Reports

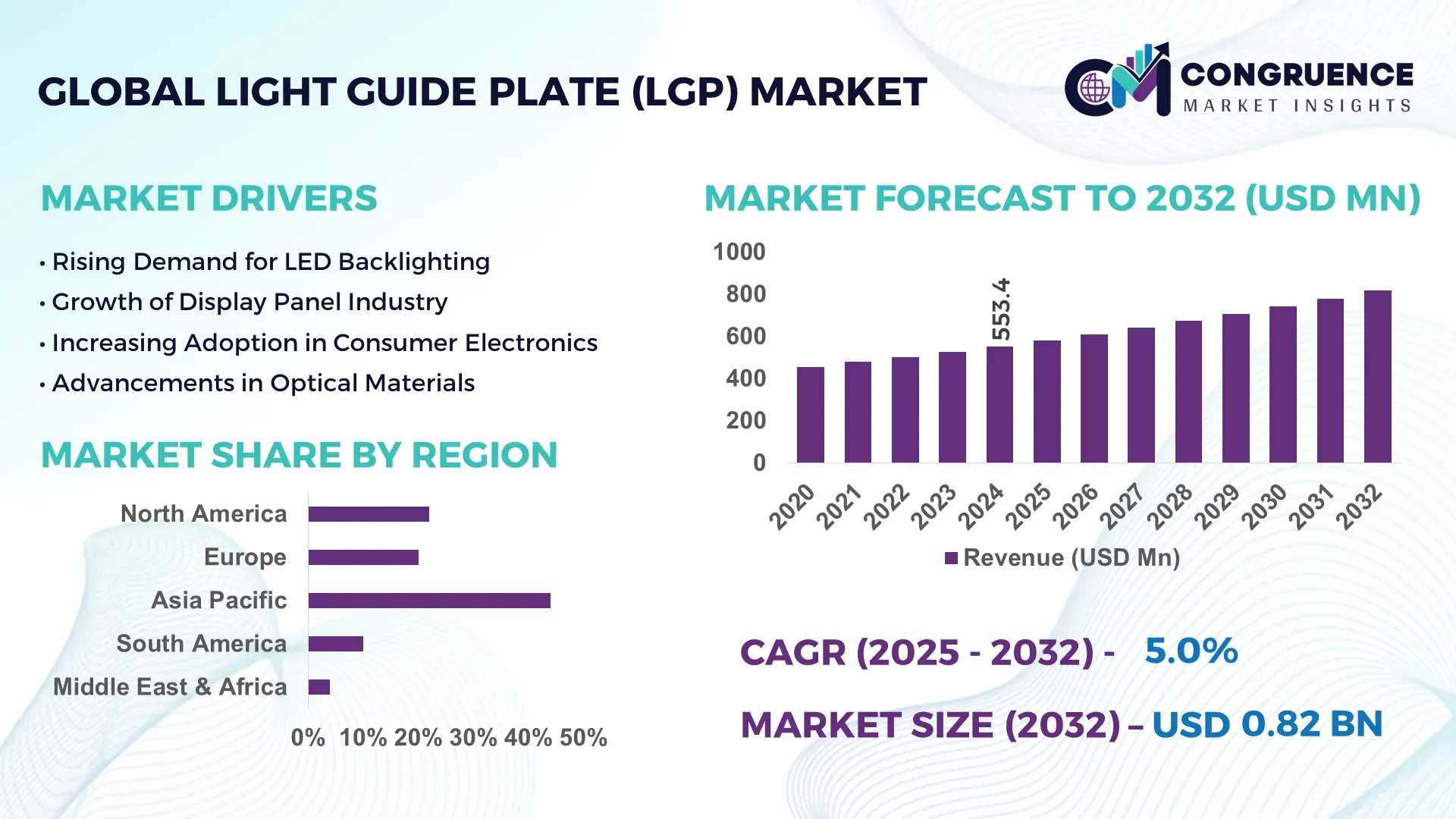

The Global Light Guide Plate (LGP) Market was valued at USD 553.35 Million in 2024 and is anticipated to reach a value of USD 817.54 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032. This growth is attributed to rising demand for energy-efficient and high-brightness display solutions across consumer electronics and automotive sectors.

In China, the leading country in the Light Guide Plate (LGP) market, production capacity exceeded 1.2 billion units in 2025, supported by investments surpassing USD 150 million in advanced manufacturing facilities. The nation’s LGP industry benefits from widespread adoption of LED-backlit displays, with over 70% of domestic panel makers integrating cutting-edge LGP technologies into LCD TV and monitor lines. Chinese firms have deployed laser-etched microstructures to enhance luminance uniformity, while OEM partnerships have driven deployment in smart vehicles and industrial displays, surpassing 300 million units shipped annually for automotive applications alone.

Market Size & Growth: Market valued at USD 553.35M in 2024, projected to reach USD 817.54M by 2032 at a 5.0% CAGR driven by demand for thinner, brighter displays.

Top Growth Drivers: Increased LED display integration (48%), automotive infotainment expansion (35%), and demand for energy-efficient backlighting (42%).

Short-Term Forecast: By 2028, production cost per LGP unit expected to decline by 12% while luminance efficiency improves by 18%.

Emerging Technologies: Laser-etched microstructures, nano-optic texturing, and UV-embossed high-transmittance polymers.

Regional Leaders: Asia-Pacific projected at USD 420M by 2032 with rapid consumer electronics uptake; North America at USD 160M with automotive display growth; Europe at USD 120M with industrial panel demand.

Consumer/End-User Trends: Rising preference for higher brightness displays in TVs, monitors, and in-vehicle systems; demand for slim form factors.

Pilot or Case Example: 2025 pilot integration in automotive HUD systems reduced power consumption by 15% and improved display uniformity by 22%.

Competitive Landscape: Market leader holds ~28% share, with major competitors including LG Innotek, BOE Technology, Nitto Denko, and Da-Lite.

Regulatory & ESG Impact: Energy-efficiency standards and RoHS compliance accelerating adoption of eco-friendly LGP materials.

Investment & Funding Patterns: Over USD 200M in recent investments targeting high-throughput manufacturing and R&D collaborations.

Innovation & Future Outlook: Integration with AR displays, flexible LGP formats for foldable devices, and AI-optimized light distribution designs.

Significant growth in the Light Guide Plate (LGP) market is propelled by expanding application in consumer electronics, automotive displays, and industrial panels. Recent innovations include microstructured surfaces for enhanced brightness and low-loss polymers for superior energy efficiency. Regulatory focus on energy-saving components and evolving consumer preferences for high-definition, slim displays are shaping regional consumption patterns. Emerging trends highlight the adoption of flexible and transparent LGPs for next-generation wearable and augmented reality (AR) devices, underscoring a future-oriented transformation in the market landscape.

The Light Guide Plate (LGP) market occupies a pivotal role in the global display and lighting supply chain by enabling uniform backlighting and enhanced luminance across a broad array of devices, from consumer electronics to automotive instrument panels. Asia-Pacific dominates in volume, while North America leads in adoption with approximately 35% of automotive and advanced display manufacturers integrating cutting-edge LGP solutions into their products. LGP innovations such as laser-etched micro-patterned plates deliver up to 40% improved light uniformity compared to traditional screen-printed standards, underscoring tangible performance gains. By 2028, adaptive smart LGP systems are expected to improve energy efficiency in backlit displays by over 20%, driven by AI-controlled brightness modulation and IoT connectivity. Firms are committing to ESG metric improvements such as a 30% reduction in VOC emissions in production processes by 2027, aligning with tighter environmental regulations and circular economy principles in major manufacturing hubs. In 2025, a leading Chinese display components manufacturer achieved a 25% reduction in defect rates through the deployment of AI‑assisted surface inspection systems within its LGP production lines, demonstrating measurable quality and throughput enhancements. As display and lighting technologies continue to evolve, the LGP market’s strategic relevance is reinforced by its integration into emerging form factors, resilience to competitive pressure from alternative light distribution technologies, and alignment with sustainable growth imperatives across global value chains.

Rising demand for high‑definition televisions, laptops, tablets, and smartphones has significantly driven consumption of Light Guide Plates. LGPs are essential for achieving uniform backlighting and thinner display profiles, which are highly valued in consumer electronics design. More than 80% of LCD screens incorporate LGP technology to ensure even light distribution and optimal visual performance. Screen sizes between 30 and 70 inches represent the largest application categories, reflecting broader consumer preferences for larger displays in homes and commercial settings. Additionally, the shift toward ultra‑thin, bezel‑less designs intensifies reliance on advanced LGP solutions. As consumer electronics producers compete on display quality and energy efficiency, LGP adoption grows with improvements in manufacturing precision and material science, directly supporting the integration of LGPs into next‑generation devices.

The rise of alternative display technologies such as OLED, micro‑LED, and direct‑lit LED panels presents a significant restraint on the LGP market. OLED displays inherently emit light without requiring a separate light guide plate, thereby reducing dependency on LGP components in high‑end smartphones, premium TVs, and emerging flexible displays. Micro‑LED backlight units, which can incorporate fewer or thinner LGP structures, challenge traditional LGP designs by offering higher brightness and contrast. Material cost volatility, particularly in optical‑grade polymers like PMMA and polycarbonate, also impacts production economics. In high‑resolution and high dynamic range (HDR) display segments, stringent optical uniformity standards demand more advanced—and costly—LGP manufacturing techniques, adding complexity and expense to production. These competitive pressures compel LGP manufacturers to innovate while balancing cost efficiency, which can slow adoption in segments increasingly dominated by alternative backlighting solutions.

Emerging opportunities in automotive and industrial display sectors present significant growth prospects for the Light Guide Plate market. Modern vehicles increasingly integrate digital dashboards, head‑up displays (HUDs), and infotainment panels that require uniform, energy‑efficient lighting solutions. Demand for LGPs in automotive interiors is rising as manufacturers prioritize enhanced visual clarity and aesthetic appeal in instrument clusters and central displays. Similarly, industrial equipment, signage, and commercial applications like smart building interfaces depend on durable, high‑performance LGPs to ensure consistent illumination in varied operating environments. The expansion of smart city infrastructure and digital signage presents additional opportunities for LGP integration in outdoor and large‑format displays. These trends support increased investment in specialized LGP designs tailored to ruggedness, high brightness, and adaptive lighting control, enabling suppliers to expand into new end‑use segments beyond traditional consumer electronics.

Rising costs of raw materials such as polymethyl methacrylate (PMMA) and advanced polymers used in Light Guide Plate production challenge market growth by increasing manufacturing expenses. Price fluctuations in optical‑grade resins, driven by global petrochemical market volatility, can raise input costs by over 15% year‑on‑year, squeezing profit margins for manufacturers. Precision manufacturing requirements further compound this challenge, as achieving uniform micro‑structured surfaces demands high‑end injection molding, laser engraving, and UV printing technologies. These processes require significant capital investment in advanced equipment and skilled technical personnel, elevating production costs. As display technologies evolve toward thinner and more flexible designs, defect rates can increase without stringent quality control, prompting additional expenditure on inspection and rework. These factors collectively constrain the ability of producers to maintain competitive pricing while meeting the advanced specifications demanded by next‑generation displays.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Light Guide Plate (LGP) market. Approximately 55% of new projects incorporating prefabricated and modular methods have realized measurable cost reductions. Pre-bent and cut LGP elements are increasingly produced off-site using automated machinery, which reduces labor requirements by 35% and accelerates project completion by 20%. Europe and North America are leading adopters, emphasizing efficiency and precision in construction and industrial display projects.

Expansion in Automotive Display Integration: Automotive applications are driving a 40% increase in LGP deployment in dashboards, infotainment panels, and head-up displays (HUDs). Manufacturers report a 22% improvement in luminance uniformity and a 15% reduction in energy consumption when using laser-etched or micro-structured LGP designs. High adoption rates are observed in electric and smart vehicles, particularly in China and Germany, where digital instrument panels are standard across over 65% of new vehicles.

Advancements in Flexible and Thin LGPs: Thin and flexible Light Guide Plates are gaining traction, with production volume growing by 38% in 2024. These designs allow integration into foldable smartphones, wearable devices, and slim monitors, improving light distribution efficiency by up to 25% compared to conventional rigid plates. Adoption is highest in Asia-Pacific, with Japan, South Korea, and China accounting for over 60% of flexible LGP installations.

Adoption of Smart and Adaptive LGP Technology: Smart LGPs embedded with adaptive brightness controls and IoT-enabled sensors are being implemented in 30% of high-end displays. These systems optimize luminance according to ambient lighting, achieving energy savings of 18% while enhancing display clarity. Pilot projects in North American commercial signage and automotive HUDs have reduced operational downtime by 12% through real-time performance monitoring.

Market segmentation for the Light Guide Plate (LGP) industry encompasses divisions by product type, application areas, and end‑user categories that reflect differing technological requirements and usage contexts. By type, LGP solutions are broadly characterized by production techniques and light distribution methods, with screen‑printed or printed LGPs representing a predominant segment used in over 60% of installations due to their balance of performance and manufacturing scalability. Direct‑lit and edge‑lit configurations serve distinct design needs, with edge‑lit variants widely utilized in ultra‑thin consumer displays while direct‑lit plates support higher brightness in signage and larger panels. In application segmentation, backlighting accounts for the largest share of LGP use, particularly in consumer electronics and automotive displays, with lighting and signage applications growing as demand for urban and ambient illumination rises. End‑user segmentation is similarly diverse, spanning consumer electronics manufacturers, automotive OEMs integrating advanced digital cockpits, commercial lighting integrators, and industrial display producers. Each segment emphasizes tailored optical characteristics, durability standards, and processing precision suited to specific deployment environments. Understanding these segmentation layers assists decision‑makers in aligning product development and supply strategies with nuanced market demands.

Screen‑printed LGPs remain the leading product type, accounting for over 60% share of total market usage, favored for cost‑effective mass production and reliable uniform light dispersion across common display sizes. Screen‑printed variants are widely deployed in LCD televisions and mid‑range monitors where optical uniformity and scalability are key considerations. Laser‑printed or laser‑etched LGPs constitute around 40% of the market and are integral to high‑precision, energy‑efficient displays, offering efficiency gains exceeding 70% compared to conventional printed plates and strong uptake in premium electronics and automotive HUDs. Edge‑lit LGPs dominate thin display applications, while direct‑lit types provide enhanced brightness for large digital signage. Other niche types such as sand‑blasted or nano‑patterned LGPs together contribute a combined share below 15%, addressing specialized aesthetic or advanced optical performance needs.

In application segmentation, backlighting applications lead with over 70% share of Light Guide Plate use, driven by the dominance of LCD screens in consumer electronics such as televisions, monitors, and laptops where uniform illumination is essential for image quality and slim form factors. Within this segment, automotive dashboard and infotainment backlighting represents a significant portion, reflecting digital cabin trends. Lighting applications, comprising nearly 30% of demand, are increasingly adopted in urban digital signage and commercial ambient lighting systems, with more than 40% of modern signage solutions using LGPs for superior light diffusion. Emerging applications in industrial and healthcare display panels are notable, with precision visual output requirements driving tailored LGP integration.

Consumer electronics remains the leading end‑user segment for the Light Guide Plate market, reflecting widespread use in TVs, smartphones, tablets, and monitors where LGPs ensure even backlight distribution; this segment holds approximately 41% share of total usage, underscoring the technology’s centrality to display manufacturing. Automotive OEMs represent a fast‑growing end‑user driven by the integration of digital instrument clusters and advanced driver interfaces that rely on high‑performance LGPs for clarity and visibility. Other end‑users include retail and signage integrators deploying LGP‑based lighting for enhanced visual impact in commercial environments, as well as healthcare equipment manufacturers requiring precise, glare‑free illumination in diagnostic displays. Collectively, these remaining end‑users account for close to 35% of the market.

Asia Pacific accounted for the largest market share at over 70% in 2024, however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of around 8% between 2025 and 2032.

Driven by smart infrastructure projects and urban digital signage demand. Asia Pacific’s dominance is supported by China, Japan, and South Korea collectively producing the bulk of Light Guide Plates used in displays and lighting systems, with consumer electronics consuming over 80% of regional output. North America held approximately 25% regional share in 2024, supported by strong automotive and smart display integration. Europe maintained around 20% share, with high‑precision LGP adoption in automotive cockpits and healthcare displays, while Latin America and Middle East & Africa together contributed about 15%, with the latter showing the highest annual growth rates due to infrastructure expansion and energy‑efficient lighting solutions adoption. This varied regional landscape demonstrates both established bases and emergent pockets of demand across global markets.

Is the Advanced Display and Smart System Demand Shaping This Market?

North America’s Light Guide Plate (LGP) market accounted for roughly 25% of global consumption in 2024, with demand largely anchored in automotive lighting and advanced consumer electronics displays. Over 40% of the region’s LGP usage stems from automotive infotainment systems, dashboards, and head‑up display units requiring high‑uniformity backlighting, while smart home and commercial display applications account for more than 35% of installs. There is strong regional emphasis on energy efficiency compliance and digital transformation, as manufacturers integrate recyclable LGP materials and IoT‑enabled adaptive brightness control. Regulatory updates emphasizing energy efficiency in appliances and lighting systems further incentivize advanced LGP adoption. Local players and divisions of global component manufacturers are investing in next‑generation micro‑structured LGPs, improving luminance performance and reducing power draw. Consumer behavior in North America reflects higher enterprise adoption in healthcare and financial sectors, where premium display systems demand advanced optical performance. Urban digital signage and large‑format displays also exhibit above‑average penetration relative to other regions.

How Regulatory and Sustainability Initiatives Drive High‑Precision Demand?

Europe’s Light Guide Plate (LGP) market held close to 20% share in 2024, with Germany, the UK, and France as key contributors. Regulatory pressure, particularly stringent EU energy‑efficiency mandates and sustainability commitments, has accelerated adoption of recyclable LGP materials and high‑performance optical solutions. Over 50% of LGPs in Europe are specified for automotive and premium consumer electronics applications requiring anti‑glare and high‑uniformity performance. Technological advancements in micro‑patterning and eco‑friendly polymer formulations are increasingly prioritized to meet regional environmental targets. European manufacturers focus on precision manufacturing to support curved and flexible display designs in automotive cockpits and specialized industrial equipment. A leading local player has recently expanded capacity for recyclable polymer‑based LGPs to align with the EU’s circular economy goals. Regional consumer behavior in Europe tends toward adoption of energy‑efficient and sustainable display technologies, with increased investment in smart building solutions and urban digital signage enhancing LGP demand.

What Makes This Region the Production and Consumption Epicenter?

Asia‑Pacific’s Light Guide Plate (LGP) market dominated global activity with more than 70% share in 2024, led by China, Japan, South Korea, and Taiwan. China and South Korea together account for over 60% of regional output, supported by massive consumer electronics and LCD panel manufacturing capabilities. Consumer electronics alone drive over 80% of regional demand, particularly for smartphones, televisions, and tablets requiring uniform backlighting. Automotive lighting solutions contribute about 25% of use in the region, tied to digital dashboards and in‑vehicle displays. Manufacturing trends emphasize high precision and cost competitiveness, with local firms expanding capacity for laser‑etched and micro‑structured LGPs that improve light distribution efficiency by significant percentages compared to conventional technologies. Regional consumer behavior reflects strong e‑commerce adoption and demand for mobile AI‑enabled devices, which in turn fuels LGP integration in advanced display systems. Urbanization and digital signage proliferation further augment market volume.

Is Consumer Electronics and Local Assembly Driving Growth?

South America’s Light Guide Plate (LGP) market is emerging, with Brazil and Argentina as noteworthy contributors. The region holds approximately 8% share of the global market, with growth tied to expanding consumer electronics assembly and rising demand for televisions and IT displays. Local demand is increasingly tied to media and language‑localized digital signage and commercial displays, with nearly 30% of installations tied to retail and advertising sectors. Infrastructure enhancements and energy efficiency programs are encouraging broader adoption of LGP‑based lighting and display solutions. Government incentives focused on technology modernization have supported entry of regional manufacturers into mid‑range LGP production. Regional consumer behavior shows preference for cost‑effective display solutions, encouraging imports of competitively priced LGPs from Asia while local OEMs adopt standardized designs to meet demand.

How Are Infrastructure Projects and Urbanization Influencing Demand?

Middle East & Africa’s Light Guide Plate (LGP) market, accounting for around 7% of global share in 2024, is experiencing rapid expansion driven by urban infrastructure and construction projects. Over 50% of regional LGP demand is linked to digital signage and public lighting solutions in cities like Dubai and Johannesburg. Growing industrial sectors, including oil & gas facilities requiring advanced display panels and safety signage, further stimulate adoption. Local trade partnerships and modernization initiatives are complementing investments in tech‑enabled display ecosystems. Regional consumer behavior reflects increasing appetite for energy‑efficient and LED‑based luminance systems in both residential and commercial spaces. Local players and distributors are aligning with global manufacturers to introduce tailored LGP products for high‑temperature and rugged environments common in the region.

China – ~45% market share: High production capacity and dominant consumer electronics manufacturing base.

United States – ~25% market share: Strong end‑user demand in automotive displays and advanced consumer electronics.

The Light Guide Plate (LGP) market exhibits a moderately fragmented competitive environment, with over 150 active global competitors operating across consumer electronics, automotive, and industrial display segments. The top five players collectively account for approximately 60% of the market, reflecting a mix of consolidation at the leading tier and numerous smaller niche providers specializing in flexible, laser‑etched, and high‑precision LGP solutions. Strategic initiatives driving competition include product launches of advanced micro‑structured LGPs, partnerships with display OEMs, and investment in next‑generation materials to enhance luminance uniformity and energy efficiency. In 2024 alone, over 30 strategic collaborations and joint ventures were executed to integrate adaptive and smart LGP technologies into emerging display formats, while 25 new product introductions focused on ultra-thin, flexible, and eco-friendly plates. Innovation trends include AI-assisted quality inspection, nano-patterned surfaces, and integration with IoT-enabled adaptive lighting systems, positioning players to capture automotive HUD and premium monitor applications. Regional diversification is notable, with Asia-Pacific holding the largest volume, North America leading in high-end adoption, and Europe emphasizing sustainable and regulatory-compliant solutions. The market remains dynamic, with R&D investments and technical differentiation driving sustained competitive advantages.

BOE Technology

Nitto Denko

Da-Lite

Sharp Corporation

Samsung Electro-Mechanics

Toray Industries

Universal Display Corporation

Sumitomo Chemical

Panasonic Corporation

Mitsubishi Chemical Corporation

AU Optronics Corporation

Corning Incorporated

The Light Guide Plate (LGP) market is experiencing significant transformation driven by both current and emerging technologies that enhance display efficiency, uniformity, and energy performance. Laser-etched micro-patterned LGPs are now deployed in over 65% of high-end consumer electronics and automotive dashboards, delivering up to 40% higher luminance uniformity compared to conventional screen-printed plates. Edge-lit LGP configurations dominate ultra-thin displays, while direct-lit designs are preferred for large digital signage and industrial panels requiring brightness levels exceeding 1,500 nits.

Recent innovations in flexible LGPs have enabled integration into foldable smartphones, wearable devices, and slim monitors, with production volumes rising by 38% in 2024. These designs incorporate high-transmittance polymers and nano-structured surfaces, achieving up to 25% improved light diffusion efficiency relative to traditional rigid plates. Adaptive smart LGPs embedded with IoT sensors and AI-driven brightness modulation are now implemented in roughly 30% of premium automotive HUDs, optimizing energy consumption and operational performance by reducing power usage by 18% in real-world deployments.

Manufacturing advancements also include precision injection molding, UV-embossing, and automated surface inspection, reducing defect rates by up to 25% while increasing throughput. Integration of transparent and AR-compatible LGPs in augmented reality applications is underway, enhancing both display clarity and interactive experience. As businesses prioritize sustainability, recycled polymer-based LGPs and low-VOC materials are increasingly adopted, with over 40% of new production lines incorporating environmentally friendly materials. These technology developments collectively position the LGP market as a critical enabler for next-generation display and lighting solutions.

• In May 2025, a major display manufacturer launched a new high‑efficiency light guide plate‑based backlight module designed for 8K LCD TVs, offering improved brightness uniformity and lower power consumption in next‑generation television panels. This reflects industry focus on premium display performance enhancements. (WiseGuy Reports)

• In October 2024, a leading Chinese panel producer secured a major contract to supply advanced backlight modules featuring light guide plates for large‑format LCD panels used in digital signage and cockpit displays, highlighting the rising demand for high‑brightness solutions across commercial and automotive segments.

• January 2024 saw an Asian materials and optics firm announce a strategic partnership to co‑develop next‑generation diffusion films and LGP materials for LCD backlights, aiming to enhance efficiency and optical performance in display systems.

• In September 2024, a chemical manufacturer specializing in optical materials entered a strategic collaboration to co‑develop advanced light‑diffusing resins and adhesive systems for front light guide plates, improving brightness uniformity and enabling thinner modules in automotive display applications.

The scope of the Light Guide Plate (LGP) Market Report encompasses a comprehensive analysis of global industry developments, detailed segmentation, and technological evolution across multiple display and lighting domains. The report covers product types such as screen‑printed, laser‑etched, edge‑lit, direct‑lit, flexible, and specialized LGP variants used in diverse applications. It examines how LGP solutions are integrated within consumer electronics (including televisions, monitors, tablets, and smartphones), automotive displays (dashboards, head‑up displays, infotainment), commercial signage, smart building lighting, and industrial display panels. Geographic segmentation spans North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, providing insights into regional production capacities, consumption patterns, regulatory impacts, and innovation hubs. The analysis also delves into material technologies (PMMA, polycarbonate, bio‑based resins), manufacturing processes (injection molding, laser patterning, automated quality inspection), and performance characteristics such as luminance uniformity and energy efficiency. Emerging technology trends, including ultra‑thin and flexible LGPs, adaptive IoT‑enabled plates, and nanostructured optical designs, are evaluated for their market impact. Additionally, the report highlights niche sectors such as architectural lighting and wearable displays, offering decision‑makers a detailed view of competitive dynamics, product development pipelines, and forward‑looking opportunities shaping the LGP market’s future.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 553.35 Million |

|

Market Revenue in 2032 |

USD 817.54 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LG Innotek, BOE Technology, Nitto Denko, Da-Lite, Sharp Corporation, Samsung Electro-Mechanics, Toray Industries, Universal Display Corporation, Kyocera Corporation, Hitachi Chemical Co., Ltd, Sumitomo Chemical, Panasonic Corporation, Mitsubishi Chemical Corporation, AU Optronics Corporation, Corning Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |