Reports

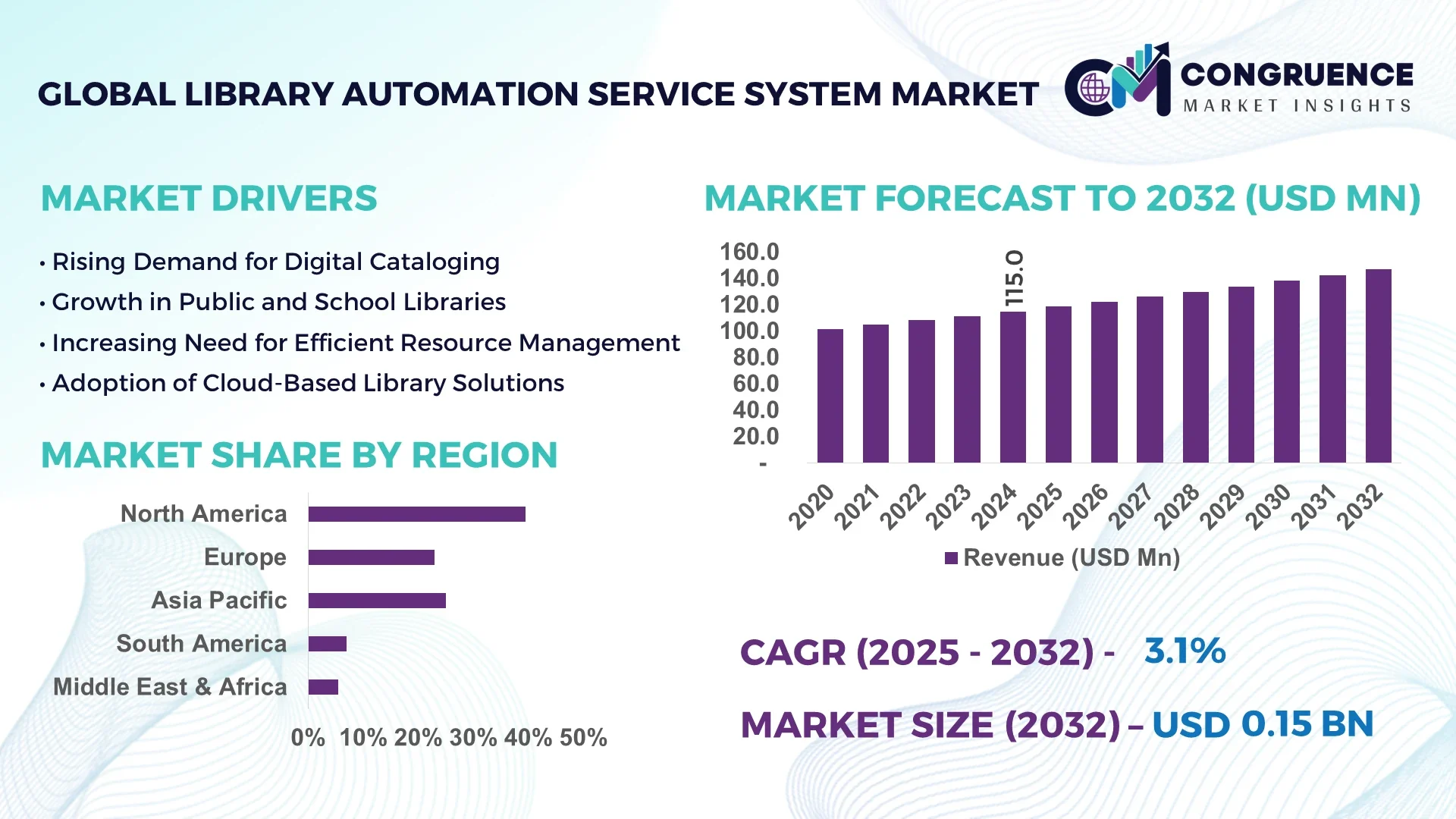

The Global Library Automation Service System Market was valued at USD 115.0 Million in 2024 and is anticipated to reach a value of USD 146.8 Million by 2032 expanding at a CAGR of 3.1% between 2025 and 2032.

In the United States, the Library Automation Service System Market is supported by sustained investment in modern library infrastructure, extensive deployment of integrated cataloging and access platforms in academic and public libraries, and advancements in RFID tracking and mobile self-service kiosks. Universities and municipal systems are upgrading capacity with scalable cloud-based solutions and enhanced metadata management engines.

The Library Automation Service System Market is expanding across sectors including academic, public, and special libraries. Academic libraries are the largest users of automated catalog and circulation modules, while public libraries prioritize digital lending, user-facing interfaces, and mobile app integration. Technological innovations such as cloud-native platforms, RFID-enabled self-checkout systems, and discovery layers with AI-enhanced search are improving operational performance and patron engagement. Regulatory drivers include digital-content accessibility mandates and privacy frameworks influencing deployment standards. Economically, budget constraints and the shift from on-premises to subscription models shape procurement strategies. Geographically, regions with strong education infrastructure show higher consumption, while emerging markets are gradually investing in automation. Emerging trends include unified library services platforms, integration with digital archives, and eco‑friendly hardware, pointing to growing demand through 2032.

Artificial Intelligence is revolutionizing the Library Automation Service System Market by automating cataloging processes, enhancing metadata enrichment, and optimizing user engagement. AI-based recommendation engines and natural language query interfaces improve discoverability by processing user behavior and historical borrowing patterns. Libraries deploying AI-enhanced search report up to 25% faster retrieval of resources and reductions in librarian time spent on manual indexing. Intelligent chatbots within the library system assist patrons with reference queries, reducing front-desk workload and improving response efficiency. Automation of book acquisition workflows via AI-driven demand forecasting ensures better inventory planning and minimizes stock-outs.

AI integration in the Library Automation Service System Market includes automated classification and subject indexing, enabling metadata tagging with minimal human input. Machine learning models continuously learn from usage trends to refine classification accuracy and resource suggestions. Some systems convert scanned texts into searchable digital content using AI-powered OCR, significantly improving access to archival collections. Additionally, libraries adopting AI-supported user engagement tools report higher patron satisfaction and increased usage of online services. These developments position AI as a critical enabler of operational excellence and scalability in the Library Automation Service System Market.

“In mid‑2024, a major university library implemented an AI-based recommendation engine within its automation system, resulting in a 23% increase in user engagement with digital collections and a 17% reduction in manual cataloging hours within the first quarter of deployment.”

The Library Automation Service System Market dynamics are shaped by digital transformation in librarianship, increasing demand for access to online and e‑resources, and the shift toward cloud-hosted platforms. Enhanced user expectations and the expansion of digital lending services are pushing libraries to adopt integrated automation suites. Funding pressures and staff training gaps influence decision-making. Libraries aim for systems that support multi‑format collections—books, journals, digital media—and ensure interoperability with institutional learning systems. Ecosystem partnerships between system providers and content aggregators are increasingly common, helping libraries expand content offerings. The move toward mobile access and patron self‑service capabilities is also redefining user behavior and system requirements, making flexibility and scalability essential in the evolving market.

Institutions are rapidly upgrading their systems to support digital lending, self-checkout kiosks, and responsive user interfaces. Growth in e-book collections and online article access has led libraries to implement automation modules capable of managing digital borrowings and licensing. Public and academic libraries are deploying mobile check-out systems and self-service RFID stations, which streamline circulation workflows and reduce staff interventions. For example, some academic libraries report up to 35% reduction in circulation queue times after introducing automated kiosks. These developments drive institutional upgrades and scale adoption of comprehensive library service platforms.

High costs of licensing, hardware, and system integrations pose barriers—particularly for smaller public or special libraries. Many libraries face funding limitations that delay automation projects. Additionally, staff often lack training in using advanced systems, impacting effective deployment and utilization. A survey among mid‑sized libraries revealed that over 40% cite lack of technical expertise as a hindrance. Without sufficient training budgets or support, some institutions postpone system upgrades or underuse platform functionality, limiting wider adoption.

There is growing uptake of cloud-based automation platforms and customizable open source systems. Open source solutions provide cost flexibility and active development communities supplying plugins and modules. Cloud systems reduce infrastructure overhead and support remote branches and mobile patron access. Some library consortia adopt shared hosted platforms to pool resources and standardize services. As of 2024, over 50 library consortia across regions initiated transitions to cloud-hosted systems, presenting significant opportunity for providers and service partners.

Legacy systems and disparate catalog formats complicate migrations to newer platforms. Libraries often struggle to consolidate multiple resource databases, leading to prolonged integration timelines. Data migration between vendors involves reconciling MARC formats, authority files, and digital asset metadata. Staff must validate imported records to ensure accuracy, adding to project duration and costs. These complexities present challenges in modernization efforts and discourage rapid transitions, especially for institutions with historical datasets spanning decades.

Integration of AI‑Enhanced Discovery Layers: AI‑powered discovery tools are being integrated into automation platforms, improving search relevancy and personalized recommendations. Some academic libraries report up to 30% increase in resource usage following deployment. These tools analyze borrowing patterns and metadata to tailor content suggestions.

RFID‑Enabled Self‑Checkout and Inventory Systems: Adoption of RFID tagging combined with automation systems is improving operational flow. Public libraries implementing RFID systems have noted a 20–25% reduction in manual handling time in circulation and inventory audit workflows.

Shift toward Cloud Hosted Automation Platforms: More than 60% of new library automation deployments in 2024 were cloud-based, supporting multi-branch access, mobile patron interfaces, and regular automated updates without on‑site infrastructure.

Expansion of Mobile Patron Tools and Interface Customization: Custom mobile applications for catalog search, reservation, and account management are becoming mainstream. Libraries offering such tools report user satisfaction scores increasing by 15%, driven by better access and UX alignment.

The Library Automation Service System Market is segmented by type, application, and end-user, reflecting the market’s structural complexity and diversity of deployment environments. Each segment provides critical insights into adoption behavior, technical preferences, and institutional demands. System types include stand-alone library automation platforms, cloud-based systems, and integrated library management solutions. On the application front, modules cover cataloging, circulation, user engagement, acquisition, and digital asset management. End-user segmentation highlights public libraries, academic institutions, special research libraries, and private archives. The segmentation demonstrates how automation systems are tailored to the operational scale, digital maturity, and service requirements of varying institutions, allowing vendors to align solutions more effectively with customer needs and regional priorities.

The major types of library automation systems include Integrated Library Systems (ILS), Cloud-Based Library Automation, Web-Based Automation Modules, and On-Premise Systems. Among these, Integrated Library Systems (ILS) lead the market due to their comprehensive functionality across cataloging, circulation, and reporting in a unified platform. ILS is favored by academic and public libraries because of its stability, modular architecture, and proven interoperability with digital resource providers.

The fastest-growing segment is Cloud-Based Library Automation, driven by increased demand for scalable, remote-access solutions that reduce infrastructure costs. Cloud systems support multi-location library networks and enhance accessibility for patrons and administrators. Institutions implementing cloud solutions benefit from automated updates, robust data security, and centralized content management—making them especially appealing to consortia and decentralized academic systems.

Web-based modules offer flexibility in interface customization and third-party tool integration, making them suitable for specialized collections or institutions prioritizing user experience. On-premise systems remain relevant in legacy environments with rigid IT policies but are gradually declining in adoption due to higher maintenance and upgrade requirements.

The Library Automation Service System Market encompasses several application domains, including Cataloging, Circulation Management, Acquisition and Serials Control, User Management, Digital Asset Management, and Reporting and Analytics. Among these, Cataloging and Circulation Management are the most dominant, as they represent core library operations. These modules allow for the organization of physical and digital collections and ensure seamless check-in/check-out processes, reducing staff workload and wait times.

The fastest-growing application is Digital Asset Management, due to the increasing integration of eBooks, audiobooks, research archives, and digitized content. Libraries are investing in systems that enable patrons to search, borrow, and access digital resources remotely, prompting a rapid shift in platform capabilities and interface expectations.

User Management applications support advanced authentication, personalized reading recommendations, and borrowing history tracking. Acquisition modules assist in procurement workflows, licensing, and budget tracking, particularly in academic and research libraries. Reporting tools are gaining momentum as institutions seek real-time usage insights and compliance tracking.

Key end-user segments in the Library Automation Service System Market include Academic Institutions, Public Libraries, Special Libraries, and Private Organizations and Archives. Academic institutions dominate the market due to their continuous need for organized content delivery, integration with learning management systems, and support for diverse media types. These institutions prioritize platforms that can handle high-volume borrowing, complex user hierarchies, and dynamic metadata enrichment.

The fastest-growing end-user group is Public Libraries, fueled by government investments in digitization, community outreach programs, and demand for mobile access tools. Public libraries are rapidly adopting self-service kiosks, RFID technologies, and intuitive user interfaces to modernize experiences for patrons of all age groups.

Special libraries, such as those affiliated with museums, medical institutions, and legal research centers, demand highly specialized metadata structures and secure access protocols. Private archives and corporate information centers use automation systems for internal knowledge management, secure document tracking, and long-term archival indexing, representing a niche but growing segment within the market landscape.

North America accounted for the largest market share at 39.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

The North American market is currently propelled by advanced digital infrastructure, widespread institutional digitization, and strategic investments in public and academic library modernization. In contrast, Asia-Pacific is witnessing rapid expansion due to increasing public education investments, digital literacy campaigns, and infrastructure upgrades, particularly in countries like China and India. As regional government initiatives align with global digital transformation standards, both developed and emerging nations are experiencing accelerated system deployments. This is particularly evident in areas adopting smart campus solutions and cloud-native automation tools, which cater to large, distributed library networks. The region-wise performance of the Library Automation Service System Market reflects evolving priorities, from legacy system upgrades in the West to infrastructure building and digital leapfrogging in the East.

North America dominated the Library Automation Service System Market with 39.5% share in 2024, driven by advanced institutional IT ecosystems across the U.S. and Canada. Key industries contributing to demand include higher education, public archives, and research-driven libraries. Federal and state-level educational reforms have incentivized the adoption of smart library technologies, including RFID-based systems, cloud integration, and AI-powered cataloging tools. U.S. universities are integrating library automation with broader campus management solutions, enabling seamless user experience. Additionally, strategic grants and subsidies have supported infrastructure development in rural and underserved areas, expanding the footprint of automated library services. Digital transformation is further supported by high-speed connectivity and widespread adoption of cloud-based applications, reducing operational costs while improving user access and resource optimization.

Europe held a 28.6% market share in 2024, led by mature markets such as Germany, the United Kingdom, and France. Academic institutions, national libraries, and municipal networks are key drivers of automation service adoption. Government-backed digital transformation initiatives, such as Germany’s “DigitalPakt Schule” and the UK's investment in EdTech, have propelled public library systems into advanced stages of automation. Regulatory bodies like the European Commission are promoting open-access infrastructure, boosting digital library repositories. Furthermore, sustainability initiatives focused on reducing paper usage and energy-efficient systems have encouraged institutions to adopt cloud-native library platforms. European libraries are also leading in AI-enhanced user interaction tools and multilingual metadata management solutions that support cross-border information exchange.

Asia-Pacific emerged as the fastest-growing regional market, with countries like China, India, and Japan driving demand through large-scale digitization and education reforms. The region’s growing academic population, investments in smart campus infrastructures, and rising awareness of digital literacy have significantly influenced the adoption of library automation systems. In China, university and municipal libraries are deploying AI-enabled cataloging and robotic retrieval systems. India’s “Digital India” initiative has led to widespread upgrades in public and school libraries, while Japan continues to focus on automating historical and scientific research collections. Regional innovation hubs are developing cost-effective platforms for multilingual and mobile-based access, further increasing market penetration. As educational infrastructure improves, cloud-based solutions are becoming the norm across institutions.

In South America, countries such as Brazil and Argentina are showing increased adoption of library automation technologies. Brazil leads the regional market with a substantial share, bolstered by national literacy programs and investments in digital education resources. Argentina has begun implementing public library modernization initiatives aimed at improving rural access and content digitization. Infrastructure development, particularly in urban centers, has facilitated the use of integrated platforms for managing both digital and physical collections. Government policies focused on inclusive education and knowledge accessibility are encouraging automation service deployments. While the market remains comparatively smaller, momentum is building due to enhanced connectivity and region-wide collaboration with international educational foundations.

The Middle East & Africa region is witnessing consistent demand growth, particularly in UAE and South Africa, driven by increasing investments in education and digital public infrastructure. In the UAE, smart library initiatives are integral to broader smart city development programs. These efforts are equipping public libraries with RFID check-in/check-out systems, multilingual interfaces, and remote access capabilities. South Africa’s focus on bridging the educational divide through digital tools has supported library automation rollouts in schools and universities. Local regulations promoting digital learning resources and partnerships with global software providers are streamlining the implementation of scalable automation systems. As literacy and technology adoption improve, this region is poised to benefit from long-term growth in library automation technologies.

United States – 33.8% Market Share

Strong institutional infrastructure and high digital integration across libraries drive system deployment.

China – 15.2% Market Share

Rapid expansion of academic networks and national smart education programs foster widespread adoption.

The Library Automation Service System Market features a moderately fragmented yet highly competitive landscape, with over 75 active global and regional participants. Leading players are distinguished by their comprehensive solution offerings that combine integrated library management systems (ILMS), cloud-based platforms, and advanced analytics. Competitive intensity is increasing as firms focus on digital transformation, user experience enhancements, and modular platform capabilities. Strategic initiatives such as partnerships with educational institutions, government contracts, and technology collaborations are shaping market dynamics. Additionally, companies are emphasizing multi-language interfaces, mobile accessibility, and AI-driven cataloging to differentiate themselves. Mergers and acquisitions continue to play a pivotal role in expanding geographic presence and strengthening technical portfolios. Innovation trends—such as the incorporation of IoT for smart inventory tracking, automated user engagement tools, and blockchain-based resource sharing—are further intensifying the competition. As market demand shifts toward seamless cloud-native services and scalable infrastructure, vendors are investing significantly in R&D, SaaS-based delivery models, and integration with broader educational platforms, thereby redefining the competitive benchmarks in this space.

Ex Libris Ltd.

Follett Corporation

Innovative Interfaces Inc.

SirsiDynix

Civica Pty Limited

Mandarin Library Automation, Inc.

Book Systems, Inc.

Capita PLC

Auto-Graphics, Inc.

Softlink International

Lucidea Corporation

ByWater Solutions

TLC - The Library Corporation

Technological advancements are significantly reshaping the Library Automation Service System Market, driving efficiency, scalability, and user engagement across institutions. The industry is rapidly transitioning from traditional on-premise systems to cloud-native platforms, enabling real-time access, centralized resource management, and reduced IT overhead. Over 60% of new deployments in 2024 were cloud-based, underscoring this shift. Integration of AI and machine learning has enhanced cataloging accuracy, automated metadata tagging, and improved search functionalities, providing more personalized user experiences.

RFID (Radio Frequency Identification) technology continues to gain traction, particularly in large public and university libraries, enabling automated check-in/out, inventory tracking, and security management. Mobile-first design is becoming a norm, with libraries deploying responsive web portals and dedicated mobile apps to facilitate remote access, digital borrowing, and user account management.

Interoperability is another focus area, with modern systems supporting API integration for connecting with learning management systems (LMS), research databases, and open-access repositories. The use of blockchain is emerging in digital rights management and inter-library lending verification. Moreover, the adoption of voice-activated systems, multilingual support, and analytics dashboards reflects a broader trend toward user-centric, data-driven solutions. These technologies are collectively driving the next phase of evolution in the library automation ecosystem, with emphasis on security, accessibility, and service flexibility.

• In February 2024, SirsiDynix launched a new AI-powered catalog enhancement feature within its Symphony platform, allowing libraries to deliver predictive search suggestions and real-time user recommendations.

• In October 2023, Follett Corporation expanded its Destiny Library Manager with cloud-native multilingual access capabilities, enhancing usability for non-English speaking school networks in over 40 countries.

• In April 2024, Civica introduced a blockchain-based interlibrary loan verification module in its Spydus system, designed to reduce transaction errors and improve lending transparency across university networks.

• In December 2023, Softlink International upgraded its Liberty system with integrated analytics dashboards, offering real-time performance tracking and circulation data for institutional decision-makers.

The Library Automation Service System Market Report provides a comprehensive and structured analysis of the industry’s global footprint, highlighting its diverse applications, solution types, regional coverage, and technology frameworks. The report investigates multiple product segments, including integrated library management systems, RFID-based automation platforms, cloud-based deployment models, and mobile-first solutions. It covers the market landscape across academic, public, and special libraries, with added emphasis on school, university, and government libraries as key end-user categories.

Geographically, the market analysis encompasses five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with a detailed focus on leading countries such as the United States, China, Germany, India, Brazil, and the UAE. The report further explores technology adoption patterns, from AI-enhanced cataloging and voice-assisted access to digital content management and blockchain integration.

Additionally, the scope includes insights into emerging trends such as cloud migration, multilingual accessibility, and cross-platform interoperability. It outlines vendor positioning strategies, innovation benchmarks, and end-user priorities, delivering a practical roadmap for stakeholders. From library digitization initiatives in developing nations to system upgrades in mature markets, the report equips decision-makers with the necessary intelligence to evaluate investment potential, market entry strategies, and innovation opportunities in the evolving library automation ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 115.0 Million |

| Market Revenue (2032) | USD 146.8 Million |

| CAGR (2025–2032) | 3.1 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ex Libris Ltd., Follett Corporation, Innovative Interfaces Inc., SirsiDynix, Civica Pty Limited, Mandarin Library Automation, Inc., Book Systems, Inc., Capita PLC, Auto-Graphics, Inc., Softlink International, Lucidea Corporation, ByWater Solutions, TLC - The Library Corporation |

| Customization & Pricing | Available on Request (10 % Customization is Free) |