans and app-based nutrition tracking to serve this growing user base.

Other notable applications include special occasions, such as holiday meals or gourmet-themed dinners, and trial kits for first-time users. While their frequency is lower, these segments help onboard new customers and introduce premium features, expanding market exposure and creating upsell opportunities across broader applications.

The dominant end-user group in the meal kit market is individual consumers, particularly working professionals and young couples in metropolitan areas. Their preference for planned, home-cooked meals without grocery hassles aligns perfectly with the value proposition of meal kits. High digital literacy and openness to subscription services among this group make them the primary target for most brands.

Corporate clients and wellness program providers are emerging as the fastest-growing end-user segment. Organizations are incorporating meal kit subscriptions into employee wellness packages to promote better nutrition and work-life balance. This trend is particularly strong in urban centers and tech-driven industries, where employee satisfaction is closely tied to personalized lifestyle benefits.

Other contributing end-users include elderly populations, who value the ease and nutrition of meal kits tailored for dietary needs, and hospitality partners, such as boutique hotels and serviced apartments, using meal kits to offer unique in-room dining experiences. These niche segments add diversity to the market and support tailored service innovation.

North America accounted for the largest market share at 35.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2025 and 2032.

The Global Meal Kit Delivery Services Market continues to witness diverse growth trajectories across regions due to varying consumer preferences, digital infrastructure maturity, urbanization rates, and dietary patterns. North America’s strong lead stems from established e-commerce networks, early adoption of subscription models, and high disposable income. In contrast, Asia-Pacific’s rapid urbanization, growing middle class, and digital transformation initiatives are accelerating demand. Europe follows closely with its strong sustainability mandates and rising health-conscious population. Emerging economies in South America and the Middle East & Africa are increasingly investing in smart logistics and cold chain systems, positioning themselves for gradual expansion. Regional market dynamics are further shaped by public policy, cross-border e-commerce capabilities, and culturally specific meal preferences, influencing the overall competitive landscape.

North America captured a significant 35.6% share of the Meal Kit Delivery Services Market in 2024, driven by widespread demand in the United States and Canada. High adoption among time-constrained professionals, millennials, and dual-income families has reinforced the region's leadership. Key industries such as health and wellness, e-commerce logistics, and personalized nutrition solutions are fueling sustained demand. Regulatory support promoting food safety labeling and packaging transparency has further supported consumer trust. The region has also seen the rise of AI-powered dietary personalization, app-based reordering systems, and automated supply chain integrations. North America’s mature internet penetration and high mobile device usage make it a digital-first hub for subscription-based meal kits, with leading players investing in same-day delivery, AI-driven inventory systems, and sustainable packaging innovations to retain consumer loyalty.

Europe held an estimated 27.8% of the Meal Kit Delivery Services Market in 2024, with the United Kingdom, Germany, and France being key contributors. The region benefits from a strong culture of home-cooked meals, heightened awareness around sustainable consumption, and active regulatory frameworks. Regulatory bodies such as the European Food Safety Authority (EFSA) promote strict packaging and labeling guidelines, fostering transparency. Government-backed sustainability initiatives, such as food waste reduction and carbon-neutral delivery incentives, are gaining traction. Additionally, the integration of digital technologies like blockchain for traceability and AI for meal recommendation engines is transforming consumer experiences. Europe's focus on organic and locally sourced ingredients is driving innovation in meal kit content and sourcing, especially among health-conscious and environmentally aware consumers.

Asia-Pacific is rapidly gaining momentum in the Meal Kit Delivery Services Market and is projected to be the fastest-growing region by 2032. In 2024, countries such as China, India, and Japan accounted for the majority of regional consumption, supported by expanding urban middle-class populations and an increasing preference for convenient, nutritious meals. Rising awareness around healthy eating habits and the influence of Western lifestyles are reshaping eating patterns. Infrastructure developments, such as last-mile cold chain delivery systems and cloud kitchens, are enabling scale. Technological innovations—particularly app-based ordering platforms and AI-enabled dietary tracking tools—are driving user acquisition and retention. Innovation hubs in Singapore, Seoul, and Bengaluru are spearheading smart logistics and nutritional analytics, strengthening the digital backbone of the meal kit economy in the region.

South America’s Meal Kit Delivery Services Market is led by Brazil and Argentina, contributing to a regional market share of approximately 6.4% in 2024. Evolving urban consumption patterns and increased awareness around health and dietary planning are reshaping traditional food preparation habits. While infrastructure limitations had previously hindered growth, recent improvements in e-commerce logistics and cold storage chains have begun to unlock new market potential. Government policies encouraging entrepreneurship in food-tech and dietary health campaigns have created opportunities for local and international players. The rise of mobile-first consumer engagement, especially in metro areas, is helping providers penetrate deeper into the market with app-based subscriptions and regionalized meal options.

The Middle East & Africa region holds a modest yet growing portion of the Meal Kit Delivery Services Market, estimated at 4.7% in 2024. Countries such as UAE and South Africa are at the forefront of market development due to high urbanization, increasing disposable incomes, and the popularity of Western dietary trends. The demand is largely concentrated in metropolitan areas where consumers seek convenient, time-saving food options aligned with fitness goals and nutritional needs. Regional governments are supporting local startups with food-tech incubators and trade-friendly policies. Technological modernization—particularly in logistics automation, app integration, and multilingual interfaces—is facilitating greater accessibility. The region also shows potential in hospitality-driven meal kit offerings tied to tourism, with eco-conscious and halal-certified options becoming increasingly prominent.

United States - 32.4% Market Share

High subscription penetration and advanced e-commerce infrastructure

China - 16.8% Market Share

Rapid digital adoption and strong urban consumer base for convenience-based food solutio

The Global Meal Kit Delivery Services Market is characterized by a moderately fragmented competitive landscape, with over 40 prominent players actively operating across regional and global levels. Companies in this space are competing primarily on innovation, geographic reach, price differentiation, and subscription customization. Strategic initiatives such as partnerships with grocery chains, direct-to-consumer expansions, and eco-friendly packaging rollouts have become central to gaining a competitive edge. Notably, firms are increasingly investing in AI-based menu planning, logistics automation, and customer analytics to enhance service efficiency and user experience.

Mergers and acquisitions are common, as larger companies aim to consolidate their market position by acquiring niche players or regional brands with strong local followings. Competitive intensity is particularly high in North America and Europe, where mature players dominate, while newer entrants are exploring underserved markets in Asia-Pacific and Latin America. Innovation trends such as sustainable packaging, dietary personalization, and integration with wearable health tech are shaping competitive dynamics, pushing companies to continuously evolve. The presence of tech-savvy consumers is further accelerating the race for differentiation in user experience, nutritional quality, and same-day delivery capabilities.

HelloFresh SE

Blue Apron Holdings, Inc.

Sun Basket, Inc.

Freshly Inc.

Marley Spoon AG

Gousto Ltd.

Dinnerly

Home Chef

Purple Carrot

Cook it Inc.

EveryPlate

Green Chef Corporation

Mindful Chef Ltd.

Factor75 LLC

Technology plays a pivotal role in shaping the evolution of the Meal Kit Delivery Services Market. One of the most significant innovations is AI-driven meal customization, enabling providers to analyze user preferences, dietary restrictions, and ordering history to tailor personalized meal plans. These intelligent systems enhance user satisfaction and retention while minimizing food waste.

Machine learning algorithms are being utilized to forecast demand more accurately and optimize inventory management, resulting in improved operational efficiency. Additionally, real-time delivery tracking and route optimization powered by GPS and telematics are improving last-mile logistics, which is essential for maintaining food freshness.

Sustainability is another area benefiting from technological advancement. Many companies are integrating biodegradable and recyclable packaging solutions, often guided by software that calculates optimal packing configurations to reduce material usage. Cloud kitchens, which rely on IoT-enabled smart kitchen tools, are also emerging as a low-overhead alternative for regional fulfillment.

Moreover, the use of blockchain for supply chain transparency is gaining traction, allowing consumers to trace ingredient origins and quality in real-time. Integration with mobile apps and smart devices such as wearables and virtual assistants is deepening user engagement through automated reorder functions and health-tracking features. These advancements collectively enhance convenience, sustainability, and personalization—cornerstones of the modern meal kit delivery experience.

• In March 2024, HelloFresh launched a new AI-powered menu personalization engine, allowing customers to receive real-time meal suggestions based on past orders and dietary preferences, increasing retention rates by 18% in pilot markets.

• In September 2023, Gousto opened its second automated fulfillment center in the UK, doubling its order processing capacity and reducing packaging time per kit by 40%.

• In January 2024, Marley Spoon introduced fully compostable insulation materials in its packaging, reducing single-use plastic usage by approximately 65% across its European operations.

• In November 2023, Sun Basket partnered with a major wearable fitness tracker brand to offer nutrition-based meal kits integrated with real-time activity and health data tracking.

The Meal Kit Delivery Services Market Report offers a comprehensive analysis of the global landscape, covering a wide spectrum of key market parameters. The report includes detailed segmentation by type (Ready-to-Eat, Reheat & Eat, Cook It Yourself), application (Health & Wellness, Weight Loss, General Household Use), and end-users (Individuals, Households, Enterprises). It further explores regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting distinct growth patterns and strategic developments.

The report focuses on emerging technologies such as AI-powered personalization, blockchain-enabled supply chain transparency, sustainable packaging materials, and smart kitchen integration. It identifies niche and high-growth areas such as vegan meal kits, elderly-focused meal plans, and child-specific dietary kits, reflecting diversification within the product ecosystem.

Additionally, the report analyzes market entry barriers, consumer behavior trends, digital transformation impacts, and competitive strategies employed by leading players. Through an in-depth understanding of innovation trends, operational challenges, and strategic investments, the report provides actionable insights for stakeholders, decision-makers, and investors looking to capitalize on opportunities in this rapidly evolving sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,843.0 Million |

| Market Revenue (2032) | USD 8,053.2 Million |

| CAGR (2025–2032) | 13.94 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | HelloFresh SE, Blue Apron Holdings, Inc., Sun Basket, Inc., Freshly Inc., Marley Spoon AG, Gousto Ltd., Dinnerly, Home Chef, Purple Carrot, Cook it Inc., EveryPlate, Green Chef Corporation, Mindful Chef Ltd., Factor75 LLC |

| Customization & Pricing | Available on Request (10 % Customization is Free) |