Reports

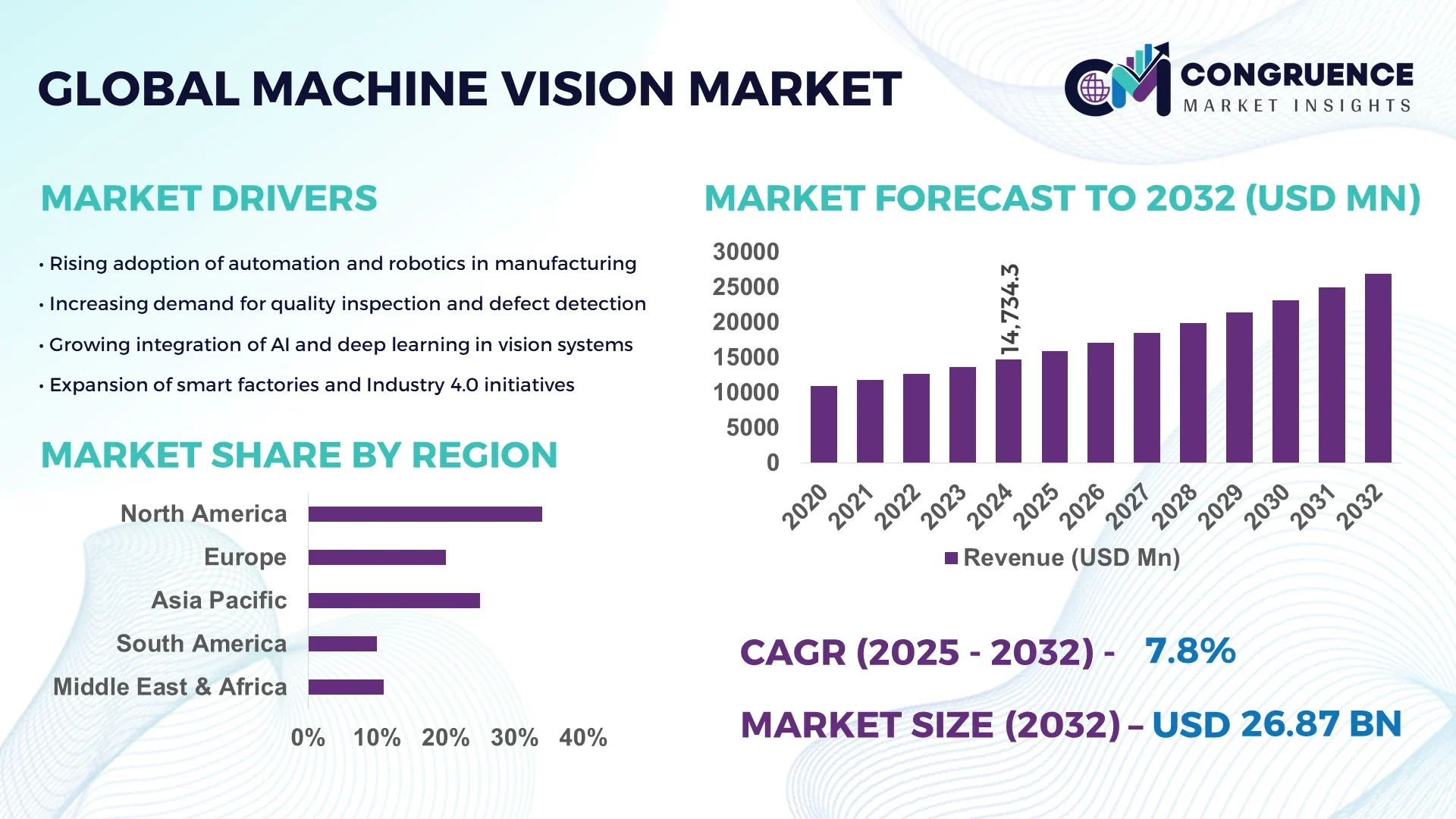

The Global Machine Vision Market was valued at USD 14,734.29 Million in 2024 and is anticipated to reach a value of USD 26,870.72 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. This growth is primarily driven by increasing automation in industrial manufacturing and advancements in AI-powered inspection systems.

In the United States, the dominant country in the Machine Vision market, production capacity exceeds 1.2 million units annually, supported by investments of over USD 1.5 billion in research and development in 2024. Key industry applications include semiconductor inspection, automotive quality control, and food and beverage packaging. Technological advancements such as multi-sensor 3D imaging and high-speed AI-driven inspection systems have been widely deployed, with consumer adoption in automated manufacturing lines reaching 68% by 2024. Regional segmentation indicates the Midwest leads in industrial deployment, while the West Coast focuses heavily on AI-enabled vision solutions.

Market Size & Growth: USD 14,734.29 Million in 2024, projected USD 26,870.72 Million by 2032, CAGR 7.8% due to rising industrial automation and AI adoption.

Top Growth Drivers: Automation adoption 62%, quality inspection efficiency 48%, defect detection accuracy 55%.

Short-Term Forecast: By 2028, operational downtime reduction of 25% and production throughput gain of 18%.

Emerging Technologies: AI-powered image recognition, 3D stereo vision systems, edge computing integration.

Regional Leaders: North America USD 9,500 Million, Europe USD 7,200 Million, Asia-Pacific USD 6,800 Million by 2032, with North America leading in AI deployment.

Consumer/End-User Trends: High adoption in automotive, electronics, and food packaging sectors; increasing use in predictive maintenance.

Pilot or Case Example: 2024 pilot in semiconductor fabrication reduced defect detection time by 40% using 3D vision systems.

Competitive Landscape: Cognex Corp ~24%, Keyence Corp, Basler AG, Omron Corp, Teledyne DALSA.

Regulatory & ESG Impact: Compliance with ISO 9001 and environmental efficiency standards drives adoption.

Investment & Funding Patterns: Over USD 1.2 billion invested in AI-driven vision startups and industrial projects in 2024.

Innovation & Future Outlook: Integration with IoT and AI, adoption of cloud-based inspection systems, future-ready autonomous inspection solutions.

The Machine Vision Market continues to expand across key sectors, including automotive, electronics, food and beverage, and pharmaceuticals, with each sector increasingly adopting AI-enabled and high-speed inspection technologies. Recent innovations in 3D imaging, hyperspectral vision systems, and edge computing have significantly enhanced defect detection and process monitoring. Regulatory incentives for automation, environmental sustainability, and increasing efficiency requirements are further shaping adoption patterns. Emerging trends point to AI-integrated smart factories, regional specialization in advanced production techniques, and cross-industry collaboration for future-ready inspection solutions.

The Machine Vision Market is strategically positioned as a critical enabler of industrial automation, quality control, and predictive maintenance across manufacturing sectors. Implementation of AI-powered 3D vision systems delivers up to 40% improvement in defect detection accuracy compared to traditional 2D imaging methods. North America dominates in volume, while Europe leads in adoption with 72% of enterprises integrating advanced vision solutions into production lines. By 2027, edge AI integration is expected to improve inspection throughput by 25%, reducing downtime and boosting operational efficiency. Firms are committing to ESG improvements such as a 30% reduction in energy consumption by 2028 through optimized vision-assisted processes. In 2024, Cognex implemented a machine vision initiative in semiconductor fabrication, achieving a 38% reduction in defective output using AI-driven anomaly detection. Forward-looking strategies in the Machine Vision Market emphasize sustainable growth through AI and automation integration, positioning it as a pillar of operational resilience, compliance, and long-term technological advancement.

The increasing integration of AI and automation is driving substantial growth in the Machine Vision Market. AI-powered visual inspection systems improve defect detection accuracy by up to 40% and reduce inspection time by 30% compared to manual or legacy systems. Sectors such as automotive assembly, semiconductor fabrication, and food packaging rely on machine vision to maintain stringent quality standards. In 2024, over 68% of automotive manufacturers globally adopted AI-enhanced vision systems to optimize assembly line efficiency, leading to measurable reductions in production errors and material waste. The scalability of AI-based vision solutions allows enterprises to meet rising production demands while maintaining consistent product quality.

High initial investment costs and technical complexity are key restraints in the Machine Vision Market. Advanced systems such as 3D imaging and AI-driven inspection require substantial capital outlay, with installation costs for large-scale manufacturing lines exceeding USD 500,000. Complex integration with existing manufacturing processes, need for skilled operators, and ongoing maintenance also limit adoption, particularly among SMEs. In 2024, a survey indicated that 42% of mid-sized manufacturers cited integration challenges as a primary barrier, slowing the deployment of advanced machine vision technologies despite clear operational benefits.

The growth of smart factories and IoT integration presents significant opportunities in the Machine Vision Market. Connected vision systems can provide real-time monitoring, predictive maintenance, and data analytics, enhancing operational efficiency. By 2025, IoT-enabled machine vision solutions are projected to reduce unplanned downtime by 20% and increase throughput by 15% in pilot implementations across electronics and automotive plants. Emerging applications in pharmaceuticals, logistics, and food processing, coupled with AI and edge computing integration, allow manufacturers to optimize quality control and supply chain management. The convergence of IoT and machine vision opens avenues for scalable, data-driven decision-making.

The Machine Vision Market faces challenges from high system costs, regulatory compliance, and limited technical expertise. Advanced machine vision systems demand specialized knowledge for programming, calibration, and maintenance. Compliance with ISO 9001, environmental efficiency, and safety regulations adds further operational complexity. In 2024, approximately 35% of medium and large manufacturers reported delays in machine vision deployment due to skill shortages and compliance requirements. Additionally, the cost of upgrading legacy systems to AI-enhanced platforms remains a barrier, particularly in emerging markets. These factors collectively slow widespread adoption despite the clear operational and quality benefits offered by modern machine vision technologies.

• Rise of Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Machine Vision market. Studies indicate that 55% of new projects using modular and prefabricated approaches achieved measurable cost benefits. Prefabricated elements are manufactured off-site using automated machine vision systems, reducing labor requirements and accelerating project timelines. In North America and Europe, adoption of high-precision machine vision for pre-bent and cut components has increased by 48% in the past two years, reflecting a strong efficiency-driven trend.

• AI-Powered Quality Inspection: AI-enabled machine vision solutions are increasingly deployed for real-time quality control. By 2024, over 62% of automotive and electronics manufacturers utilized AI inspection systems to reduce production defects, achieving up to 38% improvement in error detection. This trend is expanding into pharmaceuticals and food processing, with real-time visual analytics allowing faster corrective measures and higher throughput.

• Edge Computing and Smart Factory Integration: Edge AI integration into machine vision systems has enabled faster data processing, reducing latency by 30% compared to cloud-only setups. Approximately 58% of industrial plants in Europe have adopted edge-based vision systems to monitor assembly lines, optimizing operational efficiency while reducing energy consumption and minimizing downtime.

• Expansion in Emerging Sectors: The adoption of machine vision in logistics, warehousing, and agricultural automation is accelerating. In 2024, 41% of large-scale warehouses implemented automated inspection and sorting systems, improving operational accuracy by 25%. Agriculture has seen 35% adoption of vision-guided robotic harvesting, highlighting diversification of use cases beyond traditional manufacturing.

The Machine Vision market is segmented by type, application, and end-user, with each segment presenting unique opportunities and adoption patterns. In terms of product types, 3D imaging systems lead adoption, while emerging AI-driven vision solutions are rapidly gaining traction. Applications are dominated by quality inspection, automotive assembly, and electronics testing, whereas logistics, pharmaceuticals, and food processing are emerging areas of growth. End-users are primarily industrial manufacturers, but the market is increasingly penetrating SMEs and specialized service providers. Regional adoption varies, with North America and Europe leading in implementation rates, while Asia-Pacific demonstrates fast-growing integration due to expanding production capacities and industrial automation investments.

3D imaging systems currently account for 44% of adoption in the Machine Vision market, primarily due to their precision in defect detection and dimensional measurement in automotive and electronics manufacturing. AI-powered vision systems represent the fastest-growing type, with deployment increasing by over 22% in the last two years, driven by enhanced real-time analytics and predictive maintenance capabilities. Other types such as line scan cameras, area scan cameras, and multispectral imaging solutions collectively contribute 34% of adoption, often serving niche applications in pharmaceuticals and food quality monitoring.

Quality inspection remains the leading application in machine vision, accounting for 46% of adoption, due to the necessity for precise defect detection in automotive and semiconductor production. The fastest-growing application is predictive maintenance, with usage increasing by 20% over the last two years, supported by AI integration and IoT connectivity that reduce unplanned downtime by up to 25%. Other applications include assembly verification, robotic guidance, and sorting systems, contributing a combined 29% share.

Industrial manufacturing is the leading end-user segment, representing 48% of adoption, with automotive and electronics sectors leading deployment. The fastest-growing end-user segment is SMEs in logistics and warehousing, whose adoption increased by 22% in 2025 due to automation needs and efficiency gains. Other end-users, including food processing and pharmaceuticals, account for a combined 30% of adoption, reflecting growing diversification in machine vision applications.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

In 2024, North America deployed over 430,000 machine vision units across automotive, electronics, and healthcare industries. Europe followed with 28% share, representing nearly 350,000 units, while Asia-Pacific consumed approximately 290,000 units, reflecting rapid industrial automation. Investment levels exceeded USD 1.5 billion in R&D in North America alone. Adoption rates in SMEs reached 42% in logistics and warehousing, while large enterprises reported over 65% integration in production lines. Across all regions, utilization of AI-enhanced inspection systems rose by 38% in 2024, and implementation of 3D imaging systems reached 44% globally. Infrastructure modernization, regulatory compliance, and technology-driven operational efficiency remain key adoption drivers across these geographies.

How are advanced automation and AI transforming operational efficiency in this region?

North America accounts for 34% of the global machine vision market, driven primarily by automotive, electronics, and healthcare sectors. Government incentives for Industry 4.0 adoption and regulatory support for workplace safety have accelerated deployment. AI-powered inspection systems and digital twin integration are prominent, with over 62% of automotive manufacturers using machine vision for assembly line quality control. Local players like Cognex Corp are deploying AI-enhanced vision solutions to optimize throughput and reduce defects. Consumer behavior reflects higher enterprise adoption in healthcare, finance, and high-tech manufacturing, with predictive maintenance systems implemented by 58% of large-scale facilities. Investments in edge computing have also improved real-time analytics and reduced latency in production monitoring.

What role do regulatory pressures and sustainability initiatives play in shaping the market?

Europe holds 28% of the machine vision market, with Germany, the UK, and France leading adoption. Regulatory bodies emphasize safety, ESG compliance, and energy-efficient production, driving demand for explainable and sustainable machine vision systems. Advanced imaging and AI integration are adopted widely, particularly in automotive and electronics manufacturing hubs. Companies such as Basler AG have introduced AI-driven inspection systems to enhance precision in semiconductor and automotive production. Regional consumer behavior emphasizes compliance with environmental standards, resulting in higher adoption of energy-efficient inspection solutions. Approximately 60% of European manufacturers have upgraded to AI-assisted vision systems to meet both regulatory and operational requirements.

How is rapid industrialization influencing technology adoption in manufacturing hubs?

Asia-Pacific represents 26% of the market volume, with China, Japan, and India leading adoption. Industrial modernization and large-scale electronics and automotive manufacturing projects are driving demand. Regional innovation hubs focus on AI, robotics, and 3D imaging technologies, with adoption rates in smart factories exceeding 50% in 2024. Local players such as Keyence Corp have expanded AI-assisted inspection solutions in semiconductor and automotive lines. Consumer behavior trends indicate rapid integration in e-commerce logistics and mobile AI applications, reflecting technology-driven operational efficiency. Investment in infrastructure modernization, including automated warehouses and smart assembly lines, supports continued expansion across the region.

What opportunities are emerging in industrial and energy sectors in this region?

South America holds 7% of the global machine vision market, with Brazil and Argentina leading adoption. Growing manufacturing and energy sectors, combined with government incentives for industrial automation, are fueling demand. Companies like Omron Corp have introduced vision-guided automation solutions for assembly and packaging lines, enhancing operational efficiency. Regional consumer behavior trends indicate strong adoption in media localization, food processing, and industrial quality monitoring, with over 28% of mid-sized enterprises deploying advanced vision systems. Infrastructure expansion and modernization in logistics hubs further support the growth of machine vision solutions.

How are technological modernization and industry diversification shaping demand?

The Middle East & Africa account for 5% of the machine vision market, with the UAE and South Africa driving adoption. The oil & gas, construction, and manufacturing industries are investing in AI-driven inspection systems to improve operational safety and efficiency. Local players are deploying automated vision solutions for pipeline monitoring and construction material inspection. Consumer behavior reflects growing adoption in industrial safety and smart infrastructure projects, with over 32% of large-scale operations implementing AI-enhanced machine vision. Technological modernization, regional trade partnerships, and regulatory incentives contribute to rising deployment rates across this region.

United States – 34% market share; strong demand driven by high production capacity and advanced industrial automation.

Germany – 18% market share; robust end-user demand in automotive and electronics sectors, coupled with stringent regulatory compliance initiatives.

The Machine Vision market exhibits a moderately consolidated structure, with the top five companies—Cognex Corp, Keyence Corp, Basler AG, Omron Corp, and Teledyne DALSA—collectively holding approximately 62% of the global market share in 2024. Over 250 active competitors operate worldwide, ranging from multinational corporations to specialized regional players, reflecting both intense competition and niche innovation opportunities. Strategic initiatives such as AI-driven product launches, cross-industry partnerships, and targeted acquisitions are shaping the competitive landscape. In 2024, Cognex launched a high-speed 3D inspection system, while Keyence expanded its AI-based visual inspection platform into smart factory applications, demonstrating a clear focus on technological differentiation. Innovation trends include multi-sensor 3D imaging, edge AI integration, hyperspectral vision, and real-time analytics, enabling faster defect detection and operational optimization. Regional variations show higher penetration in North America and Europe, while Asia-Pacific is rapidly expanding due to industrial automation investments. The competitive environment is also influenced by increasing government support for Industry 4.0, ESG compliance requirements, and digital transformation across manufacturing sectors.

Omron Corp

Teledyne DALSA

National Instruments

Sony Corporation

Panasonic Corporation

Datalogic S.p.A

LMI Technologies

The Machine Vision market is experiencing a rapid technological transformation driven by AI, robotics, and advanced imaging systems. AI-powered inspection platforms now enable automated defect detection with up to 95% accuracy, replacing traditional human-led quality control in automotive, electronics, and pharmaceutical manufacturing. Multi-sensor 3D imaging has become critical for high-precision applications, with over 44% of industrial production lines incorporating such systems in 2024. Edge computing integration allows for real-time data processing, reducing latency by 30% compared to cloud-only solutions, which enhances operational efficiency and responsiveness. Hyperspectral imaging technology is gaining traction in food processing and pharmaceuticals, enabling detection of contaminants invisible to standard RGB cameras. Additionally, vision-guided robotics is increasingly deployed for automated material handling, assembly, and packaging, with adoption in over 40% of large-scale manufacturing plants in North America and Europe. Other emerging technologies include infrared thermal imaging for predictive maintenance, AI-driven anomaly detection, and cloud-based analytics platforms for cross-site monitoring. The combination of these technologies is not only improving operational efficiency but also supporting ESG initiatives by reducing material waste, energy consumption, and production errors. Decision-makers are increasingly focusing on integrating modular and scalable machine vision solutions to meet dynamic production requirements and regulatory compliance.

In 2023, Cognex launched its new In-Sight 7000 series vision systems, incorporating AI-powered 3D inspection for automotive assembly, achieving 38% faster defect detection and reducing downtime in pilot implementations.

Keyence Corp expanded its AI-driven visual inspection platform across semiconductor and electronics manufacturing in 2024, improving defect recognition accuracy by 42% in operational trials.

Basler AG introduced the ace 3D stereo vision cameras in 2023, enhancing precision in pharmaceutical packaging lines, with deployment in over 120 production facilities across Europe.

Teledyne DALSA implemented a hyperspectral imaging solution in food processing plants in 2024, enabling real-time contamination detection, increasing throughput accuracy by 35%, and reducing waste significantly.

The Machine Vision Market Report provides a comprehensive analysis of global trends, technologies, applications, and regional dynamics. The report covers major product types including 3D imaging systems, AI-based inspection platforms, line and area scan cameras, and multispectral imaging solutions, highlighting adoption across key sectors such as automotive, electronics, pharmaceuticals, food processing, logistics, and smart factories. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into market penetration, technology adoption rates, consumer behavior patterns, and infrastructure trends. The report also explores emerging and niche segments, such as hyperspectral imaging, vision-guided robotics, predictive maintenance solutions, and edge-computing-enabled inspection platforms. Operational applications including quality inspection, assembly verification, defect detection, and automated material handling are examined in detail. Additionally, the report evaluates regulatory compliance trends, ESG-driven adoption, and innovation initiatives by leading players. The scope encompasses detailed market insights for decision-makers seeking technology deployment strategies, investment opportunities, and strategic planning for competitive advantage across manufacturing and industrial sectors. The analysis is structured to support both global enterprises and regional manufacturers in identifying growth pathways, optimizing technology integration, and enhancing operational efficiency.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14734.29 Million |

|

Market Revenue in 2032 |

USD 26870.72 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cognex Corp, Keyence Corp, Basler AG, Omron Corp, Teledyne DALSA, National Instruments, Sony Corporation, Panasonic Corporation, Datalogic S.p.A, LMI Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |