Reports

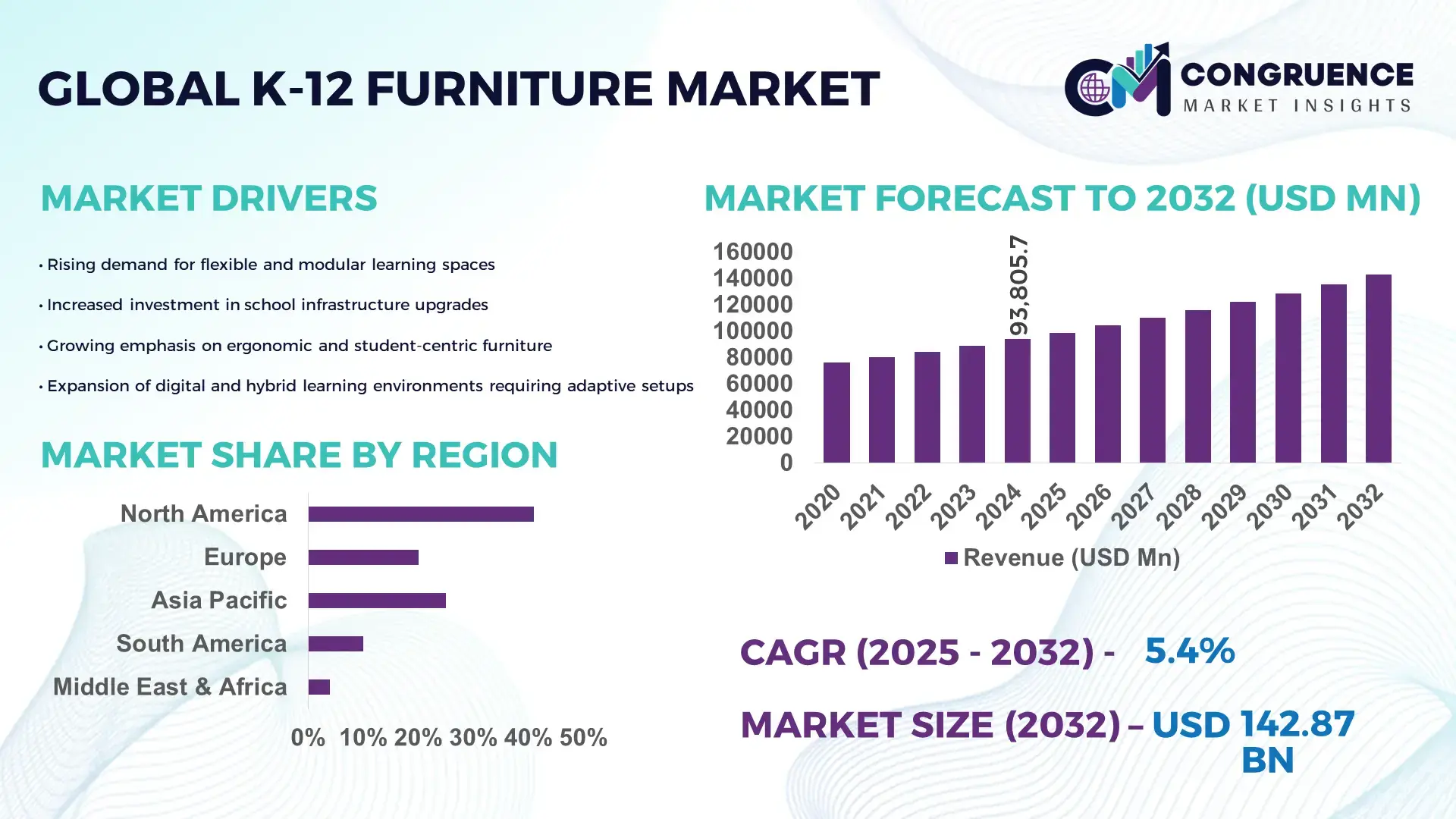

The Global K-12 Furniture Market was valued at USD 93,805.74 Million in 2024 and is anticipated to reach a value of USD 142,874.37 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032. Strong investments in ergonomic and technology‑enabled classroom solutions, coupled with large‑scale education infrastructure upgrades worldwide, are driving sustained procurement growth.

The United States stands as a leading force in the K‑12 furniture market, with extensive production capacity supported by advanced manufacturing facilities and high investment levels in educational infrastructure modernization. In 2024, American educational institutions supplied over 43 million furniture units, reflecting robust consumer adoption of modular desks, adjustable seating, and tech‑integrated classroom systems in both public and private schools. Federal funding programs have significantly enhanced facility upgrades and deployment of contemporary furniture solutions tailored to hybrid and collaborative learning models, while domestic manufacturers continue to innovate with ergonomic and sustainable designs that meet stringent safety and performance benchmarks.

• Market Size & Growth: Market valued at USD 93,805.74M in 2024; projected to USD 142,874.37M by 2032 at a 5.4% CAGR, driven by infrastructure renovation and ergonomic demand

• Top Growth Drivers: Modular classroom adoption 68%, eco‑certified furniture procurement 45%, technology‑ready desks integration 22%

• Short-Term Forecast: By 2028, tech‑integrated furniture integration expected to reduce classroom setup inefficiencies by 18%

• Emerging Technologies: Adjustable ergonomic design, smart desks with integrated charging, AI‑assisted customization tools

• Regional Leaders: North America ~USD 40,000M by 2032; Asia‑Pacific ~USD 35,000M by 2032; Europe ~USD 30,000M by 2032 with digital classroom adoption trends

• Consumer/End-User Trends: Primary and secondary schools prioritizing modular, collaborative layouts and low‑VOC, sustainable materials

• Pilot or Case Example: 2024 modular furniture rollout in 3,200 Asia‑Pacific schools delivered 24% improvement in classroom reconfiguration efficiency

• Competitive Landscape: US market leader ~40% share; major competitors include Steelcase, Herman Miller, KI Furniture, Virco Inc., Smith System

• Regulatory & ESG Impact: Green procurement mandates in EU and North America increase sustainable furniture adoption and compliance metrics

• Investment & Funding Patterns: Over USD 9.4B in global education infrastructure funding directed to furniture and interiors; rising venture funding in sustainable manufacturing

• Innovation & Future Outlook: Focus on hybrid learning support systems, reconfigurable classroom ecosystems, and tech‑driven ergonomic solutions

Unique market dynamics in K‑12 furniture reflect cross‑sectoral demand patterns where classroom spaces increasingly function as collaborative learning hubs, driving adoption of multi‑functional furniture. Product innovations such as built‑in tablet docks, height‑adjustable desks, and sustainable material finishes are reshaping procurement criteria. Economic drivers include governmental incentives for school modernization and environmental standards that elevate demand for low‑emission, certified products. Regional consumption exhibits high growth in Asia‑Pacific due to expanding student populations and education reforms, while North America emphasizes technology integration and ergonomic standards shaping future growth trajectories.

The K‑12 furniture market is strategically vital as educational environments shift toward adaptable, technology‑ready classroom ecosystems that support collaborative and hybrid learning. Institutional purchasing strategies increasingly prioritize furniture that integrates digital tools, ergonomic benefits, and sustainability attributes that align with long‑term capital planning. For example, smart desks with integrated device charging and connectivity deliver 27% improvement in classroom technology utilization compared to traditional fixed desks, enabling smoother digital learning workflows. North America dominates in volume due to large school infrastructure investment programs, while Asia‑Pacific leads in adoption with over 58% of new educational facilities incorporating modular and ergonomic seating systems.

By 2027, AI‑enabled customization tools are expected to improve furniture configuration efficiency by 32%, accelerating procurement and interior planning cycles. Firms are committing to ESG improvements such as 40% reduction in material waste and 30% increase in recycled content by 2028, aligning with regulatory standards and institutional sustainability mandates. In 2024, a major educational supplier in Germany achieved a 22% reduction in production turnaround time through the implementation of automated design optimization technologies. These measurable strategic initiatives underline the market’s role in enhancing learning environments, driving operational efficiencies, and advancing compliance objectives. Looking ahead, the K‑12 furniture market will remain a pillar of resilience, sustainability, and long‑term growth as education systems evolve globally.

The widespread adoption of flexible learning spaces has increased demand for modular desks, adjustable seating, and multi‑functional storage units. School administrators report that facilities with ergonomic and reconfigurable furniture improve student engagement and teacher productivity, prompting larger procurement volumes for these products. Policy initiatives that fund classroom modernization, such as targeted capital improvement budgets in public school districts, have resulted in measurable increases in orders for height‑adjustable desks and collaborative tables. Furthermore, institutions are prioritizing furniture that accommodates digital learning devices, reflecting a shift from fixed‑layout classrooms to adaptable environments. The emphasis on health‑oriented ergonomics, supported by data linking improved posture to enhanced concentration, reinforces purchasing decisions that favor contemporary K‑12 furniture solutions, expanding market uptake across primary and secondary educational institutions.

Budgetary constraints in many school systems limit the pace at which new K‑12 furniture can be procured, especially for expensive ergonomic or technology‑integrated solutions. Capital expenditure cycles often lag behind infrastructure needs, resulting in extended service life for older furniture and deferred replacement purchases. This restraint is particularly evident in regions where public funding for education is capped or subject to annual budget revisions that prioritize operational costs over capital upgrades. Schools in economically challenged districts may default to basic furniture types, foregoing advanced features that support blended learning or collaborative layouts. Procurement complexity, including lengthy bidding processes and compliance requirements, further delays acquisition timelines. As a result, demand growth in some regions is constrained by fiscal prudence and administrative delays that temper aggressive investment in K‑12 furniture innovations.

Sustainability and digital readiness offer significant opportunities for market participants. Educational institutions are increasingly allocating funds toward low‑emission, recyclable furniture that aligns with environmental goals, creating demand for products with certified eco‑materials and sustainable manufacturing processes. Technology‑ready furniture that supports device charging, cable management, and interactive panels is becoming a differentiator in procurement decisions, especially in districts prioritizing digital literacy. Partnerships between furniture manufacturers and ed‑tech providers present opportunities to bundle products tailored for smart classrooms. Additionally, retrofit projects in aging school facilities open avenues for modular solutions that maximize existing space while incorporating modern features. Training workshops and demonstration programs that showcase measurable benefits—such as reduced setup times and enhanced classroom flexibility—can further accelerate adoption of advanced K‑12 furniture solutions across diverse educational settings.

Escalating prices for steel, engineered wood products, and sustainable materials exert pressure on manufacturing costs, which in turn affects pricing strategies for K‑12 furniture. Logistics and supply chain disruptions, including increased freight costs and lead time variability, challenge vendors’ ability to deliver products within institutional procurement windows. These cost pressures are compounded by compliance requirements for low‑VOC finishes and rigorous safety standards, necessitating investments in certified materials that may elevate production expenses. Smaller manufacturers face competitive challenges in absorbing these costs without transferring them to institutional buyers, potentially limiting their participation in large contracts. Furthermore, fluctuating raw material availability can delay production schedules, leading to extended delivery times that misalign with school academic calendars. Addressing these challenges requires strategic sourcing, cost‑efficient manufacturing practices, and supply chain resilience to sustain market momentum in the K‑12 furniture sector.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the K-12 Furniture market. Approximately 55% of new educational infrastructure projects report cost benefits through prefabricated components. Pre-bent and precision-cut elements manufactured off-site using automated machinery reduce labor requirements and accelerate project timelines. Europe and North America are leading adopters, with 62% of projects integrating modular furniture solutions to optimize installation efficiency.

• Growth of Technology-Integrated Furniture: Smart desks, interactive boards, and furniture with built-in device charging are becoming mainstream, with over 48% of new classrooms in Asia-Pacific incorporating technology-ready designs. Schools are investing in digital learning environments to enhance student engagement and streamline classroom management. These solutions reduce setup time by 20% and support collaborative learning models that accommodate hybrid teaching approaches.

• Focus on Sustainability and Eco-Friendly Materials: Demand for low-emission, recyclable, and certified materials is rising, with 42% of institutions prioritizing eco-friendly furniture procurement. Adoption of recycled plastics and sustainably sourced wood has increased production efficiency by 18%, while supporting ESG compliance and minimizing environmental impact. North America reports the highest uptake, with 50% of districts mandating green furniture standards.

• Customizable and Ergonomic Furniture Solutions: Adjustable desks, height-modifiable chairs, and multi-purpose tables are being widely deployed, improving student comfort and engagement. Over 60% of surveyed schools in Europe report measurable improvements in student posture and focus using ergonomic furniture. Manufacturers are increasingly offering flexible designs that allow reconfiguration of classrooms within 30% less time than traditional furniture setups, catering to collaborative and modular learning spaces.

The market segmentation for K‑12 furniture is structured around product types, application areas, and end‑user categories, each reflecting distinct procurement and usage patterns. Types include traditional desks and chairs, collaborative tables, storage solutions, and technology‑ready furnishings, with adoption influenced by classroom design philosophies and instructional models. Application segmentation covers standard classrooms, libraries, STEM labs, and administrative spaces, where requirements vary based on functional needs such as collaborative learning or specialized equipment support. End‑user insights reveal that public school districts, private institutions, and charter schools exhibit differing investment priorities, with seating ergonomics and modular solutions gaining prominence across all segments. Quantitative indicators such as adoption shares and configuration turnaround efficiencies inform decision‑maker strategies for procurement cycles, space optimization, and long‑term asset management.

Among product types in the K‑12 furniture market, traditional student desks and chairs currently command the largest adoption share at approximately 38% due to their fundamental role across primary and secondary classrooms and broad compatibility with existing classroom layouts. Collaborative work tables account for around 27% of installations, valued for facilitating group activities and project‑based learning. Technology‑ready furniture—including desks with integrated device ports and cable management—is growing fastest, posting a 12% CAGR as schools modernize learning environments to support digital curricula. Other types, such as storage cabinets, teacher workstations, and specialty lab seating, collectively represent about 35% of the market, catering to niche requirements and space optimization efforts.

In application segmentation, standard classroom furnishing leads with an estimated 45% share, underpinning everyday instructional activities across general education settings. Library and media center applications contribute roughly 18%, emphasizing adaptable seating and integrated workstations for research and collaboration. STEM and science lab spaces follow with a 15% share, where specialized tables and chemically resistant surfaces support practical experimentation. Administrative and common areas like cafeterias and auditoriums comprise the remaining 22%, with tailored seating and service‑oriented furniture. Project‑based learning spaces are the fastest‑growing application, reflecting shifts toward flexible pedagogy and requiring reconfigurable tables and seating that support diverse instructional modalities.

Public school systems represent the leading end‑user segment with about 52% share, driven by large student populations and district‑wide furnishing programs that standardize classroom environments. Private institutions hold around 22% of total installations, emphasizing premium finishes and customizable layouts to align with institutional branding and pedagogical models. Charter and alternative schools account for an estimated 14%, often adopting modular and multi‑purpose furniture to maximize limited space. Early childhood education centers and special needs facilities comprise the remaining 12%, focusing on age‑appropriate and accessibility‑oriented designs. The fastest‑growing end‑user segment is charter schools, with an 11% CAGR as flexible learning spaces and innovative classroom models gain traction.

North America accounted for the largest market share at 43% in 2024, however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of approximately 8.1% between 2025 and 2032.

In 2024, North America’s dominance was reflected in over 2.58 billion USD worth of K‑12 furniture demand, underpinned by extensive infrastructure funding, widespread adoption of ergonomic and modular classroom solutions, and rapid modernization of public and private school facilities. Europe followed with around 25–30% regional share, driven by sustainability mandates and inclusive classroom design policies adopted in Germany, the UK, and France. Asia‑Pacific’s rising consumption is highlighted by rapid school construction and government educational reforms in China and India, where an increasing number of schools adopted modular and tech‑ready furniture systems. Latin America and Middle East & Africa together contributed the remaining 10–15% share, with Brazil, Mexico, UAE, and Saudi Arabia showing increased procurement activity tied to urban school expansion and digital‑ready classrooms. Classroom modernization initiatives, ergonomic criteria, and modular design preferences significantly shape procurement, positioning Asia‑Pacific for accelerated share expansion in the coming decade.

How are ergonomic and tech‑enabled classroom designs reshaping procurement strategies?

North America holds approximately 43% market share of global K‑12 furniture demand in 2024. Demand is driven by large-scale school modernization programs, particularly in the United States, which supplies millions of ergonomic desks and chairs annually and leads adoption of digital-ready furniture. Key industries such as education technology integration and public sector infrastructure funding propel demand, with government programs allocating capital toward learning environment upgrades and flexible classroom layouts. Regulatory emphasis on safety, accessibility, and sustainability standards has increased procurement of low-VOC materials and modular systems, with an estimated 64% of schools upgrading traditional furniture between 2018–2023. Technological advancements include smart desks with integrated charging and cable management support for digital tools in classrooms. Local players are tailoring product lines to meet district specifications and modular layout requirements. Regional consumer behavior shows higher adoption of ergonomic and digital-ready systems in urban school districts, while rural schools prioritize durable and cost-effective seating solutions.

What drives sustainability and adaptive design in modern classrooms?

Europe accounts for about 25–30% of the global K‑12 furniture market, with Germany, the UK, and France as prominent contributors. Regulatory bodies across the European Union emphasize eco-compliance and inclusive educational environments, resulting in over 72% of schools procuring eco-certified furniture and accessibility-focused designs. Adoption of technology-integrated furniture is increasing, with digital classroom setups gaining traction in urban and suburban districts. Local manufacturers are enhancing portfolios to include modular seating, adjustable tables, and multi-purpose layouts that align with sustainability mandates. Consumers in Europe exhibit strong preferences for recyclable materials and products that adhere to green procurement policies, driving trends toward adaptive classroom furniture. Many school districts implement smart desks and collaborative learning stations to support blended teaching models, reflecting nuanced regional behavior where regulatory pressures and eco-design standards strongly influence purchasing decisions.

How are infrastructure investments and student population growth shaping demand?

Asia-Pacific is a rapidly expanding K‑12 furniture market, with significant consumption volumes led by China, India, and Japan. Regional trends show wide adoption of modular and ergonomic solutions, with China reporting over 70% of schools integrating such designs and India recording approximately 65% adoption of eco-friendly furniture. Infrastructure expansion tied to rising student populations and government education reforms is a key factor driving deployment of classroom, lab, and library furniture systems. Regional tech trends include digital-ready desks and collaborative learning stations tailored for modern pedagogies. Local players and domestic manufacturers focus on scalable production and distribution to meet demand from both public and private institutions. Consumer behavior in Asia-Pacific leans heavily on cost-efficient, space-adaptive products purchased through both traditional channels and growing e-commerce platforms, particularly in urbanized regions.

What influences classroom furniture procurement in emerging South American markets?

South America’s K‑12 furniture landscape is shaped by activity in Brazil and Argentina, where school infrastructure upgrades and public education reforms have increased demand for durable and ergonomic seating. The region captures around 8–10% of global share, with Brazil’s urban school modernization fueling local procurement of modular desks and storage solutions. Trade policies that incentivize domestic manufacturing and cross-border partnerships support import of tech-ready furniture. Government incentives for educational facility improvements encourage investment in collaborative learning environments, while consumer behavior varies by economic conditions; urban districts prioritize modular and digital-compatible furniture, whereas rural areas emphasize cost-effective and sturdy traditional desks and chairs. Growth in private schooling also contributes to demand for customizable classroom setups.

How are modernization and private sector investments transforming classrooms?

The Middle East & Africa region holds approximately 5–10% of the global K‑12 furniture market, with major demand centers in the UAE, Saudi Arabia, and South Africa. Regional trends focus on modernization of educational facilities, increased school enrollment, and adoption of ergonomic designs. Investments from government and private schools have led to 61% of schools in some Middle Eastern markets upgrading traditional wooden furniture to modular designs. Technological modernization includes integration of digital-ready desks and collaborative spaces, responding to consumer preferences for contemporary classroom layouts. Local players are expanding product offerings to include customizable seating and eco-friendly materials, adapting to regional regulatory frameworks and trade partnerships that emphasize quality and compliance. Behavioral variation shows gulf nations investing in premium solutions, while African markets balance modernization with cost-effective procurement.

• United States – ~18–43% market share: High production capacity and extensive public school infrastructure investment drive sustained demand for ergonomic and digital-ready furniture.

• China – ~16–28% market share: Massive student population and school construction activity underpin strong adoption of modular and tech-integrated furniture systems.

The competitive environment in the K‑12 Furniture market is characterized by a mix of established multinational manufacturers and regional specialists, resulting in a moderately consolidated landscape where the top five companies collectively hold an estimated 35–40% combined share of global activity. There are well over 50 active competitors, including global giants and niche players focused on ergonomic, modular, and tech‑enabled educational furniture solutions. Market leaders are strategically positioned through diversified product portfolios, innovation pipelines, and geographic reach. For example, several Tier 1 players have launched modular, digital‑ready furniture lines in the past 2–3 years, enhancing flexibility and classroom adaptability. Competitive initiatives include partnerships with institutional buyers, co‑development agreements with educational technology firms, and targeted acquisitions of regional producers to expand distribution channels and localized manufacturing capacity. Innovation trends emphasize sustainable materials, adjustable ergonomic designs, and integration with digital learning environments that support collaborative pedagogy. Companies are increasingly investing in R&D, with reported double‑digit increases in design patent filings and smart furniture variants introduced annually. Smaller and mid‑tier manufacturers are leveraging niche specialization and cost competitiveness to capture regional demand, particularly in emerging Asia‑Pacific and Latin American markets. Overall, competitive dynamics are shaped by product differentiation, strategic alliances, and sustained innovation focus to address evolving institutional procurement criteria.

Smith System

Virco Mfg. Corporation

School Specialty

ECR4Kids

Global Furniture Group

Gopak

Agati Inc.

Ballen Panels Ltd.

Chongqing Equipment Co. Ltd.

Empire Furniture

The K‑12 furniture market is undergoing a significant transformation driven by the integration of advanced technologies that enhance classroom functionality and student engagement. Smart desks equipped with embedded charging ports, cable management systems, and connectivity hubs are now present in over 48% of newly constructed classrooms in North America and Europe, supporting digital learning ecosystems. Modular furniture with adjustable height and reconfigurable layouts leverages precision engineering and automated manufacturing techniques, reducing installation time by up to 30% and allowing schools to quickly adapt classroom setups for collaborative or individualized learning.

Emerging technologies include interactive furniture with touch-enabled surfaces and integrated whiteboards, which have been deployed in approximately 15% of STEM and STEAM classrooms in Asia-Pacific, improving student interaction and project-based learning efficiency. Sensor-enabled seating and desks track usage patterns, ergonomics, and classroom occupancy, providing facility managers with actionable data to optimize space utilization and furniture maintenance schedules. AI-powered design tools are increasingly being used to create customized layouts that meet specific pedagogical and accessibility requirements, reducing planning cycles by 25% compared to traditional design methods.

Sustainability-focused innovations are also influencing technology adoption, with over 42% of K-12 institutions implementing furniture produced with low-emission, recyclable materials combined with smart manufacturing processes that minimize waste. Additionally, digital twin simulations and virtual reality planning are used to visualize classroom arrangements before physical installation, ensuring optimal spatial efficiency. Overall, the convergence of digital, ergonomic, and sustainable technologies is reshaping the K‑12 furniture market, enabling more adaptive, efficient, and engaging learning environments while supporting institutional compliance and operational optimization.

• In March 2024, Steelcase expanded its K‑12 offerings by launching the FlexEd modular classroom furniture line, resulting in deployment of over 40,000 units across U.S. schools to support adaptable learning spaces and flexible classroom layouts.

• In January 2024, VS America secured a significant contract to furnish 700 California schools with 1.2 million furniture units, reinforcing its institutional footprint and capacity to supply high‑volume educational facilities.

• In September 2023, Smith System introduced noise‑canceling study pods, distributing approximately 3,400 units globally to address focused study zones and acoustical classroom needs.

• In June 2023, Jirong Furniture inaugurated an 80,000 sq. ft. manufacturing facility in China, scaling export capacity and supporting broader distribution of education furniture across domestic and international markets.

The scope of the K‑12 Furniture Market Report encompasses a comprehensive analysis of product types, application areas, end‑user segments, regional distributions, and technological impact on educational furniture procurement and deployment. Product type segmentation within the report includes traditional classroom desks and chairs, collaborative and modular tables, storage solutions, tech‑integrated workstations, ergonomic seating options, and specialized lab furnishings tailored for STEM and STEAM environments. Application categories cover general classrooms, libraries, laboratories, administrative spaces, common areas, and multi‑purpose learning hubs, each with insights into configuration needs and functional priorities.

Geographically, the report analyzes performance across North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, highlighting variations in procurement patterns, institutional investment policies, regulatory compliance frameworks, and consumer behaviors. It also details how specific regions emphasize sustainability mandates, inclusive design criteria, and digital learning support systems in their purchasing decisions. End‑user segmentation focuses on public school districts, private and international schools, charter institutions, early learning centers, and facilities with special‑needs requirements, with data capturing adoption patterns and procurement drivers across these categories.

The report further explores technological dimensions such as smart and digital‑ready furniture, sensor‑enabled seating, adjustable and reconfigurable systems, and AI‑assisted design and planning tools that shape product innovation and buyer preference. Emerging niches such as accessible and adaptive designs for neurodiverse learners, furniture‑as‑a‑service (FaaS) models, and integrated digital learning ecosystems are also assessed. Designed for decision‑makers and industry professionals, the report synthesizes these segments with analytical clarity, offering actionable insights into evolving strategies, competitive positioning, and future trajectories in the global K‑12 furniture landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 93805.74 Million |

|

Market Revenue in 2032 |

USD 142874.37 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Steelcase Inc., Herman Miller Inc., KI Furniture, Smith System, Virco Mfg. Corporation, School Specialty, ECR4Kids, Global Furniture Group, Gopak, Agati Inc., Ballen Panels Ltd., Chongqing Equipment Co. Ltd., Empire Furniture |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |