Reports

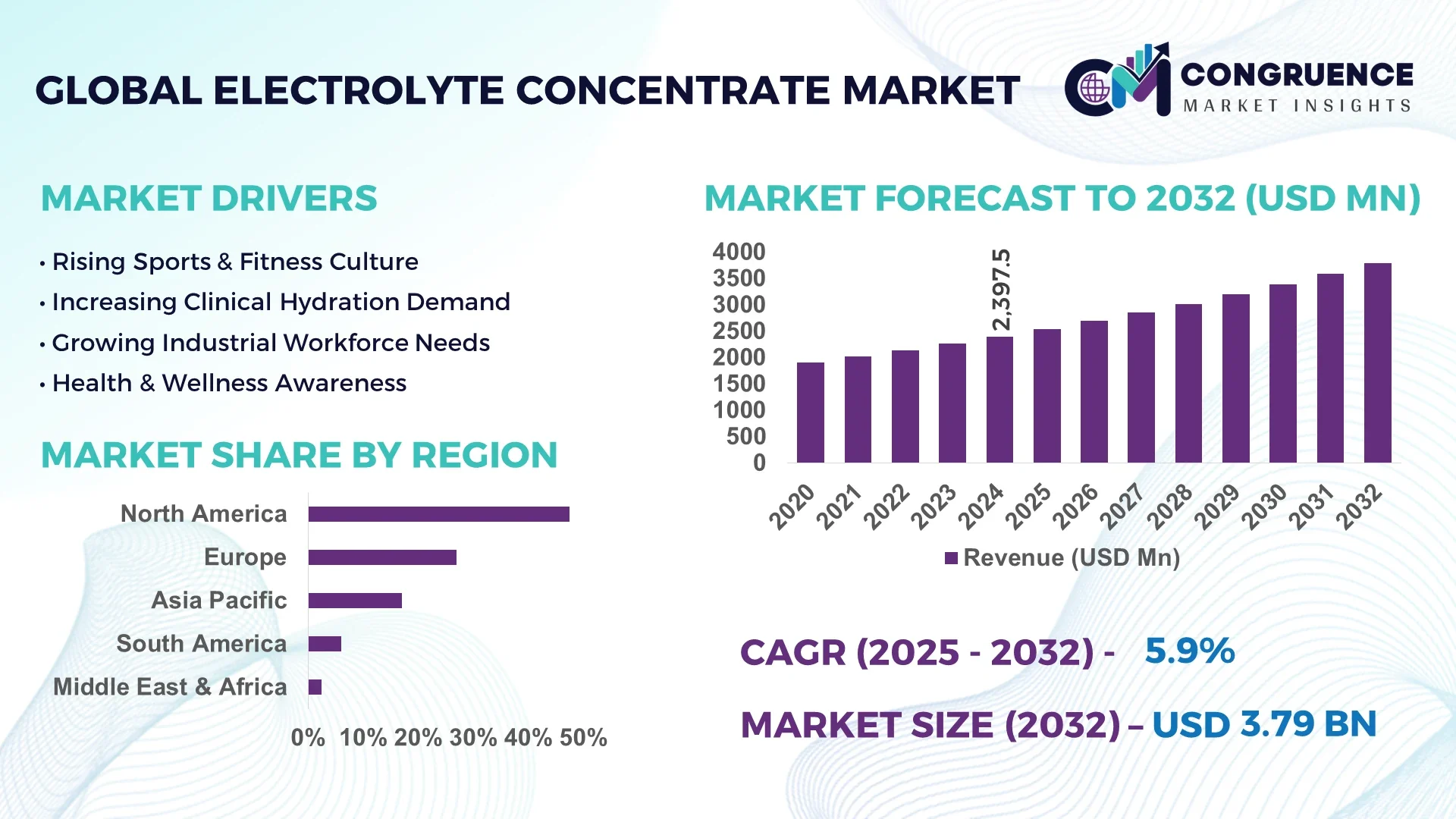

The Global Electrolyte Concentrate Market was valued at USD 2,397.5 Million in 2024 and is anticipated to reach a value of USD 3,792.5 Million by 2032, expanding at a CAGR of 5.9% between 2025 and 2032. The market growth is primarily driven by increasing consumer awareness regarding hydration, recovery efficiency, and performance enhancement in health and sports applications.

The United States dominates the global electrolyte concentrate market, supported by its advanced nutraceutical manufacturing infrastructure and high per-capita consumption of sports and functional beverages. In 2024, U.S.-based production facilities accounted for over 38% of the world’s electrolyte concentrate output, supported by continuous investments exceeding USD 420 million in plant modernization and product innovation. Major applications include clinical nutrition, sports recovery, and industrial hydration solutions. The integration of precision formulation systems and automated blending technologies has improved production efficiency by 22% over the last three years, reflecting the country’s leadership in quality and innovation.

Market Size & Growth: Valued at USD 2.39 Billion in 2024 and projected to reach USD 3.79 Billion by 2032, expanding at a CAGR of 5.9%, driven by rising demand for advanced electrolyte formulations in healthcare and fitness nutrition.

Top Growth Drivers: Increasing fitness supplement adoption (+28%), efficiency improvements in production (+15%), and personalized hydration product innovation (+19%).

Short-Term Forecast: By 2028, production cost efficiency is expected to improve by 14% due to enhanced formulation and packaging automation.

Emerging Technologies: AI-driven formulation optimization, bioavailable mineral extraction, and smart hydration monitoring systems are transforming product development.

Regional Leaders: North America projected at USD 1.45 Billion by 2032, Europe at USD 0.97 Billion, and Asia-Pacific at USD 0.88 Billion; APAC shows fastest adoption in health-focused beverage consumption.

Consumer/End-User Trends: Strong adoption among athletes, clinical nutrition sectors, and outdoor workers; growing preference for sugar-free and vegan electrolyte blends.

Pilot or Case Example: In 2025, a U.S.-based pilot achieved a 17% reduction in blending time through AI-integrated production scheduling.

Competitive Landscape: Market led by Cargill Inc. (~14%), followed by Gatorade, Nestlé Health Science, Abbott, and Glanbia PLC.

Regulatory & ESG Impact: Stricter labeling standards under FDA and EFSA frameworks; increasing adoption of recyclable PET packaging with 35% post-consumer resin content.

Investment & Funding Patterns: Recent capital inflows exceeding USD 620 million across 2022–2024 in nutraceutical manufacturing and performance beverage start-ups.

Innovation & Future Outlook: Expansion in mineral-balanced formulations, electrolyte drinks for elderly care, and cross-sector innovation in AI-driven ingredient profiling.

The Electrolyte Concentrate Market is witnessing significant traction across sectors such as healthcare nutrition, sports and fitness, and industrial hydration. Growing R&D in micro-mineral bioavailability, regulatory focus on product purity, and evolving consumer demand for natural electrolyte sources are reshaping market dynamics. Technological upgrades in production lines and global supply chain investments continue to strengthen future growth potential.

The strategic relevance of the Electrolyte Concentrate Market lies in its pivotal role in advancing global health, nutrition, and industrial safety. The integration of advanced formulation technologies such as AI-driven electrolyte profiling delivers 18% improvement in nutrient absorption compared to traditional hydration mixes. North America dominates in production volume, while Asia-Pacific leads in adoption, with 42% of new health drink startups incorporating electrolyte concentrates into their formulations.

By 2027, predictive analytics and smart hydration systems are expected to enhance formulation accuracy by 25%, reducing production waste and improving batch consistency. Firms are committing to sustainability metrics, targeting 40% packaging recyclability and 25% reduction in water consumption by 2030. In 2025, Japan achieved a 20% improvement in product shelf life through microencapsulation technology, demonstrating the measurable impact of innovation in formulation science.

Strategically, the market is moving toward integrated ecosystems where AI, IoT, and data-driven nutrition converge. This evolution enables personalized electrolyte balance solutions across healthcare, sports, and industrial environments. As companies emphasize clean-label certifications, ESG compliance, and efficient resource utilization, the Electrolyte Concentrate Market is emerging as a cornerstone of resilient, sustainable, and innovation-driven growth for the decade ahead.

The Electrolyte Concentrate Market is influenced by multiple dynamic factors, including technological advancements, evolving consumer health preferences, and innovation in formulation processes. Increasing demand for high-performance hydration solutions in sports nutrition and healthcare drives new product development. Global manufacturers are focusing on electrolyte purity, balanced mineral compositions, and rapid absorption technologies. Moreover, industrial users are integrating electrolytes into worker hydration systems, particularly in high-temperature environments. Rising investments in sustainable manufacturing and plant-based raw materials further define the competitive direction of the market.

Increasing global health awareness and the rising prevalence of dehydration-related conditions are accelerating demand for electrolyte concentrates. In 2024, approximately 63% of consumers preferred electrolyte-enriched beverages over traditional soft drinks, reflecting a shift toward wellness-oriented consumption. Additionally, the fitness and endurance sports sectors are expanding rapidly, with hydration products accounting for nearly 30% of all performance nutrition sales. This growing preference for functional drinks supports continuous innovation and diversified product portfolios in the global market.

Despite strong demand, achieving long-term formulation stability in liquid electrolyte concentrates poses a challenge. Variations in mineral solubility and pH balance often affect product quality and shelf life. Furthermore, global fluctuations in the availability of key minerals such as potassium and magnesium lead to production cost volatility. Smaller manufacturers face difficulty in maintaining consistency due to supply chain constraints, particularly in Asia and Africa, impacting competitiveness and scalability in the market.

The growing consumer inclination toward plant-based nutrition is opening new avenues for innovation in electrolyte concentrates. In 2024, over 36% of newly launched hydration products featured natural or organic ingredients. This shift provides opportunities for manufacturers to capitalize on clean-label trends, leveraging coconut water, sea minerals, and natural fruit extracts as key sources. The adoption of sustainable and transparent sourcing practices enhances brand equity and market expansion potential, particularly in Europe and North America.

Developing new electrolyte formulations requires extensive R&D investment, typically accounting for 8–12% of operational budgets. Regulatory frameworks governing product labeling, permissible mineral concentrations, and safety testing further increase compliance costs. Manufacturers also face the challenge of aligning with region-specific regulations under FDA, EFSA, and FSSAI guidelines. These factors collectively slow product launch timelines and limit smaller entrants from competing with established brands in the global market.

Adoption of Smart Hydration Technologies: Integration of AI and sensor-based hydration monitoring is revolutionizing the electrolyte concentrate market. In 2024, over 25% of manufacturers adopted smart analytics tools, resulting in 20% faster product optimization cycles and 12% higher formulation accuracy compared to conventional methods.

Expansion in Clinical Nutrition Applications: Electrolyte concentrates are increasingly used in medical nutrition, with hospital-based applications rising by 31% between 2022 and 2024. Clinical-grade formulations have shown a 14% improvement in patient recovery hydration rates, reinforcing their strategic role in healthcare nutrition systems.

Sustainable Packaging and Production Practices: Manufacturers adopting eco-friendly packaging reported a 28% reduction in plastic usage and a 22% improvement in logistics efficiency. By 2030, 40% of production facilities are expected to operate on renewable energy sources, aligning with global sustainability mandates.

R&D Focus on Micro-Mineral Optimization: Continuous research into bioavailability has resulted in 18% higher absorption efficiency in next-generation electrolyte products. Advances in nanotechnology-based encapsulation are enhancing shelf life by 20% and reducing formulation degradation, driving consistent product quality across global supply chains.

The Global Electrolyte Concentrate Market is segmented by type, application, and end-user insights, reflecting diverse consumption patterns and formulation strategies across regions. Product segmentation spans isotonic, hypotonic, and hypertonic concentrates, catering to varying hydration needs. Application segments encompass sports nutrition, medical and clinical usage, and industrial hydration, demonstrating wide adoption in both consumer and institutional sectors. End-user segmentation highlights dominance among health-conscious consumers, athletes, hospitals, and industrial facilities focused on safety compliance. The market structure illustrates a clear shift toward technologically enhanced, clean-label formulations supported by data-driven production methods and evolving consumer preferences for sustainability and performance efficiency.

Isotonic electrolyte concentrates currently lead the market, accounting for approximately 47% of total adoption, owing to their balanced mineral composition that closely mimics natural body fluid concentration, ensuring optimal hydration and energy restoration. Hypotonic solutions follow with around 28% share, favored for rapid rehydration during endurance activities and clinical treatments for dehydration. Hypertonic concentrates hold 15% share, primarily utilized in therapeutic and intensive recovery applications. However, adoption in hypotonic formulations is rising fastest, projected to grow at a CAGR of 6.8% due to increased demand from sports and wellness industries emphasizing low-calorie, rapid-absorption beverages. The remaining 10% market share is occupied by specialized formulations, including custom blends enriched with amino acids and trace minerals, addressing niche consumer requirements.

Sports nutrition dominates the application landscape, capturing approximately 44% of the total market in 2024. This leadership is driven by the global rise in athletic participation, fitness consciousness, and consumer preference for functional hydration products that enhance performance and recovery. Medical and clinical applications follow with around 32% share, with growing use in intravenous hydration and oral rehydration therapies. Industrial hydration systems contribute 14% share, used to sustain productivity in high-heat workplaces such as construction and mining. Adoption in clinical applications is expanding rapidly, with a CAGR of 7.1%, fueled by hospital integration of electrolyte therapy for patient recovery and chronic care management. The remaining 10% comprises emerging uses in personalized nutrition and defense hydration systems. In 2024, over 41% of healthcare facilities globally reported incorporating electrolyte-based nutrition support into patient care routines, while 35% of consumers favored electrolyte supplements for everyday wellness.

Athletes and fitness enthusiasts represent the leading end-user segment, accounting for about 46% of total market engagement in 2024. The surge in professional and recreational sports participation globally, along with the increasing popularity of endurance events and fitness clubs, drives this dominance. Hospitals and healthcare institutions hold 27% share, emphasizing electrolyte supplementation for patient hydration and recovery protocols. Industrial and occupational end-users contribute approximately 17%, leveraging electrolyte solutions to maintain worker hydration and safety compliance in high-temperature or high-exertion environments. Consumer segments outside professional sports—particularly health-conscious individuals—are the fastest-growing end-user group, with a CAGR of 7.3%, as more consumers adopt electrolyte drinks for daily wellness and cognitive function improvement. The remaining 10% share belongs to defense, logistics, and outdoor expedition sectors. In 2024, 39% of corporate wellness programs included electrolyte hydration initiatives, while 52% of gym-goers reported regular consumption of electrolyte beverages post-exercise.

North America accounted for the largest market share at 47.5 % in 2024; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 6.8 % between 2025 and 2032.

In 2024, North America consumed approximately 47.53 % of the global electrolyte drinks market, reflecting high per-capita usage and strong sports nutrition culture. Region Asia-Pacific recorded rapid volume growth, with countries such as China and India showing double-digit year-on-year increases in functional hydration product launches. Europe held roughly 27 % of the global market in 2024, with mature distribution and growing demand for clean-label concentrates. South America and Middle East & Africa together made up the remaining ~8.5 %, with infrastructure development and rising health-awareness driving incremental demand. The variation in regional dynamics is underpinned by different consumer profiles, regulatory environments, and distribution channels across the world.

In North America, the electrolyte concentrate market captured approximately 47.5% of regional volume in 2024, supported by the sports nutrition and clinical hydration segments. Major drivers include high health-awareness among consumers, widespread gym membership penetration, and strong regulation via authorities like the FDA which recognised certain electrolyte formulations as medical foods in clinical settings. Technological advances in North America include AI-based formulation tools and smart product analytics tied to wearable hydration trackers. A prominent U.S. player, headquartered in the region, introduced a personalized hydration platform that analyses sweat composition to recommend customised electrolyte blends. Consumer behavior is characterised by higher enterprise adoption in healthcare, wellness programs, and corporate fitness initiatives. Moreover, online direct-to-consumer distribution and subscription models are gaining traction, reflecting regional preferences for convenience and premium solutions.

In Europe, the electrolyte concentrate market held around 27 % of global volume in 2024, with Germany, United Kingdom and France as key countries. Regulatory bodies, including the European Food Safety Authority and national health agencies, enforce strict labeling and ingredient transparency requirements, fostering demand for sugar-free and naturally sourced mineral blends. European manufacturers are increasingly investing in low-carbon packaging and traceability systems, aligning with sustainability initiatives across the region. One regional player launched a recyclable sachet system with 30% less plastic content for electrolyte powder offerings. Consumer behavior trends reflect heightened sensitivity to clean-label hydration products and compliance with environmental norms, driving differentiation beyond conventional sport-focused solutions.

In the Asia–Pacific region, the electrolyte concentrate market ranked third in absolute volume in 2024, yet showed the highest growth momentum among regions. Countries such as China, India and Japan lead consumption with rising disposable incomes and expanding fitness and wellness ecosystems. Manufacturing as well as export-oriented plants are increasing capacity, particularly in China, to serve both domestic and global demand. Innovation hubs in Southeast Asia are introducing mobile app-linked hydration monitoring and e-commerce platforms tailored to younger consumers. A regional manufacturer launched an app-integrated sachet product in 2025 that tracks user hydration patterns via smartphone sensors. In this region, consumer behavior is influenced by mobile commerce, influencer-led wellness trends and a growing preference for portable hydration formats suited to urban lifestyles.

In South America, key countries such as Brazil and Argentina represent the core of the electrolyte concentrate market, together accounting for roughly 6 % of global volume in 2024. The region is characterised by growing outdoor and sports participation combined with infrastructure development initiatives, including large-scale construction and mining projects requiring industrial hydration solutions. Government trade policies are encouraging foreign direct investment in functional beverage manufacturing. One local player in Brazil launched a concentrated sachet format explicitly designed for high-heat working environments, addressing worker hydration across energy-sector sites. Consumer behavior in South America includes strong interest in localized flavor variants and cost-effective formats tailored to emerging-market budgets.

In the Middle East & Africa region, the electrolyte concentrate market held an estimated 2.5 % of global volume in 2024 but is rising steadily due to oil & gas, construction and high-temperature occupational environments. Key growth countries include the United Arab Emirates and South Africa, where modernization of workplace hydration standards is underway. Technological trends include integration of IoT-based sensors in worker hydration monitoring and automated refill stations linked to electrolyte concentrate units. Local regulations are evolving to mandate worker hydration protocols in high-heat industries, creating institutional demand. One regional manufacturer introduced a custom hydration-station bundle for construction sites in the Gulf region in 2025, reflecting adaptation to local industrial conditions. Consumer behavior varies: in these regions, functional hydration products are increasingly adopted in professional environments rather than purely recreational use.

United States - 41% Market Share: Driven by high production capacity and strong end-user demand in sports nutrition and clinical hydration.

China - 18% Market Share: Supported by rapid infrastructure build-up, increasing domestic manufacturing and rising consumer adoption of functional beverages.

The global Electrolyte Concentrate Market presents a moderately fragmented competitive environment, with approximately 70 to 90 active global competitors addressing various niche and mainstream segments. The top five companies—together accounting for an estimated 35 % to 40 % of market share—include major players that rely on broad product portfolios, strategic partnerships and frequent product launches to differentiate. Key strategic initiatives include alliances between nutrition and sports-science firms, new formulation launches featuring plant-based and sugar-free ingredients, mergers of niche hydration brands into larger conglomerates, and cross-region production expansion. Innovation trends are centered on clean-label formulations, AI-driven blending processes, smart packaging with sensory feedback and mobile-app linked hydration tracking. Because the remaining 60 %+ of share is held by a mix of regional players, ingredient specialists and start-ups, established firms continually seek acquisition opportunities and IP-led differentiation. Competitors are positioning along two broad axes: premium performance sports hydration and everyday wellness hydration. The competitive intensity is elevated by the low entry barriers in formulation but high consumer demand for brand credibility and certification. For decision-makers this means market entry strategy must consider not only product attributes but distribution channels, brand partnerships and regulatory compliance.

Abbott Laboratories

The Coca-Cola Company

Lyte Balance (Smell Taste Technology)

Livwell Products

LyteLine

Triquetra Health

Powerbar (Nestlé)

Total Hydration

B. Braun

Thorzt

Elte Electrolyte

Adapted Nutrition

The electrolyte concentrate market is undergoing a significant technological transformation. Current technologies include precision mineral blending systems capable of delivering micronutrient ratios within ±5 % tolerance, enabling manufacturers to create bespoke formulations for athlete- and clinical-usage segments. Emerging technologies include AI-driven formulation engines that analyse hydration data, sweat mineral loss profiles, and biometric feedback to tailor electrolyte concentrate blends to individual users; wearable hydration sensors are now used by over 12 % of professional sports teams in developed markets to feed real-time data into these systems. On the packaging front, smart pouches embedded with NFC tags allow consumers to track hydration frequency and product usage via smartphone apps, improving loyalty and enabling active feedback loops in formulation R&D. In manufacturing, high-throughput continuous-flow mixing lines reduce batch variation by around 18 % compared to traditional batch processes, accelerating time-to-market for new formulas. Product innovation also includes encapsulation technologies (e.g., liposomal mineral carriers) to improve bioavailability, with trials showing up to a 15 % increase in absorption compared to conventional mixes. Meanwhile, blockchain-enabled supply-chain transparency solutions are being piloted to verify clean-label and trace-mineral sourcing credentials, addressing consumer trust and regulatory scrutiny. From a strategic viewpoint, this technological evolution means companies can shift from commoditised concentrate blends to data-driven, personalised hydration solutions — a transition that alters competitive positioning, margin structure and required capabilities. Decision-makers should therefore evaluate technology investments not just in formulation but digital-services integration, connected packaging and consumer analytics.

In June 2023, Trace Minerals Research’s launch of its ZEROLyte sodium-and-electrolyte drink mix won the “Hydration Product of the Year” award, highlighting its use of ancient sea salt, coconut water, potassium, magnesium and a full-spectrum ionic trace mineral blend. Source: www.traceminerals.com

In June 2023, Nestlé Health Science introduced Nuun® Sport Hydration Powder with five essential electrolytes and 90 % less sugar than traditional electrolyte drink mixes, offered in Pink Lemonade and Strawberry Kiwi flavors and launched through Amazon and Whole Foods. Source: www.nestlehealthscience.us

In March 2025, Electrolit expanded its premium hydration offering with multipack formats of Strawberry Kiwi, Grape and Blue Raspberry available at Sam’s Club, Costco, Kroger and Publix, signalling packaging innovation and retail channel expansion. Source: www.prnewswire.com

In early 2025, Hyundai Bioland launched the Nuun® electrolyte drink (from Nestlé Health Science) into the Korean market, marking a regional expansion into East Asia and leveraging local distribution partnerships.

This report covers the global Electrolyte Concentrate Market with comprehensive segmentation by product type (such as isotonic, hypotonic and hypertonic formulations), application (sports performance, medical/clinical hydration, industrial workforce hydration, everyday wellness) and end-user (professional athletes, hospitals/clinical institutions, industrial work-forces, general wellness consumers). Geographically, it spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, offering detailed country-level insights for major markets. Technology focus areas include formulation innovation (bio-available minerals, low-sugar blends), packaging and delivery systems (smart packets, NFC-enabled pouches), manufacturing and supply-chain digitalisation (continuous mixing lines, blockchain traceability). The report also addresses emerging niche segments such as electrolyte-enriched hydration for elderly and recovery care, “functional hydration” blends combining electrolytes with adaptogens or collagen, and region-specific formats (e.g., on-the-go sachets in Asia-Pacific). Industry focus includes regulatory frameworks (labeling, permissible mineral concentrations), ESG-driven packaging transitions and ingredient sourcing risk (potassium, magnesium). With this breadth, the report is structured to guide strategic decision-makers, investors and industry professionals in identifying product development opportunities, regional expansion strategies, technology investment needs and competitive positioning within the electrolyte concentrate landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,397.5 Million |

| Market Revenue (2032) | USD 3,792.5 Million |

| CAGR (2025–2032) | 5.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Trace Minerals Research, BodyBio, Inc., Nestlé Health Science, Abbott Laboratories, The Coca-Cola Company, Lyte Balance (Smell Taste Technology), Livwell Products, LyteLine, Triquetra Health, Powerbar (Nestlé), Total Hydration, B. Braun, Thorzt, Elte Electrolyte, Adapted Nutrition |

| Customization & Pricing | Available on Request (10% Customization is Free) |