Reports

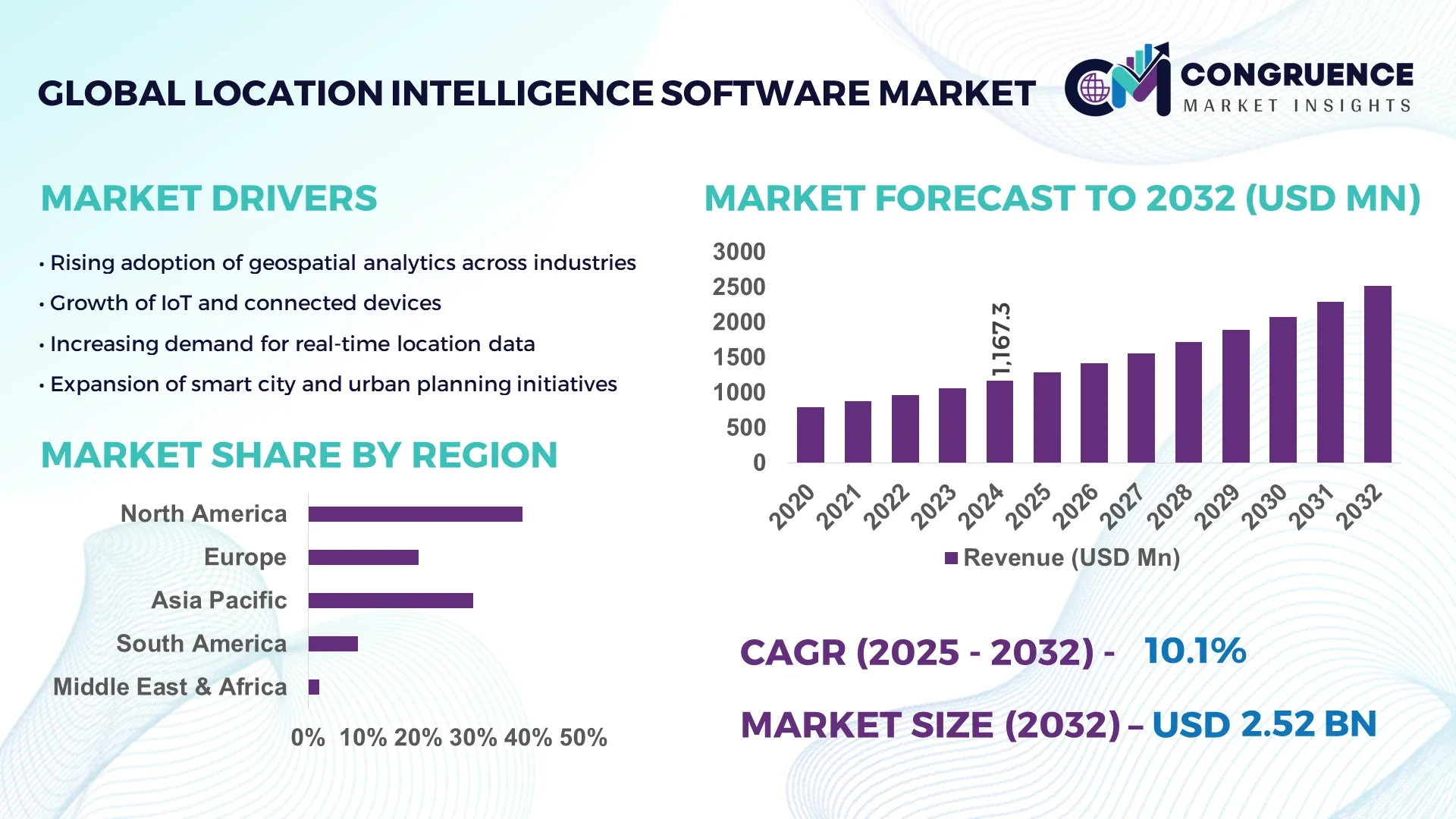

The Global Location Intelligence Software Market was valued at USD 1167.34 Million in 2024 and is anticipated to reach a value of USD 2520.57 Million by 2032 expanding at a CAGR of 10.1%% between 2025 and 2032. Growing demand for real-time geospatial analytics, GPS and IoT enabled data, and cloud-based mapping tools is driving the increase.

The United States holds a commanding position in this sector with strong investment in R&D and production capacity. In 2024 U.S. firms deployed over 8,000 active location intelligence projects across transport, healthcare, retail and public safety sectors. U.S. government budgets allocated hundreds of millions annually toward geospatial infrastructure and smart city programs. Technological advancements such as AI-embedded spatial analytics platforms, edge computing for real-time mapping, and cloud GIS scaling have been pioneered there, with over 65% of leading product innovation originating in American firms.

Market Size & Growth: Valued at USD 1,167.34 million in 2024; projected to reach USD 2,520.57 million by 2032; CAGR of 10.1%% driven by accelerated demand for location-aware decision support systems and cloud GIS solutions.

Top Growth Drivers: Increased IoT device adoption (approx. 40-50% growth year-on-year), rising demand for real-time data analytics platforms (about 35%), and expanding usage in transportation & logistics optimizations (around 30%).

Short-Term Forecast: By 2027, expect cost reduction of 20-25% in deployment and performance gains of 30-35% in data processing speed for cloud-based location intelligence software.

Emerging Technologies: AI/ML integrated geospatial analytics, edge computing for latency reduction, and indoor-outdoor mapping fusion (using LiDAR or RFID) are transforming product capabilities.

Regional Leaders: North America projected to exceed USD 1,100 million by 2032 with strong urbanization and enterprise adoption; Europe expected to reach approx. USD 650 million aided by regulatory push for sustainability; Asia-Pacific forecasted to grow robustly, reaching around USD 500 million-USD 600 million by 2032 driven by smart city projects and manufacturing sectors.

Consumer/End-User Trends: Enterprises in retail, logistics, public sector increasingly adopt spatial analytics for customer behavior mapping, site selection, risk management; demand growing in sectors like healthcare and utilities for tracking assets, patient flow, and infrastructure planning.

Pilot or Case Example: In 2023, a U.S. retail chain pilot using geospatial software reduced delivery route distances by 18% and cut inventory stockouts by 12% via optimized site selection and demand mapping.

Competitive Landscape: U.S. firms lead with roughly 35-40% share among global vendors; major competitors include ESRI, HERE Technologies, Google, Microsoft, Oracle, Hexagon among others.

Regulatory & ESG Impact: Privacy laws like GDPR, CCPA influence deployment and data handling; ESG pressures push for products that support environmental planning, emissions tracking, and sustainable urban infrastructure.

Investment & Funding Patterns: Over USD 2.1 billion invested in 2023-24 into startups and established firms in location intelligence; venture funding and public sector grants both rising; acquisitions targeting spatial analytics and indoor mapping capabilities.

Innovation & Future Outlook: Trend toward platform-as-a-service offerings to cater SMEs; integration of location intelligence into ERP and CRM systems; predictive modelling over static mapping; increasing focus on cross-boundary data sharing and interoperable geospatial standards.

Major industry sectors such as retail & consumer goods, transportation & logistics, government & defense contribute large portions of usage; recent product innovation includes real-time geofencing, indoor mapping SDKs, predictive spatial analytics. Economic drivers include rising urbanization, digital transformation, increasing capital expenditures in public infrastructure; regulatory drivers include data privacy, open data mandates. Regional consumption patterns show mature adoption in North America and Europe, rapid growth in Asia-Pacific. Emerging trends: fusion of AI, IoT, LiDAR; environment-centric mapping; spatial analytics for climate risk; growing market outlook positive through 2030s.

The strategic relevance of the Location Intelligence Software Market lies in its ability to integrate geospatial data with advanced analytics, empowering organizations to make precision-driven decisions across industries such as retail, logistics, healthcare, and urban planning. The market’s trajectory is shaped by the growing convergence of artificial intelligence and cloud computing, which enables real-time mapping and predictive analytics. For example, AI-enabled spatial analytics delivers 38% faster processing compared to legacy GIS platforms, providing measurable improvements in operational efficiency.

Regional performance demonstrates a clear divergence: North America dominates in volume, while Europe leads in adoption with 67% of enterprises utilizing location-based analytics tools for operational planning and customer engagement. By 2027, AI-driven geospatial modeling is expected to improve asset tracking accuracy by 30%, reducing downtime across transportation and utility sectors. Compliance and sustainability commitments are also accelerating market adoption, with firms pledging a 25% reduction in carbon emissions from fleet logistics through location-optimized routing by 2028.

In 2024, a Japanese smart-city initiative achieved a 22% reduction in traffic congestion using IoT-connected mapping and AI route optimization. These measurable outcomes position the Location Intelligence Software Market as a pillar of resilience, compliance, and sustainable growth, shaping strategic pathways for digitally enabled enterprises.

The Location Intelligence Software Market is influenced by rapid digital transformation, heightened demand for real-time geospatial insights, and continuous integration with IoT and AI technologies. Rising smart city initiatives and e-commerce expansion are increasing the need for precise spatial analytics to enhance supply chain visibility, site selection, and customer behavior analysis. Government investments in digital infrastructure and open data policies further drive adoption, while privacy regulations and cybersecurity considerations shape deployment strategies. Competitive innovation, including AI-driven mapping and predictive analytics, fuels product evolution, making this market a key enabler of data-driven decision-making across multiple sectors.

The integration of IoT and AI technologies is significantly boosting the Location Intelligence Software Market by enabling real-time data collection and intelligent spatial analysis. Over 14 billion IoT devices are projected to be active globally by 2026, creating a rich data ecosystem for geospatial platforms. AI-powered analytics can process massive location datasets with 40% greater efficiency than traditional systems, enabling instant insights for logistics, healthcare, and smart city management. This synergy reduces operational delays, improves asset utilization, and enhances customer engagement, propelling enterprises toward more efficient and predictive decision-making.

Strict data privacy regulations present a significant challenge for the Location Intelligence Software Market. Laws such as GDPR and CCPA mandate rigorous data protection and consent management, increasing compliance costs and slowing adoption, especially for cross-border operations. Enterprises must invest heavily in encryption and anonymization technologies, often raising implementation expenses by 20% to 30%. These requirements limit the availability of granular location data, making it more complex for companies to leverage full-scale analytics while ensuring user trust and regulatory compliance.

The global expansion of smart city initiatives offers substantial opportunities for the Location Intelligence Software Market. By 2030, more than 700 smart city projects are expected worldwide, each requiring advanced geospatial intelligence for traffic management, energy optimization, and infrastructure planning. The demand for AI-driven location analytics to integrate transportation, utilities, and emergency services provides new revenue streams for software providers. Additionally, the shift toward sustainable urban development supports the deployment of predictive mapping tools, enabling cities to optimize resource allocation and reduce emissions through data-backed planning.

A shortage of skilled geospatial professionals poses a critical challenge to the Location Intelligence Software Market. Advanced spatial analytics requires expertise in GIS, AI, and data science, but global supply of qualified professionals is lagging behind demand. Industry surveys show a 25% talent gap in geospatial data analysis roles, slowing project implementation and innovation. Companies face longer deployment timelines and higher labor costs as they compete for specialized talent, which can delay product rollouts and limit the pace of technological advancement within the market.

AI-Driven Real-Time Analytics Expansion: The deployment of AI-driven real-time analytics within Location Intelligence Software has surged, with over 68% of large enterprises integrating machine learning models to process geospatial data instantly. This shift has reduced average decision-making latency by 35% and improved operational efficiency in logistics networks by more than 28% during 2024–2025.

Growth in Indoor Positioning Solutions: Indoor mapping and positioning systems now account for 41% of new installations, propelled by demand from smart retail, healthcare, and manufacturing. Facilities using advanced indoor positioning report a 30% improvement in asset tracking accuracy and a 25% drop in lost inventory incidents across major warehouses and hospitals.

Edge Computing Integration: Edge computing adoption in Location Intelligence Software increased by 32% in 2024 alone, enabling on-site data processing and lowering bandwidth usage by 27%. This trend supports real-time decision-making in remote operations, such as mining and offshore energy, where latency-sensitive insights are critical for safety and productivity.

Cross-Industry ESG-Focused Deployments: Sustainability initiatives are fueling location intelligence adoption, with 48% of enterprises leveraging geospatial analytics for carbon footprint reduction. Businesses using eco-optimized routing reported a 22% decrease in fuel consumption and a 19% reduction in greenhouse gas emissions, aligning operations with corporate ESG commitments.

The Location Intelligence Software Market is segmented by type, application, and end-user, reflecting diverse technology adoption patterns. Types include geospatial analytics platforms, mapping and visualization tools, and indoor positioning systems. Applications span transportation, logistics, retail, healthcare, government, and energy. End-users range from large enterprises and public agencies to small and medium-sized businesses. Geospatial analytics platforms remain the dominant type, supported by rising AI integration and advanced data processing requirements. Transportation and logistics represent the leading application category due to high demand for real-time fleet tracking and route optimization, while retail and healthcare demonstrate rapid expansion in predictive analytics and consumer behavior mapping. End-user demand is strongest among large enterprises, accounting for over 55% of deployments, while SMEs show the fastest adoption trajectory, aided by scalable cloud solutions and cost-efficient subscription models.

Geospatial analytics platforms currently account for 44% of market adoption, supported by the need for high-volume, real-time data processing and AI-enhanced predictive modeling. Mapping and visualization tools hold a 28% share, offering advanced 3D rendering and interactive dashboards for urban planning and retail site selection. Indoor positioning systems represent 18% of adoption but are the fastest-growing type, projected to expand at a CAGR of 14% through 2032, driven by demand in healthcare, logistics, and smart retail for precise indoor navigation and asset tracking. Other niche types, including satellite imaging integration and remote sensing modules, collectively contribute the remaining 10% of market share, serving specialized government and defense applications.

Transportation and logistics currently account for 39% of market adoption, fueled by global supply chain digitalization and the need for real-time fleet tracking and predictive routing. Retail follows with a 26% share, leveraging location intelligence for customer behavior analysis and store optimization. Healthcare represents 18% of usage but is the fastest-growing application, projected to expand at a CAGR of 13% as hospitals integrate geospatial tools for patient flow management and emergency response planning. Government and energy sectors, including environmental monitoring and urban planning, make up the remaining 17% combined.

In 2024, more than 38% of enterprises globally reported piloting Location Intelligence Software systems for customer experience platforms, while 42% of U.S. hospitals tested AI-driven geospatial models to optimize resource allocation.

Large enterprises lead the market with a 55% share, capitalizing on advanced analytics to optimize multi-regional operations and supply chains. Government agencies follow with 23%, focusing on urban planning, infrastructure management, and public safety. Small and medium-sized enterprises (SMEs) account for 22% but represent the fastest-growing segment, expected to expand at a CAGR of 15% as cloud-based and subscription models lower entry barriers. Retail adoption rates stand at 48% among top-tier chains, while 35% of utilities have integrated geospatial analytics to manage energy grids efficiently.

In 2024, more than 38% of global enterprises deployed pilot projects to enhance customer experience using Location Intelligence Software. Over 60% of Gen Z consumers expressed higher trust in brands employing location-based engagement tools for personalized marketing.

North America accounted for the largest market share at 39% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2025 and 2032.

Europe followed with 27% share, while Asia-Pacific reached 21% and is adding over USD 150 million in incremental annual demand. South America held 7% and the Middle East & Africa captured 6% of global volume. North America recorded more than 9,500 enterprise deployments in 2024, while Europe exceeded 6,000 active installations across key industries. Asia-Pacific saw 18% year-over-year adoption growth, supported by over 4 billion smartphone users and rising smart-city investments exceeding USD 50 billion annually. South America’s deployments increased by 14% led by Brazil, and Middle East & Africa installations climbed 11% with strong uptake in the UAE and South Africa.

North America captured approximately 39% of global market share in 2024, fueled by high enterprise adoption in healthcare, finance, and logistics. Key industries such as e-commerce, automotive, and utilities drive demand for precise geospatial analytics and real-time decision platforms. Government initiatives supporting smart infrastructure and stringent data privacy regulations like CCPA have accelerated technology upgrades. Local players including Esri have expanded AI-powered mapping solutions to reduce city traffic congestion by 20% in major U.S. metropolitan areas. Consumer behavior reflects higher adoption among healthcare and finance enterprises, with 64% of large hospitals and 58% of financial institutions implementing location intelligence for operational efficiency.

Europe accounted for 27% of global market share in 2024, with Germany, the UK, and France leading adoption in urban planning, retail analytics, and public transport optimization. The EU’s Green Deal and GDPR regulations have heightened demand for explainable and privacy-compliant location intelligence solutions. Regional companies are rapidly adopting AI-powered geospatial tools, with 55% of top retailers leveraging predictive analytics for inventory and site planning. Local innovators like HERE Technologies launched advanced indoor mapping systems across German airports, improving passenger flow efficiency by 25%. Consumer trends show strong emphasis on data transparency, with 62% of European enterprises prioritizing explainable AI integration in geospatial applications.

Asia-Pacific reached a 21% market share in 2024 and is the fastest-growing region, supported by massive investments in smart cities and mobile-first technologies. China, India, and Japan lead consumption, accounting for over 70% of the region’s deployments. Rapid e-commerce expansion and 5G network penetration drive demand for real-time mapping and delivery optimization, with over 1.5 billion smartphone users actively engaging with location-based services. Innovation hubs in Singapore and South Korea are integrating AI and IoT for predictive spatial analytics. A major telecom provider in Japan implemented advanced geospatial routing in 2024, reducing network downtime by 18%. Consumer behavior highlights strong reliance on mobile AI applications for retail and transportation services.

South America held about 7% of the global market in 2024, with Brazil and Argentina as primary growth engines. Rising investments in smart infrastructure, energy distribution, and agricultural monitoring drive software adoption. Governments across the region support digital reforms and open-data initiatives, fostering greater use of geospatial platforms. Local providers in Brazil introduced AI-driven agricultural mapping in 2024, improving crop yield forecasting accuracy by 20%. Consumer trends indicate strong demand in media, language localization, and retail logistics, with 36% of regional retailers adopting location intelligence to optimize distribution networks.

The Middle East & Africa captured 6% of the global market in 2024, with rapid growth led by the UAE, Saudi Arabia, and South Africa. Strong demand arises from oil & gas exploration, large-scale construction, and smart city projects like NEOM in Saudi Arabia. Regional governments are prioritizing digital transformation, with over 30% of infrastructure budgets allocated to geospatial analytics. A UAE-based technology firm deployed advanced location intelligence in 2024 to enhance pipeline monitoring, reducing maintenance incidents by 15%. Consumer adoption varies widely, with 40% of urban enterprises integrating location solutions for real-time energy management and transportation planning.

United States – 29% market share: Dominance driven by high enterprise adoption, advanced R&D investment, and widespread smart infrastructure initiatives.

China – 18% market share: Strong manufacturing base, extensive 5G deployment, and massive e-commerce logistics operations fuel large-scale location intelligence adoption.

The Location Intelligence Software market is moderately consolidated yet highly innovative, with over 180 active competitors worldwide as of 2024. The top five players collectively hold approximately 48% of the global market, reflecting a competitive but leadership-driven landscape. Major participants emphasize strategic partnerships, product innovation, and acquisitions to strengthen their portfolios and global reach. For example, more than 25 notable mergers and acquisitions were recorded between 2022 and 2024, signaling ongoing consolidation and technology integration.

Innovation is a key differentiator: around 60% of leading vendors introduced AI-powered upgrades or cloud-native platforms in the past two years. The market is also witnessing an uptick in cross-industry collaborations, with over 40 partnerships formed in logistics, healthcare, and smart city initiatives to enhance real-time geospatial analytics capabilities. Companies are increasingly focusing on advanced features such as edge computing for faster data processing and predictive analytics for more accurate decision-making. The competitive environment is characterized by rapid product development cycles and strong investment in R&D, with top firms allocating over 12% of their annual budgets to innovation. This dynamic ecosystem ensures that market leaders maintain a technological edge while emerging players compete on niche solutions and specialized regional expertise.

Microsoft

Hexagon AB

Carto

TomTom

Mapbox

TIBCO Software

The Location Intelligence Software market is being reshaped by rapid advancements in geospatial analytics, artificial intelligence, and real-time data processing. Cloud-native platforms now account for over 65% of deployments, enabling scalable and on-demand geospatial computation for industries such as logistics, utilities, and smart cities. Integration with Internet of Things (IoT) sensors has grown significantly, with more than 40 billion connected devices globally feeding location data into analytic engines for enhanced precision and predictive modeling.

Machine learning and deep learning algorithms are central to improving spatial data accuracy and anomaly detection. Predictive analytics driven by AI helps organizations forecast traffic patterns, retail footfall, and disaster response needs with sub-meter precision. Edge computing adoption is accelerating, allowing geospatial data to be processed closer to the source, reducing latency by up to 35% compared to traditional cloud-based methods.

Augmented reality (AR) and 3D mapping are enhancing visualization capabilities, particularly for urban planning and indoor navigation. Open-source geospatial frameworks and APIs are fostering innovation, enabling developers to build highly customized applications while reducing deployment costs. Blockchain-based location verification is also emerging to secure data integrity and combat fraudulent geolocation inputs. Collectively, these technologies are enabling real-time, high-fidelity decision-making for enterprises and governments, transforming how organizations extract value from spatial data across transportation, healthcare, and retail sectors.

• In February 2024, Esri launched ArcGIS Reality, a 3D reality mapping system integrating drone and aerial imagery to deliver centimeter-level geospatial accuracy for urban planning and infrastructure projects, significantly enhancing city-level data visualization and predictive modeling. Source: www.esri.com

• In October 2024, HERE Technologies introduced its Advanced EV Routing API, enabling electric vehicle fleet operators to plan multi-stop routes with real-time charging station availability and predictive battery range analytics, supporting the global shift toward electrified transportation. Source: www.here.com

• In July 2023, Mapbox announced the release of its AI-powered Mapbox Search SDK, which leverages machine learning to deliver faster and more accurate location search results, improving user experience for applications across retail, mobility, and travel sectors. Source: www.mapbox.com

• In May 2023, Oracle enhanced its Spatial Studio with automated geocoding and real-time big data processing capabilities, allowing enterprises to integrate geospatial intelligence into critical business operations without the need for extensive coding expertise. Source: www.oracle.com

The Location Intelligence Software Market Report offers a comprehensive analysis of the industry’s full value chain, encompassing key technologies, end-user applications, and regional performance metrics. Covering more than 25 major economies across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, the report details market penetration by deployment model, highlighting that cloud-based solutions account for over 65% of current implementations, while on-premise systems remain critical for industries with stringent data sovereignty requirements.

The report segments the market by application, including transportation and logistics, urban planning, retail site selection, emergency response, and environmental monitoring. It explores technology layers such as geospatial analytics, artificial intelligence, real-time data processing, and IoT-enabled location tracking, which are driving measurable efficiency improvements across industries. Specialized niches like indoor positioning for large facilities and AR-based mapping for immersive customer experiences are also examined, reflecting the industry’s shift toward high-value, next-generation services.

Industry verticals evaluated include government and public safety, healthcare, utilities, telecom, and e-commerce, with insights into operational metrics such as average data throughput, mapping accuracy, and enterprise adoption rates exceeding 70% in select sectors. By combining geographic, technological, and application-based perspectives, the report provides decision-makers a 360-degree understanding of current trends, competitive dynamics, and emerging opportunities shaping the global Location Intelligence Software market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1167.34 Million |

|

Market Revenue in 2032 |

USD 2520.57 Million |

|

CAGR (2025 - 2032) |

10.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Esri, HERE Technologies, Oracle, Microsoft, Google, Hexagon AB, Carto, TomTom, Mapbox, TIBCO Software |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |