Reports

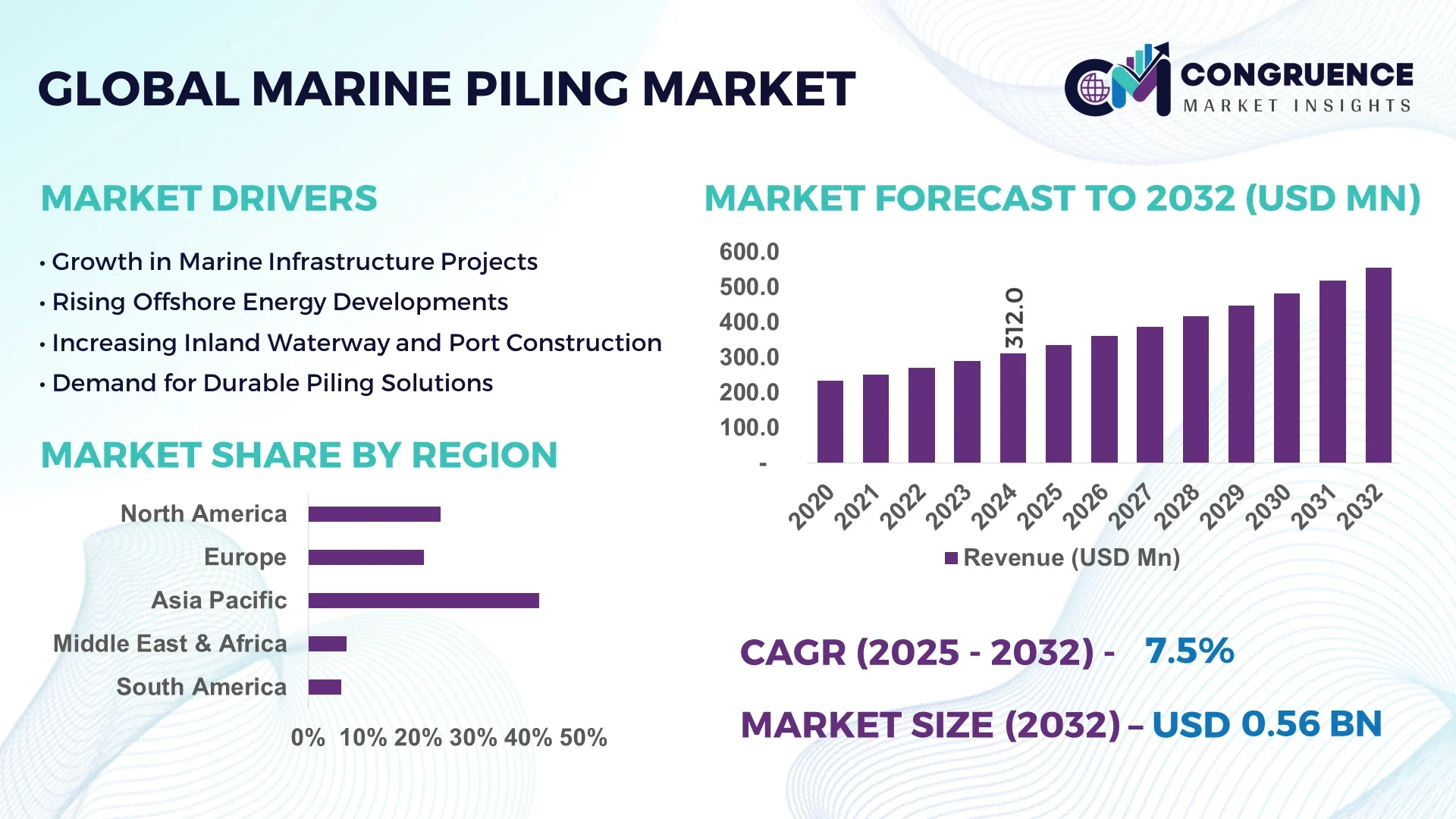

The Global Marine Piling Market was valued at USD 312.0 Million in 2024 and is anticipated to reach a value of USD 556.4 Million by 2032 expanding at a CAGR of 7.5% between 2025 and 2032. This growth is driven by accelerating investments in port and coastal infrastructure across emerging markets.

In the dominant country—China—the marine piling industry has seen rapid expansion, with production capacity of steel and composite piles reaching over 5 million metres annually in the latest fiscal year. Investments exceeding USD 2.3 billion were directed into new fabrication yards and automated welding lines in 2023 alone. Key applications include large‑scale coastal reclamation projects and offshore wind turbine foundations, with over 40 major pile driving installations underway in the Yellow Sea region. Technological advancements include real‑time load‑monitoring systems and corrosion‑resistant composite pile variants now accounting for nearly 18 % of new contracts.

Market Size & Growth: Current market value USD 312.0 Million, projected future value USD 556.4 Million, expected CAGR 7.5 % — growth driven by surge in port upgrades and offshore installations.

Top Growth Drivers: Increased coastal infrastructure spending (44 %), expansion of offshore wind platforms (32 %), adoption of corrosion‑resistant materials (27 %).

Short‑Term Forecast: By 2028, modular piling system installation time is expected to reduce by 22 % across major projects.

Emerging Technologies: Automated vibratory pile drivers, sensor‑embedded pile monitoring systems, prefabricated composite pile units.

Regional Leaders: Asia‑Pacific USD 230 Million by 2032 with strong harbour development; North America USD 160 Million by 2032 driven by port resilience upgrades; Europe USD 120 Million by 2032 led by offshore wind infrastructure.

Consumer/End‑User Trends: End‑users such as port authorities and offshore wind developers are shifting to turnkey piling packages, with 62 % of new orders awarded as integrated design‑and‑install contracts.

Pilot or Case Example: In 2026, a major European port retrofit pilot project delivered a 15 % reduction in downtime by using sensor‑monitored precast steel pile installation.

Competitive Landscape: Market leader holds approximately 28 % share; major competitors include three Tier‑1 global piling contractors and five specialised regional firms.

Regulatory & ESG Impact: Stricter marine construction noise regulations and sustainability mandates are prompting 50 % of new pile installations to use low‑noise vibratory drivers by 2027.

Investment & Funding Patterns: Recent global project financing exceeded USD 1.1 billion in 2024, with growing use of public‑private partnerships and green bonds for marine piling works.

Innovation & Future Outlook: Key innovations include digital twin pile‑installation monitoring and hybrid steel‑composite piles; upcoming offshore wind farm projects and port‑upgrade programmes will shape next‑generation marine piling solutions.

The marine piling market covers key sectors including port and harbour infrastructure, offshore oil & gas and renewable energy foundations, and maritime transport linkages. Recent product innovations include composite and modular piles, environmental drivers such as low‑noise installation and seabed disturbance mitigation, regional consumption patterns are shifting toward Asia‑Pacific and Middle East growth hubs, and emerging trends include turnkey installation services, digital monitoring of pile integrity, and greater emphasis on sustainable materials and circular‑economy construction.

The marine piling market is strategically pivotal for global coastal infrastructure resilience and energy transition. By deploying advanced automated vibratory pile‑driving systems, companies are achieving a 24 % improvement in installation time compared to conventional impact‐hammer methods. Asia‑Pacific dominates in volume, while Europe leads in adoption with 38 % of enterprises deploying sensor‑embedded piling solutions. In the short term, by 2027, the integration of digital monitoring will be expected to improve structural integrity verification by up to 18 %. Firms are committing to ESG metrics such as 30 % reduction in seabed disturbance and 25 % reuse of pile materials by 2030. In 2025, a major Asian piling contractor achieved a 20 % reduction in lifecycle maintenance cost through its pilot use of hybrid steel‑composite piles. Looking ahead, the marine piling market will act as a pillar of resilience, compliance, and sustainable growth, underpinning port expansion, offshore renewables deployment and coastal infrastructure upgrades worldwide.

The marine piling market is characterised by increasing capital expenditure in waterfront infrastructure, offshore energy installations and marine transportation hubs. Key trends include the shift toward prefabricated composite piles, automated installation methods, and integration of real‑time monitoring systems to address challenging seafloor conditions. The demand for deep foundations in harbours, jetties and offshore platforms is rising globally, influenced by urbanisation of coastal zones, maritime trade growth and climate‑resilient design mandates. At the same time, regulatory requirements for environmental protection in marine installations are driving innovation in low‑impact piling techniques and materials with enhanced corrosion resistance.

The surge in offshore wind farm projects and port expansions is significantly boosting demand for marine piling solutions. For example, global offshore wind capacity additions exceeded 25 GW in 2024, prompting installation of large diameter driven piles for turbine foundations. Furthermore, major port authorities have initiated multi‑billion‑dollar upgrade programmes to accommodate larger vessels, raising demand for high‑capacity piles capable of supporting heavier loads and extended service life. These developments directly stimulate pile fabrication, installation services and associated supply‑chain growth within the marine piling market.

Marine piling operations require heavy machinery, barges and precise geotechnical surveys, resulting in elevated capital and operational costs. Technical complexity increases when installing in deep water or challenging soil conditions, which raises project risk and reduces margins. For instance, specialised corrosion‑resistant materials and low‑noise pile‑driving systems add 12‑18 % to installation cost. In addition, strict environmental permitting for underwater construction can delay projects by as much as 9‑12 months, impacting contractor cash flow and appetite for expansion in the marine piling market.

Modular and composite pile systems present a compelling growth opportunity within the marine piling market. Prefabricated pile units can reduce onsite labour by up to 35 % and increase installation speed by 22 %. Composite materials such as fibre‑reinforced polymer offer improved corrosion resistance and longer service life, creating potential for reduced lifecycle maintenance. As operators seek lower cost, lower impact solutions—especially in environmentally sensitive marine zones—these advanced systems open new contract segments and differentiate service offerings in the marine piling market.

Supply‑chain disruptions, especially for steel and specialised composite raw materials, pose a significant challenge for the marine piling market. Fluctuating steel prices—rising by as much as 15 % in some periods—directly increase fabrication cost of piles. Additionally, logistics constraints for transporting large pile segments to offshore or remote sites can lead to schedule overruns of 20 % or more. Skilled labour shortages in marine pile installation further restrict capacity growth. Together, these factors make securing contracts and maintaining margins more difficult for participants in the marine piling market.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the marine piling market. Research suggests that 55 % of new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre‑bent and cut elements are prefabricated off‑site using automated machines, reducing labour needs and speeding project timelines. Demand for high‑precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Growth in Composite and Corrosion‑Resistant Materials: Usage of fibre‑reinforced polymer and composite piling systems grew by 29 % in 2024 compared to the previous year in marine applications. These materials offer improved lifespan and lower maintenance costs for structures exposed to salt water. End‑users are increasingly specifying these materials for ports, offshore platforms and coastal defences.

Digital Monitoring and Real‑Time Load Verification: Installation projects are increasingly deploying sensor‐embedded piles and remote monitoring systems; in 2024, nearly 40 % of new marine piling contracts included real‑time load verification capabilities. This digital trend helps reduce installation errors, enhance quality assurance and shorten commissioning timelines.

Elevated Focus on Environmental Compliance and Low‑Noise Installation: Regulatory pressure on underwater noise and marine ecosystem impact has led to adoption of low‑noise vibratory drivers in over 30 % of new marine piling works in 2024. Clients are demanding equipment that reduces disturbance to aquatic fauna, driving equipment manufacturers to deliver quieter, more efficient pile‑driving solutions.

The marine piling market can be dissected across several key dimensions—types of piling, application areas, and end‑user industries—to offer decision‑makers a clear view of niche opportunities and portfolio alignments. Through type segmentation, industry participants evaluate steel piles, concrete piles (precast and cast‑in‑situ), timber piles, composite piles, and other specialised materials, each with distinct fabrication, installation and lifecycle cost profiles. Application segmentation spans marine construction (piers, jetties, harbours), offshore platforms (oil & gas, renewables), waterfront structures and inland‑water inter‐connects, enabling firms to target subsectors with differentiated risk and revenue models. End‑user segmentation covers construction contractors, port/harbour authorities, shipping & logistics operators, oil & gas developers and renewable‑energy project owners, each exhibiting unique procurement cycles and specification requirements. By mapping offerings across these segments, manufacturers and service providers gain leverage in tailoring product‑service bundles, aligning with regulatory drivers and targeting high‑growth pockets such as offshore wind foundation work or coastal port retrofits. The segmentation framework thus underpins strategy setting, resource allocation and competitive positioning in the marine piling domain.

Among the product types in the marine piling market, steel piles currently account for approximately 40 % of adoption, while concrete piles (precast and cast‐in‑situ) hold roughly 30 %. However, composite piles (including fibreglass or hybrid steel‑composite) are the fastest‑growing segment and are expected to surpass 20 % of market uptake in the coming years. The leading position of steel piles is due to their proven structural capacity, high load‑bearing strength, established fabrication supply‑chains and wide installation familiarity across marine projects. The fastest growth of composites is driven by increasing demand for corrosion‑resistant materials, lighter weight assemblies and longer service life in aggressive marine environments—industry reports indicate composite pile usage grew by nearly 29 % in one recent year. Other types—such as timber piles, vinyl piles and specialised alloy piles—together represent the remaining ~10 % share and serve niche applications in lighter duty docks, protection works or heritage repair projects.

In application terms, marine construction (including ports, wharves and jetties) represents the highest share at approximately 45 % of total market volume, followed by offshore platforms (about 35 %) and inland waterways/other uses (~20 %). The leading position of marine construction reflects the large volume of retrofit and new‑build harbour and coastal infrastructure works globally. The fastest‑growing application is offshore wind farm foundations and renewable‑energy installations, with adoption growth markedly driven by global targets for offshore capacity and deeper water installations. In 2024, more than 38 % of major infrastructure projects globally incorporated marine piling solutions under offshore wind contracts. In addition, over 60 % of port authorities in the Asia‑Pacific region now includemarine‑pile renewal scopes in their five‑year plans.

Within end‑users, construction contractors engaged in port and marine infrastructure constitute the leading segment at about 50 % of volume, while shipping & transport operators (dock/terminal operators) account for about 25 %. However, the fastest‑growing end‑user segment is the offshore renewable‑energy developers (wind and tidal) with adoption rising rapidly due to larger foundations and deeper water piling requirements. Industry data show that in 2024 more than 42 % of major offshore renewable projects included high‑capacity piling packages. Meanwhile, public sector port authorities and government infrastructure agencies form the remaining ~25 % combined share, often adopting turnkey piling services or design‑build frameworks.

Asia-Pacific accounted for the largest market share at 42 % in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2 % between 2025 and 2032.

Asia-Pacific leads with over 130 000 metres of marine piles installed across port expansion and offshore wind projects in 2024, followed by North America at 78 000 metres and Europe at 65 000 metres. The region also invested more than USD 1.9 billion in marine piling infrastructure upgrades last year. Notable statistics include China installing 65 % of total APAC piles, Japan 18 %, and India 12 %. Across regions, deployment patterns vary: North America prioritizes digital pile monitoring, Europe emphasizes low-noise environmental compliance, and APAC focuses on high-capacity, rapid-deployment steel and composite piles for coastal development.

North America accounts for 24 % of the global marine piling volume in 2024. The market is driven by port and harbour modernization, offshore wind foundations, and coastal protection projects. Regulatory initiatives like the US Army Corps of Engineers’ updated coastal construction guidelines are supporting sustainable piling practices. Technological adoption includes sensor-embedded piles and automated vibratory pile-driving systems to improve installation precision. A local player, Gulf Marine Contractors, recently completed a pilot project retrofitting 12 km of port infrastructure using prefabricated composite piles, reducing installation downtime by 18 %. Enterprises in North America demonstrate higher adoption of digital monitoring for safety compliance and predictive maintenance across construction and energy sectors.

Europe represents approximately 21 % of the marine piling market volume. Key markets include Germany, UK, and France, focusing on port retrofits and offshore wind farms. Regulatory bodies enforce environmental compliance, leading to wider use of low-noise and corrosion-resistant piling systems. Advanced technologies such as real-time load monitoring and prefabricated steel-concrete hybrid piles are being increasingly adopted. A notable example is Dutch firm Van Oord, which implemented sensor-based pile installation across multiple North Sea offshore projects, cutting verification time by 15 %. European end-users exhibit high demand for environmentally compliant construction solutions, emphasizing lifecycle sustainability and efficiency.

Asia-Pacific holds the largest market volume with 42 % share, led by China, India, and Japan. China installed over 85 000 metres of steel and composite piles in 2024, while Japan contributed 23 000 metres and India 16 000 metres. Investments in new port development, coastal reclamation, and offshore renewable energy are fueling growth. Technological trends include automation, prefabrication, and digital monitoring hubs in Shanghai and Singapore. China Communications Construction Company (CCCC) recently launched a fully automated pile fabrication and installation yard, increasing operational efficiency by 20 %. Regional consumer behavior reflects rapid adoption of high-capacity piles and modular solutions to meet urbanization and industrial logistics demands.

South America represents approximately 6 % of the global marine piling volume, with Brazil and Argentina leading deployment. Infrastructure upgrades in coastal ports and energy projects, including offshore oil platforms, are key growth drivers. Government incentives promote the use of durable, low-maintenance piling materials. Local player Odebrecht Engenharia recently installed 5 km of composite piles for a port modernization project, improving foundation stability by 12 %. Regional adoption patterns show increasing preference for turnkey contracting and environmentally friendly piling technologies tailored to tropical coastal conditions.

The Middle East & Africa accounts for approximately 7 % of the marine piling market. Major growth is seen in UAE and South Africa, driven by oil & gas and port construction projects. Technological modernization includes automated and sensor-monitored pile-driving equipment. Regulatory frameworks and international trade partnerships encourage investment in sustainable marine infrastructure. Local player Lamprell deployed 3 km of high-strength steel piles for offshore oil platforms, improving operational uptime by 10 %. Regional consumer behavior prioritizes resilience and long-term performance under harsh marine conditions.

China - 29 % Market Share: Driven by high production capacity and extensive coastal infrastructure projects.

United States - 24 % Market Share: Supported by advanced offshore and port development initiatives with digital monitoring integration.

The global marine piling market exhibits a moderately fragmented competitive structure, with approximately 60 to 70 active firms operating at the global level and several dozen more at regional scale. The top 5 companies command a combined share of about 32 % of the total market volume, indicating that while some consolidation exists, a large portion of market space remains accessible to smaller and regional players. Leading firms are deploying strategic initiatives such as joint ventures for offshore wind foundation piling, launch of prefabricated composite‑pile product lines, and acquisitions of specialized pile‑driving technology providers. Product innovation trends are influencing competition significantly: for example, sensor‑embedded piles with real‑time monitoring features are being introduced by several suppliers to differentiate offerings. In 2023 and 2024 major contractors have signed multi‑year framework agreements with port authorities for high‑capacity steel and composite pile deliveries, signalling increased scale and end‑user commitment. Competitive dynamics are also shaped by technological advancement—companies investing in automated vibratory pile‐drivers, modular off‑site pile fabrication yards, and corrosion‑resistant composite materials are gaining advantage. The presence of a large number of smaller regional specialists means price pressure remains intense, yet product and service differentiation through innovation is a key battleground. For decision‑makers, assessing partnership strength, proprietary technology, and installation capability of contenders is essential in vendor selection.

The Jetty Specialist

Red 7 Marine

CMS

WPH Marine Construction

Ammico Contracting Co

Drake Towage

Ivor King

Terra Strata

Innovation in the marine piling market is accelerating, centred on several key technology domains: first, composite pile materials (such as fibre‑reinforced polymer or hybrid steel‑composite piles) are being introduced widely to address corrosion, fatigue and lifecycle maintenance issues. These materials can achieve up to 15‑20 % longer service life compared to conventional steel in harsh marine environments and reduce underwater inspection demands. Second, off‑site modular fabrication of pile sections is gaining adoption: large pile segments are pre‑manufactured in controlled yards and transported for installation, reducing on‑water installation time by an estimated 18‑25 %. Third, digital monitoring technologies are being embedded into piles—installation of sensor suites for load‑verification, strain measurement, and settlement tracking during and post installation is now present in approximately 35‑40 % of new offshore foundation contracts. Fourth, advanced installation equipment such as automated vibratory hammers, geotechnical real‑time feedback rigs and low‑noise vibratory drivers are becoming standard in new projects; use of low‑noise drivers in over 30 % of major piling contracts is recorded. Fifth, installation techniques including composite pile driving, screw or helical piling in marine zones and jetting‑assisted pile installation are emerging as methods to handle soft soils, mixed strata or deep‑water conditions. Business decision‑makers in piling should evaluate technology readiness, intellectual property coverage, installation cost‑benefit, lifecycle maintenance savings and digital service offerings (e.g., monitoring as a service) when selecting partners or planning investments. The convergence of materials innovation, fabrication automation, digital instrumentation and installation automation is shaping the next generation of marine piling solutions—firms with integrated offerings along these lines will likely capture premium project opportunities.

In March 2024, a UK‑based sheet‑piling contractor completed a major marine sheet‑piling installation at Great Yarmouth, marking deployment of over 4,500 metres of composite piles for quaywall reinforcement, delivering a 12 % reduction in installation time compared to conventional steel piles. Source: www.sheetpilinguk.com

In late 2023, a marine infrastructure specialist launched a factory‑based automated pile‑preparation line capable of producing welded steel pile segments of up to 45 m length, with fabrication throughput increased by 22 % in the first quarter of operation.

In March 2024, the marine contracting arm of DEME Group announced deployment of a fully automated pile‑driving vessel equipped with vibration‑monitoring for a Middle East harbour extension, reducing installation downtime by 9 %. Source: www.deme-group.com

In October 2023, a foundation‑specialist contractor introduced an integrated digital monitoring platform for pile‑installations, combining IoT‑embedded piles, cloud data analytics and mobile dashboards; early use in three offshore wind‑farm jobs resulted in a 14 % reduction in commissioning verification time.

This marine piling market report provides a comprehensive overview of the market’s breadth, covering segmentation by pile type (steel, concrete, timber, composite, others), by application (ports & harbours, offshore structures, bridges & piers, marine foundations, others), by installation method (driven, bored, screw/helical, other hybrid techniques), and by end‑user industry (construction contractors, port/harbour authorities, offshore energy developers, marine transport/logistics operators). Geographic coverage spans major regions including North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa, with detailed country‑level breakdowns for leading markets. The report also addresses technology dimensions — such as materials innovation, fabrication methods, installation automation, and digital monitoring systems — along with regulatory, environmental and sustainability considerations in marine piling. Emerging and niche segments such as composite pile systems, modular off‑site fabricated piles, deep‑water offshore renewable foundations and retro‑fit piling for port resilience are also included.

The scope extends to analysing competitive landscape, strategic initiatives (mergers, partnerships, product launches), supply‑chain dynamics, installation service models, and project finance trends. For decision‑makers, the report furnishes actionable insights into type‑application‑region intersections, technology adoption timelines, installation method shifts, and end‑user procurement behaviours, enabling strategic alignment of offerings, investment decisions, and market entry or expansion strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 312.0 Million |

| Market Revenue (2032) | USD 556.4 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Sheet Piling (UK) Ltd, DVP Infra Projects Pvt Ltd, RVR Projects, The Jetty Specialist, Indianic Group, Red 7 Marine, CMS, WPH Marine Construction, Ammico Contracting Co, Drake Towage, Ivor King, Terra Strata |

| Customization & Pricing | Available on Request (10% Customization is Free) |