Reports

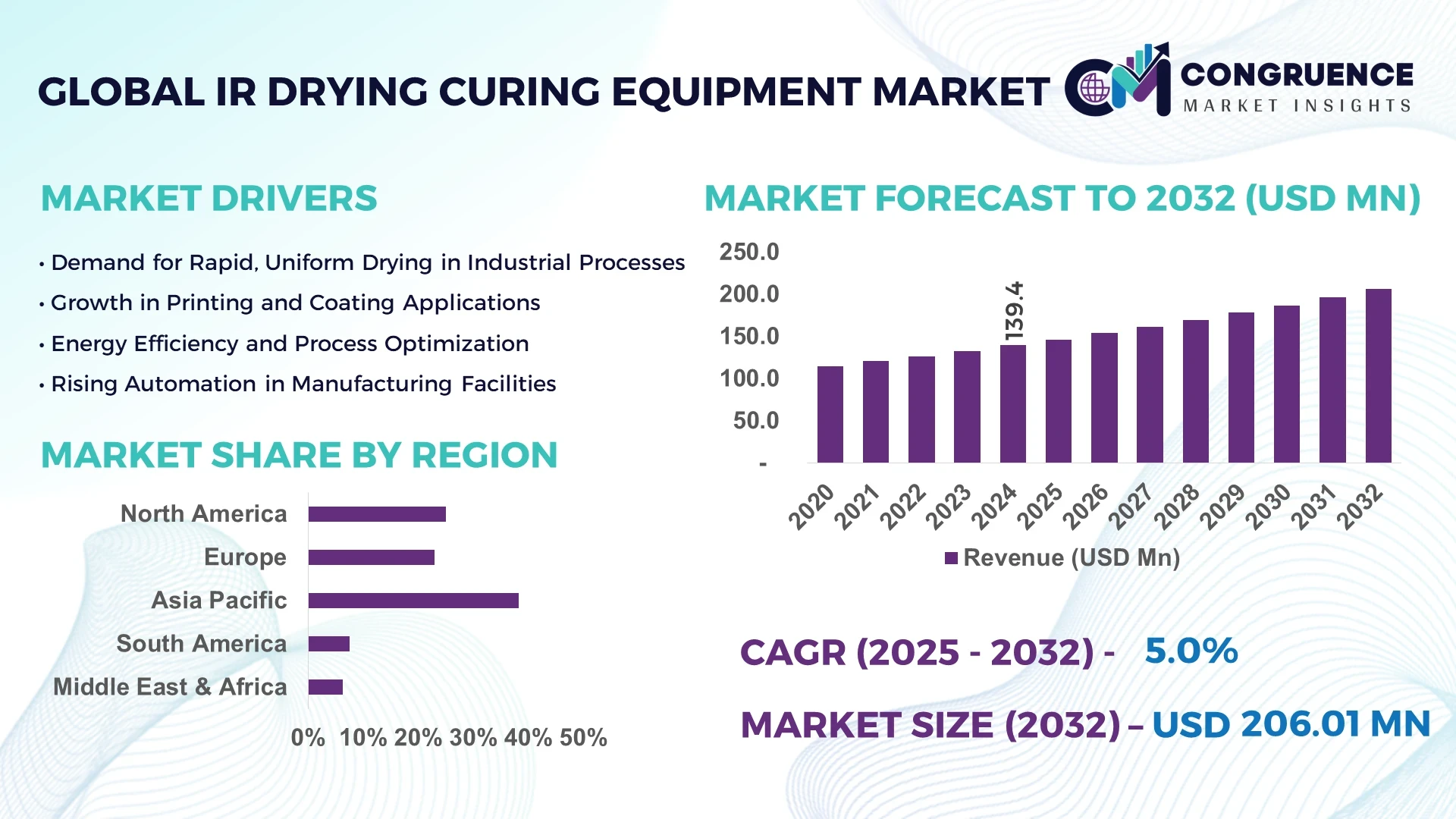

The Global IR Drying Curing Equipment Market was valued at USD 139.44 Million in 2024 and is anticipated to reach a value of USD 206.01 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032.

Germany, known for its robust industrial manufacturing base, leads in the production of IR drying curing systems. The country boasts state-of-the-art automation facilities, with high capital investment in thermal process technologies, particularly serving sectors like automotive coatings, printed electronics, and food processing lines. These facilities are often powered by energy-efficient infrared modules with advanced sensor integration.

The IR Drying Curing Equipment Market is experiencing notable momentum driven by increasing demand across industries such as automotive, pharmaceuticals, paper & pulp, textiles, and electronics. Automotive OEMs and aftermarket players are increasingly adopting IR curing technologies to speed up paint drying times, reduce VOC emissions, and enhance coating durability. Similarly, electronics manufacturing benefits from IR solutions in printed circuit board (PCB) curing, where precise heat control and rapid processing are critical. Environmental regulations have also pushed industries toward clean drying methods, favoring IR over traditional hot-air drying. Innovations like shortwave IR emitters and hybrid curing systems that combine UV and IR are further revolutionizing applications. Additionally, rapid urbanization and industrial automation in Asia-Pacific are accelerating regional adoption. The future outlook suggests a significant shift toward smart IR curing systems integrated with data-driven performance monitoring and adaptive control technologies.

Artificial Intelligence (AI) is playing a pivotal role in enhancing the operational capabilities of the IR Drying Curing Equipment Market. With increasing pressure on industries to reduce energy consumption while maintaining high throughput, AI integration is revolutionizing how drying and curing systems operate. AI-driven infrared systems now utilize predictive algorithms to optimize heat output, ensuring uniform drying while reducing material wastage and system downtimes. These smart systems also adapt to variations in humidity, material density, and surface coating in real time, significantly improving efficiency and product quality.

Manufacturers are embedding AI into IR curing equipment to enable predictive maintenance, which identifies component fatigue or irregular heating patterns before failures occur. This not only extends equipment lifespan but also lowers maintenance costs. AI is also instrumental in streamlining production workflows in sectors such as packaging, automotive, and textile, where speed and consistency are paramount. Through real-time data analysis and machine learning, AI-enhanced IR dryers can automatically adjust exposure duration, intensity, and temperature, eliminating the need for manual recalibration.

Moreover, AI is supporting the shift towards Industry 4.0 by enabling interconnectivity between IR curing systems and broader production networks, making it easier to integrate into smart factories. These advancements are not only improving system responsiveness and energy efficiency but also providing manufacturers with valuable insights into operational trends and performance optimization opportunities. The result is a smarter, more responsive IR Drying Curing Equipment Market capable of meeting evolving industrial demands with greater precision and sustainability.

“In March 2024, a leading thermal systems manufacturer introduced an AI-powered IR curing unit for printed electronics, capable of reducing drying time by 35% while improving coating uniformity by 22% across flexible substrates. The system uses adaptive machine learning to modulate IR wave intensity based on real-time surface feedback, significantly enhancing throughput for high-speed production lines.”

As industrial automation accelerates globally, manufacturers are increasingly adopting IR Drying Curing Equipment for its ability to deliver precision-controlled heat with minimal energy loss. Compared to conventional hot-air systems, infrared curing can reduce energy consumption by 30–50% due to its direct heating mechanism. This driver is particularly pronounced in automotive and electronics manufacturing, where rapid, uniform drying of coatings and adhesives is essential to maintain production line efficiency. With the push toward net-zero emissions, industries are prioritizing sustainable thermal solutions, making IR technology a top choice. Additionally, the increasing integration of programmable logic controllers (PLCs) and smart sensors into IR systems allows for automated adjustment of heat intensity and timing, optimizing throughput and minimizing waste. This demand for automation and operational efficiency is expected to further accelerate adoption in both developed and developing industrial sectors.

Despite its advantages, the IR Drying Curing Equipment Market faces significant barriers due to the high upfront costs associated with advanced IR systems and limited awareness in certain regions. Many small and medium-sized enterprises (SMEs), especially in developing countries, are unaware of the long-term benefits and energy savings offered by infrared technology. They continue to rely on older convection drying methods due to budget constraints and insufficient technical knowledge. Additionally, installation of modern IR curing systems often requires specialized setup, calibration, and employee training, adding to the initial investment burden. These challenges hinder the broader penetration of IR technology across industries such as textiles, food processing, and wood finishing, where cost sensitivity is high and ROI timelines are tightly scrutinized.

Emerging economies across Asia-Pacific, Latin America, and parts of Eastern Europe are witnessing a surge in industrial investments aimed at upgrading manufacturing facilities. This trend presents a significant opportunity for the IR Drying Curing Equipment Market. As governments incentivize energy-efficient infrastructure, industries are exploring advanced curing solutions that can enhance productivity while meeting strict environmental standards. Countries like India, Vietnam, and Mexico are witnessing new production lines in electronics, textiles, and automotive components, where compact and efficient IR systems are being adopted. The growing emphasis on “Make in India” and similar initiatives has opened up channels for local assembly and deployment of IR equipment, fostering both domestic demand and export potential. This favorable policy environment, paired with increased funding for smart factory technologies, is creating lucrative avenues for global IR system manufacturers to expand their reach.

One of the primary challenges in the IR Drying Curing Equipment Market is the high degree of customization required for different industrial applications. IR systems must be tailored to suit specific material properties, heating zones, wavelength needs, and spatial configurations. This variability complicates mass production and extends delivery timelines for both standard and bespoke units. Moreover, the lack of global standards in IR curing technology poses integration issues, especially when coordinating with other smart manufacturing systems. Industries face difficulties in benchmarking performance, troubleshooting system errors, and ensuring compatibility with upstream or downstream automation lines. These complexities can deter potential adopters who seek quick, standardized solutions, and they increase reliance on skilled technicians for ongoing system optimization.

• Rise in Modular and Prefabricated Construction: The growing trend of modular construction has significantly increased the demand for fast, uniform, and energy-efficient drying and curing systems. IR Drying Curing Equipment is now integrated into automated off-site production lines for prefabricated components like wood panels, steel modules, and insulation materials. In Europe and North America, the adoption rate of modular building systems rose by over 18% from 2022 to 2024, boosting the need for compact IR systems capable of delivering precise and repeatable curing for coatings and adhesives applied in factory settings.

• Integration of Smart Sensors and Real-Time Monitoring: Manufacturers are increasingly deploying IR Drying Curing Equipment equipped with smart sensors that monitor temperature, moisture levels, and material characteristics in real time. These systems adjust IR intensity dynamically to improve accuracy and reduce heat waste. This innovation has led to a 25% improvement in process efficiency across industrial lines using intelligent monitoring solutions, especially in food processing and electronics applications where drying precision is crucial.

• Increased Use of Hybrid IR and UV Systems: A notable trend is the rise in hybrid IR-UV curing systems, which combine the speed of IR heating with the depth-curing ability of UV light. These systems are becoming more common in sectors such as automotive coatings, where complex substrates require multi-layer curing. Adoption of hybrid systems has grown by 30% in niche sectors over the past two years, driven by the need for faster cycle times and higher curing uniformity.

• Growth in Eco-Friendly, Low-Emission Solutions: Due to tightening global environmental regulations, industries are shifting toward eco-friendly IR Drying Curing Equipment. These systems use short-wave IR and advanced reflectors to maximize energy usage and minimize emissions. The introduction of low-emission IR equipment has grown substantially, especially in regions like Japan and South Korea, where energy regulations are strict. Many plants report a reduction of over 20% in energy use after upgrading to environmentally optimized IR solutions.

The IR Drying Curing Equipment Market is segmented into types, applications, and end-user industries, each playing a critical role in shaping overall demand. In terms of type, advancements in near and far infrared systems are reshaping product offerings, with modular and compact equipment gaining momentum. Applications span across coatings, adhesives, inks, textiles, and food packaging, with electronics and automotive being the most prominent users due to their high-speed processing needs. Among end-users, manufacturing sectors such as automotive, electronics, and pharmaceuticals dominate equipment utilization, thanks to their reliance on precise, fast, and clean thermal processing. Additionally, smaller industrial workshops and contract processors are entering the space, encouraged by the availability of lower-cost, energy-efficient IR solutions. These segmented insights help technology providers better align their product development and service offerings to specific industrial requirements.

Short-wave IR Drying Curing Equipment remains the most widely adopted type due to its ability to rapidly heat surface-level coatings and inks in automotive and printing applications. These systems are favored for their quick response time and high thermal efficiency. Medium-wave IR systems are growing in relevance for textile and plastics processing, offering balanced penetration and moderate surface heating. However, far-infrared systems are currently experiencing the fastest adoption rate, especially in sensitive drying applications such as pharmaceuticals and food products, where gentle, uniform heating is essential to prevent degradation. Continuous product innovation, including modular emitters and plug-and-play IR modules, is expanding the adoption of portable and space-saving IR equipment across diverse manufacturing lines. While some segments require high-intensity systems for fast processing, others prefer programmable systems with adjustable wave ranges to handle complex materials.

Automotive surface coating and drying hold the leading position in application, due to the necessity of consistent, high-speed curing for primers, base coats, and finishes. The precision and efficiency of IR systems reduce cycle times and lower defect rates, which is crucial in lean automotive manufacturing environments. Electronics manufacturing is emerging as the fastest-growing application segment, where IR Drying Curing Equipment is used in circuit board drying and encapsulant curing. The need for non-contact, localized heating without compromising sensitive components is fueling this trend. Additionally, the textile and printing industries continue to rely on IR equipment for ink and dye fixation, particularly in roll-to-roll processing. Food packaging is also a notable application, as IR heat enables rapid sealing and sanitization of plastic and foil surfaces without chemical intervention. Each application area presents distinct heating requirements, driving further diversification in IR technology offerings.

The manufacturing sector, particularly automotive and industrial electronics, is the dominant end-user of IR Drying Curing Equipment. Their need for precision-controlled, rapid thermal processing makes infrared systems a cost-effective solution for enhancing production throughput and quality control. The electronics sector is currently the fastest-growing end-user group, driven by increasing investments in semiconductor packaging, flexible electronics, and wearable devices. These processes often demand ultra-precise heat control that only advanced IR technology can deliver. The pharmaceutical industry is also investing in IR-based systems for capsule drying and surface sterilization, where non-contact heat offers hygienic processing advantages. Additionally, food and beverage manufacturers use IR curing for drying labels, containers, and packaging films. With growing energy-efficiency goals and tighter compliance mandates, a broader range of mid-sized manufacturers is turning to modular IR equipment that aligns with sustainability and operational excellence targets.

Asia-Pacific accounted for the largest market share at 38.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2025 and 2032.

The Asia-Pacific region leads the IR Drying Curing Equipment Market due to substantial infrastructure development, high-volume manufacturing, and widespread industrial applications across China, India, and Southeast Asia. Significant investments in smart factories and government-backed initiatives promoting industrial automation continue to fuel market momentum. The widespread deployment of IR systems in automotive, electronics, and textile sectors is strengthening equipment demand. Meanwhile, North America is projected to witness accelerated growth driven by rapid digital transformation in manufacturing, stricter environmental regulations encouraging energy-efficient drying systems, and increased adoption in pharmaceuticals and defense manufacturing. Across all regions, a growing preference for precision-controlled thermal processing technologies, along with modular system installations, is influencing adoption patterns. Countries are also ramping up production capacities and exploring innovations in hybrid IR systems, aiming to improve energy efficiency and throughput while meeting sector-specific drying requirements.

High-Precision IR Equipment Adoption Accelerates Across Industries

North America held a market share of 24.6% in 2024, supported by robust demand from automotive, aerospace, and defense sectors. The regional expansion of industrial automation and smart factory initiatives has further fueled demand for energy-efficient IR Drying Curing Equipment. The U.S. remains the leading contributor, driven by advancements in short-wave IR systems for high-speed coating and adhesive curing. Notably, the introduction of incentives under clean manufacturing programs has led to wider deployment of eco-efficient drying equipment. Regulatory bodies are encouraging manufacturers to invest in low-emission curing technologies, which has resulted in an 18% increase in new system installations since 2022. Additionally, digital transformation strategies across food processing and electronics manufacturing are reshaping equipment configurations to allow real-time thermal control, predictive maintenance, and modular flexibility.

Green Policies and Hybrid Technology Adoption Drive Growth

Europe accounted for 21.4% of the IR Drying Curing Equipment Market in 2024, with strong contributions from Germany, the United Kingdom, and France. The region’s emphasis on green manufacturing policies and net-zero targets has pushed companies to adopt infrared drying systems with reduced environmental impact. Germany has emerged as a center for technological innovation, with firms integrating hybrid IR-UV solutions to meet multi-process industrial needs. The UK and France continue to show high demand for IR equipment in printing, packaging, and pharmaceuticals. The European Commission’s energy efficiency directives are accelerating the replacement of conventional dryers with low-energy IR alternatives. In addition, research funding from Horizon Europe and local green manufacturing initiatives are fostering pilot installations of AI-integrated infrared systems that offer energy savings and precise control across varying industrial substrates.

Manufacturing Expansion and Automation Fuel Market Leadership

With the largest market share of 38.2% in 2024, the Asia-Pacific region is driven by dynamic industrial growth, especially in China, India, Japan, and South Korea. China leads consumption, supported by vast production lines across electronics, textiles, and packaging industries. India is quickly emerging as a manufacturing hub due to low labor costs and incentives for capital investment in industrial automation. Japan, with its focus on high-tech innovation, is adopting compact IR systems for use in precision electronics and medical equipment. Manufacturing growth is supported by large-scale infrastructure projects, advanced robotics integration, and the proliferation of smart manufacturing plants. The region is also witnessing investments in eco-friendly infrared systems that align with emerging environmental standards, offering companies competitive advantages in global trade.

Government Incentives and Construction Projects Bolster Demand

South America contributed 6.5% to the global IR Drying Curing Equipment Market in 2024, with Brazil and Argentina being the principal markets. The Brazilian government has introduced policies aimed at upgrading industrial energy efficiency, which is fostering the adoption of infrared curing systems in packaging and construction materials processing. Infrastructure growth across Argentina is driving demand for modular IR drying units, particularly in cement board and drywall fabrication. Additionally, the region's push to localize manufacturing has led to capacity expansions in electronics and automotive assembly. These industries are increasingly integrating IR Drying Curing Equipment to reduce drying time and optimize operational costs. With regional free trade agreements lowering import tariffs, access to next-generation drying technologies is improving, further stimulating adoption in both mid-sized and large enterprises.

Oil & Gas Projects and Tech Upgrades Spur Industrial Adoption

The Middle East & Africa region contributed 4.3% of global IR Drying Curing Equipment demand in 2024, driven by expansion in construction, petrochemical, and energy sectors. The UAE and Saudi Arabia are investing in large-scale industrial diversification programs like Vision 2030, prompting growth in sectors that require heat treatment solutions. South Africa, a key market, is modernizing its manufacturing base with energy-efficient IR solutions in mining and materials processing. Regulatory incentives supporting cleaner production technologies are further pushing adoption, especially in drying and curing coatings applied in harsh environments. Innovations in durable, high-temperature IR equipment tailored for heavy industrial use are gaining traction. Increased regional trade partnerships and infrastructure investments are expected to sustain momentum, even in traditionally underserved markets.

China – 26.3% market share

High production capacity and strong industrial infrastructure across multiple sectors including electronics, textiles, and construction.

United States – 21.7% market share

Strong end-user demand in automotive, aerospace, and pharmaceutical manufacturing supported by advanced automation technologies.

The IR Drying Curing Equipment Market features a moderately consolidated competitive environment, with over 45 active global and regional manufacturers offering specialized solutions across diverse industries. Competition is shaped by the demand for innovation in energy-efficient systems, compact design adaptability, and integration with digital manufacturing platforms. Leading companies are focused on strategic product development, with over 30% of market players having launched AI-enhanced or hybrid infrared systems between 2023 and 2025. Partnerships with automation firms and material handling companies are on the rise, enabling vendors to offer turnkey drying and curing solutions suited for industrial 4.0 environments.

Several companies are enhancing their geographic footprint through targeted acquisitions, especially in Southeast Asia and Eastern Europe, where demand for cost-effective drying technologies is increasing. In terms of product strategy, modular, customizable IR systems are gaining popularity, especially among OEMs in electronics, automotive, and packaging sectors. Additionally, a growing number of manufacturers are emphasizing sustainability by incorporating recyclable components, advanced insulation, and low-energy IR emitters. As digital transformation and green regulations intensify, competitive positioning in the IR Drying Curing Equipment Market is now closely tied to technological leadership, after-sales service capability, and regional adaptability.

Heraeus Noblelight GmbH

GEW (EC) Limited

Vulcan Catalytic Systems

Fannon Products, LLC

Eltosch Grafix GmbH

Emit Inc.

Solaronics Inc.

Casso-Solar Technologies LLC

Red-Ray Manufacturing Company

BBC Industries, Inc.

Technological innovation in the IR Drying Curing Equipment Market is reshaping the operational efficiency, precision, and sustainability of industrial drying processes. One of the key advancements includes the integration of near-infrared (NIR) and medium-wave infrared (MWIR) emitters, which enable faster and more uniform heating for substrates in electronics, automotive coatings, and flexible packaging. These emitters are being optimized for instant on/off capabilities and targeted wavelength emissions, which reduce energy wastage and processing times by up to 30%.

The rise of smart control systems, equipped with AI-driven sensors and machine learning algorithms, allows real-time monitoring and adaptive process optimization. Manufacturers are leveraging these tools to improve product consistency and reduce material defects, especially in temperature-sensitive operations like medical device manufacturing and printed circuit board (PCB) drying. For instance, digital twin technology is now being adopted in high-capacity curing lines, enabling predictive maintenance and reducing downtime by approximately 20%.

Another significant development is the shift towards eco-friendly IR systems using ceramic and quartz-based heating elements. These units are designed to minimize emissions while delivering precise thermal profiles. Moreover, automation and robotics are being integrated into IR drying systems, particularly in food packaging and textile finishing lines, to increase throughput and maintain hygiene standards. These innovations reflect a trend toward intelligent, sustainable, and high-precision IR drying solutions that align with the evolving demands of modern manufacturing environments.

• In April 2024, Heraeus Noblelight launched its new high-performance NIR system designed for rapid moisture evaporation in battery electrode drying. The system reduced drying time by 40% while improving energy efficiency through automated sensor controls in lithium-ion battery production.

• In December 2023, BBC Industries unveiled a compact tabletop IR curing unit targeted at the screen-printing industry. Designed for small and mid-size businesses, the unit supports curing speeds up to 900 shirts per hour and features modular heater arrays for cost-effective scalability.

• In August 2024, GEW (EC) Limited expanded its LeoLED product line with enhanced IR modules for wide-web printing applications. These modules provide peak output at 365 nm with improved heat dissipation, enabling smoother curing on high-speed flexographic presses.

• In February 2023, Solaronics introduced an AI-integrated control interface for its IR drying systems, allowing real-time adjustment of drying parameters based on substrate feedback. This upgrade has resulted in a 25% reduction in thermal variation during multi-shift operations across food processing facilities.

The IR Drying Curing Equipment Market Report offers an in-depth evaluation of the global industry landscape, covering key technological, application-specific, and regional developments that shape demand and supply dynamics. This report examines the full spectrum of infrared-based drying and curing solutions, including short-wave, medium-wave, and near-infrared technologies, with analysis spanning across fixed and modular configurations. It explores advanced features such as intelligent control systems, AI-integrated process automation, and energy-efficient emitter designs that are now being deployed across various industrial environments.

The market segmentation assessed in the report includes product types such as conveyor-based, chamber-style, and tunnel-type IR systems. Applications analyzed span diverse sectors including automotive coatings, electronics manufacturing, food packaging, pharmaceuticals, textiles, and printed circuit boards. Each segment is studied for its current volume contribution, growth trajectory, and technological adaptation, particularly in high-throughput or temperature-sensitive processes.

Geographically, the report evaluates demand trends across five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—while also highlighting key country-level developments in markets like the United States, China, Germany, and India. It additionally identifies growth opportunities in emerging economies where industrial expansion and energy-efficient practices are driving demand for cost-effective and sustainable drying technologies. The report also delves into the strategic role of regulatory compliance, automation, and digital transformation in shaping future investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 139.44 Million |

|

Market Revenue in 2032 |

USD 206.01 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Quectel Wireless Solutions Co., Ltd., Telit Cinterion (formerly Telit Communications PLC), Sierra Wireless Inc., u-blox Holding AG, Thales Group (IoT Division), Fibocom Wireless Inc., Sunsea AIoT Technology Co., Ltd., Neoway Technology Co., Ltd., MultiTech Systems, Inc., Murata Manufacturing Co., Ltd., Laird Connectivity, Semtech Corporation, Cavli Wireless |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |