Reports

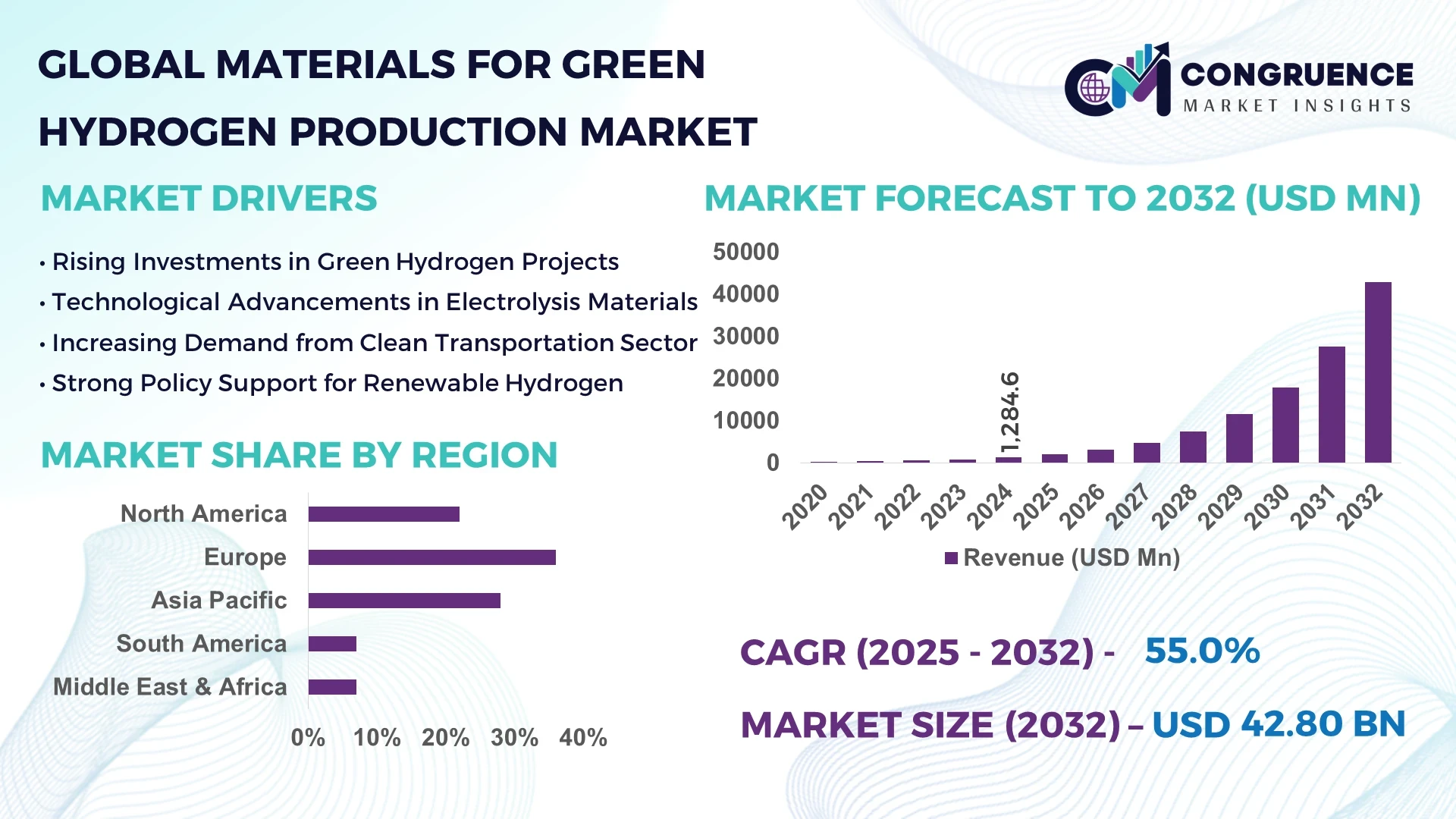

The Global Materials for Green Hydrogen Production Market was valued at USD 1,284.6 Million in 2024 and is anticipated to reach a value of USD 42,797.8 Million by 2032 expanding at a CAGR of 55% between 2025 and 2032.

Japan firmly leads the market with its substantial capacity for advanced catalytic material manufacturing, significant investments in proton-exchange membrane technology, prominent deployment in industrial-scale electrolyzers, and strong focus on nanostructured electrode innovation.

The Materials for Green Hydrogen Production Market is witnessing dramatic transformation as demand for high-performance catalysts, membranes, and electrode supports accelerates globally. Critical sectors such as renewable energy integration, heavy industry decarbonization, and transportation are driving demand for materials with high conductivity, long-term stability, and resistance to degradation under electrochemical stress. Recent innovations include low-cost, non-platinum group metal (non-PGM) catalysts, doped proton-conducting ceramics, and composite electrode backbones with enhanced mass transport. Governments worldwide are introducing stringent environmental mandates and incentives for green hydrogen adoption, particularly in Europe, North America, and Asia-Pacific. Market growth is characterized by regional investments, interdisciplinary R&D collaborations, and supply chain scaling, while emerging trends such as circular material use and AI-enhanced formulation development are shaping the future outlook for industrial decision-makers.

Artificial Intelligence is catalyzing a revolution in the Materials for Green Hydrogen Production Market by dramatically accelerating the discovery, optimization, and deployment of advanced material systems. AI-driven modeling platforms can screen thousands of catalyst and membrane candidates, reducing development timelines from years to weeks. Machine learning algorithms now analyze compositional and structural data to predict key properties such as catalytic activity, durability, and conductivity, empowering researchers to focus on high-potential candidates.

In commercial and industrial settings, AI-enhanced process control systems have been deployed to optimize operating environments—adjusting temperature, pressure, and electrolyte composition in real time, improving stability and performance of electrolyzer materials. Digital twin simulations, powered by AI, allow manufacturers to simulate material behavior under stress conditions, enabling proactive design modifications and predictive maintenance schedules.

Moreover, AI is aiding material manufacturers in quality control by analyzing production-line sensor data to detect anomalies in membrane thickness or catalyst morphology early. AI-enabled supply chain tools ensure traceability of raw materials like nickel, iridium, and proton-conducting ceramics, enabling faster risk mitigation and compliance. As AI applications become entrenched in materials design and manufacturing, the Materials for Green Hydrogen Production Market is transitioning into a data-optimized, highly agile ecosystem that supports scalable and cost-effective green hydrogen infrastructure.

“In March 2024, a research team deployed an AI-based screening framework to identify platinum-group-free electrolyzer electrode materials from a dataset of over 3,000 candidates, completing in just one month what would have taken nearly six years using traditional methods.”

The Materials for Green Hydrogen Production Market is driven by a complex interplay of technological, regulatory, and economic factors. Green hydrogen production now relies heavily on materials that can achieve high efficiency under rigorous electrochemical conditions while remaining cost-effective at scale. The shift from expensive platinum-based catalysts to more abundant transition-metal oxides, doped ceramics, and composite nanomaterials has accelerated. Demand from renewable-rich economies is fueling large-scale electrolyzer deployment, while emerging industrial use cases—such as green ammonia and steel decarbonization—are boosting material requirements. Concurrently, global policies such as carbon pricing and green hydrogen quotas are compelling manufacturers to enhance material durability and circularity. As supply chains mature and material innovation continues, strategic partnerships and vertical integration are increasingly shaping competitive positioning within the Materials for Green Hydrogen Production Market.

The Materials for Green Hydrogen Production Market is gaining momentum through accelerated development of non-platinum group metal (non-PGM) catalysts. Innovative materials such as manganese-nickel-iron oxide composites and doped perovskite catalysts are delivering comparable performance to platinum-based systems with dramatically lower cost and improved scalability. Some implementations now report over 1000 operational hours of stable chlorine-free electrolysis with performance within 10% of benchmark catalysts. These material advancements are enabling manufacturers to scale production of green hydrogen, especially in resource-constrained and cost-sensitive regions, solidifying their market leadership.

A critical restraint in the Materials for Green Hydrogen Production Market is the limited availability and geopolitical concentration of key specialty metals such as iridium, ruthenium, and certain rare-earth dopants. With plasma-based electrolyzers requiring small but critical amounts of iridium, market stability can be highly sensitive to supply chain disruptions. Furthermore, recycling infrastructure for spent electrolyzer materials remains underdeveloped—recovery rates of precious metals fall below 60% in many cases, placing sustained pressure on cost and net environmental footprint.

Promising opportunities in the Materials for Green Hydrogen Production Market include the commercialization of earth-abundant catalysts and composite constructs. Lightweight cobalt-free alloys, carbon-nanotube-supported catalysts, and proton-conducting polymer blends are stepping into industrial-scale trials. For example, pilot systems using these materials report over 500 operating cycles without performance degradation. With a growing focus on circular economy principles, scalable composite solutions offer potential for lower lifecycle cost, higher performance, and reduced environmental impact.

While innovation in catalyst and membrane design is accelerating, ensuring long-term durability and manufacturability at scale remains a major challenge. Advanced ceramics and nanocomposites often exhibit excellent laboratory performance but struggle under industrial electrolyzer conditions—cycling degradation and material delamination can occur after 1,000–2,000 hours of continuous operation. Moreover, scaling production of these advanced materials requires precise and repeatable synthesis protocols, often involving high-cost processes such as atomic layer deposition or reactive sputtering. Overcoming these engineering and economic hurdles is essential for mainstream adoption of materials in the Materials for Green Hydrogen Production Market.

Development of Platinum-Group-Free Catalysts: A significant shift is underway toward high-performance catalysts composed of earth-abundant elements such as Fe, Ni, Mn, and Ag. AI-assisted research has identified candidates that surpass traditional benchmarks in stability and electrochemical activity within weeks of screening.

Adoption of Composite Membrane Materials: Next-generation proton-exchange membranes now incorporate reinforced polymer layers and nano-sized ceramic fillers, achieving higher mechanical strength and improved conductivity under fluctuating temperatures.

Circular Material Initiatives: Recycling programs have begun repurposing spent electrolyzer electrodes, recovering over 60% of valuable metals, aligning material innovation with environmental sustainability goals in green hydrogen manufacturing.

AI-Accelerated Material Screening Platforms: AI and machine learning systems are being deployed to sift through enormous chemical combinations and structural configurations, reducing discovery timelines from years to weeks and lowering experimental costs.

The market segmentation for Materials for Green Hydrogen Production is shaped by material type, electrochemical application, and end-user industry. Leading material categories include catalysts, membranes, electrodes, and structural supports. Applications span alkaline, proton exchange membrane, and solid oxide electrolysis technologies. From an end-user perspective, the chemical industry (e.g., for ammonia synthesis), transportation (via hydrogen refueling), and utilities (for grid energy storage) dominate uptake. This segmentation illustrates the strategic role of materials across diverse hydrogen production pathways—highlighting innovation nodes, sector-specific drivers, and industrial adoption channels within the green hydrogen ecosystem.

Catalysts remain the leading material type in the Materials for Green Hydrogen Production Market, as they directly influence reaction kinetics and system efficiency. Proton-conducting membranes follow closely due to their role in maintaining high electrolysis efficiency and output. Emerging types such as composite electrodes with integrated catalysts are gaining interest for providing enhanced mass transport and thermal resilience. Ceramic supports and bipolar plates, while niche, contribute to high-temperature systems such as solid oxide electrolysis. Among them, catalysts lead on performance impact, while composite electrodes represent the fastest-growing type due to their multifunctional advantages across diverse electrolyzer configurations.

Alkaline electrolysis leads in application volume due to its maturity and lower material cost, despite operating efficiency challenges. Proton exchange membrane (PEM) electrolysis is the fastest-growing application, benefitting from superior dynamic response and compatibility with renewable electricity inputs. Solid oxide electrolysis, used for high-temperature industrial processes, is gaining traction in sectors such as steelmaking and cement, although still niche. This application segmentation reflects the varied material needs—from corrosion-resistant membranes to high-temperature ceramic components—enabling tailored solutions across hydrogen production methods.

Large-scale industrial players, including chemical producers and utilities, represent the leading end-user segment in the Materials for Green Hydrogen Production Market due to their ability to deploy electrolyzer systems at scale. The fastest-growing end-user category is transportation infrastructure developers and mobility providers, particularly with rising demand for green hydrogen in heavy-duty sectors. Additionally, emerging consumer and microgrid users are beginning to integrate electrolyzers into localized renewable systems, increasing the material demand across decentralized energy landscapes. The diversity of end-users underscores the need for adaptable and resilient material solutions.

Europe accounted for the largest market share at 36% in 2024; however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 59% between 2025 and 2032.

Europe’s strong position is supported by its extensive electrolyzer manufacturing base, favorable hydrogen policies, and advanced R&D ecosystem. Meanwhile, Asia-Pacific benefits from rising infrastructure investments, large-scale industrial adoption, and growing government-led hydrogen roadmaps. Both regions continue to shape the strategic evolution of materials innovation and deployment for green hydrogen production.

Advanced Material Adoption for Decarbonization Initiatives

North America captured nearly 22% of the global Materials for Green Hydrogen Production Market in 2024, with strong uptake across energy storage, mobility, and industrial decarbonization projects. The U.S. has accelerated demand through federal funding programs supporting electrolyzer deployment and clean hydrogen hubs. Key industries driving material demand include chemical processing, power generation, and transportation fleets integrating hydrogen fuel. Regulatory frameworks such as the Inflation Reduction Act incentivize clean energy investments, driving a measurable rise in electrolyzer installations. Technological advancements in AI-driven catalyst development and additive manufacturing of electrode components are boosting production efficiency and lowering material costs across the region.

Pioneering Innovation in Hydrogen Electrolysis Materials

Europe held the largest share at 36% of the global Materials for Green Hydrogen Production Market in 2024, driven by strong adoption in Germany, France, and the UK. The region benefits from ambitious hydrogen roadmaps under EU regulatory frameworks that mandate clean energy transition and carbon neutrality by 2050. Government-backed initiatives are propelling investment into advanced catalyst and membrane technologies. Germany is leading in electrolyzer scaling, while France and the UK are investing in fuel-cell-ready hydrogen supply chains. Europe is also spearheading composite membrane integration and platinum-free catalyst commercialization. The synergy between sustainability initiatives and material innovation secures Europe’s leadership in this sector.

Rapid Expansion in Manufacturing and Industrial Applications

Asia-Pacific represented 28% of the global Materials for Green Hydrogen Production Market in 2024 and is expected to be the fastest-growing region through 2032. China leads material consumption due to its aggressive electrolyzer manufacturing expansion and investment in non-platinum catalyst supply chains. Japan is advancing proton exchange membrane (PEM) technologies, while India is accelerating renewable hydrogen adoption through national hydrogen missions. Infrastructure development, such as dedicated hydrogen corridors and industrial hubs, is creating large-scale opportunities for catalyst, membrane, and electrode material suppliers. Innovation hubs across Japan and South Korea are pioneering AI-enabled material screening for hydrogen applications.

Growing Potential in Renewable Energy-Linked Hydrogen Production

South America accounted for nearly 7% of the global Materials for Green Hydrogen Production Market in 2024, led by Brazil and Chile. Brazil’s strong renewable base and rising ammonia production industry are driving material adoption in electrolyzers. Chile is progressing toward large-scale hydrogen projects linked to solar and wind power capacity, further strengthening demand for durable catalyst and membrane materials. Regional governments are introducing tax incentives and favorable trade policies to attract foreign investment in hydrogen infrastructure. Advances in composite electrode technology and lightweight structural supports are gaining attention as South America prepares for export-oriented green hydrogen production.

Hydrogen Expansion from Oil & Gas Diversification Strategies

The Middle East & Africa region contributed 7% to the Materials for Green Hydrogen Production Market in 2024, with rapid expansion expected in the coming years. The UAE and Saudi Arabia are investing heavily in mega-projects that integrate advanced electrolyzer materials with large-scale renewable energy installations. South Africa is developing a hydrogen corridor to support industrial decarbonization, particularly in mining and steel. Regional demand trends are shifting from traditional energy reliance toward clean hydrogen, supported by international trade partnerships. Technological modernization, including adoption of ceramic membranes and advanced electrode composites, is enabling high-capacity hydrogen systems aligned with export goals.

Germany – 19% share

Strong leadership driven by extensive electrolyzer manufacturing capacity and sustained government-backed R&D programs in catalyst and membrane technologies.

China – 17% share

High material demand due to rapid infrastructure scaling, industrial hydrogen adoption, and large-scale production of low-cost non-platinum catalysts.

The Materials for Green Hydrogen Production Market is characterized by intense competition with over 120 active players globally spanning catalyst producers, membrane developers, and electrode material suppliers. European companies dominate advanced research and pilot deployments, while Asian manufacturers are scaling industrial production with cost advantages. Strategic initiatives such as joint ventures between electrolyzer OEMs and material developers are becoming common, targeting integrated value chains. Recent partnerships have focused on recycling technologies to recover iridium and platinum-group metals from spent catalysts, ensuring material circularity. Innovation trends highlight AI-driven screening platforms, nanocomposite electrode fabrication, and membrane durability enhancements as differentiators in the competitive landscape. Smaller entrants are leveraging proprietary intellectual property and specialized material formulations, while established players are consolidating through acquisitions to strengthen supply chain resilience.

Johnson Matthey

Umicore

3M

Ballard Power Systems

Toray Industries

BASF

Heraeus Group

SGL Carbon

Evonik Industries

NEL ASA

The Materials for Green Hydrogen Production Market is undergoing a technological transformation with advancements in catalysts, membranes, and composite structures driving efficiency improvements. Catalysts are transitioning from platinum-based systems to non-PGM alternatives such as transition-metal oxides, nitrides, and perovskites, which offer comparable performance with lower cost. Proton-exchange membranes are evolving with hybrid polymer-ceramic structures, achieving enhanced conductivity and thermal resilience at fluctuating loads. Solid oxide electrolyzer materials now leverage yttria-stabilized zirconia ceramics to withstand high operating temperatures above 700°C, enabling industrial hydrogen integration.

Digital technologies, including AI and digital twins, are revolutionizing R&D by predicting catalyst stability and membrane degradation under diverse conditions. Additive manufacturing is enabling precision fabrication of electrodes with optimized porosity and conductivity. Recycling technologies are emerging to recover critical metals such as iridium, ruthenium, and nickel, reducing supply risks. Emerging materials such as graphene-coated electrodes and nanostructured bipolar plates are advancing toward commercialization, promising longer lifespans and higher energy efficiency. Together, these innovations are transforming scalability, reducing lifecycle costs, and enabling integration of green hydrogen across multiple industrial sectors.

In February 2024, Johnson Matthey introduced a next-generation non-platinum catalyst for PEM electrolyzers, enabling over 2,000 operational hours with stable efficiency during large-scale industrial testing.

In October 2024, BASF launched a composite proton-exchange membrane integrating ceramic fillers, reporting 15% higher conductivity compared to conventional polymer membranes under fluctuating temperatures.

In July 2023, Heraeus Group unveiled a recycling process capable of recovering up to 85% of iridium from spent electrolyzer catalysts, significantly enhancing circular material supply.

In May 2023, Toray Industries developed a graphene-coated electrode with 25% improved durability, targeting heavy-duty hydrogen production applications across industrial plants.

The Materials for Green Hydrogen Production Market Report provides comprehensive coverage of key material types including catalysts, membranes, electrodes, and bipolar plates, along with applications across alkaline, PEM, and solid oxide electrolysis. The report evaluates industry adoption by major end-user segments such as chemicals, utilities, transportation, and decentralized renewable energy systems. Geographic insights cover North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional investment trends and policy frameworks.

Additionally, the report addresses technological advances in non-PGM catalysts, hybrid membranes, and recycling systems critical to sustainable growth. It incorporates detailed segmentation analysis of material adoption trends and identifies niche markets such as graphene-based electrodes and nanostructured composites. The scope extends to emerging opportunities within industrial-scale hydrogen-to-ammonia projects, mobility-focused hydrogen fueling, and renewable-powered grid storage solutions. By integrating insights on market dynamics, competition, technology, and policy, the report equips decision-makers with strategic intelligence to navigate the rapidly evolving Materials for Green Hydrogen Production Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1284.6 Million |

|

Market Revenue in 2032 |

USD 42797.8 Million |

|

CAGR (2025 - 2032) |

55% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Johnson Matthey, Umicore, 3M, Ballard Power Systems, Toray Industries, BASF, Heraeus Group, SGL Carbon, Evonik Industries, NEL ASA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |