Reports

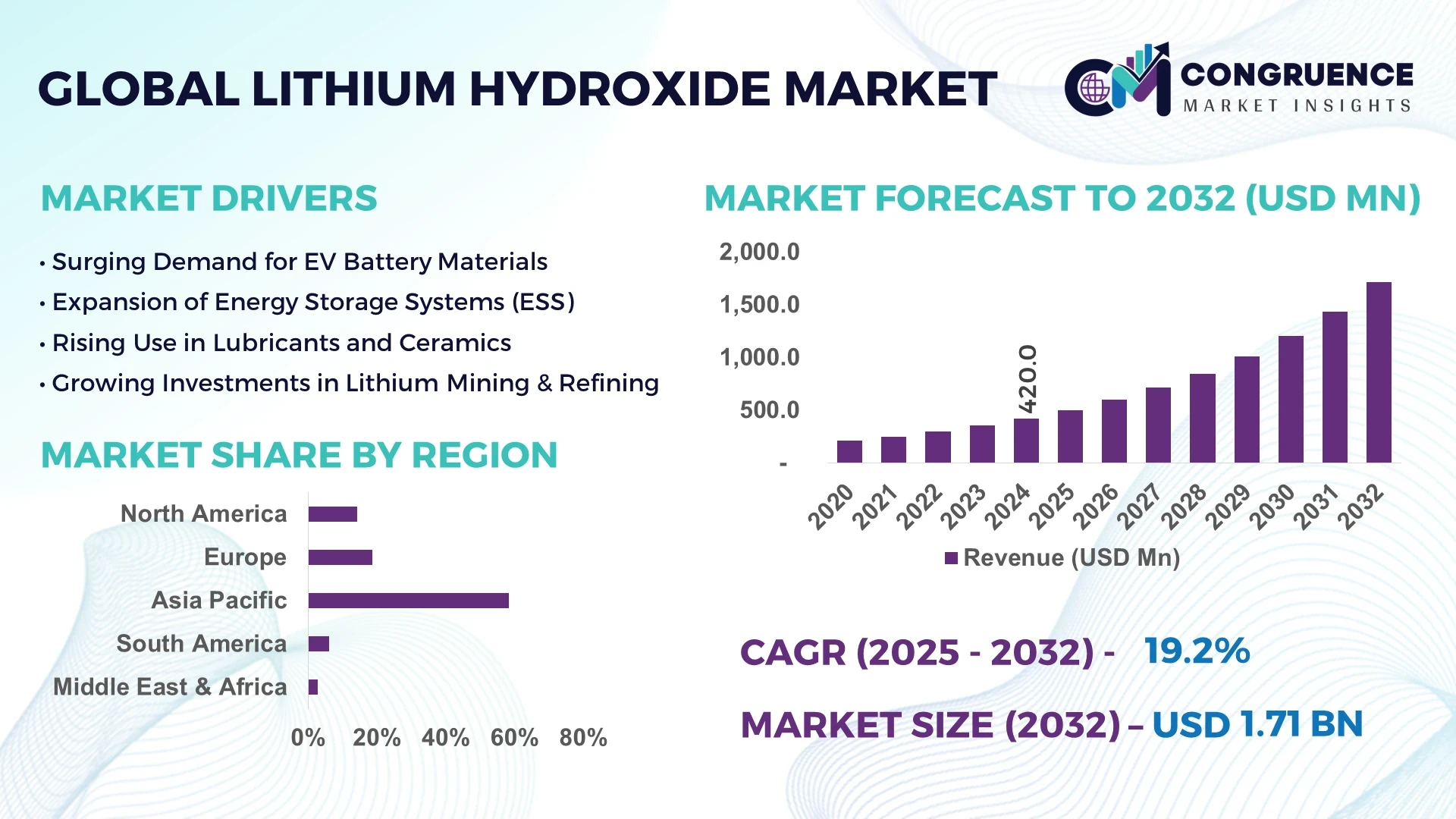

The Global Lithium Hydroxide Market was valued at USD 420.0 Million in 2024 and is anticipated to reach a value of USD 1,711.8 Million by 2032 expanding at a CAGR of 19.2% between 2025 and 2032.

China remains the leading force in the global Lithium Hydroxide Market, with a production capacity exceeding 200,000 tons annually, supported by strategic investments in refining infrastructure, advanced processing technology, and vertically integrated supply chains catering to battery-grade hydroxide used in electric vehicles and energy storage systems.

The Lithium Hydroxide Market is driven by a robust demand across several high-growth sectors, primarily electric vehicles (EVs), energy storage, consumer electronics, and industrial lubricants. The EV industry alone accounts for over 70% of global consumption due to the compound’s role in manufacturing high-nickel cathode batteries, which offer greater energy density and performance. Technological innovations, including direct lithium extraction (DLE) and more sustainable refining techniques, are improving yield rates and reducing environmental impact. Regulatory frameworks—particularly in the EU, U.S., and East Asia—continue to push for cleaner energy storage materials, further incentivizing lithium hydroxide adoption. Regionally, Asia-Pacific leads consumption due to strong EV manufacturing bases, while North America and Europe are rapidly expanding domestic capacities. Future trends suggest growing integration of recycling streams, AI-driven process optimization, and tighter supply chain controls to mitigate geopolitical risks and meet the escalating demand for high-purity lithium hydroxide across the globe.

Artificial Intelligence is playing a pivotal role in revolutionizing the Lithium Hydroxide Market by enhancing precision, efficiency, and scalability across production, logistics, and quality assurance. AI algorithms are being deployed to monitor and control complex chemical processes in real time, enabling lithium refiners to optimize operational parameters such as temperature, pressure, and chemical ratios. This has led to a reduction in energy consumption by up to 18% in advanced refineries. Predictive maintenance powered by AI analytics reduces equipment downtime by 25–30%, directly improving output reliability and minimizing costly interruptions. In logistics and inventory management, machine learning tools are streamlining global supply chain operations by forecasting raw material availability and adjusting procurement in advance to avoid bottlenecks. Furthermore, AI-driven quality control systems using visual recognition and sensor data are ensuring consistent battery-grade purity levels, a critical requirement for EV manufacturers. These technologies are also being used to simulate future market conditions and aid strategic planning, offering stakeholders a competitive edge.

“In early 2025, a major lithium processing facility in Western Australia implemented an AI-powered digital twin system that reduced processing variability by 22% and increased lithium hydroxide yield by 12.7%, through real-time simulations and predictive analytics integrated directly into the production line.”

The Lithium Hydroxide Market is experiencing accelerated transformation driven by structural demand from battery manufacturers, regulatory pushes toward sustainability, and evolving extraction and refinement technologies. With the shift toward high-performance batteries requiring lithium hydroxide over carbonate, market participants are recalibrating investment strategies to secure access to higher-purity lithium sources. Additionally, integration of AI, data analytics, and automation across processing plants is significantly optimizing production cycles. Environmental considerations, particularly around water use and tailings management, are prompting adoption of cleaner technologies and tighter regulatory compliance. Regionally, market activity is concentrated in Asia-Pacific, with growing investments now flowing into Latin America and Africa. The global push for clean energy infrastructure, particularly grid-scale storage and electrified transport, continues to fuel long-term demand.

The global transition to electric mobility is significantly impacting the Lithium Hydroxide Market, primarily through the rising demand for high-nickel NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminum) battery chemistries. Lithium hydroxide is essential for producing these high-nickel cathodes, which offer improved energy density and thermal stability over alternatives. Recent data indicates that over 80% of new electric vehicle battery production lines being established in China and Europe are designed for high-nickel battery chemistries. As governments tighten emissions regulations and EV manufacturers target longer-range vehicles, lithium hydroxide demand is expected to grow more rapidly than carbonate-based alternatives. Strategic partnerships between battery producers and lithium refiners are becoming common to secure long-term supplies of battery-grade lithium hydroxide and ensure consistent quality and availability.

The Lithium Hydroxide Market faces notable challenges due to the significant environmental footprint associated with lithium extraction and refining. Particularly, the conversion of spodumene and brine into lithium hydroxide involves energy-intensive processes and considerable freshwater use. In regions like South America, where water scarcity is already a pressing issue, lithium extraction has led to ecological concerns, prompting stricter environmental scrutiny. In Australia and China, refiners are under increasing pressure to adopt greener practices or face operational slowdowns due to community and governmental opposition. These environmental and water management issues not only raise operating costs but also delay permitting for new projects. As a result, industry players must invest heavily in cleaner technologies and community engagement strategies to maintain social license and compliance.

The advancement of Direct Lithium Extraction (DLE) technologies presents a transformative opportunity in the Lithium Hydroxide Market. Unlike traditional evaporation pond methods that can take up to 18 months and yield lower recovery rates, DLE can extract lithium within hours and with recovery efficiencies exceeding 80%. Several pilot projects in North America and South America have demonstrated successful scalability, positioning DLE as a potential game-changer in lithium hydroxide supply chains. These technologies also reduce land use and water consumption, aligning with global sustainability objectives. DLE’s ability to produce battery-grade lithium hydroxide more efficiently makes it especially attractive for regions lacking extensive solar evaporation conditions. Investors and government programs are increasingly directing funds toward commercializing DLE platforms, suggesting this trend will accelerate over the coming years.

The Lithium Hydroxide Market is heavily exposed to geopolitical risks due to its reliance on a geographically concentrated supply chain. Most lithium refining and hydroxide production facilities are located in China, which has led to concerns among Western markets over potential supply disruptions and strategic dependencies. Trade disputes, export restrictions, and evolving foreign investment regulations are complicating procurement strategies and introducing volatility into pricing and availability. Additionally, efforts by the U.S., EU, and others to localize lithium refining face technical and regulatory hurdles, slowing diversification efforts. Companies are now forced to navigate complex geopolitical landscapes while securing long-term contracts and considering dual sourcing, all of which increase operational complexity and cost.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Lithium Hydroxide Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Investment Surge in Western Lithium Refining Facilities: Over the past 18 months, North America and the EU have collectively announced more than 25 new lithium hydroxide refining projects. These investments are intended to reduce dependence on Asian processing facilities and support regional battery manufacturing hubs. Notably, several facilities are leveraging renewable power inputs and AI-based operational management systems to reduce carbon footprints.

Growing Integration of Battery Recycling Technologies: As end-of-life lithium-ion batteries increase, the integration of closed-loop recycling systems is becoming a defining trend in the Lithium Hydroxide Market. Advanced hydrometallurgical processes now allow for the recovery and conversion of lithium compounds back into battery-grade hydroxide with over 95% efficiency. This not only supports supply stability but also aligns with circular economy principles.

Technological Collaboration in EV Supply Chains: Strategic collaborations between lithium hydroxide producers and EV manufacturers are intensifying. Companies are entering into joint development agreements to co-design battery materials with specific performance metrics. This collaboration ensures consistency in cathode material supply and enhances performance outcomes, particularly for long-range and high-speed vehicle models.

The Lithium Hydroxide Market is strategically segmented based on type, application, and end-user insights, each offering distinct growth dynamics and value contributions. Type-wise, the market is divided into battery-grade, technical-grade, and industrial-grade lithium hydroxide, with battery-grade dominating due to its critical role in EV battery production. Application segmentation spans batteries, lubricants, polymers, ceramics, and others—each segment reflecting specialized usage trends. Among end-users, automotive, electronics, aerospace, industrial manufacturing, and energy storage stand out, with the automotive sector holding a leading share. The segmentation landscape is shaped by factors such as shifting raw material preferences, regulatory compliance requirements, and evolving end-use technology standards. Each segment plays a vital role in addressing specific performance criteria and sustainability benchmarks within this high-demand global market.

Battery-grade lithium hydroxide remains the leading product type in the global market due to its indispensable role in high-energy density lithium-ion battery production. It is the preferred input for nickel-rich cathodes like NMC 811 and NCA, both of which are essential for long-range electric vehicles. Its superior thermal stability and compatibility with high-voltage battery chemistries have solidified its position as the industry’s benchmark standard. The fastest-growing type is technical-grade lithium hydroxide, driven by increased use in industrial lubricants and ceramics, where purity levels are less stringent but demand for performance materials is rising. Technical-grade is gaining traction in high-temperature greases used in wind turbines and heavy machinery, where durability under extreme pressure is essential. Industrial-grade lithium hydroxide, although limited in volume, continues to serve niche roles in sectors such as glass production and air purification systems. While its contribution remains smaller, it fulfills essential requirements in applications that value cost-efficiency over ultra-high purity.

The battery segment dominates the Lithium Hydroxide Market, accounting for the majority of consumption due to the explosive growth of electric vehicles and grid-scale energy storage systems. Lithium hydroxide’s compatibility with high-nickel cathode chemistries makes it indispensable for battery manufacturers seeking greater energy efficiency, safety, and charge cycles. The fastest-growing application is in energy storage systems (ESS), particularly with the expansion of renewable energy grids in North America, Europe, and East Asia. Government mandates for cleaner energy infrastructure and increased investments in solar and wind projects are accelerating ESS deployment, thus boosting demand for lithium hydroxide-based batteries. Other significant applications include lubricants, where lithium hydroxide is used in the formulation of high-performance greases, and the ceramics industry, which relies on it to improve heat resistance and glaze quality. Though smaller in scale, these applications are critical to specific industrial sectors and contribute to a well-diversified market structure.

The automotive industry is the primary end-user in the Lithium Hydroxide Market, driven by the aggressive global shift toward electric vehicles. EV manufacturers increasingly demand high-purity lithium hydroxide to support advanced battery technologies capable of delivering longer ranges and faster charging times. Production expansions by leading carmakers and localized battery manufacturing in Europe and North America have cemented automotive’s dominance in this space. The fastest-growing end-user segment is energy utilities and grid operators, fueled by the need to stabilize intermittent renewable energy sources through advanced storage systems. As governments mandate higher renewable energy adoption, utility companies are rapidly scaling up ESS capacity, thereby increasing demand for lithium hydroxide. Other notable end-users include the electronics industry, which utilizes lithium-based power sources for consumer devices, and the aerospace sector, where lightweight, high-efficiency energy storage is critical. These segments, while secondary in scale, contribute to the broader adoption and innovation cycles within the lithium hydroxide ecosystem.

Asia-Pacific accounted for the largest market share at 58.3% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 21.7% between 2025 and 2032.

Asia-Pacific’s dominance stems from the presence of major lithium hydroxide processing facilities, particularly in China, and a robust battery manufacturing ecosystem. The region is also home to top electric vehicle producers and lithium-rich reserves in countries like Australia. Meanwhile, North America's growth trajectory is being propelled by escalating investments in domestic EV battery production, strategic collaborations, and government support for critical mineral independence. Regionally tailored regulations, evolving consumer preferences, and increasing downstream applications are further shaping the competitive landscape of the Lithium Hydroxide Market across global geographies.

North America captured approximately 14.2% of the global Lithium Hydroxide Market in 2024, driven largely by the rapid growth of electric vehicle production and energy storage systems. The United States and Canada are leading demand due to federal initiatives supporting EV infrastructure and battery supply chain localization. The automotive and renewable energy sectors are the region's top consumers of lithium hydroxide, seeking high-purity inputs for long-life, high-capacity batteries. Regulatory frameworks like the Inflation Reduction Act are incentivizing domestic sourcing and refining of critical minerals. Additionally, digital transformation trends—such as AI-based process optimization and the use of digital twin technology in lithium refining—are being adopted across facilities to improve yield and efficiency. The growing presence of joint ventures between battery manufacturers and lithium producers marks a strategic shift toward supply chain resilience.

Europe accounted for roughly 18.7% of the global Lithium Hydroxide Market in 2024, with strong demand led by Germany, the United Kingdom, and France. The continent’s focus on decarbonization and automotive electrification is driving consumption in battery-grade lithium hydroxide. Regulatory bodies such as the European Commission are enforcing strict sustainability guidelines, pushing manufacturers to adopt ethically sourced and locally processed materials. Additionally, Europe's Green Deal and Critical Raw Materials Act are accelerating investment in lithium refining and recycling facilities. Emerging technologies like Direct Lithium Extraction (DLE) and AI-powered quality control systems are being introduced to meet purity and efficiency standards. The region’s shift toward strategic autonomy in battery production continues to boost regional lithium hydroxide demand, especially among next-generation EV battery manufacturers.

Asia-Pacific dominated the global Lithium Hydroxide Market in 2024, accounting for an estimated 58.3% of total market volume. China remains the region’s largest consumer and producer, followed by Japan and South Korea. The regional surge in electric vehicle production, large-scale battery manufacturing, and clean energy initiatives is propelling demand for battery-grade lithium hydroxide. Australia’s robust spodumene mining infrastructure further strengthens regional supply chains. Significant manufacturing clusters, particularly in China’s Sichuan and Jiangxi provinces, are equipped with advanced refining capabilities and AI-driven process controls. Technology innovation hubs like Shenzhen and Tokyo are also accelerating the integration of automated systems into lithium hydroxide production. Asia-Pacific remains critical for global battery supply chains due to its scale, infrastructure maturity, and sustained policy support for electrification and decarbonization.

South America holds a growing presence in the Lithium Hydroxide Market, contributing approximately 6.1% to global market share in 2024. Key countries such as Brazil and Argentina are driving this momentum through large lithium reserves and increased foreign direct investment in refining capacity. Argentina’s lithium triangle is seeing the integration of new lithium-to-hydroxide conversion plants aimed at supplying global battery manufacturers. Brazil, on the other hand, is promoting domestic battery production supported by regulatory frameworks that favor value-added processing over raw material exports. Regional governments are also offering tax incentives and trade agreements to attract downstream investment. Infrastructure improvements, including rail and port upgrades, are enabling more efficient export logistics. These developments collectively position South America as an emerging strategic supplier within the global Lithium Hydroxide Market.

The Middle East & Africa region is gaining traction in the Lithium Hydroxide Market, with emerging demand from industrial, energy, and construction sectors. South Africa and the UAE are notable contributors, leveraging resource availability and infrastructural investment. South Africa’s mining sector is exploring lithium extraction and local refinement to support regional industrialization, while the UAE is focusing on battery storage technologies as part of its clean energy goals. Technological modernization across refining facilities, including digitalized monitoring and process automation, is gradually improving regional capabilities. Local regulations are increasingly aligned with international standards to facilitate trade and attract foreign investment. Though currently accounting for a modest 2.7% of global demand, the region shows potential for accelerated development through public-private partnerships and strategic alliances with global battery supply chain players.

China – 51.2% Market Share

High production capacity, advanced refining infrastructure, and strong end-user battery demand drive China’s leadership in the Lithium Hydroxide Market.

Australia – 13.4% Market Share

Major source of spodumene concentrate with expanding domestic conversion facilities supporting global lithium hydroxide production.

The Lithium Hydroxide Market is marked by an increasingly competitive environment with over 50 active global and regional participants competing across various value chain stages. The market is primarily characterized by vertically integrated companies with operations ranging from lithium extraction to hydroxide refinement. Leading competitors are prioritizing capacity expansion, especially in North America, Asia-Pacific, and Europe, where demand for battery-grade lithium hydroxide continues to surge. Recent trends indicate a wave of strategic collaborations between lithium refiners and electric vehicle or battery manufacturers, aimed at securing long-term supply agreements and improving material performance. Mergers and acquisitions are also reshaping the landscape, enabling companies to gain access to new reserves, processing technologies, and geographic markets. Innovation remains a key differentiator—firms investing in AI-powered process optimization, sustainable extraction methods, and advanced purification technologies are gaining competitive advantages. Moreover, regional players are emerging with niche capabilities in low-impurity or specialty-grade lithium hydroxide, contributing to product diversification and intensifying global competition.

Albemarle Corporation

Tianqi Lithium Corporation

Ganfeng Lithium Co., Ltd.

Livent Corporation

SQM (Sociedad Química y Minera de Chile S.A.)

Nemaska Lithium Inc.

AMG Lithium GmbH

Pilbara Minerals Limited

Chengxin Lithium Group Co., Ltd.

IGO Limited

Vulcan Energy Resources

Allkem Limited

Eramet S.A.

Technological innovation is playing a pivotal role in shaping the Lithium Hydroxide Market, with advancements influencing extraction, processing, and quality control. A key development is the widespread testing and deployment of Direct Lithium Extraction (DLE) technologies, which significantly improve lithium recovery rates—often exceeding 80%—while reducing water usage and environmental impact. These systems are increasingly being integrated into brine-based operations, replacing traditional solar evaporation methods. In the area of refining, AI and machine learning are now deployed to optimize conversion processes from spodumene and brine into battery-grade lithium hydroxide. These technologies have improved yield consistency and reduced energy consumption by up to 18% in several pilot plants.

Additionally, digital twin models are now being applied in operational control systems to simulate and manage refinery conditions in real-time. The adoption of hydrometallurgical processes—particularly in recycling—has enabled the extraction of lithium hydroxide from end-of-life batteries with over 95% purity, creating a viable circular economy pathway. Automation in packaging and logistics has also improved material handling for lithium hydroxide powders and granules, increasing efficiency and reducing contamination risks. As regulatory and environmental pressures mount, more facilities are adopting closed-loop water systems, solar integration, and emissions control technologies to meet sustainability benchmarks, further pushing the market toward greener, smarter operations.

• In February 2024, Albemarle began construction of a new lithium hydroxide processing facility in South Carolina, designed with a planned annual capacity of 50,000 metric tons and equipped with AI-driven process automation systems.

• In October 2023, Ganfeng Lithium launched an advanced pilot facility in Jiangxi Province utilizing Direct Lithium Extraction (DLE) from geothermal brines, reporting a 30% reduction in processing time and 25% improvement in resource utilization.

• In March 2024, Livent Corporation partnered with a U.S.-based battery manufacturer to supply high-purity lithium hydroxide under a five-year agreement, with plans to scale supply from its expanded Argentina operations.

• In July 2023, AMG Lithium inaugurated a refining plant in Germany capable of producing 20,000 tons of battery-grade lithium hydroxide annually, reinforcing Europe’s strategic battery materials infrastructure.

The Lithium Hydroxide Market Report provides an in-depth analysis of the global market, covering a broad range of critical areas including product types, applications, end-user industries, technologies, and geographic regions. The report focuses on three key product types—battery-grade, technical-grade, and industrial-grade lithium hydroxide—each addressing distinct performance specifications and industrial requirements. Applications analyzed include batteries, lubricants, ceramics, polymers, and specialty uses, with a strong emphasis on battery-related demand, especially for high-nickel cathode chemistries.

Geographically, the report evaluates market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting region-specific trends, infrastructure development, regulatory frameworks, and end-use market drivers. It also explores the technological advancements shaping the market, such as Direct Lithium Extraction, AI-driven operational systems, and lithium recycling processes. Additionally, the report profiles leading companies, maps recent strategic developments, and identifies growth opportunities in emerging markets and secondary applications such as grid energy storage and industrial lubricants. Tailored for business executives, analysts, and strategic planners, the report serves as a comprehensive resource for understanding the competitive and technological landscape of the Lithium Hydroxide Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 420.0 Million |

| Market Revenue (2032) | USD 1,711.8 Million |

| CAGR (2025–2032) | 19.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Albemarle Corporation, Tianqi Lithium Corporation, Ganfeng Lithium Co., Ltd., Livent Corporation, SQM (Sociedad Química y Minera de Chile S.A.), Nemaska Lithium Inc., AMG Lithium GmbH, Pilbara Minerals Limited, Chengxin Lithium Group Co., Ltd., IGO Limited, Vulcan Energy Resources, Allkem Limited, Eramet S.A. |

| Customization & Pricing | Available on Request (10% Customization is Free) |