Reports

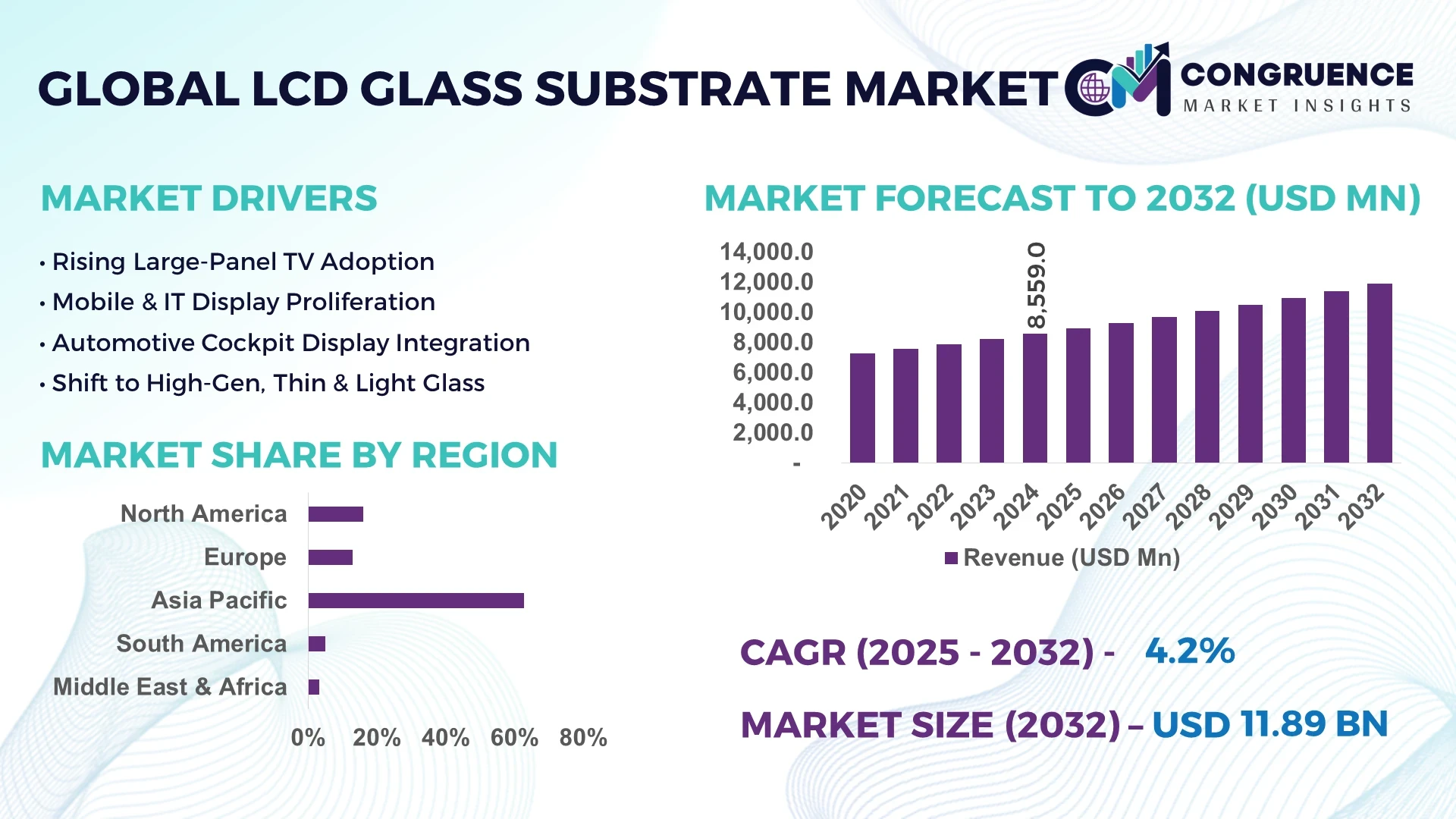

The Global LCD Glass Substrate Market was valued at USD 8,558.98 Million in 2024 and is anticipated to reach a value of USD 11,894.99 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032.

In South Korea, the LCD Glass Substrate Market benefits from a robust production capacity exceeding 75 million square meters annually, advanced ultra-thin substrate processing lines, consistent investments in high-generation fabs, and integration of smart manufacturing technologies across LCD panel fabrication facilities.

The LCD Glass Substrate Market serves diverse sectors, including consumer electronics, automotive displays, industrial monitoring, and healthcare visualization systems, driving the demand for high-resolution, durable, and energy-efficient LCD panels. Recent technological advancements include the development of Gen 10.5 and Gen 11 substrate lines that allow manufacturers to produce larger and higher-quality panels, reducing per-unit production costs. Environmental and regulatory factors encouraging low-emission and lightweight display solutions are supporting the adoption of advanced glass substrates globally. Regional consumption patterns highlight Asia-Pacific as a major hub for manufacturing and assembly, while North America and Europe are seeing increasing demand driven by smart devices, automotive HUDs, and medical monitors. Additionally, the integration of OLED hybrid technology with LCD backplanes and the emergence of flexible substrates for automotive dashboards and wearable devices are shaping the future landscape of the LCD Glass Substrate Market, providing new avenues for technological differentiation and long-term growth.

Artificial intelligence is transforming the LCD Glass Substrate Market by significantly improving production process efficiency, enhancing defect detection, and reducing operational downtime across advanced substrate manufacturing facilities. By integrating AI-powered predictive maintenance systems, manufacturers within the LCD Glass Substrate Market can analyze sensor data in real time, allowing equipment to operate at optimal conditions while reducing the frequency and cost of unplanned maintenance. AI algorithms are also being utilized for smart defect mapping during the inspection of ultra-thin glass substrates, enabling higher yield rates while maintaining quality standards required for premium display applications.

The LCD Glass Substrate Market benefits from AI-driven energy optimization models that manage and adjust energy consumption across annealing and coating processes, contributing to cost savings while meeting sustainability goals. Advanced machine learning models are being integrated into process control systems to optimize etching and chemical strengthening parameters, reducing waste and improving consistency across high-volume substrate lines. Additionally, AI applications are facilitating automated grading and classification of glass substrates for different end-use segments, enhancing supply chain agility within the LCD Glass Substrate Market. As manufacturers transition to higher-generation glass substrates, AI-based robotic systems are being deployed for precise handling and transportation of large glass sheets, reducing the risk of microcracks or edge damage during processing. These AI-driven advancements in the LCD Glass Substrate Market collectively foster higher productivity, lower operational costs, and improved quality, aligning with the growing demand for high-resolution, energy-efficient displays across the electronics and automotive sectors.

“In March 2025, a leading South Korean display manufacturer deployed an AI-enabled defect inspection system on its Gen 8.6 LCD Glass Substrate production line, achieving a 37% reduction in defect detection time and improving substrate yield by 4.8% within the first quarter of integration.”

The LCD Glass Substrate Market is witnessing dynamic growth driven by the rising adoption of high-resolution and energy-efficient display panels across smartphones, automotive displays, and industrial monitors. The transition towards Gen 8 and above glass substrate manufacturing is increasing the availability of larger panels while reducing unit production costs, contributing to overall capacity expansion within the LCD Glass Substrate Market. Environmental regulations and sustainability initiatives are pushing manufacturers to adopt advanced lightweight and recyclable glass materials. Technological innovations such as ultra-thin substrate production and integration with OLED hybrid layers are influencing product development strategies, while the increasing demand for automotive HUDs, medical visualization devices, and smart wearable displays further supports steady consumption patterns across regions.

The increasing demand for high-resolution consumer electronics is a significant driver of the LCD Glass Substrate Market, with manufacturers focusing on developing ultra-thin, durable, and low-reflective substrates to meet evolving end-user requirements. The global shipment of 4K and 8K televisions, which require advanced glass substrates for high pixel density, continues to rise, fueling substrate production across key manufacturing hubs in Asia-Pacific. Smartphones, tablets, and laptops now emphasize high-refresh-rate displays, requiring substrates with excellent thermal and mechanical stability for advanced TFT-LCD structures. The emergence of gaming monitors with enhanced color accuracy and low-latency capabilities is further strengthening demand, while industrial and medical displays require substrates capable of withstanding prolonged operational conditions, adding to the LCD Glass Substrate Market’s growth momentum.

The technical complexity involved in producing ultra-thin and large-area substrates poses a significant restraint within the LCD Glass Substrate Market. Producing Gen 10 and Gen 11 substrates requires advanced handling and transportation processes, with even minor vibrations or surface inconsistencies leading to microcracks and yield loss during the cutting and lamination stages. Manufacturers face challenges in balancing substrate thinness with mechanical durability while ensuring defect-free surfaces essential for high-resolution display panels. Additionally, the requirement for precision in temperature and chemical treatment during the annealing and etching processes adds operational complexity, increasing the costs associated with quality control and maintenance, thereby constraining scalability in the LCD Glass Substrate Market.

The integration of LCD glass substrates within advanced automotive and medical display technologies presents a promising opportunity for the LCD Glass Substrate Market. Automotive applications such as head-up displays (HUDs), digital instrument clusters, and in-vehicle infotainment systems increasingly require high-brightness and durable glass substrates capable of withstanding temperature fluctuations and vibrations while providing clear visibility. In the healthcare sector, the rising demand for medical imaging systems, surgical monitors, and patient monitoring devices is driving the need for glass substrates with high color accuracy and stability. The push towards smart and connected devices in these sectors aligns with substrate manufacturers’ focus on producing high-performance glass solutions, enabling market expansion into high-value application areas within the LCD Glass Substrate Market.

Supply chain vulnerabilities and raw material constraints represent a notable challenge for the LCD Glass Substrate Market, particularly amid geopolitical uncertainties and trade restrictions affecting the global flow of key materials such as silica sand and specialty coatings required in substrate manufacturing. Fluctuations in raw material availability can lead to delays in production schedules, while transportation disruptions impact timely delivery to panel manufacturers. Furthermore, the need for consistent quality in raw materials to achieve defect-free substrates adds pressure on procurement processes. Manufacturers are required to diversify supply chains and adopt risk mitigation strategies to manage these challenges effectively, ensuring operational continuity and maintaining competitiveness in the LCD Glass Substrate Market.

• Shift Toward Ultra-Thin Substrate Production: Manufacturers in the LCD Glass Substrate market are increasingly investing in ultra-thin substrate lines, with thicknesses reaching 0.3 mm and below, to support the development of lighter, slimmer displays in smartphones and advanced monitors. This trend is driven by the demand for high-resolution and energy-efficient displays that require substrates capable of maintaining mechanical stability while reducing weight, enabling the creation of foldable and flexible devices within the premium consumer electronics sector.

• Adoption of Gen 10 and Gen 11 Production Lines: The implementation of Gen 10 and Gen 11 glass substrate production facilities is rising to meet the manufacturing of large-sized LCD panels for television and commercial display applications. These advanced lines enable the cutting of eight to ten 65-inch panels from a single substrate, optimizing production efficiency while reducing per-panel production costs, thus addressing the growing demand for large-format displays in North America and Asia-Pacific.

• Increased Integration with OLED Hybrid Panels: The LCD Glass Substrate market is experiencing a measurable increase in demand due to the integration of OLED hybrid technology with LCD backplanes. Manufacturers are leveraging existing LCD substrate infrastructure to produce OLED panels with improved durability and cost-effectiveness, enhancing the adoption of OLED-equipped devices in laptops and high-end monitors while maintaining the scalability benefits of LCD substrate processing.

• AI-Powered Quality Control in Manufacturing: AI-powered inspection and predictive maintenance systems are being deployed across LCD Glass Substrate manufacturing lines, enabling real-time defect detection and improving yield rates. Facilities utilizing AI-based quality control have reported defect detection time reductions by up to 40% while maintaining precision for micro-level surface inconsistencies, which is critical for ensuring the quality of ultra-thin and large-area substrates for high-performance display applications.

The LCD Glass Substrate market segmentation is structured around type, application, and end-user categories, reflecting its diverse industrial integration across electronics and automotive sectors. Types include ultra-thin, standard, and flexible glass substrates, aligning with the evolving demand for lightweight and high-performance displays. Application areas span smartphones, televisions, automotive displays, industrial monitoring equipment, and medical visualization systems, indicating widespread sectoral usage. End-users range from electronics manufacturers and automotive OEMs to healthcare equipment providers, each leveraging specific substrate features for precision display performance and durability. This segmentation supports strategic supply chain planning and production scaling, enabling stakeholders to align capacity with sector-specific consumption trends while maintaining quality standards required across end-use industries.

The LCD Glass Substrate market comprises ultra-thin glass, standard-thickness glass, flexible glass, and chemically strengthened glass types, each catering to specific display requirements. Ultra-thin glass dominates due to its lightweight nature and compatibility with high-resolution smartphone and wearable displays, enabling manufacturers to produce slimmer devices while maintaining durability. Flexible glass is the fastest-growing type, driven by the rising demand for foldable devices and curved automotive displays, providing flexibility without compromising clarity or mechanical strength. Standard-thickness glass remains essential for television and monitor panels due to its cost-effectiveness and reliable mechanical stability in large-size panels. Chemically strengthened glass retains niche relevance in applications requiring additional impact resistance, particularly in rugged industrial and automotive display systems. This diverse product landscape allows manufacturers to tailor substrate production based on end-user needs, enhancing market responsiveness while maintaining efficiency in production lines.

Applications in the LCD Glass Substrate market include smartphones, televisions, automotive displays, industrial monitors, and medical devices, each contributing to the demand for high-quality display substrates. Smartphones are the leading application due to the ongoing demand for high-resolution, lightweight displays that support advanced touch functionalities. Automotive displays are the fastest-growing application area, driven by the increasing use of digital instrument clusters, head-up displays, and infotainment systems requiring high-brightness, durable glass substrates capable of withstanding temperature fluctuations. Televisions maintain a significant share within the application landscape due to steady consumer demand for large-format, high-definition displays. Industrial monitors and medical visualization devices also contribute by requiring substrates with enhanced clarity, color accuracy, and durability, supporting mission-critical operations across various industries.

End-users in the LCD Glass Substrate market include electronics manufacturers, automotive OEMs, healthcare equipment providers, and industrial display integrators, reflecting the extensive integration of advanced display technologies across sectors. Electronics manufacturers lead in substrate consumption, leveraging high-quality glass for smartphones, tablets, laptops, and televisions to meet consumer expectations for lightweight, high-resolution devices. Automotive OEMs are the fastest-growing end-user segment, driven by the integration of advanced displays in vehicle dashboards and infotainment systems that require durable, high-brightness substrates for enhanced user experience and safety features. Healthcare equipment providers use high-clarity substrates for medical imaging and monitoring systems, ensuring accurate diagnostics and patient monitoring. Industrial display integrators utilize substrates for equipment that demands reliability and clear visualization, including factory monitoring systems and rugged outdoor displays, contributing to the consistent demand within the LCD Glass Substrate market.

Asia-Pacific accounted for the largest market share at 62.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

The Asia-Pacific region, led by China, Japan, and South Korea, remains the global hub for the LCD Glass Substrate Market, driven by high-volume manufacturing capabilities, advanced fabrication infrastructure, and strong demand across smartphones, televisions, and automotive displays. North America’s growth outlook is supported by rising demand for automotive HUDs, medical visualization displays, and premium large-format monitors, coupled with the region’s initiatives toward reshoring advanced electronics manufacturing. Technological advancements in ultra-thin substrate production and energy-efficient display manufacturing, paired with regional environmental directives promoting low-emission production methods, are enhancing regional consumption patterns in the LCD Glass Substrate Market. As smart device penetration and industrial automation grow, these regions continue to shape production priorities and consumption trends in the LCD Glass Substrate Market.

Strategic Growth in Advanced Display Manufacturing Driving Market Potential

The LCD Glass Substrate Market in this region held a market share of 13.5% in 2024, driven by the rising adoption of high-resolution display panels in automotive, consumer electronics, and healthcare sectors. Demand is fueled by industries manufacturing advanced infotainment systems and medical diagnostic displays requiring ultra-thin, durable substrates. Regulatory frameworks encouraging domestic semiconductor and display manufacturing, including government funding initiatives for advanced electronics, are supporting local production capacity. Technological advancements such as AI-enabled defect detection systems and precision substrate handling robotics are being integrated into production facilities, enabling efficient manufacturing and quality consistency in the LCD Glass Substrate Market. The focus on digital transformation and Industry 4.0 in fabrication plants is also optimizing energy usage and operational efficiency across production lines.

Emerging Trends in Eco-Friendly Display Substrate Production

The LCD Glass Substrate Market in this region accounted for 11.2% of the global market share in 2024, with Germany, France, and the UK leading in demand due to their strong electronics and automotive manufacturing bases. Regulatory bodies within the EU are actively promoting sustainable and energy-efficient manufacturing processes, encouraging producers to adopt low-emission technologies in substrate fabrication. The adoption of advanced thin-glass technologies for high-resolution displays in automotive dashboards and medical devices is notable across European markets. Additionally, the push toward recycling and using eco-friendly materials in substrate production aligns with the EU’s Green Deal objectives, influencing manufacturers within the LCD Glass Substrate Market to invest in greener technologies while meeting performance standards in display panels.

High-Volume Manufacturing Dominance Supporting Market Leadership

The LCD Glass Substrate Market in this region maintains the highest volume globally, with China, Japan, and South Korea collectively driving over 60% of substrate consumption in 2024. China’s continued investment in Gen 10.5 and Gen 11 production lines enables scalable manufacturing of large-format display panels for televisions and commercial screens, while Japan and South Korea focus on high-quality, ultra-thin substrate development for advanced consumer electronics and automotive displays. Regional trends highlight investments in smart factories using AI-powered inspection systems and robotic handling solutions to enhance productivity and reduce defect rates. Innovation hubs within the region are also focusing on flexible and foldable substrate technologies, aligning with rising demand in the smartphone and wearable markets and maintaining Asia-Pacific’s leadership in the LCD Glass Substrate Market.

Expanding Opportunities with Rising Electronics Assembly Demand

The LCD Glass Substrate Market in this region is witnessing notable traction in Brazil and Argentina, which are key countries driving demand due to the growth of local electronics assembly and automotive industries. The region accounted for a 4.3% market share in 2024, supported by government incentives promoting local manufacturing and reduced import dependency for electronic components. Infrastructure development projects and the increasing adoption of advanced automotive infotainment systems are further supporting substrate demand. The energy sector’s modernization efforts, including smart grid displays, are also influencing the regional substrate market, while trade agreements and reduced tariffs on electronic components contribute to the favorable environment for expanding LCD Glass Substrate Market operations within the region.

Industrial Modernization Fueling Display Substrate Demand

The LCD Glass Substrate Market in this region is supported by the growing demand for display solutions in industrial automation, healthcare, and consumer electronics sectors, with the UAE and South Africa leading consumption in 2024. The market reflects regional modernization initiatives, including the development of smart healthcare systems and automotive digital dashboard integrations, increasing demand for durable, high-resolution display substrates. Trade partnerships and incentives promoting advanced manufacturing and technology adoption are further supporting the regional expansion of the LCD Glass Substrate Market. Local regulations focusing on technological integration in industrial sectors are enabling the adoption of high-quality substrates for mission-critical display applications, aligning with broader digital transformation strategies across these markets.

China (42.6%) – High production capacity with advanced Gen 10.5 and Gen 11 lines enabling large-scale substrate manufacturing.

South Korea (16.3%) – Strong end-user demand across smartphones and automotive displays supported by continuous R&D in ultra-thin glass substrate technologies.

The LCD Glass Substrate market is characterized by a competitive environment with over 20 active global competitors operating across Asia-Pacific, North America, and Europe. Leading manufacturers are focusing on technological innovations such as ultra-thin substrate processing, defect-free surface treatment, and Gen 10 and Gen 11 large-area substrate production to strengthen their market positioning. Strategic initiatives including joint ventures with panel manufacturers and the establishment of localized production facilities are enhancing supply chain agility while reducing delivery timelines for clients. The market has seen several notable product launches, including advanced flexible glass substrates designed for foldable smartphones and automotive displays, which are creating differentiation among competitors. Mergers and partnerships are also shaping the landscape as companies seek to integrate AI-enabled inspection systems and robotics for automated handling, ensuring quality consistency while reducing operational downtime. Additionally, investment in sustainable manufacturing practices and recycling technologies is gaining traction as environmental regulations tighten, pushing competitors to innovate while aligning with customer sustainability objectives in the LCD Glass Substrate market.

Corning Incorporated

AGC Inc.

Nippon Electric Glass Co., Ltd.

Shenzhen Laibao Hi-Tech Co., Ltd.

AvanStrate Inc.

IRICO Group New Energy Co., Ltd.

Tunghsu Optoelectronic Technology Co., Ltd.

NEG Technology Co., Ltd.

XinYi Glass Holdings Limited

Plan Optik AG

The LCD Glass Substrate Market is advancing through the integration of ultra-thin glass processing, precision edge grinding, and advanced annealing technologies to support high-resolution displays in smartphones, televisions, and automotive panels. Manufacturers are deploying 0.3 mm and thinner substrates while maintaining structural integrity for foldable and curved display applications, with ultra-slim glass technologies expanding capacity in premium device production. Gen 10 and Gen 11 substrate production lines are enabling the efficient manufacturing of large-format displays by allowing multiple 65-inch and 75-inch panels to be cut from a single substrate, improving production yields while reducing waste.

AI-powered defect inspection systems are being adopted across substrate manufacturing lines, improving detection accuracy for micro-level surface inconsistencies, leading to up to a 40% reduction in inspection times. Robotic automation in substrate handling and transportation is reducing microcrack risks during processing while enhancing operational efficiency. Chemically strengthened glass substrates are being utilized for applications requiring enhanced impact resistance in industrial and automotive displays. The LCD Glass Substrate Market is also witnessing advancements in hybrid OLED-LCD backplane integration, allowing cost-effective OLED production using LCD substrate infrastructure. Additionally, manufacturers are adopting environmentally conscious etching and coating processes, reducing emissions and water usage, aligning technological innovation with sustainability goals while ensuring the delivery of high-quality substrates to diverse end-use industries.

• In March 2023, Corning launched its ultra-slim 0.3 mm LCD glass substrate line for next-generation foldable smartphones, enhancing flexibility while maintaining clarity and mechanical stability, with initial production capacities of 20 million square meters annually to support expanding OEM demand.

• In July 2023, AGC Inc. announced the installation of a new Gen 11 substrate manufacturing line in China, enabling the production of large-format panels up to 85 inches, aligning with the increasing demand for high-definition televisions and commercial displays in Asia-Pacific markets.

• In February 2024, Nippon Electric Glass introduced an advanced AI-powered inspection system across its LCD glass substrate lines, reporting a 38% reduction in defect detection time and an improvement in substrate yield rates by 4.5%, enhancing operational efficiency across its manufacturing network.

• In May 2024, Shenzhen Laibao Hi-Tech commenced production of hybrid OLED-LCD glass substrates, leveraging existing LCD infrastructure to supply cost-effective OLED panels to smartphone and wearable manufacturers, with a reported output capacity of 15 million units annually in the first operational phase.

The LCD Glass Substrate Market Report covers a comprehensive analysis of type, application, end-user, and regional segments with clear numerical insights, addressing current and emerging trends impacting the market. It evaluates ultra-thin glass, flexible substrates, and standard-thickness substrates used across consumer electronics, automotive displays, industrial monitoring systems, and healthcare visualization devices. The report explores the strategic importance of Gen 8 and above production lines in enabling large-format panel manufacturing and investigates the role of AI-driven inspection systems and robotic automation in enhancing substrate quality and operational efficiency.

Geographically, the report examines market dynamics in Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, focusing on their infrastructure developments, manufacturing capacities, and regulatory environments. It highlights the role of leading consumption regions such as China, Japan, South Korea, the United States, and Germany in shaping demand trends while addressing growth opportunities in emerging markets.

The report further explores technological innovations in surface treatment, annealing, and etching processes, including the integration of hybrid OLED-LCD technologies. It outlines the competitive landscape, profiling key market players, and analyzing their strategic initiatives, product advancements, and expansion plans. The LCD Glass Substrate Market Report serves as a critical decision-making tool for stakeholders evaluating opportunities within this market, enabling strategic planning aligned with evolving industry demands and technological trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 8558.98 Million |

|

Market Revenue in 2032 |

USD 11894.99 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Corning Incorporated, AGC Inc., Nippon Electric Glass Co., Ltd., Shenzhen Laibao Hi-Tech Co., Ltd., AvanStrate Inc., IRICO Group New Energy Co., Ltd., Tunghsu Optoelectronic Technology Co., Ltd., NEG Technology Co., Ltd., XinYi Glass Holdings Limited, Plan Optik AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |