Reports

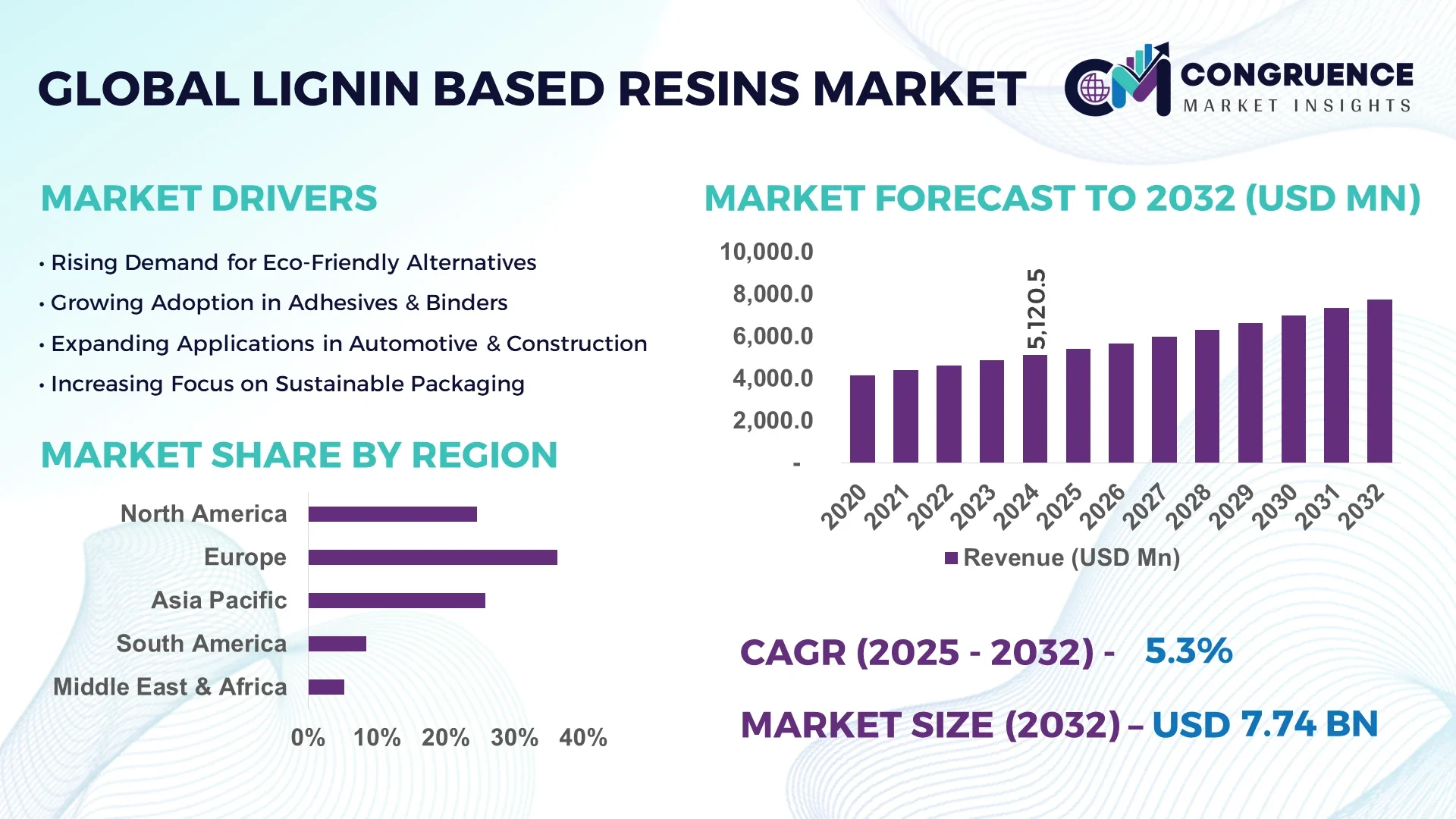

The Global Lignin Based Resins Market was valued at USD 5,120.5 Million in 2024 and is anticipated to reach a value of USD 7,757.6 Million by 2032 expanding at a CAGR of 5.33% between 2025 and 2032.

The United States leads in the production and industrial utilization of lignin-based resins, backed by substantial investments in biorefinery infrastructure, advanced polymer processing technologies, and a well-established industrial base. The U.S. also benefits from research collaboration between government institutions and major chemical manufacturers that continuously optimize lignin conversion technologies.

The Lignin Based Resins Market is gaining traction across multiple industries including construction, automotive, adhesives, coatings, and agriculture. These resins are increasingly adopted as sustainable alternatives to phenol and formaldehyde-based materials due to their low toxicity and renewability. In the construction sector, lignin-based phenolic resins are being integrated into plywood, insulation, and engineered wood products. Technological advances have enabled improved lignin purification and resin modification, expanding their use in high-performance applications. In agriculture, lignin-based encapsulants for fertilizers and pesticides are showing strong market potential due to environmental regulations. Moreover, rising demand for low-carbon and bio-based raw materials in packaging and consumer goods is supporting growth across Europe and Asia-Pacific. Regulatory bodies in several countries are incentivizing biopolymer use, influencing procurement patterns in both public infrastructure and consumer manufacturing. The market is also witnessing increased R&D activities aimed at enhancing resin mechanical properties and thermal resistance, making them suitable for more demanding industrial uses.

Artificial Intelligence (AI) is playing an increasingly influential role in transforming the Lignin Based Resins Market by optimizing manufacturing processes, improving formulation accuracy, and accelerating R&D efforts. AI-powered predictive modeling is now commonly used to simulate lignin behavior under varying thermal and chemical conditions, which helps manufacturers design resins with tailored properties for specific industrial applications. This significantly reduces trial-and-error time in labs, cutting development cycles by up to 30%.

AI-enabled systems are also being used to optimize lignin extraction processes from biomass sources. By integrating real-time sensor data and machine learning algorithms, companies can enhance lignin yield, reduce energy consumption, and improve batch consistency. In addition, AI-driven supply chain analytics are aiding procurement managers in forecasting raw material availability and minimizing waste. Machine learning algorithms are also identifying new lignin derivative combinations to expand resin application areas.

Furthermore, AI tools are streamlining regulatory compliance by automatically validating environmental and safety benchmarks throughout product development. From early-stage molecular design to final resin blending, AI technologies are supporting efficiency and sustainability improvements in the Lignin Based Resins Market, making them an essential part of future-proofing operations.

“In April 2024, a U.S.-based chemical company implemented an AI-driven formulation platform that improved the tensile strength of its lignin-based resin products by 18% while reducing manufacturing waste by 22%, demonstrating the measurable impact of AI on both product quality and process efficiency.”

The Lignin Based Resins Market is characterized by increasing demand for bio-based materials and environmental regulations pushing industries to reduce reliance on synthetic chemicals. Innovation in lignin purification and integration into high-performance resin systems is opening new opportunities, especially in packaging, construction, and automotive sectors. Regional growth is driven by increased funding in biorefinery R&D in North America and Europe, while Asia-Pacific exhibits significant manufacturing scalability potential. Market stakeholders are focused on improving resin mechanical properties and compatibility with various industrial substrates to enhance product viability across applications.

The push toward sustainable production is a major driver for the Lignin Based Resins Market. With rising environmental concerns and tightening regulatory frameworks, industries such as packaging, construction, and automotive are shifting to bio-based inputs. Lignin-based resins offer a renewable alternative to petroleum-derived adhesives and composites, reducing carbon footprint and toxic emissions. In packaging, lignin-based resins are increasingly used in barrier coatings for biodegradable films. Moreover, large-scale construction projects in Europe and the U.S. are beginning to specify bio-based resins in procurement tenders, further accelerating industrial uptake.

A significant limitation affecting the Lignin Based Resins Market is the inconsistency in feedstock quality derived from different biomass sources and processing conditions. This variation affects the chemical structure of lignin, leading to unpredictable resin performance and reduced reliability in end-use applications. Manufacturers often require additional refining or blending steps to achieve consistent output, increasing operational costs. The lack of standardized feedstock grading and limited commercial infrastructure for lignin purification adds to supply chain complexity and deters wider industrial adoption, especially in applications that require strict mechanical and chemical consistency.

An emerging opportunity lies in the increasing investment in high-performance bio-composite materials. Lignin-based resins, when combined with natural fibers, can be used to develop strong, lightweight, and thermally stable composites for the automotive and aerospace industries. Government-funded initiatives across North America and Europe are actively supporting pilot projects to commercialize such materials. These initiatives also include grants for startups innovating in resin chemistry and scaling modular processing systems. The potential for lignin-based composites to replace traditional polymers without sacrificing performance is creating new commercialization pathways in high-value manufacturing.

Despite their environmental advantages, lignin-based resins face technical and financial hurdles due to the high cost of lignin modification processes. Functionalizing lignin to meet industrial performance standards involves complex chemical treatments and specialized equipment, limiting commercial scalability. Additionally, the scarcity of processing facilities capable of handling high-purity lignin impedes supply chain development. This is particularly challenging for small and mid-sized manufacturers that lack access to capital-intensive infrastructure. Until cost-efficient and scalable technologies are developed, widespread adoption in high-volume industries remains constrained.

Advancement in Reactive Lignin Modification Techniques: Recent developments in reactive chemistry have enabled more precise modification of lignin molecules, resulting in resins with enhanced bonding strength and thermal resistance. This trend is particularly visible in wood adhesives and composite materials, where improved performance has expanded lignin resin use into new structural applications. Pilot projects in Germany and South Korea are currently scaling modified lignin production using low-energy catalytic pathways.

Growth in Biodegradable Packaging Solutions: The packaging industry is rapidly integrating lignin-based resins into biodegradable coating and barrier solutions. These resins help improve the moisture and oxygen resistance of paper-based packaging, enhancing shelf life while complying with plastic reduction mandates. As consumer goods companies increase investment in sustainable packaging, demand for lignin resins in food-grade and cosmetic applications has grown markedly across Europe and Japan.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Lignin Based Resins Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Increasing Focus on Carbon-neutral Material Sourcing: Manufacturers are prioritizing carbon-neutral sourcing by integrating lignin derived from sustainably managed forestry operations. This aligns with broader ESG goals and enables companies to differentiate in eco-conscious markets. Certification programs and blockchain tracking tools are increasingly used to verify sustainable sourcing across supply chains, strengthening transparency and brand credibility.

The Lignin Based Resins Market is segmented by type, application, and end-user, each presenting diverse demand dynamics and innovation trends. By type, the market is characterized by a broadening range of lignin-based resins including phenolic, epoxy, and polyurethane resins tailored to meet industry-specific performance criteria. Applications are diverse, with a growing focus on wood adhesives, packaging coatings, and high-performance composites. End-user insights reveal the growing prominence of construction, automotive, and packaging industries, each leveraging lignin-based resins for their sustainability and performance benefits. The segmentation analysis underscores a clear shift toward bio-based materials that balance mechanical strength with environmental responsibility. Innovation in lignin chemistry is expanding product utility beyond traditional uses, particularly in sectors prioritizing carbon-neutral materials. Each segment reflects strategic adoption pathways shaped by evolving regulatory mandates, consumer preferences, and performance benchmarks across global manufacturing sectors.

Lignin-based phenolic resins dominate the market due to their widespread use in adhesives and binders for plywood, oriented strand boards (OSB), and insulation materials. Their thermal stability, water resistance, and compatibility with wood substrates make them the preferred choice in the construction and furniture industries. These resins are increasingly replacing petroleum-based phenolics in formaldehyde-restricted applications, offering an eco-conscious yet high-performance solution.

Epoxy lignin resins are emerging as the fastest-growing type, driven by their potential use in high-strength composites, electronics, and automotive parts. Advances in lignin functionalization have improved the adhesion, curing behavior, and chemical resistance of these resins, allowing them to compete with synthetic epoxies in performance-intensive environments. They are especially favored in lightweight structural components and in green electronics packaging solutions.

Polyurethane lignin resins serve niche segments in coatings, sealants, and flexible foams, offering improved biodegradability. Although still in developmental phases compared to phenolics and epoxies, their tunable properties make them promising for customized industrial uses. Other resin types, such as acrylate or polyester-lignin blends, are also being evaluated for specialty coatings and biomedical applications, though their market penetration remains limited. Overall, product innovation and compatibility with industrial systems continue to shape the competitive dynamics in this segment.

Wood adhesives represent the leading application in the Lignin Based Resins Market, largely due to the extensive use of lignin-phenol blends in the production of engineered wood products. These adhesives offer strong bonding, improved environmental profiles, and are compliant with low-emission construction regulations. They are increasingly preferred in green buildings and sustainable construction projects where conventional formaldehyde-based adhesives are restricted.

The fastest-growing application is biodegradable packaging coatings. As regulatory pressure mounts to reduce single-use plastics, lignin-based coatings are gaining adoption in food packaging, personal care products, and consumer goods. These coatings improve barrier performance against moisture and oxygen while maintaining compostability standards. Packaging manufacturers are scaling lignin-based solutions to meet increasing demand for eco-labeled products, particularly in Europe and Asia.

Other applications such as molded composites, insulation foams, and sealants are expanding steadily. In molded parts, lignin resins are used to reduce weight and enhance strength in automotive interiors. In foams and sealants, the bio-based composition helps companies meet green procurement criteria while offering comparable performance to traditional materials. As application innovation accelerates, lignin-based resins are expected to integrate into more multifunctional products across sectors.

The construction industry stands out as the leading end-user segment in the Lignin Based Resins Market. Driven by increasing demand for sustainable building materials, lignin-based phenolic adhesives are widely used in wood panels, insulation boards, and structural laminates. The preference for low-emission, durable, and environmentally safe binders in green buildings and public infrastructure projects has significantly boosted the use of lignin-based alternatives.

The packaging industry is emerging as the fastest-growing end-user, propelled by the global push for sustainable and biodegradable solutions. Lignin-based coatings and films offer viable replacements for petroleum-based materials, aligning with new legislation banning non-recyclable plastic packaging. The trend is particularly strong in the food, beverage, and cosmetics sectors, where brand owners seek eco-friendly packaging to meet consumer expectations and regulatory mandates.

Other significant end-users include the automotive and electronics industries. In automotive, lignin-based epoxy resins are being explored for lightweight composites, soundproofing panels, and interior trims, all contributing to improved fuel efficiency and sustainability goals. In electronics, lignin-based dielectric materials and thermosets are under development for low-toxicity and thermally stable applications. Collectively, these end-users reflect a growing commitment across industries to incorporate renewable raw materials into their production ecosystems.

Europe accounted for the largest market share at 36.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

Europe’s leadership is largely attributed to stringent environmental policies and robust demand from the construction and packaging sectors. Germany, France, and the Nordics are prioritizing bio-based resin adoption in engineered wood, insulation, and food packaging. In contrast, Asia-Pacific's rapid industrialization, especially in China and India, is creating substantial demand for sustainable materials in automotive, construction, and electronics. Regional governments are also launching initiatives to reduce dependence on petroleum-derived resins. Across all regions, lignin-based resins are gaining momentum as industries respond to green procurement mandates and global net-zero emission goals. The competitive landscape is increasingly shaped by localized production strategies, public-private R&D partnerships, and sustainable certification programs that support broader market penetration of lignin-derived resin systems.

North America held a market share of 24.5% in 2024, driven primarily by rising investments in sustainable construction and automotive manufacturing. The United States leads regional adoption with strong backing from green building standards such as LEED and corporate carbon-reduction commitments. Canadian manufacturers are also exploring lignin resins in composite materials, particularly in the forestry and packaging sectors. Regulatory shifts, including restrictions on formaldehyde emissions in wood adhesives, have further increased reliance on lignin-derived alternatives. Technological advancements in lignin extraction and resin formulation are supporting scalability, while digital modeling tools enhance formulation performance. Public and private R&D investments across the U.S. and Canada are expanding application feasibility for lignin resins in high-performance structural and packaging materials.

Europe commanded the highest market share at 36.2% in 2024, with Germany, France, and the UK leading the regional expansion. Government-led initiatives to phase out fossil-based chemicals and stringent REACH regulations have propelled the shift toward lignin-based alternatives. The European Green Deal and associated funding for bioeconomy projects have been instrumental in accelerating commercial adoption. Germany’s automotive and construction sectors are integrating lignin resins in lightweight panels and adhesives, while France and the Nordics are using them in compostable packaging materials. Emerging technologies in lignin valorization and resin customization are creating a competitive edge for European manufacturers, making the region a hub for circular materials innovation.

Asia-Pacific ranked as the fastest-growing market in 2024, with market volume expansion led by China, India, and Japan. China’s aggressive push toward sustainable manufacturing and its large-scale infrastructure projects are significantly driving demand for bio-based resins. India is emerging as a promising market due to rising environmental awareness, public initiatives promoting green buildings, and rapid industrialization. Japan is focusing on advanced packaging and electronics applications, leveraging lignin for barrier coatings and composite substrates. Regional innovation clusters in South Korea and Singapore are fostering lignin-derived technology applications. Increasing investments in green chemistry and partnerships between universities and resin producers are also helping scale up next-gen lignin resin solutions across Asia-Pacific.

In South America, Brazil and Argentina are the key countries driving lignin-based resin adoption, accounting for a combined 8.4% of regional share in 2024. Brazil’s expansive forestry sector and pulp & paper industry provide abundant lignin supply, which is being redirected toward resin manufacturing for construction and furniture. Argentina is focusing on agricultural waste valorization, promoting lignin use in molded products and adhesives. Government-backed bioeconomy policies, along with trade incentives for eco-friendly exports, are encouraging adoption. The region is also witnessing a growing presence of biorefinery projects and small-to-midscale lignin resin producers targeting local construction and consumer goods markets.

The Middle East & Africa region shows growing traction, led by the UAE and South Africa, with a regional share of 5.2% in 2024. Demand is rising across construction, oil & gas, and packaging industries, where sustainability goals are aligning with national development agendas. South Africa’s forestry industry and eco-packaging trends are enabling lignin resin adoption, especially in panel boards and food packaging. The UAE is integrating lignin-based materials into smart city projects and green building frameworks. Regional governments are increasingly supporting circular economy frameworks and public-private partnerships aimed at reducing dependence on synthetic polymers. Digital transformation and modernization of production technologies are improving resin efficiency and formulation control.

Germany – 18.5% Market Share

Germany dominates due to its advanced biochemicals sector and high demand from automotive and construction industries embracing sustainable alternatives.

China – 16.8% Market Share

China leads in lignin supply from paper industries and aggressively adopts green materials across infrastructure and electronics manufacturing.

The Lignin Based Resins Market features a moderately fragmented competitive landscape with over 45 active participants operating across global and regional levels. These players include well-established chemical manufacturers, biotechnology firms, and emerging startups focused on bio-based material innovations. The competitive dynamics are shaped by product differentiation, integration across the lignin value chain, and application-specific customization capabilities. Market leaders are increasingly investing in green chemistry platforms, proprietary lignin extraction technologies, and downstream resin formulation techniques to enhance performance and reduce environmental footprint.

Strategic initiatives such as joint ventures, partnerships, and licensing agreements are common, particularly between lignin producers and end-use manufacturers in automotive, construction, and packaging. Companies are also expanding production capacity by establishing dedicated biorefinery units and investing in pilot-scale plants for lignin valorization. Innovation trends revolve around developing formaldehyde-free adhesives, recyclable thermoplastics, and reactive lignin-based epoxy alternatives. Many players are aligning their strategies with sustainability goals, eco-label certifications, and circular material standards, further intensifying competition and market consolidation in high-demand segments.

Domtar Corporation

Stora Enso

Borregaard ASA

Nippon Paper Industries Co., Ltd.

The Dallas Group of America, Inc.

Domsjö Fabriker AB

GreenValue Enterprises LLC

West Fraser Timber Co. Ltd.

Suzano S.A.

Aditya Birla Group

The Lignin Based Resins Market is experiencing a technological transformation driven by advancements in lignin extraction, purification, and polymerization techniques. Kraft lignin, organosolv lignin, and soda lignin are the most commonly used types, each offering unique structural and reactive properties that influence final resin performance. Recent developments focus on modifying lignin’s hydroxyl functionality through chemical grafting, oxidative depolymerization, and cross-linking, enabling enhanced compatibility with thermosetting and thermoplastic matrices.

Technologies such as enzymatic functionalization and solvent-free processing are gaining traction, reducing energy consumption and improving environmental performance. In adhesives, lignin is replacing phenol in phenol-formaldehyde systems, while in composites, lignin-derived polyols are being utilized to produce bio-based polyurethanes. Companies are also incorporating AI and machine learning models for molecular design, optimizing formulations for strength, thermal stability, and biodegradability.

The use of continuous flow reactors in lignin processing enables scalability and precision control, making commercial production more viable. Additionally, 3D printing filaments and coating materials containing lignin resins are being developed for niche applications in packaging and consumer electronics. These innovations are positioning lignin resins as a competitive alternative to synthetic resins, accelerating their integration into circular economy strategies across multiple industries.

• In February 2024, Stora Enso expanded its Sunila Biorefinery in Finland, doubling kraft lignin production capacity to 100,000 tons annually to support demand from bio-based adhesives and thermoplastics.

• In December 2023, Domtar Corporation launched a new line of lignin-based binders for wood composite panels, offering a 30% reduction in formaldehyde emissions compared to conventional resins.

• In May 2024, Borregaard ASA announced a collaboration with a leading German automotive OEM to supply modified lignin resins for use in lightweight vehicle interiors, focusing on improved thermal performance and biodegradability.

• In August 2023, Nippon Paper Industries commissioned a pilot plant to produce lignin-based dispersants and resin intermediates, aimed at sustainable coating applications in the electronics and packaging industries.

The Lignin Based Resins Market Report offers a comprehensive analysis of the global industry landscape, focusing on the development, commercialization, and application of lignin-derived resin systems. The report segments the market by product type (kraft lignin, soda lignin, organosolv lignin), application (adhesives, composites, coatings, thermoplastics), and end-use industries (construction, automotive, packaging, electronics, and agriculture). It covers five key regional markets—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with country-level breakdowns for major markets such as Germany, China, the United States, and Brazil.

In terms of technological scope, the report examines innovations in lignin extraction, resin formulation techniques, and performance-enhancing modifications, as well as the integration of lignin resins into existing industrial supply chains. It also highlights emerging use cases, such as lignin in 3D printing filaments, biodegradable packaging, and green building materials. Special attention is given to sustainability metrics, regulatory influences, and bioeconomy frameworks driving adoption. The report is tailored for stakeholders seeking strategic insights into investment opportunities, competitive dynamics, and innovation trends shaping the future of lignin-based resins in both mature and emerging markets.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 5,120.5 Million |

| Market Revenue (2032) | USD 7,757.6 Million |

| CAGR (2025–2032) | 5.33% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Domtar Corporation, Stora Enso, Borregaard ASA, Nippon Paper Industries Co., Ltd., The Dallas Group of America, Inc., Domsjö Fabriker AB, GreenValue Enterprises LLC, West Fraser Timber Co. Ltd., Suzano S.A., Aditya Birla Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |