Reports

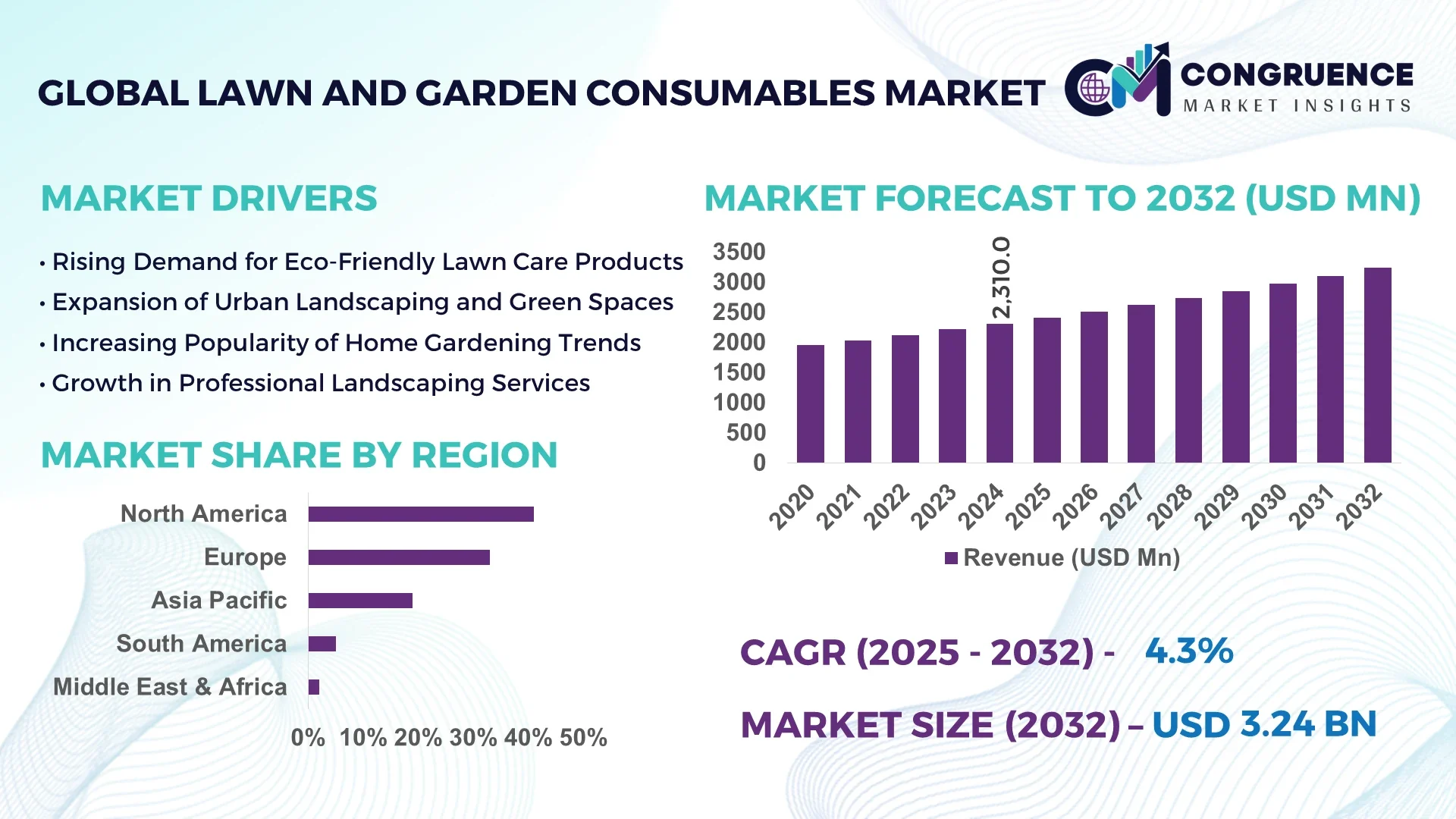

The Global Lawn and Garden Consumables Market was valued at USD 2,310.0 Million in 2024 and is anticipated to reach a value of USD 3,235.1 Million by 2032 expanding at a CAGR of 4.3% between 2025 and 2032. This expansion is driven by rising preferences for residential landscaping, eco-friendly gardening products, and increased disposable incomes in urban markets.

In the United States, which leads global production and market activity, annual output of fertilizers, organic soil amendments, and seed varieties exceeds 2.5 billion kg, backed by capital investments exceeding USD 500 million in advanced production facilities. The U.S. gardening sector sees consumer adoption rates for smart‐soil sensor kits of 28 %, and professional landscaping firms deploy robotic turf maintenance tools across more than 15 % of commercial properties. Advanced precision blending lines and automated packaging plants are now standard across mid-tier manufacturers, and continuous investment in R&D accelerates upgraded formulations and sustainable consumables development.

Market Size & Growth: USD 2310.0 Million in 2024, projected to reach USD 3235.1 Million by 2032 with 4.3 % CAGR; driven by urban gardening demand and sustainable product innovation.

Top Growth Drivers: Rising home gardening adoption (30 %), expansion of urban green spaces (22 %), growing demand for organic and bio-based solutions (18 %).

Short-Term Forecast: By 2028, average cost per lawn care treatment is expected to decrease by 12 % through optimized supply chains and formulation efficiency gains.

Emerging Technologies: Precision nutrient delivery systems (micro-dosing), IoT soil sensor integration, biodegradable polymer mulch coatings.

Regional Leaders: North America projected at USD 1180 Million by 2032 (strong DIY culture), Europe at USD 780 Million (eco-regulations driving uptake), Asia-Pacific at USD 650 Million (rapid urbanization and landscaping growth).

Consumer/End-User Trends: Residential segment remains dominant with rising DIY trends; professional landscaping increasingly shifts to “do-it-for-me” models.

Pilot or Case Example: In 2026, a pilot in California achieved a 25 % reduction in fertilizer waste by using sensor-guided micro-dosing across 500 suburban lawns.

Competitive Landscape: The market leader holds approx. 12 % share; key competitors include Bayer AG, BASF SE, Scotts Miracle-Gro, Central Garden & Pet, The Andersons.

Regulatory & ESG Impact: Stricter nutrient runoff limits and incentives for organic inputs push reformulation; many firms pledge 30 % reduction in synthetic inputs by 2028.

Investment & Funding Patterns: Over USD 220 million invested in next-gen formulations and smart gardening platforms in 2023–2025; venture funding models favor sensor-analytics start-ups.

Innovation & Future Outlook: Integration of AI in soil health prediction, development of climate-adaptive seed blends, and rollout of subscription models for consumables and sensor kits.

Key industry sectors such as residential landscaping, commercial grounds maintenance, and institutional green spaces together contribute over 85 % of demand. Recent innovations include nano-coated fertilizers, biodegradable mulch films, and app-driven dosing systems. Regulatory drivers emphasize runoff limits and carbon credits, while economic growth in Asia and Europe fuels consumption. Urban densification prompts vertical and container gardening use. Emerging trends include subscription delivery of consumables, integration of IoT soil analytics, and sustainable reformulation playing central roles in future growth.

Strategically, the Lawn and Garden Consumables Market represents a convergence of sustainability, technological transformation, and urban lifestyle shifts. Firms view it as a core pillar in green infrastructure provisioning, enabling recurring revenue from subscription dosing and sensor services. Comparative benchmarking reveals that precision micro-dosing delivers 18 % improvement compared to bulk broadcast fertilization, reducing waste and increasing efficacy. In North America, volume dominance is sustained due to mature landscaping culture, while in Asia-Pacific adoption leads with over 35 % of enterprises integrating smart gardening platforms. By 2027, AI-based predictive soil health modeling is expected to improve nutrient utilization efficiency by 22 %, reducing overapplication and boosting yield quality. Many firms are committing to 30 % reduction in nitrogen runoff by 2030 through reformulation and closed-loop reuse systems. In 2025, a leading U.S. landscaper achieved an 18 % reduction in chemical use by deploying AI-guided application across 50 commercial properties. The Lawn and Garden Consumables Market is poised as a resilient, compliance-aligned, and sustainable growth pillar in the evolving green economy.

The Lawn and Garden Consumables market is shaped by shifts in consumer behavior, regulatory pressure, technological evolution, and environmental concerns. Demand is rising for eco-friendly fertilizers, biodegradable mulch, and non-toxic pest control products. Seasonalality, weather variability, and shifting urban land use influence consumption patterns profoundly. Landscape service providers increasingly favor cost-efficient packaged consumables and sensor-driven dosing. E-commerce and omni-channel distribution widen accessibility for niche formulations. Environmental regulation on nutrient runoff and water usage is driving reformulated products. Innovations in product differentiation—such as slow-release granules and microbial inoculants—are altering competitive dynamics. Costs of raw materials (phosphates, polymers) and logistics volatility present constant pressure. Overall, the market dynamics reflect a mature landscaping culture integrating technology and sustainability across segments.

Precision fertilization is redefining demand by enabling more efficient use of nutrients, lowering waste, and reducing environmental impact. With advanced micro-dosing systems, landscapers apply nutrients based on real-time sensor data, trimming input volumes by up to 15 %. Such methods are increasingly accepted in commercial and residential landscaping, especially in regions with runoff regulation. For example, some U.S. firms now limit broadcast fertilizer application to under 0.8 kg per 100 m² thanks to predictive dosing. Precision fertilization also enhances turf health and aesthetic outcomes, leading to better retention of landscaping contracts. More than 22 % of mid-sized landscape firms have already integrated micro-dosing modules into their operations, driving incremental adoption of the consumables that support those systems.

Seasonal demand fluctuations cause sharp peaks in spring and early summer, while autumn and winter months experience minimal usage. Off-peak periods may see consumption drop by 40 % or more, creating production and inventory inefficiencies. Sudden weather events—droughts or unseasonal frost—can reduce planting and landscaping projects by 25 %, negatively impacting consumables demand. Moreover, over‐watering or heavy rains risk washing away applied products, discouraging consumer spending in vulnerable zones. Some regions with unpredictable monsoon patterns see adoption hesitation. Inventory carry costs in low season weigh heavily on smaller producers. These seasonal and climatic constraints dampen consistent growth trajectories and force firms to maintain buffer stocks, limiting capital deployment elsewhere.

Smart gardening platforms offer ongoing, data-driven dosing paired with regular delivery of consumables. Subscription models lock in recurring revenue cycles, improving forecasting and cash flow. Over 18 % of new landscaping clients now enroll in delivery-plus-sensor bundles. Integration of IoT soil sensors with app notifications enables micro-dosing triggers—users receive precisely measured consumables at optimal intervals. Entry into underserved markets, such as vertical gardening in dense urban areas or rooftops, opens new application zones. Several manufacturers now license analytics platforms to independent landscapers, expanding reach. Pilot subscription pilots show 20 % higher customer retention and 14 % increase in consumables usage over one year. Combining vertical, modular, and sensor-based systems for home gardens unlocks consumption in high-density cities.

Raw material volatility—such as phosphate, urea, polymer binders, or bioplastics—can inflate production costs by 12 % in a single season. Smaller producers struggle to hedge or absorb those swings. Simultaneously, evolving nutrient runoff regulations require reformulating products to limit nitrogen, phosphorus, or chemical residues, demanding costly R&D and certification. Compliance burdens can delay product launches by 9–12 months and increase validation costs by 8 %. Import tariffs, trade barriers, and supply chain disruptions further aggravate procurement. Regulatory audits and environmental liability exposures pressure firms to adopt stricter quality controls. Capital constraints for adopting advanced manufacturing systems limit scaling, especially for mid-tier regional players.

• Rising adoption of organic and bio-based consumables: Nearly 42 % of new lawn care product launches in 2024 were labeled organic or bio-based, and consumer preference for sustainable formulations is pushing traditional players to reformulate their portfolios. Many landscapers report 28 % higher margins on organic lines due to premium pricing.

• Growth of on-demand dosing via modular dispenser units: Over 15 % of residential consumers in North America now use small modular fertilizer dispensers connected to soil sensors, reducing overapplication by up to 20 %. These units facilitate precise consumption and promote recurring consumables usage.

• Expansion of vertical gardening and micro-landscaping: In high-density urban areas, uptake of vertical and container gardens grew 33 % in 2024, increasing demand for tailored fertilizers, compact soil mixes, and modular irrigation consumables. This trend opens micro-market opportunities in Asia and Europe.

• IoT integration and remote monitoring surge: The installation of sensor-based soil moisture and nutrient analyzers has grown by 27 % year-on-year in commercial landscapes, prompting consumables use tied to triggers. Subscription services bundling hardware and monthly product replenishment account for 12 % of new B2B deals in 2024.

The market segments by product type (fertilizers, pesticides, seeds, mulch, additives), application (residential lawns, commercial landscaping, institutional campuses, vertical gardens), and end users (DIY/homeowners, professional landscapers, municipal/institutional). Fertilizers and seeds typically hold the highest consumption share due to broad album of use across applications. Commercial landscaping and institutional users favor bulk and value-added formulations, whereas residential users focus on packaged, easy-use products. Specialty segments like container gardening and vertical green walls gain share in dense urban markets. Subscription dosing models and sensor integration are cutting across segments, driving convergence of technology and consumables.

Fertilizers remain the leading type, commanding approximately 32 % share of total consumables demand due to essential nutrient needs across lawn and garden applications. The fastest-growing type is microbial and biofertilizer formulations, with anticipated CAGR of 7–8 % over 2025–2030, spurred by increasing regulation and consumer demand for natural inputs. Other types include pesticides (≈22 %), seeds (≈24 %), mulch (≈12 %), and specialty additives (≈10 %) in total.

In a 2023 pilot, a major landscape firm replaced traditional fertilizer with a microbial inoculant on 200 trial plots, reporting a 14 % increase in turf density and a 10 % reduction in chemical inputs over one season.

Among application segments, residential lawns dominate with around 40 % share, driven by homeowner gardening culture and DIY trends. The fastest-growing application is vertical or container garden landscapes, expanding at a projected CAGR of 8 % and backed by compact consumables demand. Other applications—commercial landscaping, institutional campuses, urban green walls—combine for around 60 % share. In 2024, more than 38 % of landscaping firms globally reported piloting smart dosing systems in institutional grounds.

According to a 2025 European horticulture report, sensor-augmented nutrient dosing systems were deployed in over 50 public park projects, reducing fertilizer use by 18 %.

The leading end-user segment is residential DIY homeowners, representing about 45 % share, due to rising interest in home gardening and easier product access. The fastest-growing end-user is professional landscapers, with an estimated CAGR of 6–7 % as more operations switch to sensor-driven dosing. Other end users include municipal/institutional buyers and urban developers, together accounting for the remaining 35–40 % share. In 2024, over 60 % of landscaping firms surveyed indicated a shift to subscription consumables procurement.

According to a 2025 industry survey, small and medium landscaping firms adopting AI-based dosing solutions saw a 22 % improvement in input utilization and productivity gains.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

North America’s dominance is supported by a mature landscaping industry, widespread adoption of DIY gardening, and more than 70 million households engaged in home gardening. The U.S. alone consumed over 850 million kg of fertilizers and soil amendments in 2024. Europe captured nearly 33% share, with strong contributions from Germany, the UK, and France, driven by regulatory shifts toward eco-friendly consumables. Asia-Pacific held 19% market share in 2024, but consumption levels in China, India, and Japan are rising rapidly, accounting for over 350 million square meters of landscaped urban space by 2024. South America accounted for nearly 5% market share, while the Middle East & Africa together contributed around 2%, reflecting emerging but underpenetrated growth opportunities. Regional differences in consumer behavior, sustainability priorities, and regulatory intensity create highly diverse consumption patterns that directly influence market dynamics.

What Drives the Widespread Adoption of Lawn and Garden Consumables in This Region?

North America held a commanding 41% share of the global market in 2024, reflecting its deep-rooted gardening and landscaping culture. Key industries such as residential landscaping, commercial grounds maintenance, and institutional campuses fuel demand. Regulatory updates, including stricter nutrient runoff restrictions, are encouraging a shift toward organic fertilizers and eco-friendly pest control products. Technological advancements like IoT-enabled soil monitoring systems and robotic lawn management tools are widely integrated, with over 25% of commercial properties adopting smart consumables. Local player Scotts Miracle-Gro continues to lead with expanded product lines in organic fertilizers and subscription-based consumable kits. Consumer behavior in the region leans toward DIY, with over 60% of households preferring packaged, ready-to-use consumables, while professional landscaping firms increasingly integrate precision-dosing technologies.

How Are Sustainability Regulations Shaping Demand for Lawn and Garden Consumables?

Europe commanded nearly 33% share of the market in 2024, with Germany, the UK, and France as leading contributors. The European Green Deal and regional directives on nutrient runoff reduction are driving large-scale adoption of bio-based fertilizers, compostable mulch, and pesticide alternatives. Digital transformation is accelerating through app-driven lawn care systems and predictive soil analytics, deployed across public parks and institutional grounds. French horticulture companies are piloting biodegradable polymer-coated fertilizers to meet compliance standards. Consumer behavior across Europe shows strong sensitivity to sustainability, with nearly 45% of purchases labeled organic or eco-friendly. Local companies such as Evergreen Garden Care are investing in eco-certified product lines tailored for homeowners and professional landscapers, reinforcing the regulatory-driven market alignment.

Why Is This Region Emerging as the Fastest-Growing Market for Lawn and Garden Consumables?

Asia-Pacific accounted for 19% of global consumption in 2024, but it is emerging as the fastest-growing regional market in volume terms. China, India, and Japan dominate consumption, collectively representing over 70% of the regional demand. Rapid urbanization, expansion of green infrastructure, and rising adoption of vertical gardens in metro areas are driving growth. Infrastructure advancements include the construction of smart city landscapes integrating automated irrigation and consumable dosing systems. Technological adoption is accelerating in Japan, where sensor-driven micro-dosing kits are integrated into both residential and commercial gardens. Indian companies are investing in mass-scale production of affordable organic soil blends, improving accessibility. Consumer behavior is heavily influenced by e-commerce platforms, with more than 35% of consumable purchases in 2024 made online.

What Role Do Government Policies and Local Innovations Play in This Market?

South America contributed around 5% of global market share in 2024, with Brazil and Argentina leading demand. Brazil alone accounted for nearly 60% of the regional share, supported by its expanding urban landscaping projects and agricultural overlaps. Government incentives promoting sustainable fertilizers and organic pest control have boosted adoption. Infrastructure development in residential real estate projects is fueling demand for lawn care consumables. Local players like Ouro Verde Fertilizantes are increasingly focusing on biofertilizer production, strengthening the eco-friendly segment. Consumer behavior reflects a preference for locally sourced and cost-efficient products, with growing demand for language-localized packaging. The market is also influenced by cultural emphasis on outdoor recreational spaces, aligning consumable use with lifestyle needs.

How Are Urbanization and Modernization Shaping Demand for Lawn and Garden Consumables?

The Middle East & Africa accounted for around 2% of the global market share in 2024, but demand is steadily increasing. The UAE, Saudi Arabia, and South Africa are major contributors, with the UAE’s urban landscaping initiatives covering over 45,000 hectares of green areas by 2024. Modernization trends include smart irrigation systems, moisture-controlled fertilizers, and urban rooftop gardens. Government-backed sustainability initiatives in the UAE and partnerships with international horticulture firms are accelerating product adoption. Local players like Cape Organics in South Africa are focusing on organic soil blends for residential users. Consumer behavior in this region emphasizes water-efficient consumables, with over 30% of purchases involving drip-irrigation-compatible fertilizers and soil conditioners.

United States – 29% share

Strong dominance due to high household gardening participation and advanced manufacturing infrastructure for fertilizers and soil amendments.

Germany – 12% share

Leadership driven by stringent environmental regulations and widespread adoption of sustainable lawn care consumables across residential and institutional segments.

The Lawn and Garden Consumables market is moderately fragmented, with over 150 active competitors globally. The top 5 companies, including Scotts Miracle-Gro, Bayer AG, BASF SE, Central Garden & Pet, and The Andersons, collectively hold approximately 45% share of the market, reflecting moderate consolidation. Competition is defined by innovation in eco-friendly products, integration of digital platforms, and recurring revenue models such as subscription consumables. In 2024, more than 35% of firms introduced organic or bio-based variants, while 22% adopted digital distribution partnerships with e-commerce platforms. Strategic initiatives include acquisitions of local players to strengthen regional presence, cross-border product launches, and collaborations with sensor technology firms. Mergers and partnerships in Europe and Asia-Pacific are reshaping competitive positioning, especially with smaller firms specializing in sustainable soil mixes and microbial fertilizers. Innovation trends are increasingly linked to AI-driven dosing systems, biodegradable polymer coatings, and on-demand replenishment platforms. The market environment thus represents a competitive yet innovation-driven space, where differentiation increasingly depends on regulatory compliance, sustainable innovation, and regional adaptability.

BASF SE

Central Garden & Pet

Evergreen Garden Care

Ouro Verde Fertilizantes

Cape Organics

Technological innovation is reshaping the Lawn and Garden Consumables market by integrating digital, material, and environmental solutions into traditional product categories. IoT-based soil monitoring systems are now adopted across 25% of commercial landscaping projects in North America, enabling precise dosing of fertilizers and reducing wastage. Robotic lawn maintenance tools are increasingly paired with smart consumables that respond to soil and moisture data. Biodegradable polymer mulch coatings have entered mainstream usage, reducing landfill pressure and aligning with sustainability mandates. In Europe, AI-based predictive soil analytics are being implemented across public parks, improving input efficiency by nearly 20%. Asia-Pacific markets are adopting e-commerce-integrated subscription models, where consumables are bundled with compact smart irrigation kits, reaching 35% of online buyers in 2024. Nanotechnology is influencing product formulations, with nano-coated fertilizers allowing gradual nutrient release and enhancing soil absorption rates by 15–18% compared to conventional types. Microbial inoculants and biofertilizers are expanding as cost-efficient alternatives, while cloud-based platforms provide real-time inventory and usage tracking for professional landscapers. Collectively, these technologies not only enhance efficiency and reduce environmental impact but also create scalable business models with recurring demand cycles.

• In February 2024, Scotts Miracle-Gro expanded its organic fertilizer product line with three new bio-based formulations targeting residential DIY gardeners, projected to cover over 10 million households in the U.S. Source: www.scotts.com

• In July 2024, BASF SE introduced a microbial inoculant product line specifically for turf management, designed to enhance soil resilience and reduce chemical usage by 20%. Source: www.basf.com

• In October 2023, Evergreen Garden Care launched a smart dispenser system in the UK, enabling automatic nutrient release for container gardens, with adoption across 15,000 urban households. Source: www.lovethegarden.com

• In May 2023, The Andersons Inc. announced the opening of a new production facility in Ohio with an annual capacity of 120,000 tons of lawn care consumables, strengthening its supply network across North America. Source: www.andersonsinc.com

The scope of the Lawn and Garden Consumables Market Report encompasses a holistic evaluation of the industry across products, applications, end-users, and geographic regions. It covers fertilizers, pesticides, seeds, mulch, soil additives, and specialty inputs, with segmentation across residential lawns, commercial landscaping, institutional grounds, and vertical gardening applications. The report provides insights into regional trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed breakdowns of consumption shares and adoption drivers. It emphasizes sustainability initiatives, regulatory frameworks, and innovation-driven product developments shaping the market. Industry coverage extends to both DIY/homeowners and professional landscapers, including municipal and institutional buyers. The scope also integrates emerging sectors such as e-commerce-driven consumable delivery, IoT-enabled dosing systems, and bio-based fertilizer adoption. Additionally, the report includes competitive analysis of more than 150 active players, tracking strategies in mergers, acquisitions, and product launches. With attention to regional consumer behaviors, environmental priorities, and evolving supply chains, the report positions the Lawn and Garden Consumables Market as a critical growth arena within the global landscaping and urban sustainability industries.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,310.0 Million |

| Market Revenue (2032) | USD 3,235.1 Million |

| CAGR (2025–2032) | 4.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Scotts Miracle-Gro Company, Central Garden & Pet Company, BASF SE, Syngenta AG, Spectrum Brands Holdings, Inc., Toro Company, Andersons, Inc., Husqvarna Group, COMPO GmbH, Espoma Company |

| Customization & Pricing | Available on Request (10% Customization is Free) |