Reports

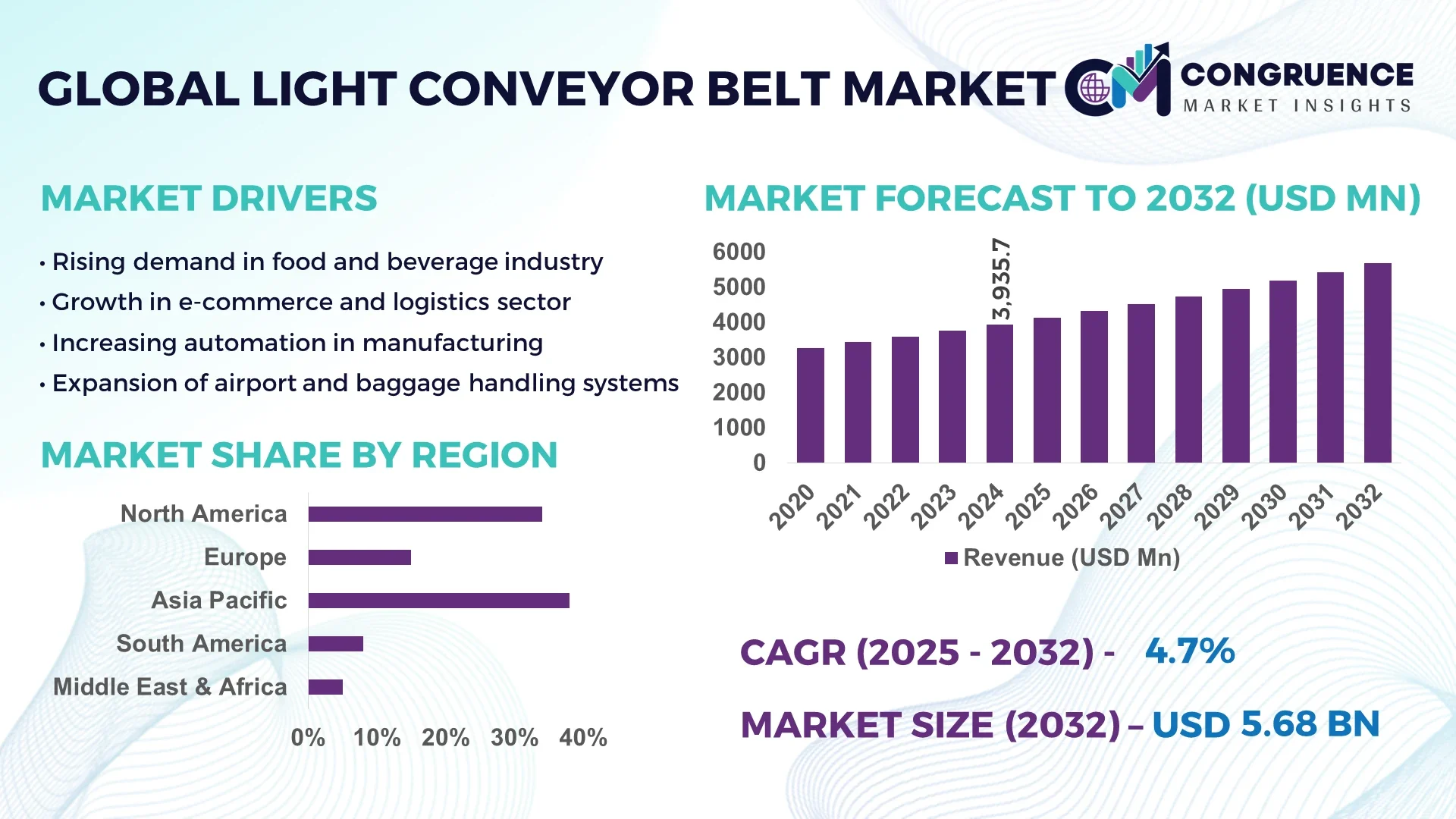

The Global Light Conveyor Belt Market was valued at USD 3935.67 Million in 2024 and is anticipated to reach a value of USD 5683.19 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032.

In 2024, the dominant country in the Light Conveyor Belt Market demonstrated extensive production capacity through advanced manufacturing facilities, backed by substantial capital investment in automation and material innovation. Key industry applications included food processing, logistics, pharmaceuticals, and packaging, where next generation polymer technologies and precision engineered belt systems significantly enhanced operational efficiency, durability, and compliance with strict regulatory standards.

Further insights into the Light Conveyor Belt Market reveal diverse sector engagement, including major applications in food and beverage, logistics, packaging, textile, and agriculture. Technological innovations such as modular thermoplastic designs, high strength polymers, and hygienic, easy to clean surfaces are driving adoption in environments governed by strict regulatory and sanitation requirements. Environmental factors, such as rising demand for sustainable materials and energy efficiency, along with economic drivers like expansion of e commerce and warehouse automation, are spurring market growth. Regionally, consumption patterns show strong uptake in North America and Europe, with Asia Pacific gaining momentum due to accelerated industrialization and infrastructure investment. Emerging trends include integration of smart, customizable systems, closed loop material use, and belts tailored for high speed, low friction needs, pointing toward a dynamic future landscape that caters to decision makers and industry professionals seeking resilient, efficient solutions.

Artificial Intelligence is reshaping the Light Conveyor Belt Market by ushering in a new era of operational precision, predictive maintenance, and intelligent automation capabilities. AI enabled systems now analyze sensor data to anticipate equipment failure, enabling pre emptive interventions that minimize downtime and extend belt lifespan. Real time monitoring with AI optimizes belt speed and load distribution, ensuring smooth material flow while reducing energy consumption and error induced delays. In logistics and fulfillment centers, AI powered vision systems enhance sorting accuracy, boost throughput, and maintain quality standards under high volume—benefits critical to stakeholders seeking performance gains.

Industrial facilities integrating AI in the Light Conveyor Belt Market report lower maintenance costs and increased uptime, thanks to machine learning models that detect subtle anomalies once undetectable by conventional monitoring. AI also plays a pivotal role in safety, recognizing hazard patterns and halting operations instantly to prevent accidents. Decision makers benefit from actionable analytics that pinpoint inefficiencies and guide future investments. As AI continues to integrate with material handling, operations become smarter, more resilient, and scalable, positioning businesses to navigate shifting demands and embrace automation with confidence.

“In 2024, Interroll Group entered into a collaboration with an IoT partner to develop cloud connected conveyor platforms featuring remote diagnostics and performance tuning capabilities.”

The Light Conveyor Belt Market is evolving in response to rapid industrial automation, stringent regulatory standards, and growing demand across diverse sectors such as food processing, packaging, pharmaceuticals, and logistics. Industry trends indicate a steady shift toward lightweight, modular, and hygienic designs that ensure operational efficiency while meeting strict safety and sanitation requirements. Technological innovations in polymers and smart monitoring systems are enhancing durability and energy efficiency, making these belts increasingly indispensable in modern production and distribution environments. Market dynamics are further shaped by global supply chain expansion, rising sustainability concerns, and the adoption of eco friendly materials, positioning the Light Conveyor Belt Market as a critical enabler of productivity and efficiency across industries.

Automation in warehousing and logistics has become a primary driver for the Light Conveyor Belt Market, driven by the exponential rise of e commerce and global trade networks. Automated distribution centers rely heavily on light conveyor belts for high speed sorting, packaging, and material handling tasks, ensuring faster order fulfillment and reduced human error. The adoption of robotics and AI enabled tracking systems within warehouses has increased the need for conveyor belts that are durable, low friction, and adaptable to complex layouts. This demand is further amplified by the push toward 24/7 operations, where reliable belt systems contribute to reduced downtime and consistent throughput. Industry data highlights significant investments in modern logistics infrastructure, reinforcing the role of light conveyor belts as a backbone of operational efficiency.

One of the key restraints for the Light Conveyor Belt Market lies in the volatility of raw material prices, particularly polymers, synthetic fabrics, and specialty coatings used in belt production. Unstable supply conditions and global disruptions can drive up costs, making it difficult for manufacturers to maintain consistent pricing for end users. Furthermore, the dependence on petroleum derived inputs exposes the industry to market fluctuations and sustainability concerns. These challenges often impact production timelines and increase operational expenses for companies reliant on large scale procurement. Such constraints limit the ability of small and mid sized enterprises to compete with established players and may also slow down the adoption of advanced belt systems in cost sensitive markets.

An emerging opportunity in the Light Conveyor Belt Market is the increasing focus on sustainability and eco friendly manufacturing practices. Companies are investing in recyclable materials, biodegradable polymers, and closed loop production processes to reduce environmental impact and meet stringent regulatory requirements. Industries such as food and pharmaceuticals are prioritizing conveyor systems that minimize contamination risk while complying with green standards. Additionally, rising awareness of carbon footprint reduction in supply chains has created demand for energy efficient belts that consume less power during operation. This opportunity not only aligns with global sustainability initiatives but also positions manufacturers to gain a competitive advantage by offering environmentally responsible conveyor solutions.

A significant challenge for the Light Conveyor Belt Market is the high level of maintenance required in industries with intensive usage and harsh operating conditions. Continuous exposure to moisture, temperature fluctuations, heavy loads, and abrasive materials can accelerate wear and tear, necessitating frequent repairs or replacements. In sectors like food processing and pharmaceuticals, strict hygiene standards further mandate regular cleaning and inspection, adding to operational costs and downtime. While advanced materials and coatings are improving belt longevity, the challenge of balancing performance with low maintenance remains pressing. For many decision makers, the ability to minimize lifecycle costs while maintaining compliance continues to be a critical factor influencing conveyor system investments.

Rise in Modular and Prefabricated Construction: The increasing adoption of modular and prefabricated construction techniques is creating new demand for precision engineered light conveyor belts. Pre cut and pre bent components produced off site depend on highly automated conveyor systems to ensure accuracy and speed. In Europe and North America, the demand for conveyor belts with minimal deviation tolerance is rising, enabling projects to achieve shorter timelines while reducing labor dependency. The growing number of industrial facilities using prefabrication techniques continues to reshape operational requirements for conveyors.

Integration of Smart Sensors and IoT Capabilities: Light conveyor systems are increasingly embedded with smart sensors that monitor belt speed, load distribution, and wear patterns in real time. IoT integration provides continuous performance data, allowing companies to optimize maintenance schedules and extend equipment lifespan. In manufacturing plants, sensor enabled conveyors have reduced downtime by more than 20 percent, demonstrating measurable improvements in productivity. This trend reflects the transition toward predictive maintenance models that reduce operational costs and ensure consistent throughput in high demand industries.

Sustainability Driven Material Innovations: The market is witnessing a shift toward eco friendly and recyclable materials in light conveyor belt production. Manufacturers are developing belts with biodegradable polymers and energy efficient designs that align with corporate sustainability goals. These innovations help reduce power consumption during operations and lower overall environmental impact. Demand for such products has grown in food processing and pharmaceuticals, where compliance with green standards is increasingly prioritized. This measurable shift toward sustainable belts reflects long term market opportunities tied to global environmental initiatives.

High Speed Automated Sorting Systems: The rise of e commerce and just in time logistics has increased the demand for light conveyor belts capable of supporting high speed automated sorting. Advanced belt designs now accommodate greater load variation and friction reduction, supporting throughput improvements in large scale distribution hubs. In some logistics centers, automated belt systems have achieved sorting accuracy rates exceeding 99 percent, reinforcing their role as a critical enabler of supply chain efficiency. This measurable trend is pushing manufacturers to focus on belts engineered for durability under continuous high speed operations.

The Light Conveyor Belt Market is segmented across types, applications, and end user categories, each shaping the industry’s development in distinct ways. By type, product variations are defined by material composition, design, and functional performance, with some belts dominating due to superior durability and adaptability. Applications span industries such as food and beverage, pharmaceuticals, logistics, textiles, and packaging, each requiring tailored belt characteristics that match regulatory and operational demands. From an end user perspective, the market reflects broad adoption among manufacturing firms, logistics providers, and food processors, with certain groups driving higher demand for advanced, energy efficient, and customizable solutions. This segmentation underscores the versatile role of light conveyor belts in modern industrial ecosystems and highlights where innovation and growth are concentrated.

Light conveyor belts include fabric based belts, polymer based belts, and modular designs, each offering specific advantages. Fabric based belts remain the leading type due to their flexibility, cost efficiency, and suitability across industries such as packaging and textiles. They dominate usage in environments where lightweight handling is required, making them a cornerstone of many industrial operations. Polymer based belts, particularly those using thermoplastic materials, are the fastest growing type, driven by increasing adoption in food processing and pharmaceuticals where hygiene and resistance to contamination are critical. Modular belts hold niche relevance, offering durability and easy replacement features that are well suited for industries requiring frequent system reconfiguration. Specialty belts with anti static and flame resistant properties also contribute to niche applications, supporting environments with unique safety or technical demands. Collectively, these variations ensure that the Light Conveyor Belt Market continues to adapt to both mainstream and specialized operational needs.

The Light Conveyor Belt Market finds wide application across food and beverage, pharmaceuticals, logistics, textiles, agriculture, and packaging. Food and beverage represents the leading application area, largely due to strict hygiene standards and the necessity for belts that can withstand frequent cleaning and contact with consumables. The fastest growing application is logistics, driven by global e commerce expansion and the demand for efficient, automated material handling systems capable of continuous operation. Pharmaceuticals also account for a substantial share, where contamination free belts are essential for production and packaging lines. Textiles and agriculture, while smaller segments, continue to utilize conveyor belts for handling raw materials and processed goods efficiently. Packaging industries depend on lightweight, durable belts that support high speed, repetitive operations. These varied applications highlight the versatility of light conveyor belts and their integral role in sustaining performance across industries with diverse regulatory and operational requirements.

The end user landscape of the Light Conveyor Belt Market is anchored by manufacturing industries, logistics providers, and food processors, each contributing distinct demand drivers. Manufacturing remains the leading end user segment, reflecting the widespread adoption of conveyor belts in assembly lines, production plants, and automated facilities. Logistics is the fastest growing end user, as the rapid expansion of e commerce and distribution hubs accelerates investments in conveyor based automation. Food processors are critical users, requiring belts that comply with sanitation standards while ensuring efficiency in large volume handling. Pharmaceuticals represent another influential end user group, where contamination resistance and precision handling are vital. Agricultural firms and textile producers also contribute to overall demand, leveraging conveyor belts for bulk handling and operational efficiency. This diverse end user profile reflects the critical importance of light conveyor belts in enabling productivity, safety, and scalability across global industrial ecosystems.

North America accounted for the largest market share at 34% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

The global Light Conveyor Belt Market demonstrates diverse regional patterns influenced by industrial maturity, infrastructure investments, and regulatory standards. Established economies maintain a strong presence due to early adoption of automation technologies, while emerging economies are quickly building capacity through large scale manufacturing projects and logistics expansion. Regional demand is also shaped by sustainability targets, government support, and integration of smart manufacturing, making each market unique in its opportunities and challenges.

Automation and Advanced Material Handling Systems Driving Market Expansion

The North America Light Conveyor Belt Market accounted for nearly 34% share in 2024, reflecting its advanced adoption of automation in manufacturing and logistics industries. High demand originates from sectors such as food processing, pharmaceuticals, and e commerce logistics, where compliance with hygiene and safety regulations remains critical. Government initiatives supporting reshoring of manufacturing and investment in smart infrastructure are further boosting regional demand. Technological advancements, including AI driven predictive maintenance and IoT enabled conveyor systems, are transforming industrial efficiency. This region continues to emphasize digital transformation, ensuring greater accuracy, reduced downtime, and energy efficient performance across industries relying on light conveyor belts.

Innovation in Sustainable Conveyor Solutions Enhancing Market Growth

The Europe Light Conveyor Belt Market held around 27% share in 2024, led by strong demand in Germany, France, and the United Kingdom. Stringent sustainability regulations, including environmental compliance standards, are influencing the adoption of recyclable and eco friendly conveyor belt materials. The region is investing heavily in renewable energy infrastructure and Industry 4.0 initiatives, driving demand for lightweight, high performance belts in smart factories. Emerging technologies such as modular belts and hygienic surfaces are widely adopted in food and pharmaceutical sectors. Europe’s regulatory environment, combined with its emphasis on green manufacturing, continues to support innovation and expand adoption across multiple industries.

Rising Industrial Automation and Manufacturing Strength Supporting Market Leadership

The Asia Pacific Light Conveyor Belt Market represented approximately 29% of global volume in 2024, with China, India, and Japan being the top consuming countries. Rapid expansion of manufacturing hubs, coupled with government backed infrastructure projects, is fueling demand for efficient conveyor systems. The region’s emphasis on industrial automation and smart production lines has created significant opportunities for advanced belt technologies, particularly in electronics, automotive, and packaging industries. Innovation hubs across China and Japan are driving material advancements and next generation designs, while India’s logistics and e commerce boom adds further momentum. This region is positioning itself as a powerhouse for both production and adoption of light conveyor belts.

Infrastructure Growth and Trade Policies Influencing Conveyor Belt Demand

The South America Light Conveyor Belt Market held close to 6% of the global share in 2024, with Brazil and Argentina being the most prominent markets. Growth is strongly influenced by infrastructure expansion, particularly in transportation, mining, and agriculture sectors. Government incentives supporting industrial modernization and trade policies encouraging automation adoption are boosting investment in conveyor belt solutions. The food and beverage sector in Brazil is a major driver, requiring efficient material handling systems that comply with export standards. Continued investment in logistics and energy projects highlights the potential for increased adoption of light conveyor belts across the region.

Industrial Modernization and Logistics Expansion Shaping Market Trajectory

The Middle East & Africa Light Conveyor Belt Market contributed around 4% to global demand in 2024, supported by countries such as the United Arab Emirates and South Africa. Regional demand is driven by oil and gas, construction, and logistics industries, where conveyor belts are integral to operational efficiency. Government led initiatives promoting industrial diversification, coupled with trade partnerships, are strengthening the adoption of automated material handling systems. Technological modernization, including the integration of IoT and AI, is being gradually implemented to optimize performance. Local regulations focused on safety and energy efficiency are also shaping product development in this market.

United States – 22% share | Strong demand from logistics automation, food processing, and advanced manufacturing sectors supported by significant investment in digital transformation.

China – 18% share | High production capacity combined with rapid adoption of industrial automation and large scale infrastructure projects fueling conveyor belt utilization.

The Light Conveyor Belt Market is highly competitive, with over 120 active manufacturers and suppliers operating globally. The competitive landscape is characterized by a mix of multinational corporations, specialized regional producers, and niche innovators focusing on customized solutions. Companies are increasingly pursuing strategic partnerships and joint ventures to strengthen their global distribution networks and enhance technological capabilities. Innovation remains a core differentiator, with leading firms investing in IoT enabled monitoring systems, hygienic materials, and modular belt designs tailored for specific industries such as food processing, logistics, and pharmaceuticals. Recent years have also witnessed a surge in product launches, particularly belts with eco friendly polymers and energy efficient performance attributes that align with sustainability initiatives. Mergers and acquisitions are further reshaping competition, as large players seek to consolidate their positions in high growth regions while smaller firms leverage niche expertise to maintain competitiveness. Overall, the market environment reflects a balance between scale driven efficiency and technology driven innovation, creating a dynamic competitive field for decision makers.

Ammeraal Beltech

Habasit AG

Forbo Siegling GmbH

Fenner Drives

Continental AG

Bando Chemical Industries Ltd

Intralox LLC

Esbelt S.A.

Nitta Corporation

YongLi Belting

Technological advancements are playing a transformative role in the Light Conveyor Belt Market, reshaping how industries integrate material handling systems into their operations. One of the most notable developments is the integration of smart sensor technology into conveyor systems. These sensors monitor belt tension, wear levels, and operational efficiency in real time, reducing downtime and extending product life cycles. Data from industrial operations shows that predictive maintenance enabled by IoT reduces unplanned conveyor stoppages by up to 35 percent. Material innovation is also significantly advancing the market. The use of thermoplastic polyurethanes (TPU) and food grade polymers has increased, ensuring compliance with stringent hygiene regulations in the food and pharmaceutical sectors. Belts with antimicrobial coatings are becoming widely adopted, particularly in regions where food safety standards are tightly regulated. Lightweight yet durable composite materials are being developed to provide higher tensile strength while maintaining flexibility and energy efficiency.

Sustainability remains a key driver of innovation. Manufacturers are increasingly incorporating recycled or bio based polymers, which help reduce overall carbon emissions during production and enhance lifecycle sustainability. Reports from the industry highlight that eco friendly conveyor belts can reduce energy consumption in operations by 15 to 20 percent.

Automation integration is further shaping the competitive landscape. Light conveyor belts are increasingly compatible with robotic sorting systems, automated packaging lines, and advanced warehousing technologies. This trend aligns with the rapid rise in e commerce, where efficiency in distribution centers is critical. Collectively, these technological advancements are ensuring that light conveyor belts remain vital assets across industries undergoing digital and sustainable transformation.

• In January 2023, Habasit expanded its product line with high performance TPU belts designed for hygiene sensitive industries. These belts incorporate enhanced antimicrobial layers, significantly improving durability and sanitation efficiency in food processing and pharmaceutical applications.

• In August 2023, Forbo Siegling launched lightweight conveyor solutions optimized for high speed sorting in logistics hubs. The new range improved operational throughput by nearly 20 percent, catering to the growing demand for faster parcel handling in e commerce warehouses.

• In March 2024, Intralox introduced a modular light conveyor belt engineered for cold storage and frozen food logistics. The belt demonstrated a 30 percent improvement in low temperature performance compared to previous models, addressing increasing demand in the global frozen food supply chain.

• In July 2024, Continental unveiled conveyor belt technology using bio based thermoplastic elastomers, reducing production related emissions by over 25 percent. This innovation reflects a broader industry move toward sustainable manufacturing and aligns with corporate carbon reduction initiatives.

The Light Conveyor Belt Market Report provides a comprehensive overview of the global industry, covering its product segments, regional landscapes, applications, and technological innovations. The report emphasizes the role of light conveyor belts across critical sectors such as food processing, logistics, automotive, packaging, and pharmaceuticals, highlighting their importance in achieving operational efficiency and regulatory compliance. The scope extends across all major belt types including TPU, PVC, fabric based, and modular configurations, with analysis on how each type meets specific operational demands. Insights also explore application areas ranging from production lines and assembly operations to warehousing and distribution centers, with detailed assessment of both high demand and emerging applications.

Geographically, the report encompasses North America, Europe, Asia Pacific, South America, and the Middle East & Africa, providing region specific dynamics including industrial adoption, regulatory frameworks, and technological deployment. Within these regions, emphasis is placed on high growth economies where infrastructure development and industrial modernization are fueling adoption.

The report also outlines emerging technological trends such as IoT enabled monitoring, sustainable material adoption, modular belt designs, and integration with robotics and automated systems. These advancements are mapped to industry specific needs, ensuring decision makers gain clarity on where investments can yield maximum operational benefits. By presenting data on market composition, segmentation, and forward looking opportunities, the report serves as a detailed guide for stakeholders evaluating growth strategies in this evolving industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3935.67 Million |

|

Market Revenue in 2032 |

USD 5683.19 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ammeraal Beltech, Habasit AG, Forbo Siegling GmbH, Fenner Drives, Continental AG, Bando Chemical Industries Ltd, Intralox LLC, Esbelt S.A., Nitta Corporation, YongLi Belting |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |