Reports

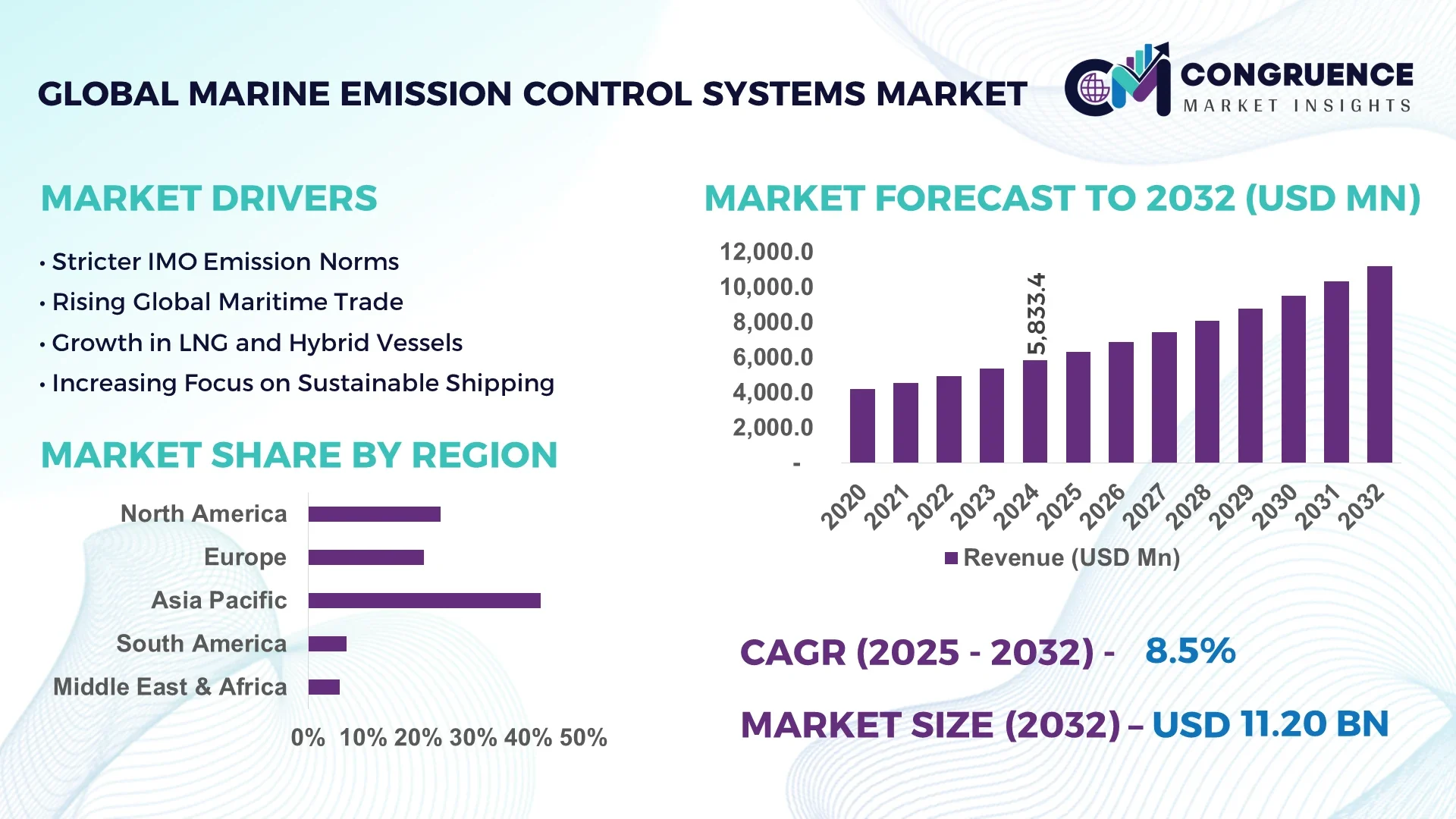

The Global Marine Emission Control Systems Market was valued at USD 5,833.39 Million in 2024 and is anticipated to reach a value of USD 11,203.64 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

South Korea has advanced its position in the Marine Emission Control Systems Market with enhanced production capacities across Busan and Ulsan yards, high investment in scrubber retrofitting lines, and robust technological integration in emission monitoring systems for LNG carriers and large container vessels.

The Marine Emission Control Systems Market is evolving rapidly due to intensifying global maritime emission regulations, a surge in retrofitting activities across ageing fleets, and the growing adoption of hybrid and closed-loop scrubber systems within container ships, bulk carriers, and LNG-fuelled vessels. Notable technological innovations, such as exhaust gas recirculation systems, hybrid scrubber units, and selective catalytic reduction systems, are transforming operational efficiency while ensuring compliance with IMO 2020 and EU MRV standards. Regional consumption patterns highlight strong adoption in Asia-Pacific and Northern Europe due to strict sulfur cap regulations, while emerging economies are investing in advanced solutions to meet evolving environmental standards. The market is further influenced by government initiatives to decarbonize maritime logistics, the expansion of green shipping corridors, and increased R&D spending on advanced filtration materials and automated emission monitoring systems. Future outlook indicates steady growth driven by the transition towards zero-emission shipping and integration of real-time emission analytics for operational optimisation.

Artificial intelligence is significantly transforming the Marine Emission Control Systems Market by enabling predictive maintenance, emission optimisation, and intelligent compliance management in maritime operations. Through machine learning-powered sensors and advanced data analytics, shipping companies can now monitor NOx, SOx, and particulate matter emissions in real-time, enabling vessels to adjust scrubber operations and catalytic reduction systems for optimal efficiency during varying voyage conditions. AI-enabled emission control systems are improving fuel efficiency by dynamically managing exhaust treatment operations, helping operators reduce operational costs while meeting stringent global environmental regulations.

The Marine Emission Control Systems Market is witnessing AI integration in emission monitoring systems that automate data collection and reporting under IMO and EU regulations, ensuring compliance while reducing administrative workloads for fleet managers. Intelligent algorithms analyse engine load data and voyage patterns to predict emission peaks, allowing pre-emptive system calibration to minimise environmental impact. AI-powered diagnostics within exhaust treatment units detect and address component degradation early, reducing downtime and repair costs while extending the operational life of scrubber and SCR units. These advancements are also aiding the Marine Emission Control Systems Market by supporting environmentally conscious shipping corridors and decarbonisation initiatives globally, ensuring that emissions remain within permissible limits even in Emission Control Areas (ECAs). The deployment of AI in these systems supports automated compliance verification, empowering decision-makers to maintain sustainable operations while optimising vessel performance.

“In 2024, an AI-based emission monitoring upgrade was installed across 35 LNG carriers by a leading Korean maritime technology provider, achieving a 12% improvement in emission tracking accuracy while reducing manual monitoring efforts by 18% across fleet operations.”

The Marine Emission Control Systems Market is shaped by stringent global environmental regulations, increasing awareness about maritime pollution, and a consistent rise in demand for sustainable shipping practices across key global routes. Heightened enforcement of IMO 2020 sulfur caps, the expansion of Emission Control Areas, and the transition towards decarbonisation are compelling shipping companies to invest in advanced scrubbers, exhaust gas recirculation units, and selective catalytic reduction systems to reduce NOx and SOx emissions effectively. The Marine Emission Control Systems Market is also influenced by the push for LNG and alternative fuels, which complements the adoption of hybrid and closed-loop systems for emission control. The market’s dynamics further reflect technological advancements in emission monitoring, real-time analytics, and the integration of AI to improve system efficiencies and compliance automation, fostering growth in retrofitting activities and new installations across commercial fleets and naval vessels globally.

The imposition of strict emission regulations by the International Maritime Organization and regional authorities is driving technological adoption within the Marine Emission Control Systems Market. The enforcement of the 0.5% global sulfur cap and the establishment of Emission Control Areas with even lower limits are pushing vessel operators to implement advanced scrubbers and catalytic reduction technologies to remain compliant. The need for reducing particulate matter and NOx emissions has led to the deployment of hybrid scrubber systems and selective catalytic reduction units across large container ships and bulk carriers. These regulations are further supported by national governments providing incentives for adopting environmentally sustainable maritime solutions, propelling investments in advanced emission control technologies. Additionally, regulatory frameworks are encouraging the use of continuous emission monitoring systems, driving the demand for integrated, real-time monitoring capabilities within emission control solutions, enhancing operational efficiency while maintaining environmental compliance.

The Marine Emission Control Systems Market faces challenges due to high initial installation costs and complex retrofit procedures associated with advanced scrubber systems and catalytic reduction technologies. Retrofitting older vessels to accommodate large and heavy emission control equipment often requires structural modifications, leading to increased shipyard downtime and additional labour expenses for shipping operators. The high costs of high-grade alloys and corrosion-resistant materials used in scrubbers, along with expenses for automated monitoring and control systems, add to the financial burden for fleet owners. Additionally, the technical complexity of integrating new emission control systems with existing engine configurations and operational processes can lead to delays in project execution, affecting shipping schedules and operational efficiencies. These factors, combined with maintenance complexities and ongoing operational expenditures associated with emission control systems, act as restraints limiting widespread adoption across smaller fleets and operators with tight capital expenditure budgets.

The expansion of LNG-fuelled vessels and the establishment of green shipping corridors are creating significant opportunities in the Marine Emission Control Systems Market. The global shift towards LNG as a cleaner fuel alternative in maritime transport aligns with the need for advanced emission control systems to manage residual emissions effectively, including particulate matter and NOx reduction. Additionally, ports and shipping companies are collaborating on the development of green shipping corridors, where stringent emission standards and low-carbon operations are mandatory, further driving the demand for emission control technologies. The increasing adoption of hybrid scrubber systems in LNG carriers and container ships enables compliance while supporting sustainable maritime operations. With governments and international bodies investing in decarbonisation strategies and promoting eco-friendly shipping practices, the market has opportunities to expand its offerings in automated, AI-powered emission control systems that enhance operational efficiency while reducing environmental footprints across global shipping lanes.

One of the significant challenges in the Marine Emission Control Systems Market is the technical and operational complexity of deploying and maintaining emission control systems in harsh marine environments. Systems such as scrubbers and selective catalytic reduction units require high levels of durability and resistance to corrosion due to continuous exposure to saltwater, high humidity, and extreme temperatures. The marine environment’s challenging conditions often lead to accelerated wear and tear on system components, increasing the frequency and cost of maintenance. Operational challenges also arise in optimising system performance across varying engine loads and voyage conditions, requiring precise calibration to avoid system inefficiencies or failures during transit. Additionally, training crew members to manage advanced emission control systems and respond to system alerts effectively is necessary, adding to operational burdens for shipping companies. These complexities can lead to higher operational risks and unplanned downtimes, impacting shipping schedules and increasing operational costs for maritime operators.

• Adoption of Hybrid Scrubber Systems Expands: The Marine Emission Control Systems market is witnessing a significant shift towards hybrid scrubber systems that allow ships to switch seamlessly between open-loop and closed-loop modes based on regional water discharge regulations. Over 40% of new installations on container vessels in Asia-Pacific now incorporate hybrid scrubbers, ensuring compliance in Emission Control Areas while maintaining operational flexibility during international voyages. This adoption trend is driven by rising demand for flexible compliance solutions and the need to reduce operational downtime associated with scrubber maintenance.

• Integration of Real-Time Emission Monitoring: There is a clear increase in the deployment of real-time emission monitoring technologies across global fleets, enabling precise tracking of SOx, NOx, and particulate emissions during voyages. Over 1,000 vessels globally have integrated advanced emission sensors connected to cloud-based analytics platforms for automated compliance reporting. This trend is improving operational decision-making for shipping companies while ensuring immediate detection of deviations from permissible emission levels, aligning operations with tightening environmental standards.

• Growth in LNG-Fuelled Vessel Installations: The rise in LNG-fuelled vessel orders globally has created higher demand for emission control systems compatible with low-carbon fuels. In 2024 alone, over 120 LNG-powered vessels, including large tankers and container ships, were equipped with advanced emission control systems to manage non-CO₂ pollutants, reflecting a growing preference for LNG to meet emission reduction goals while adhering to regulatory frameworks in high-traffic shipping corridors.

• Automation and AI in Emission Control: Automation and AI integration within the Marine Emission Control Systems market have accelerated, enhancing predictive maintenance and operational optimisation capabilities. Advanced AI algorithms analyse voyage, weather, and engine data to adjust emission control system settings dynamically. Fleets using AI-integrated systems report a reduction of up to 15% in operational costs associated with emission control processes, with over 300 vessels adopting AI-powered monitoring and control modules to enhance system longevity and reduce environmental footprints.

The Marine Emission Control Systems market is segmented by type, application, and end-user, each playing a vital role in shaping its growth and structure. By type, the market includes scrubbers, selective catalytic reduction (SCR) systems, exhaust gas recirculation (EGR) systems, and particulate filters, each catering to specific emission control needs across vessel types. Applications span across cargo ships, passenger vessels, and offshore support vessels, reflecting varying operational requirements and regulatory compliance strategies across shipping segments. End-user segmentation encompasses commercial shipping lines, naval forces, and offshore oil and gas operators, each with distinct investment capabilities and compliance priorities. The segmentation landscape highlights the rising trend of hybrid systems among commercial carriers, the increasing adoption of SCR systems in passenger vessels for NOx reduction, and the strategic retrofitting activities undertaken by naval operators to enhance environmental performance without compromising operational readiness. This structured segmentation ensures targeted technological adoption aligned with regulatory needs and operational efficiency within the Marine Emission Control Systems market.

The Marine Emission Control Systems market includes scrubbers, selective catalytic reduction (SCR) systems, exhaust gas recirculation (EGR) systems, and diesel particulate filters. Scrubbers lead the market due to their effectiveness in reducing sulfur oxide emissions to meet IMO 2020 requirements, with over 3,000 vessels globally equipped with scrubbers as of 2024. Hybrid scrubbers are the fastest-growing type, driven by their dual-mode flexibility that helps operators manage varying environmental regulations across different shipping corridors. SCR systems continue to gain traction, particularly in NOx Emission Control Areas, providing reliable NOx reduction and integration with high-speed engines used on passenger and cargo ships. EGR systems are utilised in new-build vessels to meet Tier III NOx limits, while diesel particulate filters are being adopted on smaller vessels and ferries operating in urban coastal waters to address particulate emission concerns. Each type plays a crucial role in the Marine Emission Control Systems market, aligning with vessel-specific compliance strategies while ensuring operational efficiency and regulatory adherence.

The Marine Emission Control Systems market spans applications across cargo ships, passenger vessels, offshore support vessels, and specialty vessels such as research ships and coastal ferries. Cargo ships are the leading application segment due to the high number of vessels requiring compliance retrofitting with scrubbers and NOx reduction systems to operate within global shipping lanes under stricter environmental regulations. Passenger vessels, including cruise ships and ferries, represent the fastest-growing application area, driven by stringent emission standards in coastal and port areas and the rising public focus on sustainable travel. Offshore support vessels and research ships are integrating advanced emission control systems to comply with environmental guidelines while maintaining operational capabilities for offshore projects and scientific missions. These application areas collectively reflect the Marine Emission Control Systems market’s direction towards reducing maritime emissions across diverse operational profiles, supporting regulatory compliance while advancing environmental sustainability in global shipping.

Key end-user segments in the Marine Emission Control Systems market include commercial shipping lines, naval forces, and offshore oil and gas operators. Commercial shipping lines are the leading end-user segment, actively retrofitting existing fleets with scrubbers and SCR systems to comply with evolving global emission standards while reducing sulfur and nitrogen oxide emissions during long-haul operations. Naval forces represent the fastest-growing end-user segment as defence ministries prioritise the adoption of advanced emission control systems to align with national environmental regulations without compromising mission readiness, with initiatives underway in Europe and Asia to retrofit naval vessels. Offshore oil and gas operators continue to adopt emission control technologies to align with strict environmental guidelines while maintaining platform supply vessel operations and offshore drilling activities. These end-user dynamics illustrate how the Marine Emission Control Systems market is evolving to cater to diverse operational and compliance requirements while supporting global efforts towards decarbonisation and emission reduction in the maritime sector.

Asia-Pacific accounted for the largest market share at 42.3% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The Asia-Pacific Marine Emission Control Systems Market benefits from a strong shipbuilding base in China, South Korea, and Japan, alongside increasing adoption of emission control technologies in LNG-fuelled vessels and large container fleets. Europe’s growth is driven by stringent EU maritime emission directives, the expansion of Emission Control Areas, and government-backed decarbonisation initiatives. Across regions, increasing retrofitting activities on existing fleets, integration of hybrid scrubber systems, and the growing penetration of real-time emission monitoring technologies are enhancing compliance and sustainability goals. Regulatory pressure, coupled with expanding green shipping corridors and port electrification trends, continues to create opportunities for innovative Marine Emission Control Systems across regional markets.

North America holds a 21.7% share in the Marine Emission Control Systems Market, supported by the expansion of retrofit programs in the United States and Canada across large container and cruise fleets. The region’s shipping and offshore oil sectors are major demand drivers, focusing on reducing NOx and SOx emissions to comply with MARPOL Annex VI and the North American ECA regulations. Recent government incentives, such as clean shipping grants and tax credits for adopting emission control technologies, are accelerating installations across key ports. Technological advancements, including AI-powered emission monitoring and hybrid scrubber systems, are transforming operational efficiencies and compliance tracking for fleet operators. Digital transformation across ports, real-time emission tracking, and the implementation of integrated control systems are key trends supporting market expansion while aligning with decarbonisation targets.

Europe holds 28.6% of the Marine Emission Control Systems Market, with Germany, the UK, and France leading adoption through proactive environmental regulations and sustainability initiatives. The European Commission’s push for maritime decarbonisation, alongside the extension of Emission Control Areas in the Baltic and North Seas, has prompted shipping companies to accelerate scrubber retrofitting and NOx reduction system installations. The market is also shaped by the Fit for 55 package, driving stringent compliance for maritime emissions. Advanced technology adoption, including automated emission monitoring, hybrid scrubber solutions, and the integration of AI for real-time compliance management, are prominent across European fleets. The emergence of digitalised ports and investments in clean shipping corridors further reinforce Europe’s role in advancing sustainable maritime practices while driving Marine Emission Control Systems demand.

Asia-Pacific dominates with a 42.3% volume share in the Marine Emission Control Systems Market, led by high demand in China, South Korea, and Japan. These nations benefit from extensive shipbuilding and repair infrastructure, facilitating large-scale retrofitting and the adoption of hybrid scrubber systems across container vessels and LNG-fuelled ships. The growing emphasis on emission reduction in heavily trafficked shipping lanes, along with government policies promoting low-sulfur and low-NOx technologies, is propelling the demand for advanced emission control solutions. Regional innovation hubs are driving the integration of real-time emission monitoring and AI-driven optimisation within emission control systems to enhance operational compliance. The focus on green shipping corridors, combined with investments in modernising fleets with advanced control technologies, positions Asia-Pacific as the leading region for market expansion and technological innovation in emission control.

South America’s Marine Emission Control Systems Market is led by Brazil and Argentina, accounting for 4.8% of the market share driven by growing regional infrastructure and energy sector activities. Brazil’s extensive port and offshore oil operations are key drivers for adopting advanced emission control technologies, while Argentina’s container and bulk carriers are progressively retrofitting with scrubbers to meet environmental regulations. Government incentives for sustainable maritime operations and regional trade partnerships are further supporting technology adoption. The expansion of LNG import facilities and the increasing focus on decarbonisation in maritime logistics are encouraging the implementation of hybrid scrubbers and emission monitoring systems across fleets. South America’s market is also witnessing digital transformation initiatives in ports, facilitating integrated compliance solutions for vessel operators.

Middle East & Africa’s Marine Emission Control Systems Market is influenced by strong demand from the oil and gas and construction sectors, with UAE and South Africa leading regional growth. The market accounts for 2.6% of global share, driven by increasing offshore oil exploration activities and the expansion of maritime logistics supporting regional trade. The adoption of emission control technologies is gaining momentum due to emerging regulations and voluntary sustainability targets among regional shipping companies. Technological modernisation trends, including the integration of emission monitoring and hybrid scrubbers in offshore support vessels and bulk carriers, are becoming evident. Local regulations and trade partnerships under Africa’s maritime sustainability frameworks are further enabling the adoption of advanced emission control solutions, supporting environmental compliance while modernising shipping infrastructure.

China – 26.8%: Dominance due to high production capacity in shipbuilding and extensive retrofitting activities across commercial fleets within the Marine Emission Control Systems Market.

Germany – 14.2%: Strong end-user demand driven by strict environmental regulations and advanced technology adoption in the Marine Emission Control Systems Market.

The Marine Emission Control Systems market features a robust and dynamic competitive environment with over 70 active global and regional players focusing on scrubbers, selective catalytic reduction systems, and exhaust gas recirculation technologies. Market positioning is shaped by continuous product innovation and the ability to deliver customised solutions that meet region-specific regulatory standards across key maritime markets. Strategic initiatives such as partnerships with shipbuilders, collaborations with maritime technology providers, and product launches focused on hybrid scrubber systems and AI-integrated emission monitoring platforms are prevalent within the competitive landscape. Companies are also leveraging digitalisation to enhance predictive maintenance capabilities and real-time monitoring for emission control systems, aligning offerings with the demand for operational efficiency and environmental compliance. Mergers and acquisitions are further consolidating market positions while expanding technology portfolios to cover comprehensive emission control solutions for LNG-fuelled vessels, container ships, and offshore support vessels. The competitive environment is influenced by a focus on sustainability, regulatory adherence, and advancements in modular emission control systems supporting retrofitting across ageing fleets.

Wärtsilä Corporation

Alfa Laval AB

Yara Marine Technologies

MAN Energy Solutions

Mitsubishi Heavy Industries

Clean Marine AS

Ecospray Technologies Srl

Valmet Corporation

Hyundai Heavy Industries

Fuji Electric Co., Ltd.

Technological advancements in the Marine Emission Control Systems market are driving operational efficiencies and compliance with tightening global maritime environmental regulations. Hybrid scrubber systems enabling seamless switching between open-loop and closed-loop operations have gained traction, now representing over 45% of new installations on container and bulk carrier vessels. Selective Catalytic Reduction (SCR) systems with advanced ammonia slip control are being integrated to reduce NOx emissions, particularly within Emission Control Areas, with adoption across over 1,500 vessels globally. Exhaust Gas Recirculation (EGR) systems are also being implemented in new-build vessels to meet Tier III NOx standards while optimising fuel consumption.

Digitalisation is significantly shaping the Marine Emission Control Systems market, with real-time emission monitoring systems being deployed on fleets for automated compliance with IMO and EU directives. AI-powered diagnostics are being incorporated to predict system performance, detect anomalies, and schedule predictive maintenance, reducing operational costs and enhancing the reliability of emission control systems. Advanced materials, including corrosion-resistant alloys and self-cleaning filtration systems, are extending the operational life of scrubbers and SCR units under harsh marine conditions. The integration of cloud-based data platforms with emission control systems is enabling centralised monitoring across fleets, aligning with sustainability goals while enhancing fleetwide transparency and compliance in the Marine Emission Control Systems market.

• In January 2024, Alfa Laval launched a new PureSOx scrubber design with integrated water treatment, reducing water consumption by 30% during scrubbing operations and supporting compliance with stricter port discharge regulations in emission control areas.

• In March 2024, Wärtsilä completed the retrofit of 25 container vessels with hybrid scrubber systems equipped with AI-powered emission monitoring, enabling real-time tracking and operational adjustments, reducing manual monitoring efforts by 20% across the participating fleets.

• In August 2023, Yara Marine Technologies introduced an upgraded SCR system with advanced ammonia slip catalysts, achieving up to 97% NOx reduction while ensuring compliance with Tier III standards in high-traffic emission control zones across Europe and Asia.

• In November 2023, Mitsubishi Heavy Industries developed a compact, modular scrubber unit suitable for small and medium-sized vessels, reducing installation time by 15% while maintaining high sulfur oxide removal efficiency, supporting the retrofitting of coastal fleets.

The Marine Emission Control Systems Market Report comprehensively covers the landscape of advanced technologies, system types, applications, and regional markets shaping the industry’s current and future trajectory. It analyses scrubbers, selective catalytic reduction systems, exhaust gas recirculation units, and particulate filters, assessing their deployment across various vessel categories including container ships, LNG carriers, offshore support vessels, and passenger ferries. The report explores geographic markets across Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, focusing on the unique regulatory and operational environments influencing technology adoption within each region.

Key insights are provided into the integration of hybrid and closed-loop systems, real-time emission monitoring solutions, AI-enabled diagnostics, and modular retrofitting innovations supporting emission reduction efforts in the maritime sector. The report highlights the impact of tightening international regulations, such as MARPOL Annex VI and regional emission directives, on driving market expansion while presenting a detailed overview of fleet retrofitting trends and the role of emerging digitalisation in compliance automation. It outlines niche market opportunities such as emission control in LNG-fuelled vessels and coastal ferries, illustrating the evolving needs of industry players. The scope enables decision-makers to evaluate investment priorities, operational strategies, and competitive positioning within the Marine Emission Control Systems market with precise, actionable insights aligned with environmental and operational performance goals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5833.39 Million |

|

Market Revenue in 2032 |

USD 11203.64 Million |

|

CAGR (2025 - 2032) |

8.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wärtsilä Corporation, Alfa Laval AB, Yara Marine Technologies, MAN Energy Solutions, Mitsubishi Heavy Industries, Clean Marine AS, Ecospray Technologies Srl, Valmet Corporation, Hyundai Heavy Industries, Fuji Electric Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |