Reports

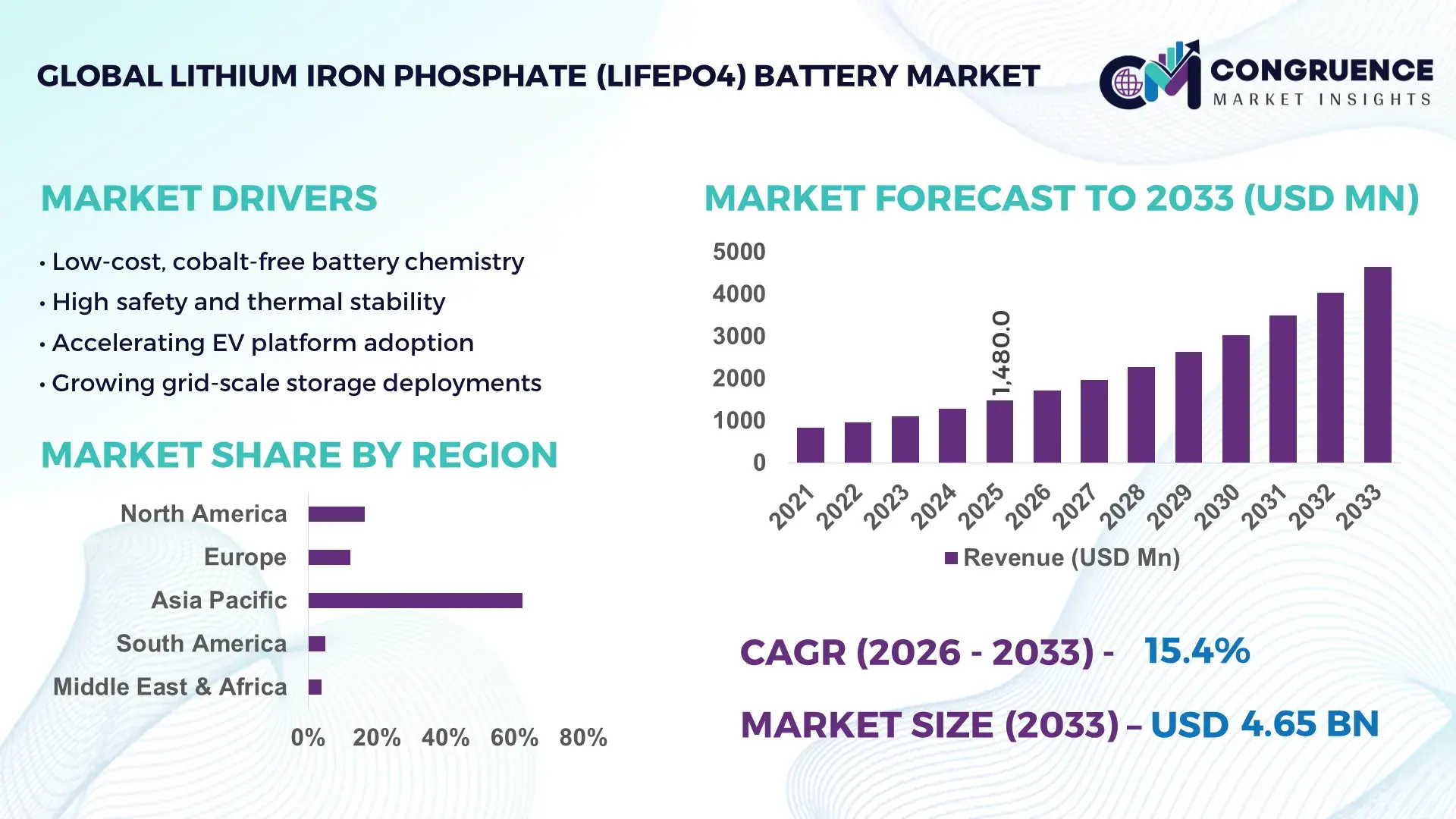

The Global Lithium Iron Phosphate (LiFePO4) Battery Market was valued at USD 1,480.0 Million in 2025 and is anticipated to reach a value of USD 4,654.9 Million by 2033, expanding at a CAGR of 15.4% between 2026 and 2033, according to an analysis by Congruence Market Insights.

This growth is driven by accelerating electric mobility adoption, grid-scale energy storage expansion, and increasing preference for safer, cobalt-free battery chemistries.

China represents the most influential country in the Lithium Iron Phosphate (LiFePO4) Battery Market in terms of industrial scale and deployment depth. The country operates LiFePO4 battery manufacturing capacity exceeding 650 GWh, supported by investments of over USD 45 billion in cathode materials, cell manufacturing, and pack integration since 2020. More than 90% of electric buses and nearly 65% of entry-level electric passenger vehicles in China use LiFePO4 batteries. Technological advancements include blade battery architectures, cell-to-pack integration, and commercial deployment of LiFePO4 cells exceeding 190 Wh/kg, alongside grid-connected storage installations surpassing 50 GWh cumulatively.

Market Size & Growth: USD 1,480.0 Million in 2025, projected to reach USD 4,654.9 Million by 2033, growing at a CAGR of 15.4% due to EV electrification and energy storage demand.

Top Growth Drivers: EV adoption growth 38%, renewable energy storage deployment 42%, battery safety performance improvement 25%.

Short-Term Forecast: By 2028, average LiFePO4 battery pack costs expected to decline by 22%.

Emerging Technologies: Cell-to-pack architecture, blade batteries, AI-enabled battery management systems.

Regional Leaders: Asia-Pacific USD 2,850 Million, North America USD 1,150 Million, Europe USD 655 Million by 2033, each driven by EV fleets, grid storage, and regulatory mandates.

Consumer/End-User Trends: Over 60% of new stationary storage projects now specify LiFePO4 chemistry.

Pilot or Case Example: In 2024, a 1.5 GWh LiFePO4 grid pilot improved peak-load management efficiency by 19%.

Competitive Landscape: Market leader holds ~28% share, followed by BYD, LG Energy Solution, Samsung SDI, and EVE Energy.

Regulatory & ESG Impact: Recycling mandates targeting 70% material recovery accelerating adoption.

Investment & Funding Patterns: Over USD 65 billion invested globally since 2021 in LiFePO4 gigafactories and storage projects.

Innovation & Future Outlook: Integration with smart grids, long-duration storage systems, and AI-driven lifecycle optimization.

LiFePO4 batteries primarily serve electric vehicles (~52%), stationary energy storage (~34%), and industrial mobility (~14%). Blade battery designs, high-cycle cathodes, and enhanced thermal stability continue reshaping product strategies. Regulatory decarbonization policies, strong Asia-Pacific consumption, and rising grid modernization initiatives support sustained long-term adoption.

The Lithium Iron Phosphate (LiFePO4) Battery Market is strategically critical as governments and enterprises prioritize energy security, safety, and sustainable electrification. Compared with conventional nickel-rich lithium-ion chemistries, cell-to-pack LiFePO4 technology delivers up to 15% higher volumetric efficiency compared to module-based lithium-ion designs, while maintaining superior thermal stability. Asia-Pacific dominates in production volume, while North America leads in enterprise adoption, with approximately 48% of large-scale energy storage operators specifying LiFePO4 systems for grid resilience.

By 2027, AI-enabled battery management systems are expected to improve operational efficiency by 30% through predictive maintenance and real-time performance optimization. Firms are committing to ESG improvements, including 80% battery material recyclability by 2030, aligning with circular-economy mandates. In 2024, China achieved a 25% reduction in battery fire incidents in public transportation fleets through large-scale LiFePO4 deployment supported by smart thermal controls. Looking ahead, the Lithium Iron Phosphate (LiFePO4) Battery Market is positioned as a cornerstone of resilient infrastructure, regulatory compliance, and long-term sustainable growth across mobility and energy ecosystems.

The Lithium Iron Phosphate (LiFePO4) Battery Market is shaped by rapid electrification, renewable integration, and heightened safety requirements. Demand is accelerating across electric mobility and stationary storage, supported by cycle life exceeding 4,000–6,000 cycles and reduced thermal runaway risk. Manufacturing automation, localized supply chains, and digital battery monitoring are reshaping procurement and deployment strategies for utilities, OEMs, and industrial operators.

Electric buses, delivery fleets, and entry-level passenger EVs increasingly rely on LiFePO4 batteries due to high safety tolerance and durability. Over 85% of electric buses deployed globally use LiFePO4 chemistry, enabling high-frequency charging and long service life. Fleet operators report 20–25% lower total ownership costs versus nickel-based alternatives, accelerating adoption across public and logistics transportation.

LiFePO4 batteries exhibit 15–20% lower energy density compared to high-nickel lithium-ion batteries, increasing pack weight and space requirements. This limits suitability for premium long-range vehicles and aerospace-grade applications, requiring design trade-offs that slow penetration in high-performance segments.

Global renewable installations are driving demand for long-duration storage. LiFePO4 batteries support daily cycling for 10–15 years, with 30% lower maintenance needs than alternative chemistries. Utility-scale solar-plus-storage and microgrid projects represent strong growth avenues.

Although cobalt-free, LiFePO4 batteries depend on lithium and phosphate refining capacity. Recycling recovery rates remain below 55% in several regions, requiring significant capital investment to scale closed-loop material recovery systems.

Expansion of Grid-Scale Energy Storage Systems: Global LiFePO4-based storage installations exceeded 120 GWh, with 40% annual capacity additions supporting renewable intermittency management and grid reliability.

Adoption of Cell-to-Pack and Blade Architectures: Advanced pack designs improved volumetric efficiency by 15–18%, reduced component count by 30%, and enhanced crash safety in EV platforms.

Growth in Commercial EV Fleets: Over 65% of newly launched electric commercial vehicles in 2024 adopted LiFePO4 batteries, driven by high cycle endurance and lower thermal risk.

Integration of Smart Battery Management Systems: AI-enabled BMS adoption rose by 32%, enabling real-time health diagnostics, predictive maintenance, and optimized asset utilization across large battery fleets.

The Lithium Iron Phosphate (LiFePO4) Battery Market is segmented by type, application, and end-user, each reflecting distinct adoption drivers, performance requirements, and investment priorities. By type, segmentation is shaped by form factor evolution, energy density optimization, and integration architecture, influencing suitability across mobility and stationary use cases. Application-wise, demand is driven by electrified transportation, grid-scale energy storage, and industrial power systems, with usage patterns varying by duty cycle intensity and safety requirements. From an end-user perspective, utilities, automotive OEMs, and industrial operators dominate deployment volumes, while commercial fleets and renewable developers are emerging as high-growth adopters. Across all segments, long cycle life exceeding 4,000 cycles, enhanced thermal stability, and lower degradation rates are key decision factors. The segmentation landscape highlights a clear shift toward scalable, safer, and cost-stable battery solutions aligned with decarbonization and infrastructure modernization objectives.

The market by type is primarily segmented into prismatic LiFePO4 batteries, cylindrical LiFePO4 batteries, pouch cells, and advanced integrated formats such as blade and cell-to-pack (CTP) designs. Prismatic LiFePO4 batteries currently lead the segment, accounting for approximately 48% of total adoption, due to their structural rigidity, efficient space utilization, and ease of thermal management in electric vehicles and stationary storage systems. Blade and CTP battery architectures, while currently representing a smaller base, are the fastest-growing type, expanding at an estimated 18.6% CAGR, driven by reduced module complexity, up to 15–20% improvement in volumetric efficiency, and enhanced safety under mechanical stress. Cylindrical and pouch LiFePO4 cells collectively contribute around 27% of demand, serving niche applications such as light electric vehicles, power tools, and modular storage units where flexibility and standardized sizing are prioritized.

In 2024, a nationally funded energy storage pilot deployed blade-type LiFePO4 cells in a utility-scale installation exceeding 200 MWh, demonstrating a 17% reduction in pack-level material usage while maintaining stable performance under high ambient temperatures.

By application, electric vehicles (EVs) represent the leading segment, accounting for approximately 52% of overall LiFePO4 battery usage, supported by widespread deployment in electric buses, two-wheelers, and entry-level passenger cars. Stationary energy storage systems follow with around 34% share, benefiting from daily cycling capability, long operational life, and strong compatibility with solar and wind assets. While EVs dominate today, grid-scale and commercial energy storage is the fastest-growing application, expanding at an estimated 20.1% CAGR, fueled by renewable integration mandates, microgrid development, and peak-load management requirements. Other applications, including industrial equipment, marine propulsion, and backup power systems, together contribute roughly 14% of demand.

Consumer and enterprise adoption trends further reinforce this segmentation: in 2025, more than 41% of renewable energy developers reported prioritizing LiFePO4 chemistry for new storage projects, and over 58% of fleet operators indicated a preference for LiFePO4 batteries due to lower thermal risk and predictable degradation profiles.

In 2024, a government-backed grid modernization program deployed LiFePO4-based storage across more than 120 substations, improving load-balancing efficiency for over 1.8 million connected consumers.

From an end-user perspective, automotive OEMs and commercial vehicle manufacturers form the largest segment, representing approximately 45% of total demand, driven by high-volume EV production and fleet electrification programs. Utilities and renewable energy operators follow closely with about 33% share, leveraging LiFePO4 batteries for grid stabilization, frequency regulation, and long-duration storage. Among end-users, renewable energy developers and independent power producers are the fastest-growing group, expanding at an estimated 19.4% CAGR, supported by increasing solar-plus-storage installations and distributed energy projects. Other end-users—including industrial manufacturers, logistics operators, and public infrastructure agencies—collectively account for around 22% of adoption. Adoption statistics highlight accelerating penetration: in 2025, nearly 39% of utilities globally reported piloting or scaling LiFePO4-based storage systems, while over 62% of commercial EV fleet operators favored LiFePO4 chemistry for high-utilization routes due to lower lifecycle maintenance requirements.

In 2024, a national public transportation authority transitioned over 10,000 electric buses to LiFePO4 battery systems, achieving a 23% reduction in battery-related downtime across its fleet within the first year of operation.

Asia-Pacific accounted for the largest market share at 62.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

The global Lithium Iron Phosphate (LiFePO4) Battery Market shows strong regional concentration driven by manufacturing scale, electrification intensity, and grid modernization programs. Asia-Pacific dominates due to large-scale battery production capacity exceeding 1,200 GWh annually, while North America and Europe collectively account for over 28% of global demand driven by electric mobility and stationary storage deployments. Energy storage installations using LiFePO4 chemistry represent more than 70% of new grid-scale battery projects in Asia-Pacific, compared to 48% in North America and 52% in Europe. Emerging regions such as South America and the Middle East & Africa together contribute around 9%, supported by renewable integration and infrastructure electrification. Regional adoption patterns vary significantly based on EV penetration rates, grid reliability needs, safety regulations, and lifecycle cost priorities.

The region holds approximately 18.6% of the global Lithium Iron Phosphate (LiFePO4) Battery Market by volume, driven primarily by electric vehicles, utility-scale energy storage, and commercial fleet electrification. EV buses and delivery fleets account for over 42% of LiFePO4 demand, while stationary energy storage contributes nearly 38%. Government incentives supporting domestic battery manufacturing, clean energy tax credits, and grid resilience programs are accelerating deployments. Technological advancements include cell-to-pack designs and AI-driven battery management systems improving cycle efficiency by 12–15%. A notable regional player, A123 Systems, continues to expand LiFePO4-based solutions for commercial vehicles and grid storage, focusing on high-cycle durability exceeding 6,000 cycles. Consumer behavior reflects higher enterprise-led adoption, particularly among logistics operators, utilities, and public transit agencies prioritizing safety compliance and predictable lifecycle performance.

Europe accounts for approximately 14.2% of global LiFePO4 battery demand, with Germany, France, and the UK collectively representing over 65% of regional consumption. Adoption is driven by electric buses, passenger EVs, and renewable energy storage systems, with grid-scale projects contributing nearly 40% of regional volume. Regulatory bodies emphasize battery recyclability, carbon footprint disclosure, and supply-chain transparency, increasing preference for cobalt-free chemistries such as LiFePO4. Emerging technologies include second-life battery reuse and digital traceability platforms. Regional manufacturers are investing in localized gigafactories and automation, improving energy efficiency per cell by 10%. Consumer behavior reflects strong regulatory influence, with enterprises prioritizing explainable lifecycle performance, compliance reporting, and sustainability-aligned procurement decisions.

Asia-Pacific leads the market with more than 60% share by volume and ranks first in both production and consumption. China alone accounts for over 75% of regional output, followed by India and Japan. Manufacturing trends include vertically integrated supply chains, blade battery architectures, and pack-level energy density improvements of 18–22%. Infrastructure investments exceed USD 40 billion in battery manufacturing expansion, with innovation hubs clustered around EV, grid storage, and industrial electrification ecosystems. A prominent regional player, BYD, continues to deploy blade-type LiFePO4 batteries across electric vehicles and stationary storage, achieving pack-level safety certifications under extreme thermal conditions. Consumer adoption is driven by mass-market EV penetration, shared mobility, and distributed energy systems, with cost-sensitive buyers favoring long-life, low-maintenance battery solutions.

South America represents approximately 5.1% of global market demand, led by Brazil and Argentina. Grid-scale energy storage linked to solar and wind projects accounts for nearly 46% of regional usage, followed by electric buses and industrial backup systems. Government incentives supporting renewable energy auctions and grid reliability are boosting LiFePO4 adoption. Trade policies encouraging local assembly and import duty reductions for battery components further support growth. Regional players are focusing on modular storage solutions for remote and industrial sites. Consumer behavior reflects demand tied to energy access reliability, public transport electrification, and localized infrastructure needs.

The Middle East & Africa region contributes around 3.8% of global demand, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Key demand comes from renewable energy storage, construction electrification, and off-grid power systems supporting oil & gas operations. Technological modernization includes hybrid solar-storage installations and smart microgrids. Local regulations promoting clean energy targets and cross-border trade partnerships are encouraging LiFePO4 deployments. Regional companies are adopting containerized storage systems optimized for high-temperature performance, maintaining operational stability above 50°C. Consumer behavior emphasizes durability, thermal safety, and low replacement frequency in harsh operating environments.

China – 54.8% Market Share: Dominates the Lithium Iron Phosphate (LiFePO4) Battery Market due to extensive manufacturing capacity, vertically integrated supply chains, and large-scale EV and grid storage deployments.

United States – 12.9% Market Share: Holds a strong position driven by rapid adoption of LiFePO4 batteries in electric fleets, utility-scale energy storage projects, and domestic battery manufacturing initiatives.

The Lithium Iron Phosphate (LiFePO4) Battery Market is characterized by dynamic competition with 20+ active global competitors, spanning traditional battery manufacturers, diversified energy firms, and modular storage specialists. The market demonstrates a moderate level of consolidation: the top 5 companies collectively command an estimated 42–48% share, while a broad group of mid-tier firms and regional players contribute the remainder, reflecting both scale competition and innovation diversity.

Contemporary Amperex Technology Co. Ltd. (CATL), BYD, LG Energy Solution, Samsung SDI, and SK On are key incumbents shaping the competitive hierarchy with integrated manufacturing networks, strategic partnerships, and portfolio diversification. CATL continues to expand its technology leadership with fifth‑generation LFP battery production, claiming leadership in advanced energy density and cycle life improvements, while LG Energy Solution has secured a multi‑billion dollar supply agreement with Tesla for LFP batteries manufactured in the U.S. SK On signed a first‑of‑its‑kind 7.2 GWh energy storage supply deal with Flatiron Energy Development, marking its shift into stationary ESS LiFePO4 batteries.

Strategic initiatives include joint ventures (e.g., large‑scale LFP gigafactory collaborations in Europe), localized production expansions in North America and Asia, and product launches that integrate advanced cell‑to‑pack technologies. Innovation trends influencing competition include improvements in thermal stability, scalable pack architectures, and digital Battery Management Systems (BMS) optimized for long‑life performance. Emerging entrants are increasingly focusing on niche segments like containerized storage solutions, modular ESS deployments, and hybrid chemistry platforms to diversify revenue streams and mitigate reliance on automotive demand cycles. Such competitive dynamics underscore a market in transition—balancing scale consolidation with an expanding ecosystem of innovators tailored to diverse energy and mobility applications.

BYD Company Ltd.

SK On

Panasonic Corporation

EVE Energy

A123 Systems

Gotion High-Tech

Farasis Energy

Northvolt

East Penn Manufacturing

SAFT

First Phosphate

American Battery Factory

SIG Energy Technology

The technology landscape of the Lithium Iron Phosphate (LiFePO4) Battery Market is evolving rapidly, driven by advances in materials science, manufacturing processes, and system integration that enhance safety, durability, and performance for diverse applications. Cell‑to‑pack (CTP) design has become a leading architectural approach, enabling significant improvements in volumetric efficiency by eliminating module layers and increasing usable energy within a given pack footprint. This innovation enhances energy density metrics without compromising the inherent safety advantages of LFP chemistry.

Manufacturers are also integrating advanced Battery Management Systems (BMS) that incorporate real‑time diagnostics, predictive maintenance, and adaptive thermal control. These systems optimize charge/discharge cycling and extend service life, particularly in utility and industrial storage environments where consistent performance over thousands of cycles is essential. Emerging materials innovations include optimized electrode compositions and electrolyte formulations that reduce degradation rates under high‑temperature conditions, extending calendar life and reliability in harsh climates.

Manufacturing digitalization and automation are reducing defect rates and improving throughput; automated quality inspection and AI‑driven process control are enabling tighter tolerances and consistent output across high‑volume gigafactory lines. Meanwhile, hybrid cell chemistries combining LiFePO4 with enhancements like silicon anodes or solid electrolyte components are under development to bridge the performance gap with higher‑energy density alternatives while retaining cost and safety benefits.

In stationary applications, modular energy storage units—pre‑configured with integrated LFP battery systems and power conversion subsystems—are reducing deployment time and enabling scalability from small commercial sites to multi‑megawatt grid installations. In the automotive segment, progress in blade and structural cell formats has improved crash resilience and thermal management, supporting integration into vehicle platforms without extensive cooling infrastructure.

The continual refinement of manufacturing technologies, digital integration tools, and materials innovations positions LiFePO4 chemistry as a versatile foundation for next‑generation energy storage, balancing affordability, safety, and operational longevity for electrification across sectors.

• In September 2025, South Korea’s SK On signed an agreement to supply up to 7.2 GWh of LFP batteries for energy storage systems (ESS) to Flatiron Energy Development between 2026 and 2030, marking its first major ESS‑focused LFP contract and expansion beyond EV applications. Source: www.reuters.com

• In July 2025, LG Energy Solution secured a $4.3 billion contract to supply lithium iron phosphate batteries globally over three years from August 2027 to July 2030, with production originating from its U.S. LFP facilities. Source: www.reuters.com

• In December 2025, major Korean battery makers including LG Energy Solution, Samsung SDI, and SK On formally accelerated LFP production for energy storage systems amid shifting EV demand, expanding output at facilities in Michigan, Poland, and South Korea to support the growing ESS market. Source: www.koreajoongangdaily.joins.com

• In July 2024, LG Energy Solution signed a large‑scale supply agreement with Renault’s EV subsidiary Ampere to deliver approximately 39 GWh of LFP battery packs from its European facilities, supporting production of around 590,000 EVs starting in 2026. Source: www.energytrend.com

The scope of the Lithium Iron Phosphate (LiFePO4) Battery Market Report encompasses a holistic analysis of product types, applications, end‑user segments, regional dynamics, technology evolution, competitive forces, and emerging trends. Product coverage includes all major LiFePO4 cell formats such as prismatic, cylindrical, pouch, and advanced integrated designs (e.g., blade and cell‑to‑pack), with insights on their performance characteristics, safety profiles, and deployment contexts across EVs, stationary storage, and industrial power systems.

Application analysis spans electric vehicles, energy storage systems, industrial equipment, and specialized sectors such as backup power infrastructure and microgrid projects, highlighting usage patterns, duty cycle requirements, and technology fit. End‑user segmentation examines demand drivers and procurement behaviors among automotive OEMs, utilities, renewable developers, commercial fleets, and residential energy adopters.

The geographic lens covers North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with a focus on manufacturing localization, policy support frameworks, and infrastructure investment flows shaping regional adoption. Technology insights explore battery architecture innovation, advanced materials research, digital integration, and manufacturing advancements that improve energy density, lifecycle reliability, and cost efficiency.

The report also includes detailed competitive intelligence on leading and emerging players, strategic partnerships, market positioning, and the evolving landscape of supply chain integration. By integrating these dimensions, the report aims to provide decision‑makers with actionable intelligence to inform investment planning, product strategy, and market entry decisions in a rapidly transforming global energy storage ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,480.0 Million |

| Market Revenue (2033) | USD 4,654.9 Million |

| CAGR (2026–2033) | 15.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Contemporary Amperex Technology Co. Ltd (CATL), LG Energy Solution, Samsung SDI, BYD Company Ltd., SK On, Panasonic Corporation, EVE Energy, A123 Systems, Gotion High-Tech, Farasis Energy, Northvolt, East Penn Manufacturing, SAFT, First Phosphate, American Battery Factory, SIG Energy Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |