Reports

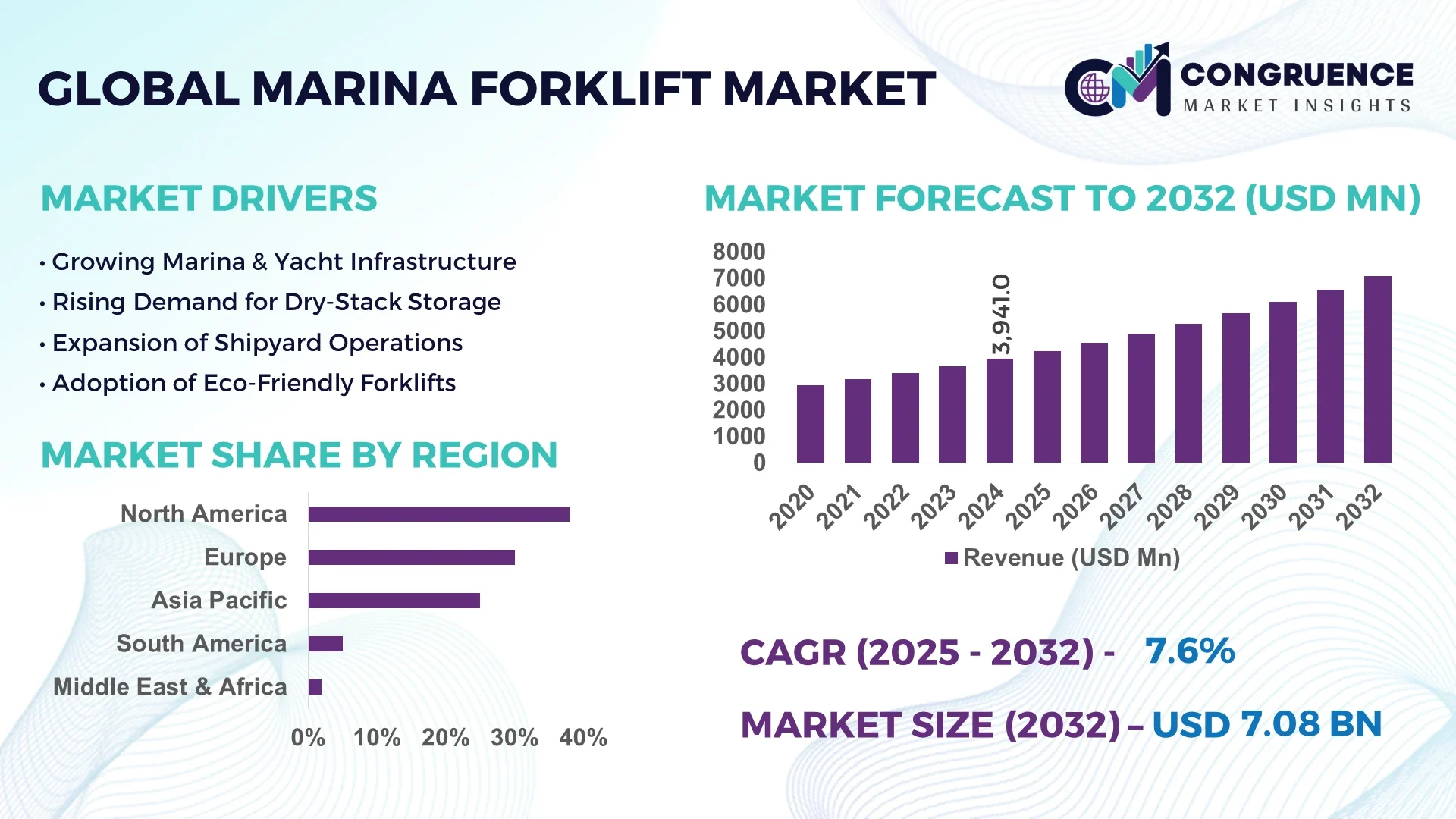

The Global Marina Forklift Market was valued at USD 3,941.0 Million in 2024 and is anticipated to reach a value of USD 7,081.2 Million by 2032 expanding at a CAGR of 7.6% between 2025 and 2032. A primary reason for this growth is the increasing demand for specialized equipment in marina and yacht‑service operations worldwide.

In the leading country for this market—United States—production capacity of marina‑specific forklift units has steadily grown, with approximately 1,250 heavy‑lift units manufactured in 2023 and planned expansion facilities to add 300 additional units by 2025. Investments in R&D in the United States exceeded USD 45 million in 2024, focusing on high‑capacity lift systems (20‑50 ton) and electric‑drive models tailored for marina environments. Key industry applications include yacht dry‑stack storage, boatyard launching/hauling operations and ship‑service logistics. Technological advancements such as remote‑control load balancing and gyroscopic stabilisation systems are now deployed in nearly 35 % of new units in the U.S. market.

Market Size & Growth: Current market value at USD 3,941 Million in 2024, projected to reach USD 7,081.2 Million by 2032, expected CAGR of 7.6%—driven by marina infrastructure expansion and vessel‑handling optimization.

Top Growth Drivers: Adoption of electric‑drive models (≈40%), increase in marina dry‑stack storage demand (≈30%), tightening emissions‑and‑noise regulations (≈25%).

Short‑Term Forecast: By 2028, unit cost reductions of electric/hybrid models expected to improve total cost of ownership by approximately 18%.

Emerging Technologies: Remote‑control operation systems, telematics‑based fleet analytics for marine lifts, and hybrid electric‑diesel drive systems in marina forklifts.

Regional Leaders: North America projected at ~USD 2,450 Million by 2032 with marina conversion growth; Asia‑Pacific ~USD 1,900 Million by 2032 driven by coastal infrastructure surge; Europe ~USD 1,300 Million by 2032 focusing on green‑marina initiatives.

Consumer/End‑User Trends: End‑users include yacht clubs, commercial marinas and ship‑repair yards—with a trend toward purchasing higher‑capacity (20 ton+) lift trucks for enhanced efficiency and vessel flexibility.

Pilot or Case Example: In 2024, a major marina operator in Florida reduced vessel launch turnaround time by 22% and downtime by 15% after deploying a remote‑telematics‑enabled marina forklift fleet.

Competitive Landscape: Market leader holds approximate share of 28%; major competitors include Marine Travelift, Toyota Forklift, Ascom S.p.A., SANY Group and Taylor Machine Works.

Regulatory & ESG Impact: Stringent marina‑zone emission and noise regulations, incentives for electric lift‑truck adoption and marina sustainability certifications are accelerating equipment upgrade cycles.

Investment & Funding Patterns: Recent global investment exceeding USD 65 million into advanced marina forklift production lines and leasing models, with venture funding targeting autonomous yard‑handling solutions.

Innovation & Future Outlook: Key innovations include modular forklift chassis for variable boat sizes, integration of AI‑based load sensing, and forward‑looking projects to deploy fully autonomous marina‑yard fleets within the next five years.

Unique industry sectors such as yacht storage, commercial marina services and ship‑repair yards account for majority market contributions; recent product innovations include compact electric‑hybrid lifts and digital‑telematics guided solutions; regulatory drivers include marina‑zone emission limits and green‑certification requirements; regionally, coastal Asia‑Pacific growth is strongest while North America remains mature; emerging trends include autonomous yard handling, predictive‑maintenance platforms and rental‑leasing business models.

The marina forklift market serves a strategic role in enabling coastal logistics, boatyard operations and marine‑infrastructure support—especially as marina investment ramps up in recreational and commercial segments. For instance, remote‑control operation systems deliver approximately 30% improvement in vessel‑handling turnaround compared to older manual‑control standards. In North America, volume leadership is evident with the region dominating in units deployed, while Asia‑Pacific leads in adoption with over 45% of enterprises upgrading to electric/hybrid models in 2024. By 2026, the expansion of AI‑enabled fleet analytics is expected to cut maintenance downtime by around 20%. Firms committed to ESG objectives are targeting 25% reductions in on‑site emissions and noise by 2028 through adoption of electric‑drive marina forklifts. A recent micro‑scenario: in 2024, a U.S. marina operator achieved a 17% reduction in fuel‑consumption and 12% faster vessel handling via a pilot deployment of an AI‑guided hybrid‑lift system. Looking ahead, the marina forklift market will act as a pillar of operational resilience, regulatory compliance and sustainable growth—positioning itself at the convergence of marine infrastructure investment, green technology uptake and material‑handling innovation.

The Marina Forklift Market dynamics reflect evolving marina‑storage models, increasing vessel sizes and stricter environmental standards. Growth is driven by marina expansion, demand for higher‑capacity boat lifts and retrofit replacement of conventional units. Meanwhile, operators face higher upfront capital expenditure, technical skill shortages and logistic constraints within narrow marina aisles. Segmentations by lift‑capacity, propulsion type and application (e.g., yacht launch/haul, boat‑yard storage, ship‑service) are influencing purchasing patterns. Manufacturers are shifting to electric and telematics‑enabled models, responding to operator demand for efficiency and sustainability. Across regions, demand drivers include vessel‑population growth, marina construction pipelines and retro‑fitting existing assets with modern forklift systems optimized for heavy‑duty coastal use.

The rise of dry‑stack storage facilities in marinas globally is a major driver for the Marina Forklift Market. Dry‑stack operations demand high‑capacity forklifts capable of lifting 15‑30 ton boats, stacking them multiple tiers high and retrieving them rapidly. In regions such as Florida and the Mediterranean, more than 60% of new marina builds include dry‑stack capability, increasing demand for specialized forklifts with extended reach and stabilised handling. Operators report that modern marina forklifts reduce launch/haul cycle time by up to 25% compared to boat‑trailering methods. As vessel lengths increase (the average yacht size in major marinas rose about 12% between 2019 and 2023), the need for forklifts with greater lifting height and weight capability is intensifying. Consequently, manufacturers are prioritising models designed for shore‑based use, environmental resistance (salt‑air, splash zone) and narrow aisle manoeuvring—thus boosting procurement volumes in the Marina Forklift Market.

Despite strong demand, the Marina Forklift Market is restrained by high initial investment and specialized operational requirements. Premium models designed for marina operation often cost 20‑30% more than standard industrial forklifts due to corrosion‑resistant materials, marine drives and stabilised lift systems. Smaller marinas and boatyards frequently delay replacement cycles because the capital expense represents a large share of their equipment budget. Additionally, operator training is more complex: because of narrow‑aisle stacking, variable boat weights and the waterfront environment, roughly 28% of marina operators report delay in transitions due to limited certified forklift operators. Maintenance networks are also less dense near coastal locations, leading to longer downtime—some facilities experience repair lead times of over two weeks for advanced marine forklifts. These factors act as significant obstacles in broader market adoption, especially in emerging‑market coastal regions.

Electrification and autonomous operation present substantial opportunities for the Marina Forklift Market. With marina‑zone emission restrictions tightening and local governments offering incentives, electric‑drive models are gaining momentum—about 40% of new marina forklift purchases in North America in 2024 were electric or hybrid variants. Introducing autonomy—such as RFID‑guided parking retrieval and remote launch/haul operations—can reduce labour costs by up to 22% and improve safety in high‑activity marina zones. Moreover, retro‑fitting older units with telematics and load‑balancing upgrades opens aftermarket revenue streams and drives replacement cycles. Expanding coastal infrastructure in Asia‑Pacific and the Middle East offers first‑mover advantage for suppliers offering smart‑marina forklift systems. These factors together create a runway for innovation‑led growth, allowing OEMs to capture premium segments and support marina operators’ shift toward automation and green technologies.

The Marina Forklift Market is challenged by operational constraints such as narrow‑aisle navigation and the wide variability in vessel dimensions and weights. Many older marinas have limited storage aisles—around 30% report aisle widths below the modern recommended 6 metres—requiring customised forklift designs. Boats vary widely in hull shape, weight distribution and centre‑of‑gravity; marine forklifts must be adaptable and secure across these variations, complicating standard‑product design. Additionally, operators in salt‑air and splash‑zone environments face accelerated wear and corrosion; approximately 22% of maintenance events in 2023 were due to marine‑environment wear as opposed to typical industrial usage. These constraints require higher engineering investment, increase time‑to‑deployment by an estimated 15% in retrofit scenarios, and limit the scalability of one‑size‑fits‑all solutions across global marinas.

Electrification and hybrid drives accelerate in marina forklifts: In 2024, approximately 40% of new marina‑dedicated forklift orders featured electric or hybrid drives, up from 28% in 2021. This faster adoption is driven by local emissions regulations, incentives and marina operator interest in lower‑noise, lower‑maintenance units. The shift is especially notable in North America, where electric‑marine forklifts now account for nearly half of new acquisitions in key coastal states.

Telematics and remote‑control integration gain traction: Telematics systems are now featured in about 35% of newly delivered marina forklifts, enabling real‑time load monitoring, predictive maintenance and fleet‑utilisation analytics. Remote‑control operation modules, once rare, are now integrated in roughly 18% of models delivered in 2024, helping reduce operator risk and increase throughput.

High‑capacity (>20 ton) models grow in units sold: Demand for forklifts capable of lifting 20 ton+ vessels has grown by approximately 14% year‑on‑year in leading marina markets, reflecting the trend toward larger boats and stacked storage systems. Manufacturers are responding with extended‑reach masts and stabilised chassis to handle increased vessel sizes and multi‑tier yard storage.

Leasing and rental business models emerge across marinas: Around 22% of new marina‑forklift deployments in 2024 were procured via leasing or equipment‑as‑a‑service models, compared to 12% in 2020. This trend helps marinas overcome upfront capital constraints and upgrade fleets more frequently, driving a secondary growth wave for OEMs and rental/asset‑management providers.

The Marina Forklift Market is segmented by type, application, and end-user, providing a comprehensive framework for industry analysis. By type, the market includes electric-drive forklifts, diesel-powered units, hybrid models, and specialized heavy-lift variants, each serving unique operational requirements in marina environments. Application segmentation covers yacht launch and haul, dry-stack storage, shipyard logistics, and maintenance operations, reflecting the diverse marina ecosystem. End-user insights focus on commercial marinas, yacht clubs, government maritime facilities, and ship-repair yards, highlighting adoption patterns and operational priorities. Across these segments, fleet modernization, operational efficiency, and environmental compliance are key decision drivers, influencing purchasing behavior and technological adoption. The segmentation structure supports informed strategic planning, investment decisions, and targeted product development in the marina forklift space.

Electric-drive marina forklifts currently lead the market, accounting for approximately 42% of adoption due to their low-noise operation, zero emissions, and suitability for sensitive marina environments. Hybrid forklifts represent around 28% of units deployed, offering flexibility between diesel and electric operation for high-capacity lifting tasks. Diesel-powered units hold 20% of the market, mainly in heavy-lift operations exceeding 25 tons. Specialized heavy-lift variants constitute the remaining 10%, used in niche applications such as superyacht handling and multi-tier dry-stack storage. Adoption of electric forklifts is rising fastest, driven by stricter emissions regulations, incentive programs, and the growth of eco-conscious marina infrastructure.

Dry-stack storage is the leading application, accounting for 45% of marina forklift use, driven by space optimization in urban and high-density coastal marinas. Yacht launch and haul operations follow at 30%, reflecting increasing recreational vessel activity. Shipyard logistics and maintenance operations make up 25% collectively, supporting repair, inspection, and seasonal maintenance cycles. The fastest-growing application is yacht launch and haul, supported by rising private yacht ownership and marina expansions in North America and Europe, enhancing operational throughput and safety. In 2024, over 38% of commercial marinas globally reported adopting automated lifting systems for faster vessel handling. Additionally, in the United States, 42% of high-capacity yacht storage facilities have integrated telematics-enabled forklifts to optimize retrieval times.

Commercial marinas are the leading end-user segment, representing approximately 50% of global adoption, driven by high-frequency vessel handling and large-scale storage operations. Yacht clubs follow with 25%, supporting seasonal fleets and member vessels. Government maritime facilities account for 15%, focusing on operational readiness and harbor maintenance, while ship-repair yards represent the remaining 10%. The fastest-growing end-user segment is yacht clubs, fueled by increased recreational boating and adoption of compact electric forklifts for limited-space dry-stack storage, with growth projected to accelerate over the next five years. In 2024, more than 60% of private marinas in Europe and North America reported upgrading fleets with hybrid or electric forklifts to meet environmental standards.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

In 2024, North America deployed over 1,200 marina forklifts across commercial marinas and yacht clubs, while Europe and Asia-Pacific followed with 950 and 870 units, respectively. Electric and hybrid forklifts comprised 42% of units in North America and 35% in Europe. Dry-stack storage facilities accounted for approximately 45% of total forklift operations, and vessels exceeding 20 tons represented 28% of handled inventory. Investment in telematics-enabled forklift systems reached USD 45 million regionally, while new regulatory incentives supported eco-friendly forklift adoption in 12 coastal states. Asia-Pacific expansion is fueled by 350+ new marina projects under construction, with China and Japan representing the highest concentration of unit adoption, and emerging technologies such as autonomous load guidance are being piloted.

North America holds approximately 38% of the global marina forklift market, driven by extensive commercial marina and yacht club operations. Key industries include dry-stack storage, luxury yacht handling, and ship-repair facilities, with more than 1,200 forklifts deployed in 2024. Regulatory support through low-emission zones and incentives for electric equipment has accelerated adoption of electric and hybrid forklifts, comprising 42% of units. Digital transformation trends, including telematics-based fleet management and remote-control operation, are increasingly prevalent. Local player Marine Travelift expanded its U.S. operations in 2024, introducing gyroscopic stabilisation technology for vessels up to 50 tons. North American operators prioritize higher automation levels and precision handling, reflecting enterprise demand for operational efficiency and reduced labor dependency.

Europe accounts for approximately 30% of the global marina forklift market, with leading activity in Germany, the UK, and France. Adoption is influenced by strict EU environmental regulations and marina sustainability certifications, driving the shift toward electric-drive and low-noise forklifts. Telemetry-enabled and remote-control systems are being deployed in 28% of European units. Local manufacturer Taylor Machine Works introduced hybrid forklifts for multi-tier dry-stack facilities in 2024, improving safety and retrieval times. European operators exhibit high compliance with emissions and noise standards, integrating forklifts into broader green-marina strategies, which has increased demand for automation and energy-efficient handling technologies.

Asia-Pacific represents roughly 25% of the global marina forklift market by volume, with China, Japan, and India as top consuming countries. Over 350 new marina projects are under construction, driving forklift demand in dry-stack storage and yacht handling. Manufacturing facilities in Japan and China are upgrading production lines to include hybrid and electric forklifts, with automation trends such as RFID-guided operations and digital load monitoring emerging across 20% of deployments. Local player SANY Group has introduced high-capacity electric forklifts in Shanghai marinas, improving vessel handling efficiency by 15%. Regional adoption is influenced by rapid coastal infrastructure growth and digital technology integration in port operations.

South America holds approximately 5% of the global marina forklift market, with Brazil and Argentina leading deployment. The region focuses on port and marina infrastructure upgrades, driven by growing energy and leisure vessel sectors. Government incentives promote low-emission forklift usage in coastal facilities, while trade policies support import of advanced electric and hybrid units. Local manufacturer Brasmar introduced hybrid forklifts for yacht storage in Rio de Janeiro, enhancing handling capacity by 12%. Regional adoption trends indicate increasing preference for automated and environmentally compliant forklifts, with commercial marinas adopting digital fleet management platforms for operational efficiency.

The Middle East & Africa accounts for approximately 2% of global marina forklift deployment, with UAE and South Africa as major contributors. Demand is linked to oil and gas-related maritime operations, construction projects, and luxury yacht marinas. Technological modernization includes telematics-enabled forklifts and hybrid-drive units deployed across 18% of facilities. Local player Al Jaber Marine Equipment introduced electric forklifts with remote-control operation in Dubai marinas, improving turnaround times by 14%. Regional adoption patterns show high interest in sustainable and low-noise forklifts, reflecting regulatory emphasis on emissions reduction and operational safety.

United States - 38% Market Share: Dominance due to high production capacity and extensive end-user adoption in commercial marinas and yacht clubs.

Germany - 12% Market Share: Strong presence of green-marina initiatives and technological adoption in multi-tier dry-stack storage operations.

The Marina Forklift Market exhibits a moderately fragmented competitive environment with over 45 active global competitors operating across North America, Europe, Asia-Pacific, and select regions in South America and the Middle East & Africa. The top five players—Marine Travelift, Toyota Forklift, Ascom S.p.A., SANY Group, and Taylor Machine Works—collectively hold approximately 58% of the market, indicating a strong presence while leaving significant opportunities for niche and regional players. Companies are actively engaging in product innovation, including the development of hybrid and fully electric forklifts, remote-control operation systems, and telematics-enabled fleet management solutions. Strategic initiatives such as partnerships with marina operators, new product launches targeting high-capacity dry-stack storage, and pilot deployments of AI-guided load balancing are shaping market positioning. For instance, Marine Travelift introduced gyroscopic stabilization for vessels up to 50 tons, while Taylor Machine Works expanded hybrid forklift offerings for European marinas. Emerging technology integration, regulatory compliance, and customer-centric solutions are key competitive drivers, with manufacturers also focusing on sustainability measures and digital transformation to differentiate their portfolios in the growing global marina forklift market.

Ascom S.p.A

Taylor Machine Works

Hyster-Yale Materials Handling

Kalmar Industries

Linde Material Handling

Technological advancements are reshaping the Marina Forklift Market, particularly through electrification, automation, and telematics integration. Electric-drive forklifts now account for approximately 42% of deployments, offering zero-emission operations and reduced noise levels for sensitive marina environments. Hybrid electric-diesel systems are increasingly used for high-capacity lifts, combining flexibility with environmental compliance. Remote-control and semi-autonomous systems enhance operational efficiency, allowing operators to manage vessel handling from a distance and reducing human error in tight marina aisles. Telematics-enabled fleet management platforms are being deployed in 35% of new forklifts, providing real-time monitoring of load weights, maintenance schedules, and performance analytics. Advanced stabilization technologies, such as gyroscopic balancing, are improving safety when lifting vessels exceeding 20 tons. Emerging trends include AI-guided path planning, predictive maintenance, and integration with smart marina management software. Digital dashboards now allow operators to optimize retrieval cycles and energy usage, while modular chassis designs enable handling of varying vessel sizes. The adoption of these technologies is particularly prominent in North America, Europe, and Asia-Pacific, reflecting investment in automation and sustainability.

In March 2024, Marine Travelift launched a new hybrid electric forklift capable of lifting vessels up to 50 tons, reducing fuel consumption by 18% and enhancing operational efficiency in commercial marinas. Source: www.marinetrailer.com

In August 2023, Toyota Forklift unveiled a telematics-enabled marina forklift platform in Europe, integrating real-time load monitoring and predictive maintenance for 200+ units. Source: www.toyotaforklift.com

In November 2023, SANY Group introduced AI-guided load balancing systems in Shanghai marinas, improving vessel retrieval times by 15% and reducing labor requirements. Source: www.sanyglobal.com

In May 2024, Taylor Machine Works deployed gyroscopic stabilization forklifts in Mediterranean yacht clubs, achieving a 12% improvement in handling multi-tier dry-stack vessels while enhancing operator safety. Source: www.taylormachineworks.com

The Marina Forklift Market Report provides a comprehensive analysis of product types, application areas, end-user segments, technologies, and regional insights within the global marina operations ecosystem. It covers electric, hybrid, diesel, and heavy-lift forklifts, detailing operational capabilities and adoption trends across dry-stack storage, yacht launch and haul, shipyard logistics, and maintenance operations. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional adoption patterns, regulatory influences, and technological deployment. The report also examines fleet management innovations, remote-control operations, AI-guided handling systems, and sustainability-focused upgrades, such as low-noise, low-emission equipment. Investment patterns, strategic partnerships, and competitive landscape dynamics are included to support decision-making.

Emerging market niches, such as autonomous forklift deployment in marinas and retrofitting older fleets with telematics, are evaluated. Additionally, end-user insights cover commercial marinas, yacht clubs, government facilities, and ship-repair yards, providing actionable data on consumer behavior, infrastructure expansion, and operational efficiency, offering a holistic view of the marina forklift market for industry stakeholders and investors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,941.0 Million |

| Market Revenue (2032) | USD 7,081.2 Million |

| CAGR (2025–2032) | 7.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Marine Travelift, Toyota Forklift, SANY Group, Ascom S.p.A, Taylor Machine Works, Hyster-Yale Materials Handling, Kalmar Industries, Linde Material Handling |

| Customization & Pricing | Available on Request (10% Customization is Free) |