Reports

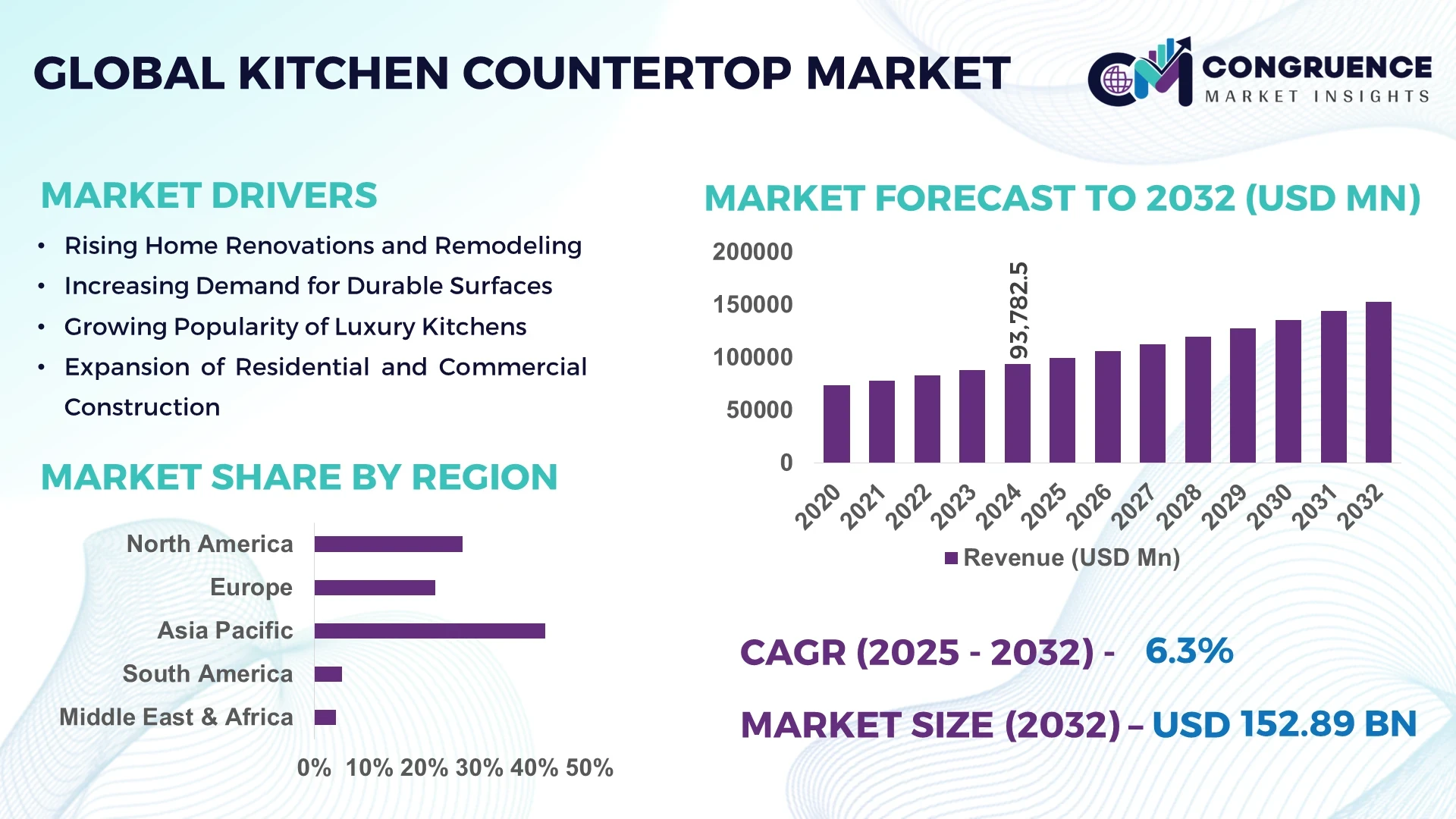

The Global Kitchen Countertop Market was valued at USD 93,782.5 Million in 2024 and is anticipated to reach a value of USD 1,52,893.1 Million by 2032 expanding at a CAGR of 6.3% between 2025 and 2032.

In China, the dominant country in the Kitchen Countertop Market, production capacity has expanded substantially through large-scale automated fabrication facilities capable of processing high-end engineered stone surfaces. Investment levels have surged across industrial clusters, especially in Guangdong and Zhejiang provinces, funding new high-throughput production lines. The industry applications now span residential, hospitality, and institutional developments, with manufacturers deploying robotics for cutting, edging, and finishing workflows. Technological advancements include deployment of AI-assisted quality inspection systems and CNC machinery programmed for micro-tolerance fabrication—enabling precision, reduced waste, and faster throughput.

Across the Kitchen Countertop Market, residential kitchens in urban developments account for a significant share, while commercial and hospitality installations contribute steadily in premium segments. Innovations include antimicrobial surface treatments integrated during resin curing, ultra-thin quartz composites engineered for lighter weight without sacrificing durability, and digital showroom tools that allow augmented-reality visualization of countertop installations. On the regulatory and environmental front, stricter emissions norms for formaldehyde and quartz dust in several regions have driven adoption of low-VOC binders and enclosed-dust-capture cutting systems. Economically, rising disposable incomes and housing renovation cycles in emerging markets drive regional consumption patterns—particularly in Southeast Asia and Latin America. Emerging trends include increasing demand for personalized countertop finishes, integration of smart touch-sensitive surfaces (e.g., embedded lighting or wireless charging), and growth in recycled-material slabs leveraging post-consumer glass or engineered composite waste—pointing toward a future outlook shaped by sustainability, digital integration, and design customization.

Artificial intelligence (AI) is transforming the Kitchen Countertop Market by elevating manufacturing precision, streamlining workflow automation, and enhancing product quality control. AI-enabled CNC systems now routinely interpret 3D model inputs and adapt cutting paths in real time to account for material variations—reducing edge-chipping and improving yield accuracy across diverse stone and engineered-surface batches. In large production centers, AI-driven robotic handling systems coordinate slab loading, cutting, finishing, and inspection tasks in a tightly choreographed sequence, shortening cycle times and enabling continuous plant operation with minimal human intervention.

In warehousing, AI-powered inventory management systems forecast demand for specific countertop materials, optimizing slab ordering, storage allocation, and minimizing overstock or spoilage of fragile stone types. Predictive maintenance algorithms monitor tool wear rates, spindle vibration patterns, and temperature profiles to schedule downtime only when necessary—thus preserving throughput while prolonging cutter lifespan.

On the customer-facing side, AI is embedded in design configurators that analyze kitchen dimensions and user preferences to recommend countertop material, edge profiles, and finish based on usage patterns—streamlining specification decisions for architects, designers, and homeowners. AI-based analytics also help manufacturers optimize supply chains by analyzing procurement, lead times, and regional consumption trends—enabling real-time adjustments to production and logistics workflows.

AI-led data analytics are facilitating continuous improvement: by aggregating quality-control data across batches, manufacturers can identify recurring surface defects, correlate them with upstream process conditions, and proactively adjust resin mixing or polishing parameters. In this way, AI is not merely an add-on; it is becoming integral to operational performance optimization across the Kitchen Countertop Market.

“In 2024, an AI-guided robotic polishing cell achieved a 25 percent reduction in finish-surface variability compared to conventionally operated lines—measured as variation in surface roughness (Ra) across 100 sampled quartz slabs.”

The Kitchen Countertop Market dynamics in the context of the keyword Kitchen Countertop Market reflect shifting customer expectations, supply-chain optimization, technological integration, and regulatory pressures. Demand is increasingly driven by the premiumization of residential interiors and rising renovation cycles in urban and suburban segments. Supply-side dynamics show consolidation among large fabricators deploying automation to offset labor shortages and rising operational costs. Regulations on fine silica particulate emissions and VOC exposure are pushing adoption of closed-loop finishing systems. Consumer preferences are evolving toward custom textured finishes and integrated smart functionality, prompting more flexible fabrication techniques. Cost volatility in raw materials—such as resin, pigments, and imported natural stone—affects margins, requiring process innovation. Sustainability is now a non–negotiable driver, with recycled composite slabs and biodegradable packaging gaining traction. Collectively, these forces are reshaping how the Kitchen Countertop Market evolves operationally and strategically.

The rising consumer preference for durable, hygienic surfaces in kitchen environments is exerting a powerful influence on the Kitchen Countertop Market. End-users—particularly in high-use households and food-service settings—prioritize surfaces that resist scratches, stains, and microbial growth. This has led manufacturers to focus R&D on resin-based composite and hard quartz formulations infused with antimicrobial agents and scratch-resistant resins. As a result, production lines are being retrofitted to incorporate UV-curing stages for surface sterilization, while new polishing methods preserve surface integrity. Detailed studies of wear-resistance under repeated cleaning tests show that antimicrobial resin-bonded countertops maintain functional surface integrity after over 50,000 abrasion cycles—outpacing traditional granite by nearly 35%. This driver is reshaping material innovation, process engineering, and market appeal across the Kitchen Countertop Market.

Volatility in raw material prices is posing a significant constraint on the Kitchen Countertop Market. Key inputs such as resin polymers, color pigments, and engineered binders experience frequent price fluctuations tied to petrochemical markets. Over a recent 12-month period, resin costs spiked by approximately 18%, while specialty pigments rose by 12%, compressing prefabbed sink-inclined slab margins and complicating pricing strategies. This instability discourages long-term fixed-price contracts and introduces uncertainty for both manufacturers and project specifiers. To maintain margin consistency, fabricators must routinely adjust purchasing strategies, renegotiate supplier terms, or institute variable-price pass-through clauses—adding administrative complexity and pricing volatility within the Kitchen Countertop Market.

The integration of smart technologies into countertop surfaces represents an emerging opportunity within the Kitchen Countertop Market. Applications such as embedded induction-charging zones, touch-sensitive lighting strips, and interactive recipe-display panels are gaining traction among affluent homeowners and luxury kitchen projects. Manufacturers pilot thin-film conductive layers seamlessly embedded during pressing, without affecting surface durability. Prototype installations in select premium housing developments demonstrate user-interactions averaging 120 uses per month per countertop—for example, quick ambient lighting activation or recipe pop-ups. This intersection of surface design and IoT offers differentiation and recurring value-added services, positioning the Kitchen Countertop Market for future growth in technology-enhanced living environments.

The Kitchen Countertop Market is facing a significant challenge due to growing regulatory scrutiny on silica dust emissions during on-site fabrication and finishing. Authorities in several regions—particularly parts of North America and Europe—have enacted stricter exposure limits and required fabricators to adopt enclosed cutting systems with negative-pressure ventilation. Retrofitting existing workshops with such systems can raise capital costs by 20–30%, lengthen project turnarounds, and necessitate operator retraining. Moreover, the compliance reporting requirements, including air-quality monitoring logs and periodic inspections, increase administrative overhead. These regulatory pressures challenge small and mid-sized fabricators particularly, limiting their ability to compete on cost and responsiveness in the Kitchen Countertop Market.

Modular and Prefabricated Construction Accelerates: The adoption of modular construction is reshaping demand dynamics in the Kitchen Countertop Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Surge in Eco-Composite and Recycled Material Slabs: There is a noticeable uptick in the use of slabs made from recycled glass, post-consumer quartz waste, and composite off-cuts. Production volumes of eco-composite slabs have risen by around 15% year-over-year, driven by growing sustainability mandates in construction and consumer demand for environmentally responsible materials—presenting a new cost-competitive alternative in the Kitchen Countertop Market.

Customization via Digital Visualization Platforms: Kitchen countertop suppliers are incorporating augmented-reality and 3D visualization tools to allow clients and architects to preview materials and edge profiles in situ. Engagement metrics from pilot programs show that proposal approval speed doubles when clients use these platforms—streamlining decision-making and differentiating public-facing offerings within the Kitchen Countertop Market.

Adoption of Low-Emission Composite Binders: Regulatory regulations have prompted manufacturers to shift toward low-VOC and formaldehyde-free composite binders. New binder formulations now meet emerging indoor-air-quality standards, with emissions reduced by approximately 40% compared to previous formulations—improving workplace safety and aligning with evolving construction certification systems across the Kitchen Countertop Market.

The segmentation of the Kitchen Countertop Market demonstrates clear distinctions across types, applications, and end-users, each contributing differently to the industry landscape. Product types vary from natural stone to engineered surfaces, offering a diverse mix of durability, aesthetics, and cost positioning. Applications extend across residential, commercial, and institutional sectors, with distinct consumption drivers tied to construction and renovation cycles. End-users include households, hospitality establishments, healthcare facilities, and large-scale developers, each influencing material choice and design adoption. Insights reveal that premium engineered surfaces are increasingly favored, commercial projects demand higher customization, and institutional installations emphasize compliance with safety and hygiene standards. Collectively, these segmentation insights underscore a market evolving with consumer preferences, technological advancements, and sector-specific requirements.

Kitchen countertops are offered in a wide range of types, including natural stone, engineered stone, solid surfaces, laminates, stainless steel, and others. Among these, engineered stone countertops, particularly quartz, hold the leading position owing to their superior durability, consistent aesthetic appeal, and low maintenance needs. Their uniformity and availability in a broad palette of colors make them the preferred choice for both residential and commercial installations.

The fastest-growing category is solid surface countertops, driven by their seamless finish, flexibility in design, and compatibility with modern modular kitchens. Increasing demand from urban households and institutions for hygienic, repairable surfaces adds to their growth momentum.

Natural stone countertops, such as granite and marble, continue to hold relevance for luxury projects, valued for their unique patterns and premium positioning. Laminates remain popular in cost-sensitive markets, offering affordable solutions, while stainless steel countertops are niche but growing within the food-service industry for their hygienic properties. Each type fulfills a specific market demand, ensuring a balanced landscape of innovation, tradition, and affordability in the Kitchen Countertop Market.

The Kitchen Countertop Market applications cover residential, commercial, and institutional sectors. The residential segment leads the market, supported by increasing urbanization, rising disposable incomes, and strong global trends in home renovation. Homeowners prioritize durable and aesthetic countertop solutions, with quartz and granite dominating this space. The combination of design versatility and easy maintenance fuels their adoption in new housing and remodeling projects alike.

The fastest-growing application segment is commercial, particularly within hospitality, restaurants, and retail. The growth is supported by rising demand for stylish yet highly durable surfaces that can withstand high-traffic usage. Modern hotels and restaurants often specify antimicrobial, scratch-resistant surfaces that blend functionality with contemporary aesthetics, driving uptake in this category.

Meanwhile, institutional applications, including healthcare and educational facilities, emphasize hygiene, compliance, and safety. Solid surfaces and stainless steel options are often specified here due to their seamless finishes and sterilization compatibility. Each application contributes uniquely to overall demand, shaping a multifaceted growth trajectory for the Kitchen Countertop Market.

The Kitchen Countertop Market caters to a diverse range of end-users, including households, hospitality, healthcare, and large real estate developers. Households form the leading end-user segment, with demand influenced by rapid residential construction, urban apartment developments, and sustained kitchen renovation trends. The growing emphasis on modern kitchen aesthetics and multifunctional spaces continues to strengthen this category’s dominance.

The hospitality sector is the fastest-growing end-user, driven by global expansion in hotels, restaurants, and catering facilities. This sector requires countertops that deliver both high visual appeal and long-term durability. Materials with enhanced resistance to stains, scratches, and heat have gained traction, aligning with the operational demands of high-use environments.

Other relevant end-users include healthcare institutions, which prioritize hygienic and non-porous materials for infection control, and large real estate developers, who drive bulk demand for standardized solutions across housing projects. These varied end-users contribute to a robust and dynamic ecosystem, ensuring steady growth and innovation across the Kitchen Countertop Market.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The Asia-Pacific region continues to dominate due to large-scale residential and commercial construction activity, significant manufacturing capacity, and rapid urbanization. Meanwhile, North America benefits from strong renovation cycles, high consumer spending on premium kitchen solutions, and rapid integration of advanced manufacturing technologies. Together, these dynamics highlight a global marketplace shaped by regional construction trends, regulatory policies, and evolving consumer preferences.

North America accounted for 27% of the global Kitchen Countertop Market share in 2024, supported by robust residential renovation activity and expanding commercial real estate developments. Key industries driving demand include housing construction, hospitality, and premium retail. Regulatory shifts such as stricter silica dust exposure standards are influencing manufacturing processes, pushing fabricators toward closed-loop cutting and dust capture technologies. Government incentives promoting sustainable housing and green building certifications are further stimulating market growth. Technological advancements include the deployment of AI-driven CNC machining and digital design tools, enabling precision cutting, seamless customization, and faster project turnaround across the United States and Canada.

Europe held 22% of the global Kitchen Countertop Market share in 2024, with Germany, the UK, and France leading consumption. Sustainability initiatives are at the forefront, as regulatory bodies enforce low-emission production and recycling mandates under the European Green Deal framework. Manufacturers are investing heavily in sustainable stone alternatives and recycled composite materials to align with these policies. Digital transformation is also evident, with widespread adoption of AR/VR visualization tools in kitchen showrooms and automated prefabrication technologies. This convergence of regulatory pressure, eco-conscious consumers, and advanced technologies positions Europe as a key hub for innovation in the Kitchen Countertop Market.

The Asia-Pacific region recorded the largest market volume, representing 42% of global consumption in 2024, with China, India, and Japan as top consumers. China’s expansive manufacturing capacity, combined with India’s growing middle-class housing demand, drives regional momentum. Japan contributes with high-value demand for premium engineered surfaces in modern urban housing. Large infrastructure development and government-driven housing schemes across emerging economies strengthen overall consumption. Technology hubs in China and South Korea are accelerating innovation through AI-assisted fabrication lines and robotic finishing units. The region’s strong combination of scale, innovation, and demand consolidation secures its leadership in the Kitchen Countertop Market.

South America accounted for 5% of the global Kitchen Countertop Market in 2024, with Brazil and Argentina leading demand. Brazil’s large urban housing projects and hospitality expansions drive the majority of installations, while Argentina benefits from growth in residential renovations. Infrastructure spending across airports, hotels, and shopping complexes is boosting the region’s countertop demand. Trade policies encouraging local stone exports also support domestic processing industries. Government incentives promoting real estate development are further strengthening the market outlook. South America’s evolving construction sector and increasing preference for modern, durable countertop materials provide steady growth opportunities across the region.

The Middle East & Africa held 4% of the global Kitchen Countertop Market share in 2024, with the UAE and South Africa as key growth countries. The UAE’s large-scale commercial and residential construction projects, coupled with South Africa’s growing urbanization, create strong demand for modern kitchen installations. Regional industries such as oil & gas and tourism fuel construction activities, particularly in luxury hospitality and residential segments. Technological modernization is evident in the adoption of CNC-based fabrication facilities and AI-driven inventory systems. Local trade partnerships and regulations encouraging sustainable building practices further contribute to the regional market’s expansion.

The Kitchen Countertop Market is characterized by a competitive environment involving more than 250 active global and regional manufacturers. Competition is driven by product differentiation, advanced fabrication technologies, and expanding distribution networks. Key players are positioning themselves through partnerships with construction companies, digital design firms, and smart home integrators to strengthen their presence. Product launches focus heavily on engineered stone surfaces with enhanced durability, antimicrobial properties, and sustainable compositions. Mergers and acquisitions are also notable, as firms seek to expand production capacity and geographical reach. Innovation trends such as the integration of AI-enabled fabrication systems, low-emission resin binders, and augmented reality design platforms are reshaping competitive strategies. Additionally, investments in sustainable materials and eco-friendly manufacturing practices are becoming central to long-term positioning. This dynamic landscape reflects a blend of scale advantages by large multinational corporations and niche specialization by regional manufacturers. Collectively, the competitive ecosystem is accelerating technological advancement and pushing the industry toward higher efficiency and consumer-centric product offerings.

Caesarstone Ltd.

Cosentino S.A.

Cambria Company LLC

Wilsonart LLC

Formica Group

Aristech Surfaces LLC

Compac Surfaces

Laminam S.p.A.

Pokarna Limited

VICOSTONE JSC

Hanwha Surfaces

Panolam Industries International, Inc.

DuPont Surfaces

Masco Corporation

Polycor Inc.

Technological advancements are significantly influencing the Kitchen Countertop Market, redefining manufacturing, design, and sustainability standards. CNC (Computer Numerical Control) machinery has become the backbone of fabrication, enabling precise cutting, drilling, and finishing with tolerances as low as 0.1 mm, thereby reducing material waste and improving output consistency. Automation and robotics have further enhanced slab handling, polishing, and edge profiling, resulting in reduced labor dependency and improved throughput across production lines.

Emerging technologies are shaping the market in several directions. AI-powered inspection systems are increasingly used to detect micro-defects in quartz and solid surfaces, ensuring high quality while minimizing rework rates. Additionally, 3D visualization and augmented reality platforms are transforming consumer engagement, allowing homeowners and architects to preview materials and finishes in virtual environments. Adoption of digital twin models in larger manufacturing facilities supports predictive maintenance and operational optimization, reducing downtime by up to 30%.

Sustainability-focused innovations are also advancing, with low-VOC composite binders and recycled material integration gaining momentum. Engineered surfaces incorporating up to 60% post-consumer glass or quartz waste are emerging as competitive products in eco-conscious markets. Furthermore, antimicrobial coatings and heat-resistant nano-surfaces are being deployed in institutional and commercial projects, enhancing functional value. Collectively, these technologies are propelling the Kitchen Countertop Market into a future defined by efficiency, sustainability, and intelligent customization.

• In March 2023, Caesarstone launched a new line of quartz countertops integrating recycled materials, with each slab containing up to 40% repurposed stone and glass, enhancing sustainability while maintaining premium aesthetics and durability.

• In September 2023, Cosentino opened a high-tech fabrication hub in Almería, Spain, equipped with fully automated CNC systems and AI-based inspection tools, increasing production efficiency by 25% compared to traditional facilities.

• In May 2024, Cambria introduced antimicrobial-infused quartz countertops designed for healthcare and hospitality applications, demonstrating enhanced hygiene performance by reducing bacterial growth rates by over 90% in standardized laboratory tests.

• In July 2024, VICOSTONE unveiled a next-generation solid surface product featuring ultrathin quartz composites, reducing material weight by 20% while preserving strength and heat resistance, aimed at modular and prefabricated housing markets.

The scope of the Kitchen Countertop Market Report encompasses a detailed examination of the industry across product types, applications, end-users, geographic regions, and technology innovations. It provides insights into natural stone, engineered stone, solid surface, laminate, stainless steel, and other countertop materials, analyzing their distinct adoption patterns and industry relevance. Applications covered include residential, commercial, and institutional, each evaluated for its demand drivers and sector-specific requirements. End-user analysis spans households, hospitality, healthcare, and real estate developers, highlighting their unique roles in shaping product demand.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing numerical insights into their market positions and growth trajectories. Particular focus is placed on leading consumption countries such as China, the United States, India, Germany, and Brazil, supported by region-specific construction, regulatory, and innovation trends.

Technology analysis includes automation, AI-enabled manufacturing, sustainable binder innovations, recycled composite materials, and digital visualization tools. The report also explores niche and emerging trends such as antimicrobial surfaces, ultrathin engineered slabs, and smart countertops with integrated touch and charging capabilities. By combining comprehensive segmentation with regional and technological perspectives, the Kitchen Countertop Market Report equips decision-makers and analysts with actionable insights to guide strategic investments, product innovation, and competitive positioning in a rapidly evolving global market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 93,782.5 Million |

| Market Revenue (2032) | USD 1,52,893.1 Million |

| CAGR (2025–2032) | 6.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Caesarstone Ltd., Cosentino S.A., Cambria Company LLC, Wilsonart LLC, Formica Group, Aristech Surfaces LLC, Compac Surfaces, Laminam S.p.A., Pokarna Limited, VICOSTONE JSC, Hanwha Surfaces, Panolam Industries International, Inc., DuPont Surfaces, Masco Corporation, Polycor Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |