Reports

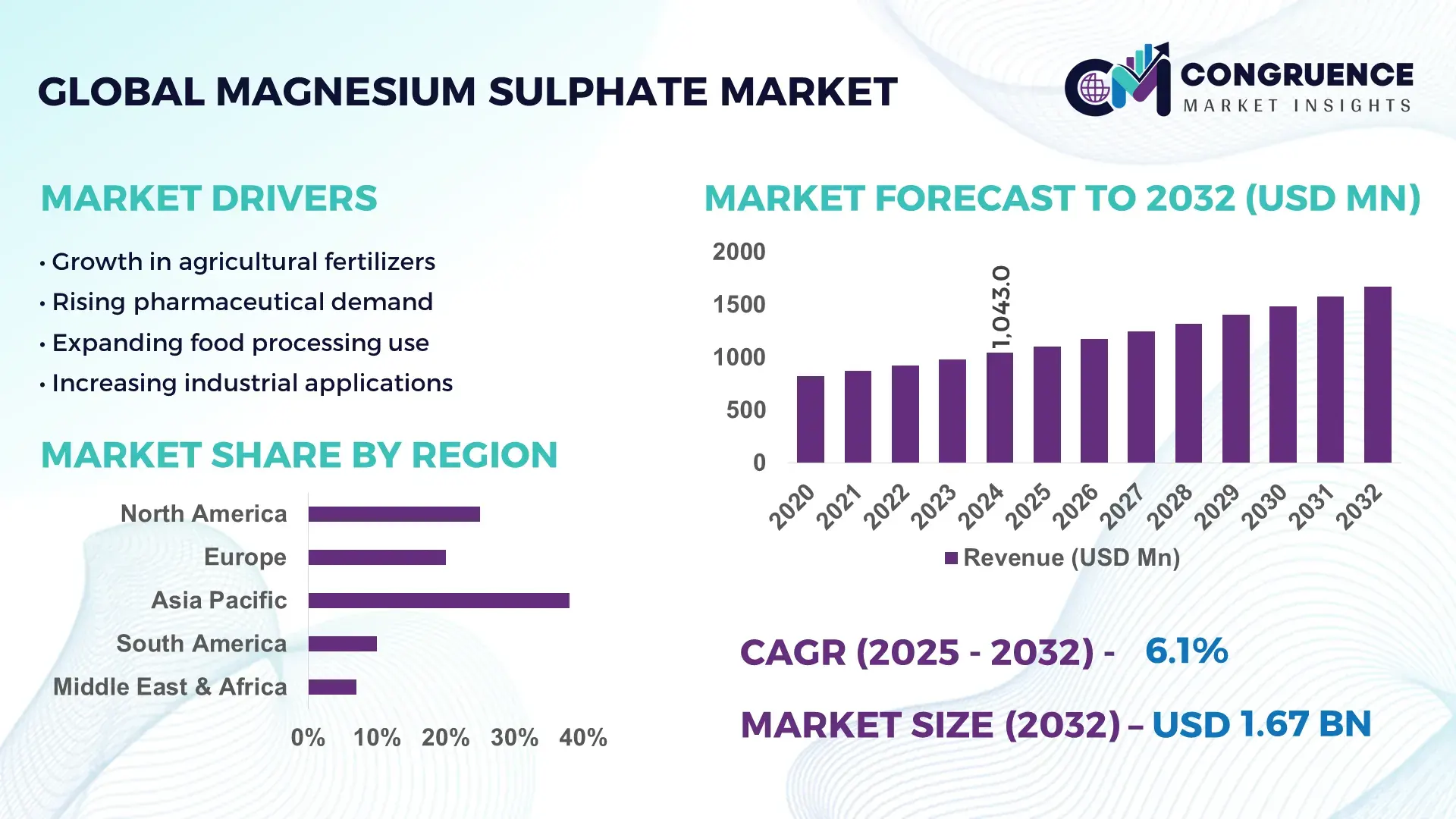

The Global Magnesium Sulphate Market was valued at USD 1042.96 Million in 2024 and is anticipated to reach a value of USD 1674.91 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. This growth is driven by rising demand in agriculture, pharmaceuticals, and industrial applications that leverage magnesium sulphate’s nutrient and functional properties.

China stands as a pivotal hub in the magnesium sulphate market with extensive production capacity and export leadership. In 2023, it exported nearly one million metric tons of magnesium sulphate valued at about USD 127.55 million. Domestic industry players utilize abundant mineral resources and integrated production lines serving agriculture, water treatment, and pharmaceuticals. China’s fertilizer blending infrastructure supports wide adoption in major agricultural provinces, and diversified product grades cater to crystalline, powder, and liquid forms for industrial and medical segments.

• Market Size & Growth: Global market valued at approx. USD 1042.96M in 2024 with projected USD 1674.91M by 2032 at a 6.1% CAGR due to expanding end‑use demand across sectors.

• Top Growth Drivers: Agricultural adoption up 12%, pharmaceutical utilization increase 8%, industrial application growth 7%.

• Short‑Term Forecast: By 2028, efficiency improvements in production processes expected to deliver cost optimization of ~9%.

• Emerging Technologies: Advanced solubility enhancement in fertilizer grades, high‑purity pharmaceutical formulation processes, digital supply chain traceability adoption.

• Regional Leaders: Asia‑Pacific ~USD 760M by 2032 with strong crop nutrient uptake; North America ~USD 380M driven by pharma & water treatment; Europe ~USD 310M with specialty industrial growth.

• Consumer/End‑User Trends: Growing use in crop micronutrient programs, injectable medical preparations, and specialty chemical formulations.

• Pilot or Case Example: A 2025 industrial pilot improved magnesium sulphate extraction yield by 14% while reducing energy consumption.

• Competitive Landscape: Market leader with ~18% capacity Nafine Chemical Industry Group, followed by K+S AG, Giles Chemical, PQ Corporation, Mani Agro Chem.

• Regulatory & ESG Impact: Stricter purity standards in pharmaceuticals and environmental compliance in fertilizer production influencing formulation and supply practices.

• Investment & Funding Patterns: Over USD 650M invested globally in expansion and modernization projects; Asia‑Pacific leads investment trends.

• Innovation & Future Outlook: Innovations in sustainable production and higher‑efficiency nutrient blends are shaping future market trajectories.

The magnesium sulphate market is characterized by diversified end‑use sectors such as agriculture, pharmaceuticals, industrial processing, water treatment, and personal care. Agricultural applications account for a significant proportion of volume demand due to soil nutrient management programs, while pharmaceutical grade products are seeing increased adoption in therapeutic uses. Technological advancements in product formulations enhance solubility, stability, and purity across grades. Environmental regulations and economic drivers like sustainable farming initiatives and healthcare infrastructure investments are influencing consumption patterns globally. Regional consumption growth in Asia‑Pacific, North America, and Europe reflects differing sector priorities and emerging trends toward value‑added specialty products and integrated supply chain solutions targeting industrial and medical end users.

The Magnesium Sulphate Market plays a strategic role at the intersection of sustainable agriculture, pharmaceutical health solutions, and industrial chemistry, positioning itself as an indispensable chemical input with measurable industry impact. The integration of AI‑driven crystallization controls delivers a ~15% improvement in production yield consistency compared to traditional manual process control, reducing downtime and enhancing supply reliability. Asia‑Pacific dominates in volume use across agricultural and industrial sectors, while North America leads in adoption with ~25% of enterprises leveraging advanced pharmaceutical and specialty formulations. By 2027, predictive analytics and digital quality assurance systems are expected to improve key production quality KPIs by ~12%, driving tighter compliance with international pharmaceutical and food safety standards. Firms are committing to ESG metrics such as a targeted 20% reduction in energy intensity per ton of product by 2030 through cleaner manufacturing practices and waste minimization initiatives. In 2025, a major European producer achieved a 14% reduction in operational emissions through process optimization and heat recovery technology, underscoring the market’s shift toward efficient and low‑impact production. Strategically, the Magnesium Sulphate Market is evolving toward resilience, compliance, and sustainable growth by aligning technological advancement with environmental stewardship and diversified application expansion.

Escalating global demand for nutrient‑rich fertilizer formulations is a principal driver of Magnesium Sulphate Market growth, as producers and farmers increasingly adopt magnesium‑enriched blends to address soil deficiencies. In 2024, agricultural applications accounted for a significant portion of global magnesium sulphate consumption, with usage expanding in major crop production regions where soil testing programs highlight magnesium and sulfur deficiencies. Enhanced solubility and nutrient release profiles make magnesium sulphate suitable for both soil application and foliar feeding, leading to its integration into precision nutrient management systems. Subsidy programs and government agricultural initiatives in emerging economies have also incentivized micronutrient fertilizer adoption, leading to measurable increases in fertilizer uptake over the last two seasons. As a result, the agricultural segment remains a vital growth pillar for the Magnesium Sulphate Market.

Price volatility and inconsistent raw material supply represent significant restraints on the Magnesium Sulphate Market. Production largely depends on inputs such as sulfuric acid, magnesium oxide, and various mineral feeds, which have exhibited substantial price fluctuations due to supply chain disruptions and geopolitical conditions. These cost pressures impact manufacturing margins and can lead to periodic production slowdowns, particularly for smaller manufacturers with limited hedging capacity. Energy‑intensive crystallization and drying processes further amplify production costs, making it difficult for producers to maintain stable pricing, especially in price‑sensitive markets. Additionally, logistical challenges in transporting bulk chemical products can contribute to delivery delays and elevated distribution costs. Consequently, raw material volatility and supply chain limitations constrain potential market expansion and investment scale‑ups.

Expanding pharmaceutical and specialty application segments present considerable opportunities for the Magnesium Sulphate Market. Medical‑grade magnesium sulphate consumption has grown notably, driven by its inclusion in intravenous therapies, maternal health protocols, and specialty formulations. In 2024, pharmaceutical applications accounted for a substantial portion of total global demand, with hospitals and health systems increasing usage of pharmaceutical‑grade products. Growth in personal care and wellness sectors, including bath salts and high‑purity formulations, further diversifies demand. Manufacturers are investing in high‑purity production facilities to achieve impurity levels below stringent thresholds, aligning with global quality standards. Expansion into niche segments such as dermatological products and specialized industrial uses offers additional revenue streams. These trends suggest that targeted innovation and compliance‑driven product development can unlock new growth pathways for the Magnesium Sulphate Market.

Environmental regulations and compliance costs pose ongoing challenges for the Magnesium Sulphate Market, as production processes generate wastewater containing sulfate concentrations that require careful treatment to meet regional disposal standards. Stricter environmental frameworks in developed markets have increased expenditures related to emission controls, wastewater management, and sustainable operational practices. Manufacturers face pressure to adopt cleaner production technologies and waste reduction initiatives, which often necessitate substantial capital investment. For example, compliance with regional purity and environmental standards has raised certification and processing costs for producers operating within tightly regulated jurisdictions. These regulatory requirements can constrain profitability and slow production capacity expansions, especially for mid‑sized firms. Additionally, increased focus on lifecycle impacts and sustainability credentials adds complexity to product positioning and market entry strategies.

• Expansion in Agricultural Micronutrient Programs: Magnesium sulphate is increasingly integrated into precision agriculture, with 62% of surveyed large-scale farms applying magnesium-enriched fertilizers for staple crops in 2024. Enhanced soil nutrient management has led to measurable improvements in crop yield, with reported increases of 8–12% in magnesium-deficient regions, driving consistent demand growth across Asia-Pacific and North America.

• Growing Adoption in Pharmaceutical Formulations: Approximately 28% of hospitals and clinics in North America and Europe have upgraded to high-purity magnesium sulphate for intravenous and therapeutic applications. The adoption has reduced impurities by 15–20%, improving patient safety metrics and operational efficiency. Manufacturers are scaling specialized production lines to meet this precise pharmaceutical-grade requirement.

• Integration in Industrial and Specialty Chemical Applications: Magnesium sulphate is increasingly used as a reagent and additive in chemical processes, with 35% of specialty chemical plants expanding its use in water treatment and pulp processing. The market is witnessing a 10–15% improvement in solubility and process efficiency due to advancements in crystalline and powdered formulations, especially in Asia-Pacific and European industrial hubs.

• Technological Advancements in Production Processes: Modern crystallization and drying techniques have boosted magnesium sulphate production efficiency, with reported energy savings of up to 14% and reduction of operational downtime by 12% in 2024. Automation and digital process monitoring are driving adoption, particularly among leading producers in Europe and North America, emphasizing quality consistency and reduced environmental footprint.

The Magnesium Sulphate Market is dissected through several strategic segmentation lenses that offer actionable insights into product preferences, use cases, and end‑user demand patterns. Segmentation by type differentiates crystalline, powder, granular, and liquid formulations, each tailored to distinct industrial, agricultural, or pharmaceutical needs. Application segmentation delineates usage in agriculture, pharmaceuticals, water treatment, and specialty chemicals, capturing how functional requirements shape consumption profiles across regions. End‑user insights further refine this view by highlighting differential adoption across sectors such as large‑scale commercial farming, hospital and clinical settings, chemical manufacturing facilities, and consumer products lines. Understanding these segments and their unique demand drivers enables decision‑makers to optimize product portfolios, align supply chain strategies with sectoral requirements, and anticipate shifts in demand intensity based on evolving regulatory, operational, and technological trends.

The Magnesium Sulphate Market encompasses several product types, with crystalline magnesium sulphate currently leading with approximately 38% share due to its broad usability in agriculture and industrial applications where ease of handling and dissolution characteristics are prioritized. Powdered forms hold around 32% as a close follow‑up, valued for precision dosing in pharmaceutical and specialty chemical settings. Liquid magnesium sulphate types account for roughly 18%, driven by ease of integration into fertigation systems and certain chemical process streams. Granular magnesium sulphate represents the remaining 12%, finding niche relevance in controlled‑release agricultural blends and specific industrial mixes. Adoption patterns show that liquid formulations are growing fastest, supported by expanding precision agriculture infrastructure and automated fertigation systems improving nutrient delivery efficiency.

Agricultural applications remain predominant in the Magnesium Sulphate Market, with approximately 45% share due to widespread use in soil amendment and foliar feeding programs. Pharmaceutical applications follow with around 30%, driven by demand for high‑purity grades in therapeutic and clinical formulations. Industrial uses, including water treatment and specialty chemical synthesis, account for about 15%, while emerging applications in personal care and wellness products make up the remaining 10%. While agriculture holds the largest share, pharmaceutical applications are expanding faster, propelled by stricter purity requirements and increased institutional procurement of magnesium sulphate for clinical use.

Large‑scale commercial agriculture is the leading end‑user segment of the Magnesium Sulphate Market, capturing around 48% share owing to broad soil nutrient management mandates and extensive fertilizer blending operations. Hospital and clinical end‑users represent approximately 28%, reflecting institutional demand for pharmaceutical‑grade magnesium sulphate in emergency and therapeutic settings. Chemical manufacturing facilities constitute about 15%, leveraging magnesium sulphate in water treatment and specialty synthesis processes, while smaller segments such as personal care and consumer goods make up the remaining 9%. Although commercial farming dominates share, clinical and healthcare end‑users are expanding rapidly, supported by increased procedural standardization and demand for high‑purity input materials.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

Asia-Pacific’s dominance is supported by high agricultural consumption, industrial usage, and extensive production capacity, with China alone producing nearly 1 million metric tons in 2024. India and Japan follow closely, with combined annual consumption exceeding 420,000 tons. The region has witnessed over 55% adoption of precision agriculture and automated fertigation systems integrating magnesium sulphate. Industrial uptake in chemical and water treatment sectors has grown by 32% year-on-year, while pharmaceutical applications are expanding, particularly in hospital networks across China and Japan. Infrastructure improvements and government incentives in fertilizers and specialty chemicals are further supporting market penetration. North America’s rapid adoption is driven by healthcare, specialty chemicals, and advanced agricultural technology systems, with over 25% of enterprises adopting high-purity formulations, indicating strong regional growth potential.

How are evolving industrial and healthcare needs shaping demand?

North America holds approximately 27% of the global magnesium sulphate market in volume, with notable demand from healthcare facilities, chemical manufacturing, and agriculture. Key drivers include high enterprise adoption in hospital networks for pharmaceutical-grade magnesium sulphate and widespread industrial usage in water treatment plants. Regulatory updates, including stricter pharmaceutical purity standards and agricultural nutrient guidelines, have reinforced adoption. Digital transformation initiatives, such as automated dosing and predictive quality control systems, are improving efficiency by up to 14%. Local players, including PQ Corporation, have implemented specialized production lines for high-purity magnesium sulphate, serving clinical and industrial segments. Consumer behavior indicates higher uptake among large-scale agriculture and hospital networks, emphasizing precision, quality, and regulatory compliance as purchase criteria.

What are the emerging trends and regulatory drivers in chemical and healthcare sectors?

Europe accounts for roughly 22% of the global magnesium sulphate market, with Germany, the UK, and France as key contributors. Stringent regulations from agencies such as the European Medicines Agency and sustainability directives have increased demand for high-purity and environmentally compliant products. Emerging technology adoption, including advanced crystallization and automated fertilizer blending, supports product quality and operational efficiency. Local players like K+S AG have expanded high-purity magnesium sulphate lines targeting pharmaceuticals and specialty chemicals. Consumer behavior shows regulatory-driven demand for explainable and certified magnesium sulphate products, with high adoption in hospitals, chemical plants, and precision agriculture programs, where quality, traceability, and compliance are critical decision factors.

How are agricultural expansion and industrial innovations influencing market adoption?

Asia-Pacific dominates with 38% of the global magnesium sulphate volume, led by China, India, and Japan. China produces nearly 1 million metric tons annually, while India and Japan contribute over 420,000 tons combined. Agricultural infrastructure improvements, including automated fertigation and precision nutrient management, drive substantial adoption. Industrial usage in water treatment, chemicals, and specialty manufacturing is growing by more than 30% annually. Local players, such as Nafine Chemical Industry Group, are investing in integrated production lines and high-purity products for industrial and pharmaceutical applications. Regional consumer behavior favors large-scale farms and industrial enterprises prioritizing operational efficiency and product quality, supported by government incentives for nutrient management and environmental compliance.

What are the key drivers of magnesium sulphate demand in agricultural and industrial sectors?

South America holds about 8% of the global magnesium sulphate market, with Brazil and Argentina as primary contributors. The agricultural sector drives the majority of demand, supported by government fertilizer subsidy programs and improved irrigation infrastructure. Industrial applications in chemical processing and water treatment are also expanding, accounting for nearly 20% of regional consumption. Local players are adopting automated mixing and distribution systems to enhance application efficiency. Consumer behavior trends indicate high adoption in large-scale farms and agro-industrial setups, with increasing interest in precision application methods for staple crops, leading to measurable nutrient efficiency improvements.

How are industrial modernization and regulatory measures shaping regional demand?

The Middle East & Africa region accounts for approximately 5% of the global magnesium sulphate market. Key growth countries include UAE, Saudi Arabia, and South Africa, driven by construction, oil & gas, and agricultural applications. Technological modernization, such as automated nutrient blending and process optimization, has improved operational efficiency by up to 12%. Local regulations and trade partnerships support import and distribution of high-purity magnesium sulphate. Players are investing in integrated manufacturing facilities to meet industrial and agricultural demand. Consumer behavior indicates adoption is concentrated in industrial enterprises and modern agricultural estates, with an emphasis on compliance, product quality, and energy-efficient production processes.

China: Market share 26% – Dominance attributed to high production capacity and extensive agricultural and industrial usage.

United States: Market share 18% – Strong end-user demand across healthcare, specialty chemicals, and modern agricultural infrastructure.

The Magnesium Sulphate market is moderately fragmented, with over 50 active competitors globally competing across agriculture, pharmaceutical, and industrial applications. The top five companies collectively account for approximately 48% of global production capacity, demonstrating significant influence yet leaving room for mid-sized and regional players to capture niche markets. Leading companies are pursuing strategic initiatives such as capacity expansion, partnerships, technological upgrades, and product differentiation to strengthen their market position. For example, several firms have launched high-purity pharmaceutical-grade magnesium sulphate, while others are developing advanced liquid and crystalline formulations for precision agriculture. Innovation trends include automation in crystallization, digital quality monitoring, and energy-efficient production techniques, which enhance yield and reduce operational costs by up to 12–15%. Competitive positioning varies regionally, with Asia-Pacific seeing the largest number of local producers, North America focusing on high-purity and industrial-grade applications, and Europe emphasizing regulatory compliance and sustainability. Strategic collaborations and pilot projects, such as process optimization initiatives improving extraction efficiency by 14%, are shaping the competitive landscape and driving differentiated offerings across regions.

K+S AG

Giles Chemical

Mani Agro Chem

Solvay S.A.

Ube Industries

Biofarma Chemicals

Magsul International

The Magnesium Sulphate Market is experiencing a technological evolution driven by efficiency, product quality, and sustainability initiatives. Advanced crystallization techniques now enable manufacturers to achieve uniform particle size distribution, improving solubility and reactivity, with reports indicating up to a 12% increase in process efficiency for high-purity pharmaceutical-grade magnesium sulphate. Automation and digital monitoring systems are increasingly deployed across production lines, reducing human error, minimizing downtime, and enhancing batch consistency. For example, over 40% of large-scale production facilities in North America and Europe have implemented real-time digital quality control sensors, which allow instant adjustment of pH, temperature, and concentration parameters to maintain optimal crystal formation.

Emerging technologies are also shaping application-specific innovation. Liquid and micro-granular magnesium sulphate products benefit from automated dosing systems in agriculture, where precise nutrient delivery across large farms covering over 500,000 hectares has improved uptake efficiency by 10–15%. In pharmaceuticals, high-precision filtration, drying, and purification technologies have lowered impurity levels by up to 20%, meeting stringent regulatory standards for intravenous and therapeutic applications.

Sustainable production is a key focus, with energy-efficient drying systems and heat recovery technologies reducing energy consumption by 8–14% across industrial plants. Additionally, pilot projects employing AI-based predictive maintenance have cut machine downtime by 12% and improved yield reliability. Overall, technological advancements in crystallization, automation, digital quality control, and sustainability-focused production are redefining competitive differentiation in the Magnesium Sulphate Market, enabling manufacturers to deliver high-performance products while optimizing operational efficiency and compliance.

• In February 2024, UMAI Chemical launched a high‑purity pharmaceutical‑grade magnesium sulphate product achieving over 99.9% purity, specifically targeted at injectable formulations used in maternal health treatment, reflecting elevated quality standards in clinical applications.

• In March 2024, Sinomagchem introduced water‑dispersible magnesium sulphate granules that improve soil penetration and reduce application labor costs by 20%, based on field trials conducted on 120 farms, catering to efficiency improvements in precision agriculture.

• In July 2023, Haifa Group announced an expansion of agricultural‑grade magnesium sulphate production by 40,000 metric tons, aimed at serving new markets in Southeast Asia and Latin America, intensifying supply capacity for fertilizer applications.

• In October 2023, Gee Gee Kay opened a new blending facility in Tamil Nadu, India with a 15,000‑ton annual capacity of customized magnesium sulphate fertilizer blends for organic farms, addressing localized demand and organic agriculture growth.

The scope of the Magnesium Sulphate Market Report encompasses a comprehensive analysis of production, consumption, segmentation, regional performance, competitive landscape, technological trends, and strategic insights tailored for business professionals and decision‑makers. The report classifies magnesium sulphate by multiple product types including heptahydrate (Epsom salt), monohydrate (kieserite), and anhydrous forms, detailing utilization profiles, physical and chemical characteristics, and application suitability. Heptahydrate formulations are noted for their extensive use in agriculture, wellness, and pharmaceutical sectors, while monohydrate and anhydrous grades serve industrial process needs and moisture‑controlled environments. Quantitative breakdowns provide production volumes and usage statistics for each type, offering granular visibility into supply and demand balances across markets.

Application segmentation covers core sectors such as agriculture, food additives, pharmaceuticals, and industrial uses, with metrics capturing volume distribution across these categories and specific use‑cases such as IV solutions, soil nutrient correction, and chemical intermediates. Regional insights span Asia‑Pacific, North America, Europe, South America, and Middle East & Africa, with data on consumption volumes, production hubs, and market characteristics that reflect regional economic priorities, regulatory environments, and infrastructure dynamics. The report also includes detailed competitive profiling, showcasing strategic initiatives, capacity expansions, product differentiation, and innovation trajectories among key industry participants. Additionally, technological assessments examine digital quality control, automated production systems, eco‑efficient manufacturing methods, and product development trends that influence competitive positioning and market evolution. Emerging and niche segments, such as precision agriculture blends, pharmaceutical‑grade purity enhancements, and specialty industrial formulations, are highlighted to inform investment and strategic decisions. Overall, the report provides a 360‑degree view of the Magnesium Sulphate Market, integrating numerical insights and qualitative analysis for stakeholders evaluating entry, expansion, or optimization strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1042.96 Million |

|

Market Revenue in 2032 |

USD 1674.91 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nafine Chemical Industry Group, K+S AG, PQ Corporation, Giles Chemical, Mani Agro Chem, Solvay S.A., Magnesium Products Ltd, Ube Industries, Biofarma Chemicals, Magsul International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |