Reports

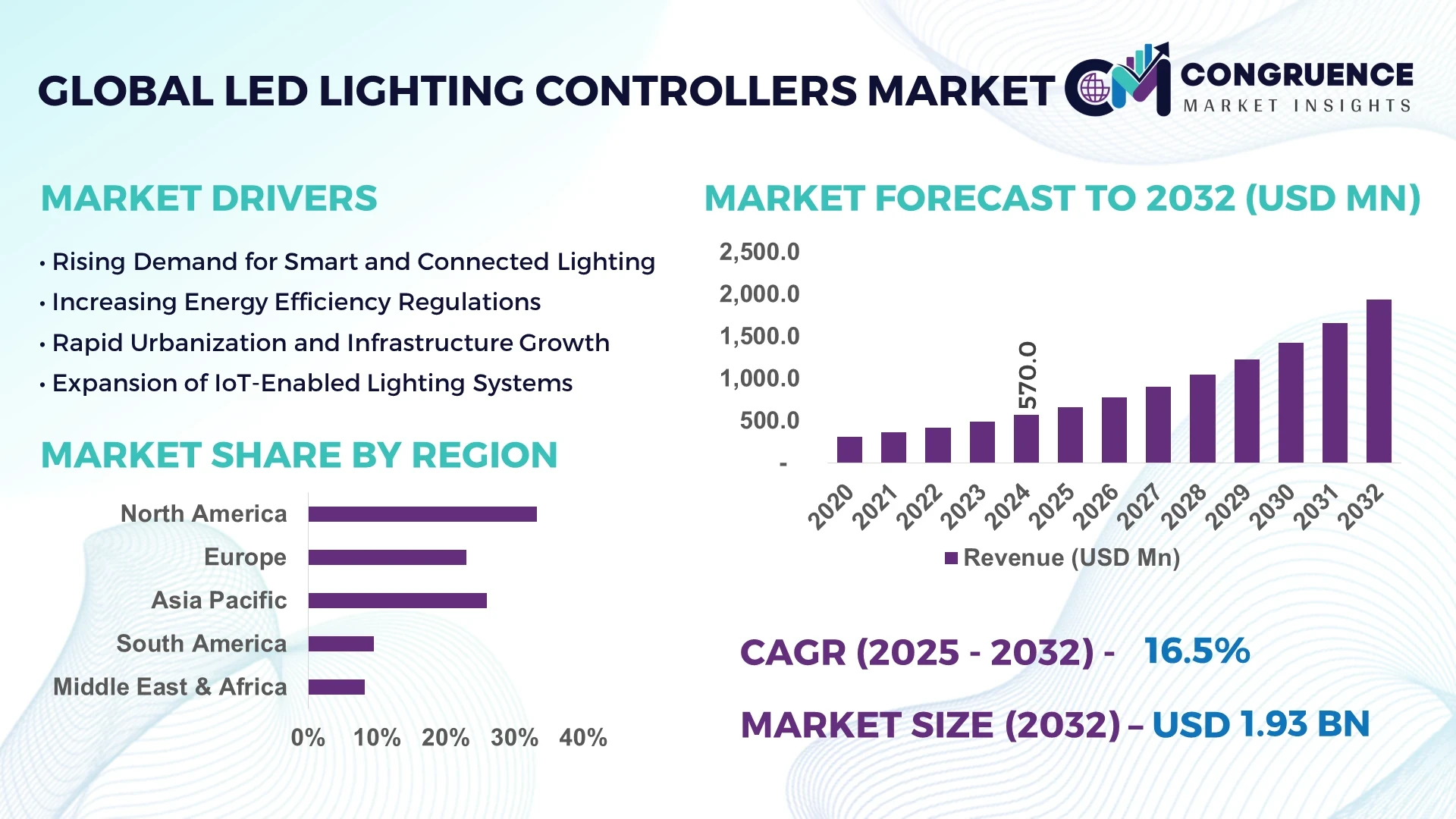

The Global LED Lighting Controllers Market was valued at USD 570.0 Million in 2024 and is anticipated to reach a value of USD 1,934.1 Million by 2032 expanding at a CAGR of 16.5% between 2025 and 2032.

The United States leads the market, representing a major share driven by rapid adoption of intelligent LED controllers across commercial office spaces and smart city lighting networks, supported by consumer demand for connected lighting and stringent energy efficiency regulations.

The market is witnessing strong innovation, with manufacturers introducing modular controller units that support seamless integration with IoT platforms and voice assistants in residential settings. In hospitality and retail environments, custom lighting scenes and adaptive brightness controls are becoming standard components of experiential design. Large infrastructure projects, such as transit hubs and campuses, increasingly specify centralized LED controller systems with advanced scheduling and sensor-based dimming capabilities for enhanced safety, cost savings, and operational efficiency.

AI is rapidly reshaping the LED Lighting Controllers market by bringing intelligent automation, dynamic energy optimization, and user-centric lighting experiences. Advanced AI-powered controllers analyze real-time sensor data—such as occupancy patterns, ambient light, and temperature—to automatically adjust brightness, color temperature, and lighting schedules. Instead of static timers or manual dimming, these systems adapt to usage trends and external conditions, ensuring lights are on only when needed and configured to occupant preferences.

In large commercial buildings, AI controllers can learn traffic flows and meeting schedules to preemptively reduce light usage in empty zones while maintaining optimal performance in active areas. Retail chains are deploying scene-aware AI algorithms that switch between brighter lighting during peak hours and mood lighting during evenings, helping increase customer dwell time and improve visual merchandising. Public infrastructure applications, such as street and park lighting, use AI to detect pedestrian and vehicle movement, adjusting illumination in real time to enhance safety and conserve power. In smart homes, AI connects with voice assistants, adapting lighting based on time of day and household routines, improving comfort with minimal user input.

"In early 2025, Philips launched a generative AI-powered feature in its Hue app. Users can request scenes like “garden party” or “relaxing evening,” and the system automatically creates full lighting setups and refines them based on feedback. Over the first quarter post-launch, the feature was used by over 250,000 users to generate daily light routines, significantly reducing manual scene creation and enhancing engagement."

Rising global energy costs and tightening efficiency regulations are driving the shift toward LED lighting systems with intelligent controllers. Corporations and municipalities actively invest in dimmers, occupancy sensors, and daylight harvesting systems to reduce electricity consumption. For instance, demand for wired LED controllers continues to increase as facilities upgrade outdated lighting systems to reduce operational costs and meet environmental targets.

As smart lighting ecosystems evolve, integrating controllers from different manufacturers often leads to compatibility challenges. Home and building automation systems that mix Zigbee, Z-Wave, Wi‑Fi, and proprietary protocols frequently suffer from syncing issues. This limits large-scale deployments and raises deployment costs when custom middleware and extensive commissioning are needed.

Global urban centers are investing heavily in smart street lighting using LED controllers integrated with traffic monitoring, emergency response, and pedestrian detection. Smart city projects—particularly those mandating remote dimming and sensor-triggered activation—are expected to drive large-volume controller procurements, creating a high-growth opportunity for manufacturers focused on scalable, IoT-ready solutions.

As LED controllers become IoT-connected, they introduce new vulnerabilities. Enterprises and municipalities must address secure encryption, patch management, and risk of malicious control hijacking. High-profile incidents in municipal lighting networks have prompted authorities to pause wide rollouts until cybersecurity standards are fully validated. The lack of unified security protocols for lighting networks remains a significant challenge for manufacturers and system integrators alike.

Demand for modular, wireless control units: Adoption of plug-and-play controller modules that work with standard LED fixtures allows retrofitting in commercial office spaces. These modules support Bluetooth mesh and Zigbee, greatly reducing installation time and complexity while facilitating scalable lighting systems.

Focus on human-centric and circadian lighting: Facilities management teams are specifying controllers capable of gradual dimming and colour shifts aligned with daylight patterns—promoting occupant wellness. In healthcare environments, LED controllers now fine-tune bluish-white light in mornings for alertness and warmer tones at night to support relaxation.

Integration with building management systems (BMS): Enterprise-grade LED controllers increasingly communicate over BACnet and Modbus to synchronize with HVAC, security, and access control. Buildings adopting this strategy report unified operational dashboards and measurable efficiency gains across utilities.

AI-enhanced commissioning and maintenance: Controllers with embedded AI optimize performance via self-calibration, auto-commissioning routines, and predictive maintenance alerts. In mixed-use campuses and hospitality venues, such systems reduce configuration time and maintenance visits significantly.

The LED Lighting Controllers market is segmented based on type, application, and end-user, each influencing the industry’s growth trajectory in unique ways. Understanding these segments provides deeper insights into current demand trends, product development focus, and end-user purchasing behaviors. While wired controllers remain dominant in legacy systems, wireless controllers are quickly gaining ground due to scalability, ease of installation, and compatibility with smart technologies. Application-wise, commercial and industrial settings lead the way, but residential adoption is growing rapidly due to increased smart home deployments. On the end-user front, enterprises, municipalities, and individual consumers present distinct needs, influencing product design, network capability, and connectivity standards.

The LED Lighting Controllers Market by type includes Wired Controllers and Wireless Controllers. Wired controllers currently hold the largest market share due to their long-established use in industrial and commercial settings, offering robust performance with minimal interference and secure connections. These controllers are particularly preferred in large-scale installations where centralized management and reliability are crucial. However, the fastest-growing segment is Wireless Controllers. Fueled by the boom in smart home technology and retrofit projects, wireless controllers are being rapidly adopted across residential, hospitality, and light commercial environments. Their ease of installation, compatibility with Bluetooth, Zigbee, Wi-Fi, and mesh networks, and lower infrastructure cost make them ideal for flexible and scalable lighting ecosystems. Wireless controllers also support remote management, app-based control, and seamless integration with voice assistants and other smart devices. As adoption of IoT and home automation surges, wireless LED controllers are expected to outpace wired variants in growth, particularly in developing markets and urban residential zones.

Key applications in the LED Lighting Controllers Market include Indoor Lighting and Outdoor Lighting. Among these, Indoor Lighting holds the leading market share due to its vast deployment in office buildings, shopping malls, schools, hospitals, and residences. The growing emphasis on energy-efficient building design and wellness-oriented lighting strategies is driving investments in intelligent indoor controllers that manage brightness, color temperature, and scheduling based on occupancy and daylight. Outdoor Lighting, however, is emerging as the fastest-growing segment. Smart city initiatives and public infrastructure upgrades are pushing governments and municipalities to adopt intelligent outdoor lighting systems. These include controllers integrated with motion sensors, ambient light sensors, and networked communication systems for streetlights, parks, campuses, and highways. Outdoor controllers with features like automatic dimming during low traffic periods and fault detection are significantly reducing energy consumption and maintenance costs. As urbanization expands, and cities invest in safety and efficiency, the demand for adaptive outdoor LED controllers is expected to rise exponentially.

The LED Lighting Controllers Market serves a diverse range of end users, including Residential, Commercial, and Industrial sectors. The Commercial segment currently dominates the market due to high deployment in retail spaces, corporate offices, hotels, and public institutions. This dominance is attributed to bulk lighting requirements, stringent energy regulations, and growing demand for building automation systems that incorporate intelligent lighting control. The fastest-growing segment is the Residential end-user category. Rapid consumer adoption of smart home technologies is leading to increased installations of smart lighting systems controlled through mobile apps, voice assistants, or home automation hubs. Consumers are opting for wireless LED controllers to manage lighting preferences, create moods, and automate schedules. Additionally, DIY-friendly devices and falling prices have accelerated penetration across urban households. Meanwhile, the Industrial segment maintains steady growth, driven by warehouses, manufacturing plants, and logistics centers optimizing energy use and safety through sensor-based lighting. However, adoption in this segment is often gradual due to integration complexity and long equipment lifecycles.

North America accounted for the largest market share at 33.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2025 and 2032.

The North American region continues to lead due to strong smart building adoption, stringent energy efficiency mandates, and robust infrastructure modernization. Meanwhile, Asia-Pacific is witnessing rapid urbanization, government-backed LED adoption programs, and booming construction sectors in countries like China and India, propelling aggressive deployment of advanced lighting systems. Europe, South America, and the Middle East & Africa are also showing stable growth driven by public infrastructure upgrades and increased adoption of IoT-enabled LED controllers.

Smart Building Integration Fueling Controller Adoption

The North America LED Lighting Controllers market leads globally, with the United States contributing over USD 161.6 million in 2024 alone. Smart lighting solutions are becoming standard across new commercial construction, with controllers integrated into HVAC and security systems for centralized automation. Wireless LED controllers equipped with Zigbee and Wi-Fi dominate new installations due to ease of deployment in both new and retrofit projects. Municipal investment in smart street lighting across the U.S. and Canada is another driving force, with thousands of LED nodes controlled by adaptive systems that respond to motion, traffic, and ambient lighting data. Utility incentives and LEED certification trends are further encouraging businesses to replace outdated systems with energy-saving smart lighting controls.

Surge in Green Building Renovations Boosting Demand

Europe is seeing steady expansion in the LED Lighting Controllers market, particularly in Germany, the UK, and the Nordic countries. The region’s strong emphasis on sustainable architecture and energy-efficient retrofits is propelling the use of daylight-harvesting and occupancy-based controllers in offices, schools, and healthcare buildings. In 2024, the region saw more than USD 110 million worth of LED controllers deployed, with a strong lean toward wired solutions in large-scale commercial projects. The European Union’s push for carbon neutrality by 2050 is driving public and private investments in advanced lighting technologies. Additionally, increasing integration with building automation systems using KNX and DALI protocols is enabling precise, programmable control over energy usage.

Urban Infrastructure Expansion Powering Market Growth

Asia-Pacific is the fastest-growing regional market for LED Lighting Controllers, led by China, India, Japan, and South Korea. In 2024, the region recorded over USD 145 million in LED lighting controller revenues. Massive urban infrastructure development—including smart cities, metro systems, and high-rise commercial complexes—is creating unprecedented demand for intelligent lighting controls. Governments in India and China are aggressively phasing out incandescent and CFL systems in favor of LED setups with programmable controllers. Wireless controllers are gaining traction in residential and small business segments, particularly in smart home ecosystems. Public lighting upgrades and industrial warehouse expansions in Southeast Asia further contribute to the strong regional momentum.

Public Infrastructure and Hospitality Renovation Driving Demand

South America’s LED Lighting Controllers Market is gradually expanding, driven by demand from Brazil, Argentina, and Chile. In 2024, controller sales across the region surpassed USD 42 million. Urban redevelopment initiatives and renovation of public and hospitality infrastructure are creating demand for automated and remotely controlled lighting solutions. Smart lighting projects in city parks, transport hubs, and government buildings are being launched to reduce power consumption and improve visibility. The hospitality industry, especially in Brazil, is investing in smart controllers that manage ambiance and energy usage. However, adoption remains moderate due to limited awareness and lower private sector investment in automation technologies.

Smart Lighting in Commercial Complexes on the Rise

In the Middle East & Africa, the market reached over USD 38 million in 2024, with strong growth potential. UAE and Saudi Arabia are driving demand through high-end residential, commercial, and entertainment projects integrating advanced lighting solutions. Dubai’s smart city vision and Saudi Arabia’s NEOM initiative are deploying thousands of smart LED systems with remote-controlled lighting environments. Africa’s LED controller market remains emerging, but uptake in South Africa and Kenya is increasing, supported by international development grants aimed at enhancing urban safety and energy efficiency. Commercial and public infrastructure projects are the primary adopters of intelligent controllers in the region.

United States - values at USD 161.6 million in 2024, due to large-scale adoption in commercial buildings and smart cities.

China - values at USD 103.4 million in 2024, is driven by rapid urbanization, state-funded smart city projects, and industrial upgrades.

The LED Lighting Controllers market is characterized by intense competition with global and regional players striving to expand portfolios and enhance technological capabilities. Companies are heavily investing in R&D to strengthen product differentiation, focusing on features like wireless connectivity, AI integration, and enhanced security. As markets globalize, vendors are forming strategic partnerships with smart building integrators and IoT platform providers to accelerate adoption in commercial and industrial segments. Regional leaders are also localizing manufacturing and after-sales support to improve supply chain responsiveness. Innovation-oriented competition has led to frequent launches of compact, modular, and plug-and-play controllers tailored for retrofit and new-construction projects. Many firms are focusing on developing controllers with multi-protocol compatibility, addressing growing demand for Zigbee, Thread, Bluetooth, DALI, and proprietary protocol interoperability. Additionally, pricing strategies are increasingly aligned with bundled offerings that include sensors and gateway modules, enhancing value for end users. Overall, the competitive landscape is gradually shifting toward ecosystem-driven differentiation rather than product specifications alone.

Signify (Philips Hue)

Lutron Electronics

Crestron Electronics

Legrand

Gre Alpha (GRE Alpha)

Casambi Technologies

Hubbell Lighting

Acuity Brands

Eaton Corporation

LED lighting controllers are becoming increasingly sophisticated, integrating a blend of hardware and software technologies to enhance usability, interoperability, and energy performance. Recent developments include the adoption of multi-protocol wireless radios supporting Zigbee, Bluetooth Mesh, Thread, and Wi-Fi networks within a single controller. Such convergence enables versatile deployments and seamless integration with smart home and building platforms. Controllers are now embedding on-device intelligence to execute occupancy-based dimming, scheduled color tuning, and voice control without dependence on the cloud—significantly reducing latency and enhancing privacy. Advanced power electronics are also being implemented, allowing controllers to operate at lower voltages and with higher dimming resolution, minimizing flicker and extending LED lifespan. Integration of ambient light sensors and thermal monitoring chips is providing adaptive control and overheating protection. Meanwhile, node-level controllers with embedded firmware are supporting over-the-air updates and remote diagnostics, enabling predictive maintenance in campus and industrial settings. Standardization around DALI-2 and Matter is enabling plug-and-play interoperability across controllers, sensors, and gateways, making installations more scalable and easier to certify.

In June 2024, Hikvision unveiled its 5th-generation LED display controller at its LED Displays Launch Event, introducing dual-optimized manufacturing operations and enhanced outdoor module controllers that improve synchronization and color consistency across large deployments.

In July 2024, Inolux released the IN-PIS63BTx, the industry’s first addressable monocolor LED controller series, offering built-in driver ICs for simplified PCB layouts and enabling high-speed refresh rates optimal for dynamic architectural lighting systems.

In Q4 2023, Philips Hue updated its mobile app with four new lighting effects—cosmos, underwater, enchant, and sunbeam—and added effect customization capabilities, increasing user control and competition with rival smart lighting brands.

In January 2025, Sensify introduced Zigbee-based ambient sensing firmware, allowing existing light controllers to detect motion without additional sensors—a feature set to democratize occupancy-based automation across millions of installed devices.

The scope of the LED Lighting Controllers Market Report encompasses a comprehensive examination of the controller ecosystem covering both hardware and software components deployed in commercial, residential, industrial, public infrastructure, and outdoor applications. It analyzes wired and wireless controller technologies, including single-zone dimmers, multi-scene controllers, sensor-integrated modules, and gateway-integrated units. The report reviews end-user segments such as smart homes, commercial buildings, municipal infrastructure, hospitality venues, and industrial facilities, documenting usage patterns, procurement cycles, and deployment dynamics. Regional insights span North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, assessing regulatory frameworks, energy standards, and infrastructure initiatives. Technological evaluation includes protocol compatibility (Zigbee, DALI‑2, Bluetooth Mesh, Thread, Wi‑Fi), AI-driven lighting logic, built-in security features, firmware update capabilities, and integration with building management systems. Furthermore, the report covers competitive landscape analysis, profiling active market players, innovation pipelines, partnership strategies, and M&A trends. Deliverables include quantitative segmentation by type, application, and end-user; regional forecasts; technology maturity assessments; strategic recommendations; and a curated list of recent product launches and market movements.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global LED Lighting Controllers Market |

| Market Revenue (2024) | USD 570.0 Million |

| Market Revenue (2032) | USD 1,934.1 Million |

| CAGR (2025–2032) | 16.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Signify (Philips Hue), Lutron Electronics, Crestron Electronics, Legrand, Gre Alpha (GRE Alpha), Casambi Technologies, Hubbell Lighting, Acuity Brands, Eaton Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |