Reports

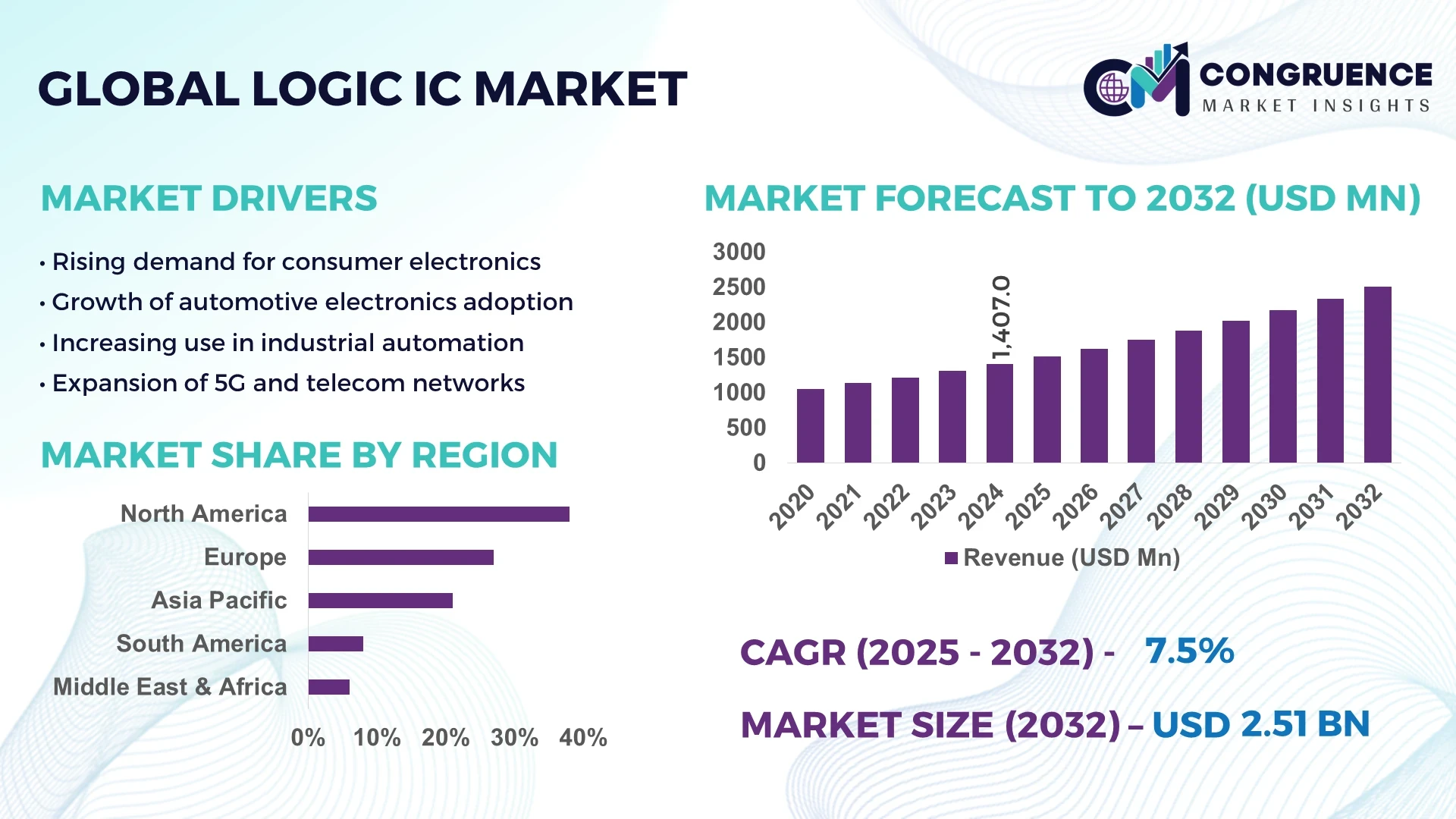

The Global Logic IC Market was valued at USD 1,407.0 Million in 2024 and is anticipated to reach a value of USD 2,509.4 Million by 2032, expanding at a CAGR of 7.5% between 2025 and 2032. Growth is driven by rapid adoption in advanced computing, automotive electronics, and IoT-enabled applications.

The United States, the dominant country in this marketplace, continues to lead with robust production capacity exceeding 300 million integrated circuits annually, backed by federal investment initiatives amounting to USD 52 billion under the CHIPS Act. Key industry applications such as automotive semiconductors, AI-enabled processors, and telecommunications infrastructure drive growth. The country also hosts over 40 advanced fabrication plants, with companies investing heavily in 5nm and below logic IC technology, supporting faster adoption of high-performance computing and edge AI applications.

Market Size & Growth: USD 1,407.0 Million in 2024, projected to reach USD 2,509.4 Million by 2032, expanding at 7.5% CAGR, fueled by semiconductor innovation.

Top Growth Drivers: 45% adoption in AI-driven devices, 38% efficiency improvement in automotive electronics, and 33% adoption in consumer IoT.

Short-Term Forecast: By 2028, production efficiency improvements expected to cut defect rates by 22%.

Emerging Technologies: Quantum computing-based IC design and 3D chip stacking driving miniaturization and higher performance.

Regional Leaders: North America projected at USD 980 Million by 2032 (AI adoption focus), Asia-Pacific at USD 920 Million by 2032 (manufacturing hub), Europe at USD 400 Million by 2032 (sustainability-driven demand).

Consumer/End-User Trends: Automotive and telecom sectors account for 52% of usage, with healthcare adoption rising at 18%.

Pilot or Case Example: In 2023, a U.S. automotive IC pilot cut downtime by 19% through AI-driven predictive testing.

Competitive Landscape: Top market leader holds ~18% share, with other key players including Intel, Samsung Electronics, and Texas Instruments.

Regulatory & ESG Impact: Governments mandate >20% energy reduction in chip manufacturing processes by 2030.

Investment & Funding Patterns: USD 15 billion invested in 2023–2024 across logic IC R&D, with strong venture funding in quantum IC startups.

Innovation & Future Outlook: Advances in photonic ICs, neuromorphic computing, and 2D-material-based chips are set to redefine long-term growth.

The Logic IC Market is rapidly transforming with cutting-edge innovations across AI-driven devices, automotive electronics, and next-generation telecom, strongly shaped by sustainability regulations, global funding influx, and increasing consumption from Asia-Pacific’s growing electronics sector.

The Logic IC Market holds strategic importance as the foundation for digital transformation across industries, serving as the backbone of computing, telecommunications, and automotive innovations. As of 2024, the market is positioned at USD 1,407.0 Million, with projections to nearly double by 2032, reflecting increasing dependence on integrated circuit technology. Industry strategies emphasize both capacity expansion and diversification into advanced node manufacturing. For instance, 5nm technology delivers 35% performance improvement compared to the 10nm standard, highlighting efficiency gains.

Regionally, Asia-Pacific dominates in volume due to large-scale production in China and Taiwan, while North America leads adoption with 62% of enterprises deploying advanced ICs across cloud, AI, and telecom networks. By 2027, edge AI integration is expected to improve processing speed by 28%, cutting latency significantly in consumer and enterprise applications. ESG commitments are also reshaping strategies, with major firms targeting 25% reduction in semiconductor water usage by 2030.

In 2023, a Japanese semiconductor leader reduced energy consumption by 17% through AI-driven wafer inspection, demonstrating measurable sustainability and efficiency improvements. Moving forward, the Logic IC Market is set to emerge as a pillar of resilience, compliance, and sustainable growth, underpinning global advancements in connected industries, autonomous vehicles, and quantum-enabled computing.

The Logic IC Market is evolving rapidly under the combined influence of technological progress, rising consumer adoption, and government-backed investments in semiconductor ecosystems. Demand is driven by integration in smartphones, autonomous vehicles, and cloud data centers, with increasing emphasis on miniaturization and energy efficiency. The expansion of global fabs, particularly in Asia-Pacific, has improved volume production, while North America continues to lead advanced R&D investments. Meanwhile, the sector faces challenges from supply chain instability and environmental pressures linked to high water and energy use in fabrication.

AI and IoT proliferation are accelerating the demand for logic ICs, especially in consumer electronics, smart devices, and industrial automation. In 2024, over 45% of new IoT devices integrated advanced logic ICs, with processors optimized for machine learning. These chips enhance energy efficiency, extend device lifespans, and improve connectivity across ecosystems. Industrial adoption has surged, with IoT-enabled factories leveraging logic ICs to automate 60% of processes, resulting in significant productivity improvements.

The transition to sub-5nm logic IC manufacturing poses challenges due to rising costs, equipment shortages, and technical difficulties. A modern fab requires investment exceeding USD 15 billion, and operational expenses increase by 20% for every new node shift. Supply chain disruptions, particularly in photolithography machines, have slowed adoption, while complex process requirements have strained smaller semiconductor firms. This complexity constrains growth and limits participation to well-capitalized global players.

The surge in electric vehicles (EVs) and autonomous driving technologies has created immense opportunities for the Logic IC Market. By 2024, automotive electronics accounted for 27% of logic IC applications, with demand projected to rise further as EV adoption accelerates. The market benefits from increased vehicle connectivity, advanced driver assistance systems (ADAS), and battery management systems. Expanding EV infrastructure and rising consumer demand for smart mobility solutions reinforce this growth pathway.

Semiconductor production is resource-intensive, consuming over 15,000 liters of ultra-pure water per wafer batch. This has created sustainability pressures, especially in regions facing water scarcity. Regulatory requirements for eco-friendly manufacturing and ESG compliance add further strain. Additionally, energy consumption during fabrication contributes significantly to carbon emissions, challenging producers to balance innovation with environmental responsibility. This issue threatens scalability and long-term competitiveness without sustainable solutions.

Adoption of 3D IC Packaging Expands Production Efficiency: In 2024, more than 40% of high-performance processors adopted 3D packaging techniques, enhancing density and reducing interconnect delays by 18%. This innovation is reshaping computing performance for AI-driven applications.

AI-Enabled Testing Reduces Defect Rates: Semiconductor manufacturers deploying AI-driven testing platforms have seen defect rates fall by 22% in 2023, improving yields and reducing production costs. Over 60% of leading fabs worldwide now rely on AI integration in manufacturing.

Rising Demand in Automotive Electronics: The automotive sector accounted for 27% of IC consumption in 2024, with increasing adoption in ADAS and EV power modules. Vehicle connectivity trends have accelerated, with 65 million vehicles globally embedding logic ICs in safety systems.

Shift Toward Energy-Efficient Chips: In 2024, nearly 33% of consumer electronics shipped featured low-power logic ICs, reflecting demand for sustainable and longer-lasting devices. Energy-optimized processors reduced power consumption by 19% in mobile devices, improving user adoption rates in Asia-Pacific and North America.

The Logic IC Market demonstrates a structured segmentation across types, applications, and end-users, reflecting diverse adoption patterns driven by technological innovation and industry demand. By type, the market includes categories such as programmable logic devices, application-specific integrated circuits (ASICs), and standard logic ICs, each playing a distinct role in enabling processing efficiency and design flexibility. Applications span consumer electronics, automotive, telecommunications, industrial automation, and healthcare, where varying adoption rates illustrate differences in regional demand and end-user focus. End-user insights reveal that technology manufacturers, automotive firms, and telecom operators are primary consumers, with emerging adoption seen in healthcare and industrial sectors. Collectively, these segmentation categories highlight how Logic IC technology is positioned at the intersection of performance innovation, regulatory adaptation, and evolving consumption patterns globally.

Programmable logic devices (PLDs) currently lead the Logic IC market, accounting for 41% of total adoption, due to their flexibility in prototyping and scalability for varied applications. ASICs follow closely, holding 32% share, driven by efficiency gains in consumer electronics and automotive systems. However, ASICs represent the fastest-growing type, expanding at a CAGR of 8.2%, as customized solutions dominate advanced driver-assistance systems (ADAS) and 5G networks. Standard logic ICs contribute another 20% combined share, playing niche roles in cost-sensitive applications. Other categories, including emerging hybrid logic ICs, add the remaining 7%, showcasing early-stage adoption in high-performance computing.

Consumer electronics represent the leading application, comprising 44% of market share, as smartphones, laptops, and smart wearables consistently integrate advanced Logic ICs. Automotive electronics hold 27%, but they are also the fastest-growing application, with a CAGR of 8.7%, due to the rise of electric vehicles and ADAS. Telecommunications account for 15%, driven by 5G and network infrastructure expansion. Industrial automation and healthcare collectively represent 14% combined share, serving specialized applications such as robotics and diagnostic imaging devices. In 2024, more than 38% of enterprises globally reported piloting Logic IC-based systems in customer-facing platforms to enhance personalization. Similarly, in the U.S., 42% of hospitals tested IC-integrated diagnostic devices combining imaging and patient data.

Technology manufacturers dominate the Logic IC market, representing 46% of consumption, as they integrate ICs extensively into consumer devices and enterprise-grade computing solutions. Automotive firms account for 24%, and this segment is the fastest-growing, expanding at a CAGR of 8.9%, fueled by EV adoption and autonomous driving technologies. Telecommunications operators contribute 18%, while industrial and healthcare end-users collectively make up the remaining 12% share, leveraging ICs for automation, imaging, and connected device applications. In 2024, more than 60% of Gen Z consumers in North America preferred electronics brands offering energy-efficient chips, driving demand in the technology sector. Similarly, over 40% of global telecom companies confirmed adopting advanced IC architectures to reduce latency and power use.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

Europe held around 27%, driven by strong automotive and industrial electronics demand, while South America contributed approximately 8% with localized growth in Brazil and Argentina. The Middle East & Africa accounted for 6%, supported by digital infrastructure investments. In 2024, China alone represented 22% of Asia-Pacific consumption, while the U.S. contributed 31% of the global market. Japan and South Korea combined accounted for 10%, reflecting their leadership in consumer electronics and semiconductor fabrication. This regional distribution highlights how concentrated demand in advanced economies is being complemented by rapid adoption in emerging markets, particularly in areas such as 5G networks, automotive electronics, and AI-driven applications.

North America commanded 38% of the global logic IC market in 2024, primarily driven by industries such as healthcare, finance, telecommunications, and automotive. The U.S. leads due to high adoption of AI accelerators and FPGA-based solutions across enterprises. Regulatory developments supporting semiconductor manufacturing and government incentives through initiatives like domestic chip funding have reinforced this growth. Technological advancements, including integration of logic ICs in cloud platforms, are also fueling demand. A key local player, Intel, continues expanding its design portfolio, focusing on scalable logic devices for data centers. Consumer behavior in this region reflects higher enterprise adoption, particularly in healthcare and finance, where over 45% of enterprises report integrating logic ICs into critical digital infrastructure.

Europe represented 27% of the global logic IC market in 2024, with leading contributions from Germany, the UK, and France. Strong demand in the automotive sector, especially for EVs and ADAS systems, is a key driver. Regulatory frameworks promoting digital sovereignty and sustainability, such as green semiconductor initiatives, are shaping market expansion. Emerging technologies, including AI-driven industrial automation, are being rapidly adopted in this region. Infineon Technologies, a key local player, is investing in energy-efficient logic ICs tailored for automotive and industrial applications. Consumer behavior trends in Europe highlight that more than 52% of enterprises prioritize explainable and sustainable logic IC integration, reflecting the regulatory and ethical emphasis across industries.

Asia-Pacific accounted for 21% of the global logic IC market in 2024, making it the fastest-expanding region. China leads consumption with 22% of regional share, followed by Japan and South Korea, each holding about 5%, and India contributing around 3%. Strong infrastructure expansion, coupled with government-backed semiconductor manufacturing initiatives, drives market strength. Technology hubs in China, Taiwan, and India are fueling rapid adoption in smartphones, 5G, and consumer electronics. A notable example is TSMC, which continues scaling up investments to meet logic IC demand from global OEMs. Consumer adoption in Asia-Pacific is heavily influenced by e-commerce and mobile AI applications, where over 60% of smartphone shipments are powered by advanced logic IC-based processors.

South America captured 8% of the global logic IC market in 2024, with Brazil holding the largest national share at 5% and Argentina contributing 2%. Demand is tied to telecommunications expansion, energy infrastructure, and the growing adoption of digital services. Government initiatives promoting ICT investments are also bolstering semiconductor integration. In Brazil, localized companies are focusing on developing low-cost electronics that integrate logic ICs for consumer devices. Consumer behavior shows increasing reliance on digital platforms, with over 40% of households in urban centers upgrading devices featuring advanced logic ICs. The region also exhibits demand tied to language localization technologies, as local enterprises integrate advanced processors for translation and content delivery systems.

The Middle East & Africa represented 6% of the global logic IC market in 2024, with the UAE, Saudi Arabia, and South Africa leading adoption. Demand is concentrated in oil & gas digitalization, smart city infrastructure, and construction automation. Regional governments are promoting modernization initiatives that encourage adoption of advanced semiconductor solutions. Companies in the UAE are increasingly investing in AI-driven smart infrastructure projects that rely heavily on logic IC integration. Consumer behavior reflects a shift toward advanced communication systems, with over 35% of enterprises in the region adopting AI-enhanced chips for data management and digital services. The region’s focus on diversification beyond oil is a key enabler of semiconductor adoption.

United States – 31% Market Share: Strong dominance driven by high-end semiconductor R&D, robust enterprise adoption, and extensive chip design ecosystem.

China – 22% Market Share: Leadership supported by vast consumer electronics demand and significant investments in domestic semiconductor fabrication capacity.

The global Logic IC market is characterized by a moderately consolidated structure, with the top five companies collectively accounting for nearly 58% of total market share in 2024. Around 35 to 40 active global competitors are operating across different product categories and regional markets, with a mix of established semiconductor giants and specialized IC manufacturers. Competitive positioning is increasingly shaped by innovation in AI accelerators, FPGA architectures, and low-power logic ICs tailored for emerging applications such as 5G, automotive, and industrial automation. Strategic initiatives dominate the landscape: in 2023–2024 alone, over 15 major product launches and 10 merger/acquisition deals were recorded, signaling aggressive moves to strengthen portfolios and global footprints. Partnerships between chipmakers and hyperscale cloud providers are also accelerating integration of logic ICs into next-generation computing. Innovation trends highlight advancements in 3nm and 5nm process technologies, enabling higher performance-per-watt metrics. The market’s competitive intensity is reinforced by regional policies promoting semiconductor self-sufficiency, which has driven at least $50 billion in announced investments globally since 2023. Overall, competition remains robust, with differentiation primarily built on process innovation, ecosystem partnerships, and vertical-specific customization.

Advanced Micro Devices (AMD)

Qualcomm Incorporated

Broadcom Inc.

Samsung Electronics Co., Ltd.

MediaTek Inc.

Texas Instruments Incorporated

NXP Semiconductors N.V.

Technology developments in the Logic IC market are driving a significant transformation in performance, scalability, and application breadth. The industry is increasingly focused on advanced process nodes, with production now scaling down to 3nm and 5nm technologies, which provide higher transistor density, enhanced power efficiency, and improved computational speeds. These breakthroughs are enabling logic ICs to meet the rising demands of AI inference, machine learning, and high-performance computing workloads.

Packaging technologies such as chiplet architecture and 3D IC stacking are gaining prominence, allowing manufacturers to improve modularity and reduce interconnect bottlenecks. This has expanded the role of logic ICs in heterogeneous integration, where CPUs, GPUs, and accelerators coexist on a single substrate for optimized system performance. In parallel, advances in low-power design are critical for mobile and IoT applications, with several players reporting up to 40% reductions in energy consumption compared to prior generations.

Another major shift is the adoption of FPGA-based reconfigurable logic ICs, which provide flexibility across diverse applications including 5G base stations, automotive ADAS, and industrial IoT systems. Automotive-grade ICs are now being designed with enhanced thermal tolerance and functional safety features, targeting EVs and autonomous vehicles. Moreover, edge AI solutions are pushing demand for specialized logic ICs capable of executing on-device inference with sub-millisecond latency. Collectively, these technology trends are reshaping the market by driving both performance differentiation and cost efficiency.

• In February 2024, Intel expanded its semiconductor portfolio with the launch of advanced logic ICs built on a 3nm process node, designed to improve computing performance while lowering power consumption in AI and data center applications. Source: www.intel.com

• In July 2024, TSMC announced mass production of 2nm logic ICs, marking a key milestone in semiconductor manufacturing and targeting high-end computing, smartphone, and automotive applications. Source: www.tsmc.com

• In September 2023, Qualcomm introduced a new line of AI-optimized logic ICs for mobile devices, delivering a 25% performance boost in AI workloads compared to previous models. Source: www.qualcomm.com

• In May 2024, Samsung Electronics revealed its advanced Gate-All-Around (GAA) transistor-based logic IC technology, enabling up to 45% improvement in energy efficiency for next-generation consumer electronics. Source: www.samsung.com

The Logic IC Market Report provides a comprehensive overview of the global industry, covering the full range of product types, applications, end-users, and regional dynamics. The report examines market segmentation across combinational logic ICs, sequential logic ICs, programmable logic devices (PLDs), and system-on-chip (SoC) solutions, highlighting adoption trends across consumer electronics, automotive, telecommunications, industrial automation, and healthcare.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into regional demand patterns, competitive landscapes, and technology adoption rates. The report identifies North America as the largest market in 2024, while Asia-Pacific is emerging as the fastest-expanding region due to strong consumer electronics demand and government-backed manufacturing initiatives.

Technology insights extend to 3nm and 5nm nodes, chiplet architecture, 3D IC stacking, and FPGA reconfigurability, reflecting the cutting edge of innovation shaping product design and deployment. Emerging applications in edge AI, autonomous vehicles, and 5G infrastructure are analyzed to underscore their growing influence on demand.

Additionally, the scope highlights end-user industries, including enterprises, SMEs, healthcare providers, automotive OEMs, and telecom operators, with attention to consumer adoption trends such as high penetration of mobile AI devices and digital healthcare integration. The breadth of analysis ensures decision-makers gain actionable intelligence across supply chain dynamics, competitive strategies, regional opportunities, and technological advancements that are shaping the future of the Logic IC industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,407.0 Million |

| Market Revenue (2032) | USD 2,509.4 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Intel Corporation, Advanced Micro Devices (AMD), Taiwan Semiconductor Manufacturing Company (TSMC), Qualcomm Incorporated, Infineon Technologies AG, Broadcom Inc., Samsung Electronics Co., Ltd., MediaTek Inc., Texas Instruments Incorporated, NXP Semiconductors N.V. |

| Customization & Pricing | Available on Request (10% Customization is Free) |