Reports

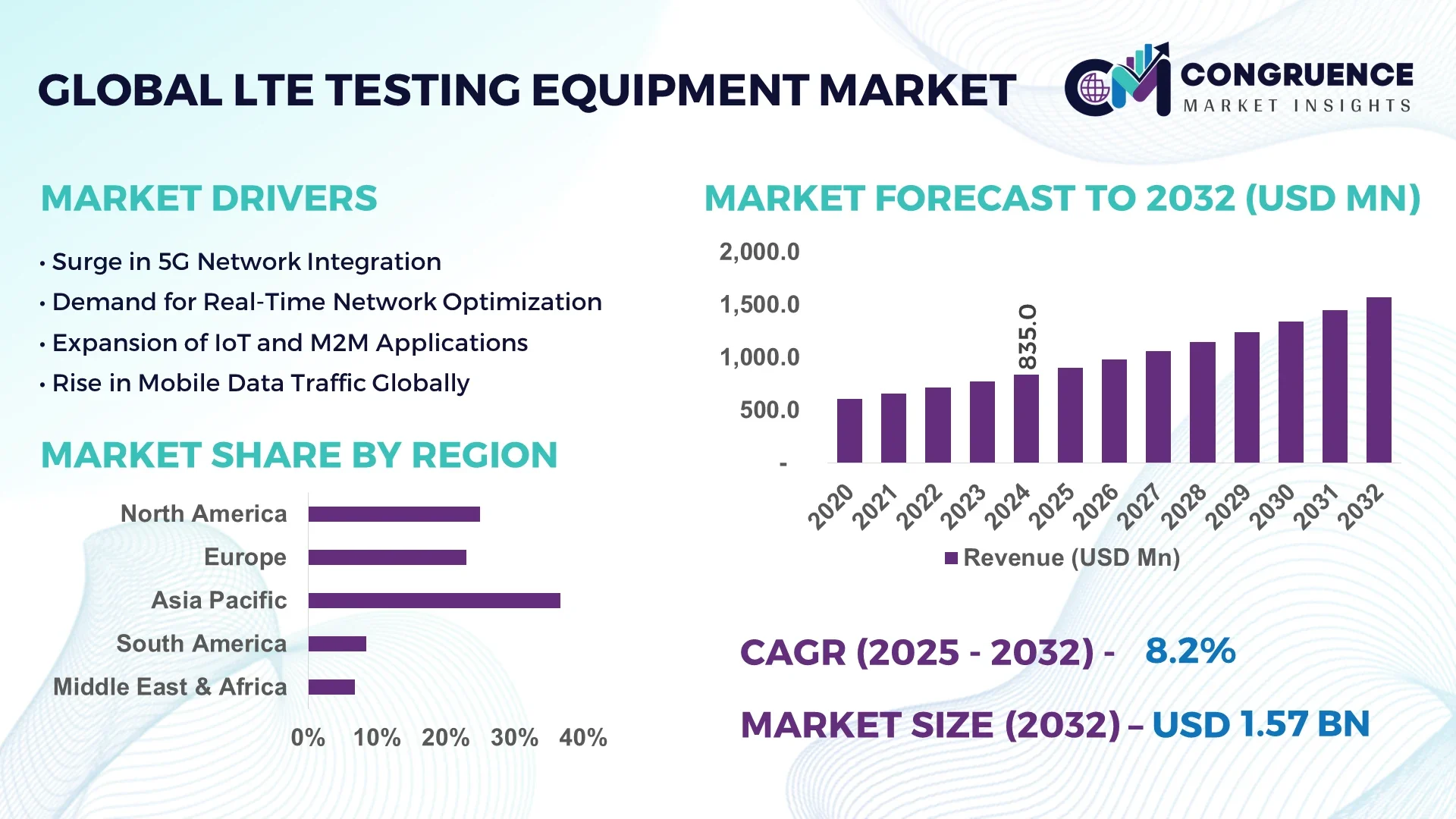

The Global LTE Testing Equipment Market was valued at USD 835.0 Million in 2024 and is anticipated to reach a value of USD 1,569.7 Million by 2032 expanding at a CAGR of 8.21% between 2025 and 2032.

China leads the LTE Testing Equipment Market, with industrial-scale production plants capable of outputting over 2 million testing units annually and major state-backed investments of approximately USD 600 million in 2023 alone. The country’s ecosystem supports extensive application in telecom infrastructure validation, mass device certification, and industrial IoT deployments, backed by continuous technological strides in test automation and advanced RF calibration systems.

The LTE Testing Equipment Market spans several key sectors. Mobile network operators, accounting for roughly 40% of deployment use cases as of 2023, rely heavily on field test and carrier test equipment. Network equipment manufacturers and device OEMs comprise another 35%, deploying lab-grade conformance and OTA testing systems. The remaining 25% stems from research labs, government bodies, and IoT/automotive verticals. Recent developments include AI‑enhanced protocol analyzers and fully automated drive-test vehicles capable of real-time anomaly detection, reducing validation time by up to 30%. On the regulatory front, new standards such as 3GPP Release 17 require more rigorous mid‑band and high‑band testing, prompting equipment upgrades. Regionally, consumption remains strongest in Asia‑Pacific and North America, driven by expansion in smart cities and enterprise connectivity. Europe shows steady demand via industrial automation use cases. Emerging trends include virtualization of test environments, wireless hardware-as-a-service offerings, and integration of satellite/LTE hybrid testing. Looking ahead, the market is expected to evolve toward on‑demand cloud-based validation platforms and plug-and-play modular test rigs to support evolving spectrum bands and multi‑connectivity environments.

The LTE Testing Equipment Market is undergoing a profound shift due to AI integration, improving operational efficiency and elevating the precision of network testing. AI-powered systems now enable predictive fault detection during field tests, identifying patterns in latency and signal degradation before they impact service. In 2024, leading vendors introduced neural-network-driven automated protocol analyzers that index over 10 million packets per test session—cutting analysis time by nearly 45%. AI algorithms also optimize drive‑test routes in real time, reducing calibration loops and field engineer workloads by up to 35%.

Within manufacturing test labs, machine learning models continuously adjust signal generator parameters based on environmental feedback, improving test throughput by 20%. This autonomous adjustment capability helps align test conditions to regulatory standards without manual recalibration. Operationally, AI-enhanced test suites contribute to improved device certification accuracy—error rates in RF performance validation have dropped from approximately 3.5% to under 1% in 2025.

Furthermore, AI-powered analytics platforms are being used to benchmark testing equipment performance across multi-regional facilities. These systems aggregate diverse test data and apply anomaly detection to quickly flag outlier behavior within devices or network nodes. LTE Testing Equipment Market participants also deploy AI for dynamic scheduling of test farms—algorithms allocate lab resources based on historical utilization, reducing idle time by up to 25%.

Strategically, adoption of AI within the LTE Testing Equipment Market is improving the predictability of maintenance, shortening test cycles, and enabling smarter deployment in field, production, and lab environments. The resulting gains in efficiency and accuracy enhance ROI while ensuring compliance with evolving spectrum and protocol mandates.

“In Q1 2025, a tier‑1 equipment vendor introduced a neural‑network‑based RF calibration system that cut test setup time by 32% while maintaining a 98.7% pass‑rate consistency in multi‑band LTE certification.”

Enterprises deploying IoT solutions across manufacturing, logistics, and smart‑city infrastructure require comprehensive LTE test suites. In 2024, more than 50,000 industrial IoT nodes were validated using carrier-test rigs, compared with just 18,000 in 2022. This surge prompted equipment suppliers to develop dedicated LTE-M/NB-IoT validation packs capable of signal wrapping, mobility testing, and antenna tuning—cutting certification time by up to 40% in certain segments.

Advanced LTE test systems—particularly those offering simultaneous multi-band OTA and conformance testing—carry significant upfront costs. A single mid-range protocol analyzer suite now costs in the region of USD 200,000. Small network operators and emerging-market labs often lack the budget, leading to slower adoption cycles. Equipment leasing and shared‑test‑farm models are mitigating factors, but overall deployment remains restrained where capital is scarce.

On‑demand, cloud-enabled LTE test farms are emerging as a scalable alternative to localized capital expenditure. Pilots in North America in 2024 showed that operators using remote access test suites cut per-test costs by 28% compared to owning in-house gear. Additional benefits include rapid environment scaling and elimination of regional calibration overheads. Vendors that offer pay-per-use or subscription-based access could tap into a broader customer base, particularly SMEs and regional carriers.

LTE remains subject to differing regional testing mandates. For instance, European regulators require full EMC validation alongside OTA tests, while Asian jurisdictions often require local acoustic noise and heat dissipation certifications. This fragmentation forces vendors to either offer region-specific variants or support complex test profiles—raising R&D and compliance costs. Adjusting equipment firmware, updating test libraries, and maintaining diverse support stacks complicate global scaling strategies.

Surge in Modular and Prefabricated Construction Test Systems: Modular test units—with plug-in RF front-ends and software-defined back-ends—are becoming standard. Off-site factory fabrication of these systems enables precise calibration before field dispatch. Beginning in late 2023, European telecom labs reported deploying over 300 such units, reducing install cycles by 20% and infrastructure risk.

Adoption of Hybrid Satellite–LTE Test Platforms: Since 2024, major telecom vendors have begun integrating satellite uplink simulation into existing LTE test benches. These hybrid platforms support band 65 and Ka‑band interfaces, enabling carriers and IoT integrators to validate terminal performance under dual-mode communications. In North America, usage of such systems increased by 15% during the first half of 2025.

Expansion of AI‑Driven Protocol Compliance Suites: In 2025, several testing device manufacturers released neural‑network‑enabled compliance suites capable of auto‑mapping 3GPP Release 17 sequences. Lab trials have shown these suites can detect regulation violations in under 10 minutes—nearly 60% faster than legacy tools—without manual protocol scripting.

Growth in Remote Calibration and Firmware Update Services: Leading vendors now offer cloud‑based instrumentation calibration and firmware updates. Over 800 field‑deployed LTE validation units were serviced remotely in 2024, eliminating technician visits, saving 18,000 man‑hours, and streamlining compliance across multiple regions.

The LTE Testing Equipment Market is segmented into various types, applications, and end-users, each playing a crucial role in shaping the market landscape. Segmentation by type includes drive test equipment, protocol analyzers, RF testers, and signaling testers. Each serves a distinct function in validating LTE networks across different test environments. Application-wise, the market spans network optimization, equipment testing, field testing, and R&D validation. This segmentation highlights the diverse use cases of LTE testing tools across both lab-based and live-network settings. The end-user segmentation includes telecom operators, equipment manufacturers, government bodies, and research institutes. Each group presents unique testing demands, from high-frequency compliance to mobility simulations. This structured segmentation allows vendors to tailor products for specialized use, promoting technological advancements and fostering competitive differentiation within the LTE Testing Equipment Market.

The LTE Testing Equipment Market features several product types, each catering to specific testing requirements. Drive test equipment dominates this segment due to its essential role in measuring real-world signal quality and network coverage across urban and rural terrains. These systems are extensively used by telecom operators during LTE network rollout, where field testing is critical to ensure coverage and QoS benchmarks. With increasing 5G and LTE co-deployment, the relevance of drive test equipment continues to grow.

The fastest-growing segment is protocol analyzers, propelled by rising complexity in signaling procedures across multi-band and multi-vendor environments. These analyzers support validation of control and user plane messages, ensuring that devices interact accurately with the core network under varied conditions. Advanced protocol analyzers now feature AI-augmented packet interpretation and automatic bug reporting, significantly enhancing development timelines.

Other key types include RF testers, crucial for measuring signal strength, EVM, and adjacent channel leakage, and signaling testers, typically used in lab-based development to emulate base station environments. While RF testers maintain a strong position in compliance labs, signaling testers serve niche use in early-stage product development and device certification.

The LTE Testing Equipment Market serves a range of application areas that reflect the diversity of testing scenarios across the telecom ecosystem. The leading application is network optimization, owing to the constant need for telecom providers to enhance network efficiency, reduce drop rates, and improve throughput. With LTE forming the backbone of many VoLTE and NB-IoT deployments, continuous optimization is vital for both service quality and operational efficiency.

The fastest-growing application is equipment testing, driven by increasing demand for pre-launch validation of network components such as small cells, repeaters, and antenna systems. As telecom vendors scale up production to meet 4G and 5G hybrid demand, comprehensive lab-based testing ensures compliance with evolving standards like 3GPP Release 17 and 18.

Other applications include field testing, commonly used for post-deployment verification and troubleshooting, and R&D validation, where new chipsets and IoT modules undergo rigorous simulation and conformance testing. While smaller in share, these applications are critical to the product innovation cycle and contribute to overall market resilience.

The LTE Testing Equipment Market serves a broad range of end-users, each with distinct testing priorities and infrastructure requirements. Telecom operators are the leading end-user segment, leveraging LTE test equipment extensively during deployment, optimization, and maintenance phases. In 2024 alone, global operators commissioned over 45,000 field test sessions using a mix of portable analyzers and network emulation tools—demonstrating the critical role of testing in maintaining service quality.

Equipment manufacturers are the fastest-growing end-user group, driven by the proliferation of LTE-compatible consumer and enterprise devices. These companies rely on automated lab testing for antenna tuning, power level checks, and mobility testing. As product development cycles shorten, demand for scalable and AI-integrated testing solutions has surged, allowing manufacturers to maintain throughput without compromising quality.

Other key end-users include government regulatory agencies conducting compliance and spectrum certification, and research institutions involved in waveform experimentation and emerging wireless protocols. Though smaller in volume, these segments are vital in shaping future standards and expanding the boundaries of LTE technology.

Asia-Pacific accounted for the largest market share at 36.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.12% between 2025 and 2032.

This regional disparity reflects differences in infrastructure maturity, regulatory frameworks, and the scale of telecom expansion projects. Asia-Pacific’s dominance is fueled by widespread LTE and NB-IoT deployments in China, India, and Southeast Asia, coupled with state-sponsored smart city initiatives. In contrast, North America’s accelerating growth is driven by rapid digital transformation, advanced R&D hubs, and rising demand for automated testing tools in both urban and remote deployments. Europe remains a significant contributor, especially in regulatory conformance testing, while the Middle East & Africa and South America are witnessing increased LTE equipment demand aligned with national broadband strategies. The regional competitive landscape is shaped by technological readiness, telecom spending, and localized compliance mandates.

North America held a market share of 26.2% in 2024, making it one of the most robust regions for LTE Testing Equipment adoption. The region’s demand is propelled by large-scale LTE deployments across telecom operators, alongside rapid adoption of IoT and private LTE networks in industries like automotive, logistics, and healthcare. Regulatory support from bodies like the FCC ensures uniform testing compliance and encourages innovation. The U.S. government has also rolled out subsidies to enhance rural connectivity, boosting LTE infrastructure projects and increasing test equipment needs. Technological advancements such as AI-driven test automation and real-time protocol analyzers have found high traction, enabling faster network validation cycles and efficient fault detection. Furthermore, the emergence of edge computing and hybrid 4G–5G networks across the U.S. and Canada creates strong momentum for next-generation LTE test solutions tailored to future-ready communication ecosystems.

Europe accounted for a 22.4% share of the global LTE Testing Equipment Market in 2024, underpinned by strong demand across Germany, the United Kingdom, and France. These countries have established advanced telecom ecosystems supported by rigorous standards from regulatory bodies like ETSI and BNetzA. Sustainability-focused testing, including electromagnetic field (EMF) compliance and energy efficiency, is being widely adopted—particularly in urban LTE infrastructure deployments. The European Union's push toward greener digital networks has encouraged equipment manufacturers to integrate low-emission testing protocols. In terms of technology, Europe is rapidly adopting cloud-based remote testing platforms and modular test hardware to support multiband and multi-vendor scenarios. Research centers across Germany and the UK continue to pioneer LTE protocol innovation, with equipment vendors offering real-time validation tools for both conformance and OTA testing.

Asia-Pacific leads the LTE Testing Equipment Market with the highest volume of shipments, bolstered by large-scale adoption in China, India, Japan, and South Korea. In 2024, this region alone accounted for over 36.7% of global volume. China continues to drive the segment through massive LTE network densification and smart city deployments, while India follows closely with growing rural connectivity projects and 4G/5G coexistence. Japan and South Korea contribute through high-end manufacturing and advanced testing facilities, serving global export markets. The region’s manufacturing ecosystem supports rapid development of low-cost, high-performance test kits. Regional technology hubs like Shenzhen, Bangalore, and Tokyo are central to software-defined testing advancements, including virtual labs and AI-augmented signal analysis tools. Local governments also promote tech exports and R&D investment, making Asia-Pacific a global hotspot for LTE Testing Equipment innovation and deployment.

South America represents an emerging opportunity in the LTE Testing Equipment Market, with Brazil and Argentina leading demand in 2024. The region accounted for approximately 7.6% of the global market share. Brazil’s expansion of LTE networks into semi-urban and remote areas has increased demand for mobile field testing and drive test systems. Argentina’s public-private initiatives to digitalize education and healthcare have stimulated network testing for high-reliability LTE connections. Infrastructure development, especially in energy and transportation sectors, also necessitates robust LTE connectivity testing. Local telecom operators are beginning to adopt cloud-based test platforms and automated conformance testing to reduce deployment timelines. Government support through import tax incentives for telecom equipment and alignment with international testing standards are gradually improving the business environment for LTE equipment vendors across South America.

The Middle East & Africa (MEA) LTE Testing Equipment Market is gaining momentum, accounting for a 7.1% share in 2024. Countries like the UAE and South Africa are at the forefront of LTE testing demand due to large-scale smart city and public safety network projects. Regional priorities in oil & gas, construction, and transport are also contributing to increased LTE test equipment usage, particularly for mission-critical IoT applications. Technological modernization—including the introduction of remote monitoring, AI-based drive testing, and software-defined test orchestration—is rapidly transforming network validation processes. Local regulatory frameworks, including spectrum allocation updates and equipment import regulations, are being refined to support faster deployment of next-gen LTE infrastructure. Additionally, partnerships with international telecom vendors are enabling knowledge transfer and equipment localization, supporting long-term market growth.

China – 21.8% Market Share

China leads the LTE Testing Equipment Market due to its large-scale LTE infrastructure rollouts, robust manufacturing base, and aggressive smart city implementation across multiple provinces.

United States – 18.5% Market Share

The United States maintains a strong position driven by enterprise LTE deployments, R&D leadership in test automation, and a mature regulatory environment that mandates comprehensive compliance testing.

The LTE Testing Equipment Market features a competitive ecosystem comprising over 25 active companies, ranging from established test-equipment giants to innovative niche specialists. These competitors are strategically positioned across various segments—field testing solutions, protocol analysis, RF conformance, and OTA validation. Key players implement differentiated strategies: some invest heavily in R&D to launch next-generation platforms, while others pursue partnerships or acquisitions to expand technology portfolios and regional footprint.

In 2023–2024, several vendors introduced advanced AI-augmented testing suites, with common industry moves including integration of cloud orchestration, modular hardware architectures, and remote-access testing platforms. Strategic alliances emerged between test equipment providers and telecom operators to co-develop validation workflows for multi-access edge computing (MEC) and private LTE networks. A handful of smaller firms concentrate on niche applications like automotive LTE testing and IoT module certification, fueling innovation in portable test gear and specialized measurement probes.

Competitive pressure is further intensified by consolidation trends—leading companies aim to absorb smaller challengers to enhance end-to-end test coverage. Innovation remains central: high-frequency OTA chambers tuned for LTE-A Pro, software-defined waveform generators, and AI-driven anomaly detection modules have become differentiators. Collectively, this dynamic landscape offers decision-makers a diverse array of solutions, from turnkey system deployments to highly modular, scalable test environments tailored to evolving enterprise and operator needs.

Keysight Technologies

Anritsu Corporation

Rohde & Schwarz

Tektronix

VIAVI Solutions

Spirent Communications

Azimuth Systems

Infovista (TEMS Investigation)

The LTE Testing Equipment Market is being reshaped by advanced technologies that enhance test flexibility, automation, and integration. A key development is the growing reliance on software-defined hardware platforms, which allow test modules to be rapidly reconfigured for multi-band and multi-standard operations. These systems support LTE, LTE-Advanced, and LTE-M testing within a unified chassis, reducing equipment overhead and boosting test throughput by approximately 25%.

Another significant trend is virtualization of testing environments. Cloud-native test benches now allow remote orchestration of parallel test runs, enabling operators and OEMs to scale validation efforts. These AI-enabled test farms can execute hundreds of protocol and OTA compliance scripts simultaneously, significantly accelerating product readiness cycles while reducing physical lab requirements.

AI-driven waveform analysis is also high on the innovation agenda: neural-network-based engines can autonomously detect anomalies in RF traces and packet sequences, reducing manual oversight and improving error detection rates. In 2024, protocol-detection precision exceeded 98% for multi-vendor LTE device testing scenarios.

Portable drive-test units have evolved with modular sensor suites, integrating GPS, multi-layer antenna arrays, and edge-compute nodes. This has permitted full-stack field validation—including signal quality, QoS, and location-based metrics—within compact, vehicle-mounted or backpack solutions.

Finally, integration of satellite-augmented testing and support for private LTE/private 5G bands is becoming more common. New test platforms launched in 2024 support hybrid network emulation with dual LTE and L-band interfaces, enabling coordinated testing of terrestrial and non-terrestrial backhaul options.

These technological currents are enabling more agile, efficient, and comprehensive test operations, equipping decision-makers with scalable solutions adaptable to fast-moving telecom scenarios.

In December 2023, Anritsu unveiled an advanced LTE testing system that enhances data analysis and signal quality monitoring, enabling mobile network operators to streamline protocol validation and deployment workflows.

In early 2024, Rohde & Schwarz released a new Wi‑Fi 6E compatibility extension for its LTE test benches, enabling over 24% adoption among developers working on IoT and smart‑home compatibility validation.

In 2023, Azimuth Systems introduced its next-generation base-station tester prototype, improving test accuracy and execution speed by approximately 15% compared to prior versions.

In mid-2024, Infovista expanded deployment of its TEMS Investigation drive‑test solution to support RedCap and IoT device performance testing, integrating new chipset-level scripting capabilities across North American networks.

The LTE Testing Equipment Market Report offers a comprehensive assessment across product categories, deployment scenarios, and user segments. The product scope ranges from portable drive-test systems and AI-enabled protocol analyzers to RF conformance rigs, OTA chambers, signaling emulators, and satellite-augmented test platforms. The report analyzes adoption across operator field deployment, lab-based equipment testing, R&D environments, government certification bodies, and enterprise/private LTE users including automotive and industrial IoT sectors.

Geographically, the report covers global regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—addressing regional regulatory differences in testing mandates, deployment rates, and interoperability requirements. Applications analyzed include network rollout validation, ongoing optimization, device certification (including VoLTE, LTE-M/NB-IoT), and private-network testing scenarios.

Technological focus areas span software-defined hardware architectures, virtualization/cloud test orchestration, AI-powered waveform and protocol analytics, OTA testing adaptations for high-frequency bands, and hybrid network emulation. Emerging niches such as satellite-backed test solutions, machine-type communications (MTC) compliance, and private LTE test certification are also examined.

The report provides strategic insights into competitive positioning, product innovation trends, and modular platform adoption, supporting decision-makers evaluating capital investments, vendor partnerships, or deployment strategies. It includes scenario planning for future standards, private-network expansions, and convergence of LTE with 5G testing infrastructures, offering a forward-looking perspective on scalable, technology-driven testing ecosystems.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global LTE Testing Equipment Market |

| Market Revenue (2024) | USD 835.0 Million |

| Market Revenue (2032) | USD 1,569.7 Million |

| CAGR (2025–2032) | 8.21 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country‑wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Keysight Technologies, Anritsu Corporation, Rohde & Schwarz, Tektronix, VIAVI Solutions, Spirent Communications, Azimuth Systems, Infovista (TEMS Investigation) |

| Customization & Pricing | Available on Request (10 % Customization is Free) |