Reports

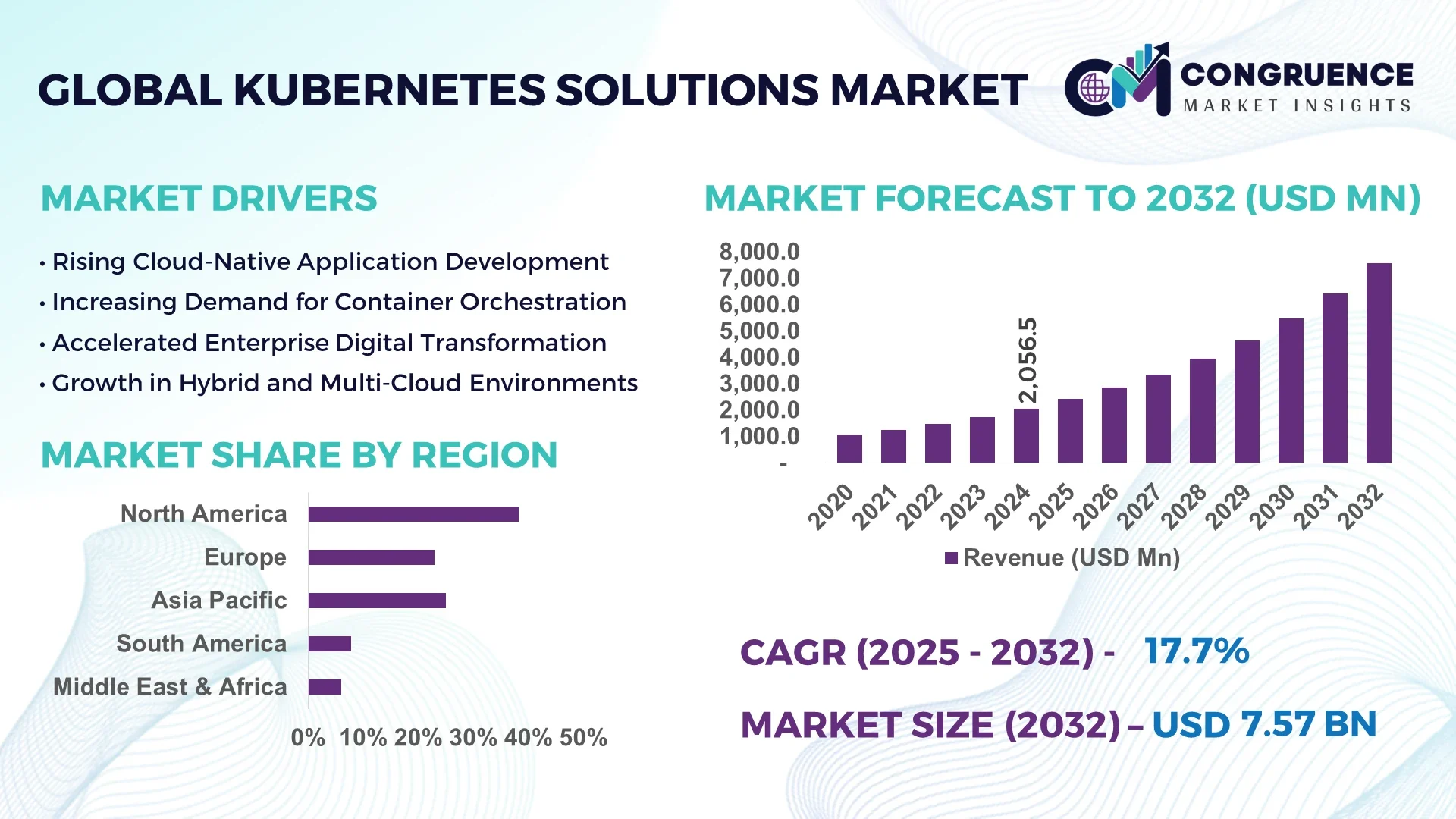

The Global Kubernetes Solutions Market was valued at USD 2,056.45 Million in 2024 and is anticipated to reach a value of USD 7,574.09 Million by 2032 expanding at a CAGR of 17.7% between 2025 and 2032.

In the United States, the Kubernetes Solutions market has seen significant momentum driven by advanced container orchestration capabilities and robust IT infrastructure. U.S.-based enterprises are investing heavily in microservices architecture, leading to widespread adoption of containerized applications across sectors like finance, healthcare, and telecommunications.

The Kubernetes Solutions Market continues to evolve rapidly, driven by the widespread adoption of hybrid cloud strategies and the increasing need for scalable infrastructure management. Enterprise-grade Kubernetes platforms are being adopted across industries such as banking, insurance, e-commerce, and manufacturing, where containerization enables agility and faster deployment cycles. Notable developments include Kubernetes-native security solutions, policy enforcement automation, and GitOps workflows. Regulatory frameworks like GDPR and sector-specific data compliance rules are shaping deployment approaches globally. Meanwhile, environmental concerns are pushing organizations to adopt more energy-efficient infrastructure models via Kubernetes optimization. Additionally, consumption patterns in Asia-Pacific and Latin America are shifting as small and mid-sized businesses increasingly implement managed Kubernetes services. Cloud-native application modernization, coupled with the rising influence of open-source development communities, is reinforcing long-term market growth. The future outlook remains highly promising with innovations in service mesh integration, multi-cloud observability, and edge computing solutions underpinned by Kubernetes orchestration.

Artificial Intelligence (AI) is profoundly reshaping the Kubernetes Solutions Market by enabling more intelligent workload management, reducing human intervention, and optimizing cluster performance. AI-powered automation tools are becoming integral to Kubernetes operations, particularly for predictive scaling, self-healing systems, and anomaly detection. By leveraging machine learning algorithms, organizations can dynamically allocate computing resources based on real-time demand, significantly minimizing latency and improving infrastructure utilization. These innovations are especially valuable in industries managing mission-critical workloads, such as digital banking and telemedicine, where system downtime is not an option.

Within the Kubernetes Solutions Market, AI is driving advancements in observability and diagnostics. Intelligent monitoring tools powered by AI allow DevOps teams to proactively detect failures, troubleshoot complex issues, and generate actionable insights. This leads to more efficient root cause analysis and reduces mean time to resolution (MTTR). In managed Kubernetes environments, AI supports policy-driven governance and compliance auditing by continuously scanning clusters for configuration drifts and security threats. This contributes to enhanced enterprise-grade Kubernetes deployments with better security postures and operational transparency.

Moreover, AI facilitates improved DevSecOps integration by automating CI/CD pipelines and enhancing container security through behavior-based threat detection. These enhancements are enabling organizations to accelerate innovation cycles while maintaining stringent security standards. As AI continues to evolve, its role within the Kubernetes Solutions Market is expected to deepen further, offering unprecedented levels of scalability, automation, and resilience in containerized application management.

"In January 2025, a leading Kubernetes platform provider integrated AI-based workload profiling into its managed service, enabling clients to reduce average CPU consumption by 23% and memory usage by 18% across cloud-native workloads, thereby improving resource efficiency without manual tuning."

The widespread shift toward cloud-native infrastructures is a key growth catalyst in the Kubernetes Solutions Market. Enterprises are migrating legacy systems to cloud platforms and adopting containerization to enhance scalability and reduce deployment time. Kubernetes, being a de facto standard for container orchestration, is central to this transformation. According to recent industry data, over 85% of organizations running containers are using Kubernetes in production environments. Major enterprises are leveraging Kubernetes to manage thousands of containers seamlessly across distributed cloud environments. The push for continuous integration and delivery (CI/CD), coupled with the rising popularity of microservices, is amplifying the need for agile orchestration tools, thereby positioning Kubernetes Solutions as an operational necessity in modern IT infrastructure.

Despite its benefits, the Kubernetes Solutions Market faces hurdles due to the inherent complexity of deploying and maintaining Kubernetes clusters. Many enterprises, particularly small to mid-sized organizations, lack the in-house expertise to manage these systems efficiently. Issues such as configuring persistent storage, network policies, role-based access control, and security patches require specialized knowledge. Studies show that 65% of Kubernetes users cite complexity as a significant barrier to scaling their deployments. The absence of standardized practices across multi-cloud Kubernetes implementations further exacerbates the problem, often resulting in misconfigurations and reduced performance. This complexity discourages adoption among businesses without dedicated DevOps or platform engineering teams.

A compelling opportunity in the Kubernetes Solutions Market lies in the convergence of edge computing and AI workloads. As industries deploy intelligent applications closer to data sources—such as sensors, IoT devices, and 5G infrastructure—the demand for lightweight, portable orchestration platforms is rising. Kubernetes is being optimized to function efficiently in resource-constrained edge environments, enabling dynamic workload distribution across decentralized nodes. Furthermore, the ability of Kubernetes to orchestrate GPU-accelerated workloads is drawing attention from AI-driven enterprises. Market data indicates increasing adoption of Kubernetes in autonomous systems, smart factories, and AI-based healthcare diagnostics. These expanding use cases present untapped potential for Kubernetes providers to offer tailored solutions for real-time, edge-based, and AI-integrated deployments.

One of the major challenges confronting the Kubernetes Solutions Market is the persistent skills shortage in Kubernetes administration and DevOps practices. As demand for Kubernetes escalates, organizations face difficulty in recruiting and retaining professionals skilled in Kubernetes architecture, cluster security, Helm chart management, and CI/CD pipeline integration. Surveys report that over 40% of organizations cite limited internal expertise as a bottleneck to scaling Kubernetes infrastructure. This scarcity leads to increased reliance on managed services and third-party consultants, raising operational costs and limiting the scope of internal innovation. Without strategic investment in upskilling and certification programs, enterprises risk falling behind in fully leveraging Kubernetes’ capabilities.

• Growing Integration of GitOps for Automated Deployments: The Kubernetes Solutions Market is seeing a major shift toward GitOps practices to streamline deployment workflows. GitOps enables automated infrastructure updates through version-controlled repositories, significantly reducing manual errors and configuration drift. As of early 2025, over 60% of cloud-native enterprises are integrating GitOps into their CI/CD pipelines, accelerating the pace of secure deployments. This trend is especially prominent among fintech and SaaS providers where reliability and rapid iteration are critical for competitiveness.

• Expansion of Kubernetes in Multi-Cloud Environments: Organizations are increasingly using Kubernetes as a unifying orchestration layer across multiple cloud platforms. This flexibility enhances workload portability and reduces dependency on a single cloud vendor. A recent enterprise survey indicated that more than 55% of large organizations are operating Kubernetes clusters on two or more public cloud providers. Multi-cloud adoption is particularly high in Europe and Asia-Pacific due to regional compliance regulations and data residency requirements.

• Rise of Kubernetes-Native Security Platforms: Security has become a core focus in the Kubernetes Solutions Market, driving innovation in Kubernetes-native security tools. Features like real-time container scanning, runtime policy enforcement, and workload identity validation are now integrated directly into orchestration workflows. Enterprises with sensitive data workloads—especially in healthcare and finance—are deploying these security frameworks to meet stringent governance standards, leading to a measurable reduction in security incidents tied to misconfigurations.

• Adoption of Lightweight Kubernetes Distributions for Edge Computing: As edge computing gains traction, the demand for lightweight Kubernetes distributions such as K3s and MicroK8s has surged. These distributions are optimized for low-resource environments, enabling seamless orchestration on edge devices and remote sites. Industrial IoT and smart manufacturing deployments are the primary drivers behind this trend, with adoption rates in the manufacturing sector rising by over 30% year-over-year.

The Kubernetes Solutions Market is segmented into three primary categories: types of solutions, application domains, and end-user industries. These segments offer strategic insights into how Kubernetes technologies are being deployed across diverse business landscapes. Solution types range from managed services to self-hosted platforms, each catering to specific operational needs. Application-wise, Kubernetes is being utilized in everything from application development and testing to real-time data processing. When it comes to end-users, the market sees high participation from sectors like IT & telecom, BFSI, healthcare, and manufacturing. Managed Kubernetes services remain especially attractive to businesses seeking operational simplicity and scalability, while self-hosted solutions are preferred by those requiring greater control and customization. As container adoption deepens and organizations pursue digital transformation, each segment of the market is undergoing dynamic shifts influenced by infrastructure demands, regulatory compliance, and innovation cycles.

The Kubernetes Solutions Market offers a variety of solution types, including Managed Kubernetes Services, Self-Hosted Kubernetes Platforms, Kubernetes Monitoring and Observability Tools, Kubernetes Security Platforms, and Kubernetes Networking Solutions. Among these, Managed Kubernetes Services lead the market due to their simplified operations, scalability, and vendor-managed infrastructure. Enterprises, especially small and medium-sized businesses, prefer managed solutions to avoid the complexity of cluster maintenance and upgrades. The fastest-growing type is Kubernetes Security Platforms, fueled by heightened compliance requirements and increasing sophistication of cloud-native threats. These platforms integrate features like runtime security, policy enforcement, and workload protection, making them indispensable in regulated industries. Self-Hosted Kubernetes Platforms remain relevant among tech-forward organizations seeking granular control over their environments. Meanwhile, Networking Solutions and Observability Tools serve as essential add-ons, particularly in multi-cluster, multi-cloud deployments where traffic control and performance monitoring are critical to service reliability.

Kubernetes Solutions are deployed across a broad range of applications, including Application Development & Testing, DevOps Automation, Real-Time Data Processing, Microservices Management, and CI/CD Pipeline Orchestration. Application Development & Testing dominates this segment, driven by Kubernetes’ ability to support agile workflows, rollback mechanisms, and scalable sandbox environments. DevOps Automation represents the fastest-growing application area, with more enterprises automating infrastructure provisioning and deployment pipelines using Kubernetes-native tools. This growth is reinforced by increased adoption of Infrastructure as Code (IaC) and GitOps practices. Microservices Management is another core use case, enabling modular application design and independent scaling of services. Real-Time Data Processing is gaining attention in edge AI and analytics-driven businesses, while CI/CD Orchestration tools integrated with Kubernetes provide continuous delivery advantages for companies focused on rapid innovation and frequent code releases.

Key end-user segments within the Kubernetes Solutions Market include IT & Telecom, Banking, Financial Services and Insurance (BFSI), Healthcare, E-Commerce & Retail, and Manufacturing. IT & Telecom is the leading end-user, accounting for the highest volume of Kubernetes deployments due to its constant need for high availability, automation, and scalable infrastructure.

Healthcare is the fastest-growing end-user category, as digital health platforms adopt Kubernetes to ensure security, uptime, and data integrity in mission-critical applications like EHRs and diagnostics. Increasing adoption of AI-powered clinical tools is accelerating this growth. BFSI institutions rely on Kubernetes for secure transaction processing and scalable digital banking solutions. The E-Commerce & Retail sector uses Kubernetes to manage peak traffic loads and support agile feature rollouts. Meanwhile, Manufacturing is gradually integrating Kubernetes to orchestrate edge computing nodes in smart factories and IoT environments, enhancing operational efficiency and data analysis capabilities.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.3% between 2025 and 2032.

The Kubernetes Solutions Market continues to thrive across North America, owing to widespread enterprise digital transformation and robust cloud infrastructure ecosystems. Simultaneously, Asia-Pacific is undergoing a surge in Kubernetes adoption, driven by smart city initiatives, increasing developer communities, and rapid industrial modernization. Europe follows closely behind with strong regulatory support for containerized data processing. These regions collectively influence global demand through investments in automation, hybrid cloud models, and open-source platforms. From financial services to e-commerce and telecom, regional diversification in Kubernetes use cases supports this upward trajectory. Moreover, public and private partnerships focused on tech innovation have created a sustainable environment for market expansion.

Accelerating Containerization Across Tech-Driven Enterprises

North America holds a commanding 38.2% share of the global Kubernetes Solutions Market, anchored by its mature IT ecosystem and strong enterprise cloud maturity. The region is home to major industries such as finance, healthcare, and telecommunications, which heavily utilize Kubernetes to support microservices, CI/CD pipelines, and scalable applications. Key digital transformation initiatives across large U.S. and Canadian corporations are intensifying demand for container orchestration platforms. In addition, federal backing for cloud-native security frameworks and data governance standards is streamlining Kubernetes deployment in government and regulated sectors. Continuous innovation in AI and edge computing is also fostering adoption across mid-sized enterprises seeking operational efficiency.

Cloud Governance and Digital Resilience Fueling Platform Adoption

Holding approximately 27.6% of the global Kubernetes Solutions Market, Europe remains a vital contributor to global demand, led by countries such as Germany, the UK, and France. Strict adherence to data protection regulations like GDPR has propelled interest in Kubernetes-native security and policy enforcement tools. Public cloud providers and hyperscalers are partnering with European governments to ensure compliance-aligned Kubernetes deployments. Simultaneously, sustainability-focused tech policies and low-emission data centers are encouraging cloud-native architectures. Enterprises across retail, logistics, and manufacturing are integrating Kubernetes to enhance operational resilience, while the regional push for AI integration in cloud systems further accelerates platform modernization.

Surging Digital Infrastructure and Developer Ecosystem Expansion

Asia-Pacific is witnessing the fastest growth in the Kubernetes Solutions Market, ranking high in volume consumption and developer participation. Countries like China, India, and Japan are leading adoption due to nationwide digitization programs and surging demand for cloud-native applications. In India, public-sector technology overhauls and startup-led cloud innovation have intensified the focus on scalable container orchestration. In China, robust smart city infrastructure and AI-powered industrial automation are driving enterprise Kubernetes deployment. Japan’s high-tech industries and IoT-heavy applications are making Kubernetes central to managing decentralized workloads. Innovation hubs in Bangalore, Shenzhen, and Tokyo are pushing adoption deeper into both IT and non-IT sectors.

Cloud-Led Modernization and Sectoral Digitization Driving Expansion

South America, with Brazil and Argentina as its key contributors, is emerging as a growing market for Kubernetes Solutions. The region contributes roughly 6.5% to the global share and is seeing traction due to expanding fintech ecosystems and modernization of public IT systems. Brazilian cloud adoption is on the rise, fueled by government efforts to digitize administrative services and promote cloud-native business applications. Argentina’s energy and infrastructure sectors are deploying Kubernetes to enhance operational analytics and system scalability. Trade policy improvements and increased investment in telecom modernization are enabling smoother cloud platform adoption across national boundaries.

Enterprise Cloud Expansion and Infrastructure Innovation Gaining Momentum

In the Middle East & Africa region, Kubernetes Solutions adoption is being led by technological modernization across energy, construction, and logistics sectors. Countries like the UAE and South Africa are central to regional demand, with cloud initiatives like Smart Dubai and e-Government projects driving investment. The region accounts for approximately 5.2% of global demand, with increasing adoption in oil & gas data operations, logistics automation, and public sector cloud transformation. Regulatory incentives for tech startups and infrastructure-as-a-service providers are accelerating the integration of Kubernetes into enterprise systems. As digital transformation spreads across non-oil sectors, demand for orchestration tools is expected to intensify.

United States – 34.1% Market Share

Strong demand across Fortune 500 enterprises and extensive cloud infrastructure capabilities power its leadership in the Kubernetes Solutions Market.

China – 17.6% Market Share

Rapid digital transformation in manufacturing, AI-based systems, and government cloud projects reinforce China's dominant position in Kubernetes adoption.

The Kubernetes Solutions market exhibits a highly dynamic and competitive landscape with over 120 active participants globally, ranging from open-source contributors to major enterprise platform providers. The market is defined by rapid innovation cycles, strategic M&A activity, and technological differentiation focused on scalability, observability, and security. Leading vendors are emphasizing container-native development platforms and multi-cloud orchestration capabilities to maintain competitive positioning.

Numerous vendors have adopted open-core business models, enhancing upstream Kubernetes while offering proprietary features for workload management, security, and automation. Strategic collaborations with hyperscale cloud providers and edge computing alliances have become central to market positioning. In 2024 alone, several players launched integrated DevSecOps toolchains and AI-driven autoscaling modules, aiming to capture demand from mid-market and enterprise-level clients.

The growing focus on edge-native Kubernetes frameworks and zero-trust container security is further intensifying R&D investments. New entrants are also leveraging AI-powered observability platforms to compete against established players. The competition is further shaped by regulatory compliance innovations, platform standardization efforts, and customer-centric support offerings—cementing Kubernetes Solutions as a high-stakes arena of enterprise digital transformation.

Red Hat Inc.

VMware Inc.

Canonical Ltd.

SUSE LLC

Rancher Labs

Mirantis Inc.

Platform9 Systems

Weaveworks Inc.

D2iQ (formerly Mesosphere)

Docker Inc.

Portworx by Pure Storage

Kubermatic GmbH

Kasten by Veeam

Sysdig Inc.

Loft Labs Inc.

The Kubernetes Solutions Market is being significantly shaped by the evolution of container orchestration technologies, hybrid and multi-cloud deployment models, and edge computing integration. As Kubernetes matures, enterprises are increasingly adopting Kubernetes-native tools for observability, cost optimization, security enforcement, and lifecycle automation. Technologies such as GitOps are enabling continuous deployment practices by integrating Kubernetes with infrastructure-as-code and version-controlled workflows, allowing for faster, safer rollouts and rollbacks. AI and ML-powered automation is gaining traction, with Kubernetes clusters now capable of intelligent auto-scaling and resource utilization based on real-time workload behavior. In 2024, over 60% of new enterprise Kubernetes deployments included integrated AI-based monitoring tools, supporting proactive infrastructure management and reducing downtime. Similarly, the adoption of service mesh architectures like Istio and Linkerd has improved microservices visibility and traffic management within Kubernetes environments.

Container storage interface (CSI) advancements are also transforming Kubernetes storage layers by enabling dynamic volume provisioning across various storage backends, improving data persistence in stateful workloads. Additionally, the integration of confidential computing and runtime security has reinforced the platform’s suitability for regulated industries such as healthcare, finance, and defense. Edge Kubernetes is another fast-emerging area. Lightweight Kubernetes distributions like K3s and MicroK8s are being deployed in remote and resource-constrained environments, enabling real-time data processing closer to data sources. Combined with 5G expansion, this is revolutionizing IoT deployments and distributed AI applications. The convergence of these technologies is reinforcing Kubernetes as the cornerstone of modern cloud-native infrastructure strategies.

• In January 2024, VMware released Tanzu Application Platform 1.6 with enhanced support for secure software supply chains and improved Kubernetes-native DevSecOps integration, reducing deployment time by up to 30% in enterprise environments.

• In March 2024, Red Hat introduced AI-enabled observability enhancements to OpenShift, utilizing predictive analytics to reduce downtime and optimize performance across hybrid Kubernetes clusters, benefiting over 5,000 deployments globally.

• In October 2023, SUSE completed the acquisition of StackState, a Kubernetes observability platform, enhancing its Rancher Kubernetes Engine with end-to-end dependency mapping and AI-driven alerting capabilities for complex, multi-cluster operations.

• In May 2024, D2iQ launched its Kommander Pro platform designed for air-gapped and high-security environments, featuring automated policy enforcement and lifecycle management for Kubernetes across defense and aerospace sectors.

The Kubernetes Solutions Market Report provides an in-depth evaluation of the global industry landscape, highlighting key technological, geographical, and application-based dimensions that define its current dynamics and future outlook. This report examines over 15 core product types and Kubernetes service variations, covering distributions ranging from enterprise-managed platforms to lightweight edge variants. The analysis includes critical functionalities such as cluster management, container orchestration, persistent storage integration, service mesh capabilities, and security hardening frameworks. Geographically, the report spans six major regions: North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. It further drills down into more than 25 key country-level markets, including major economies such as the United States, China, Germany, and India. Each region is evaluated based on adoption trends, infrastructure maturity, technological penetration, and local regulatory environments.

From an application standpoint, the report details deployment across multiple verticals such as IT & telecom, BFSI, healthcare, manufacturing, government, and retail. It also addresses emerging sectors like edge computing, automotive AI, and 5G-related use cases. The report highlights enabling technologies such as AI-driven orchestration, DevSecOps integration, and hybrid/multi-cloud architecture. Additionally, niche market areas like Kubernetes at the edge, confidential computing, and zero-trust architectures are explored for their long-term strategic importance. This comprehensive scope offers decision-makers a robust foundation for evaluating investment opportunities, vendor landscapes, and competitive positioning across diverse global ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,056.45 Million |

|

Market Revenue in 2032 |

USD 7,574.09 Million |

|

CAGR (2025 - 2032) |

17.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daikin Industries, Ltd., Thermo Fisher Scientific Inc., KKT Chillers, BV Thermal Systems, Laird Thermal Systems, RIEDEL Kooling GmbH, Glen Dimplex Group, Motivair Corporation, Filtrine Manufacturing Company, SMC Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |