Reports

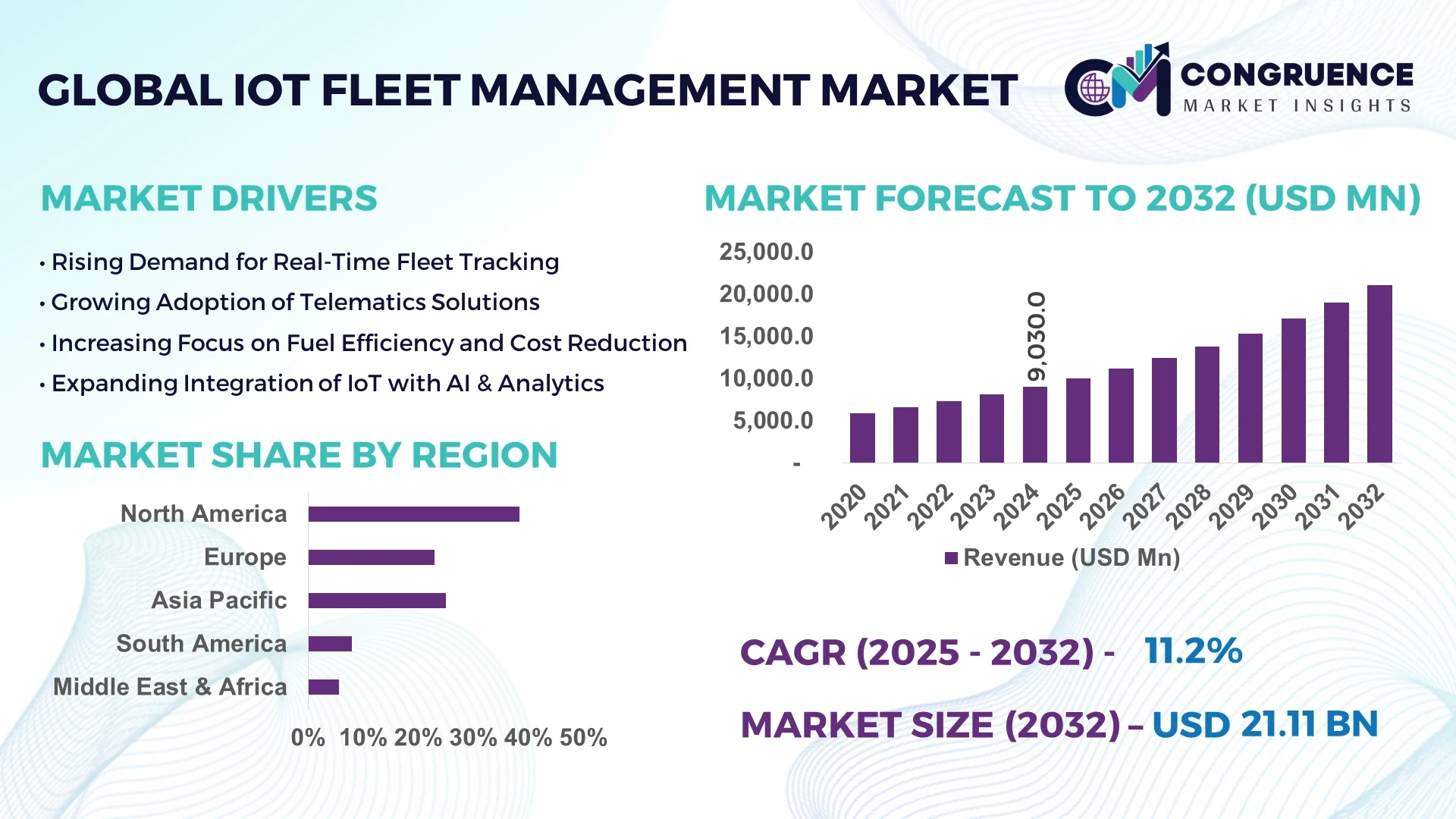

The Global IoT Fleet Management Market was valued at USD 9,030 Million in 2024 and is anticipated to reach a value of USD 21,111.8 Million by 2032 expanding at a CAGR of 11.2% between 2025 and 2032.

In the United States, leading the IoT Fleet Management Market, major fleet operators and telematics providers are investing heavily in large-scale deployment, edge analytics infrastructure, and vehicle-mounted IoT device manufacturing. Local development centers focus on integration with logistics, real-time data platforms, and AI-enabled analytics tailored to long-haul transportation and last-mile delivery networks, supporting advanced route optimization and predictive maintenance applications.

IoT Fleet Management Market segments span commercial transport, logistics & courier services, public transit, and utility fleets. Recent innovations include integration of edge computing telematics units, AI-driven route optimization modules, driver behavior analytics dashboards, and carbon emission tracking systems. Regulatory support for vehicle emissions monitoring and data-sharing mandates in several countries has driven fleets to adopt telematics. Economic factors like rising fuel costs and driver shortages have increased demand for efficiency gains. Regional usage patterns show heavy uptake in North America and Europe for long-haul trucking, while Asia-Pacific experiences rapid adoption in urban delivery services. Emerging trends include integration with 5G connectivity, blockchain-based maintenance recordkeeping, and federated learning models for secure analytics. Fleet operators and logistics firms are pursuing customized analytics, modular hardware, and cross-platform integration to remain competitive and resilient.

Artificial Intelligence is rapidly reshaping the IoT Fleet Management Market by embedding predictive analytics, computer vision, and adaptive decision-making into traditional telematics systems. AI-driven predictive maintenance tools can now analyze data from sensors measuring engine performance, fuel consumption, and brake patterns to forecast vehicle faults days in advance—reducing unscheduled downtime and extending service intervals. In driver monitoring, AI-enabled algorithms assess real-time video and sensor data to detect unsafe driving behaviors such as harsh braking or distracted driving, generating automated coaching alerts that improve safety compliance and reduce accident rates.

Furthermore, AI enables dynamic route optimization—by continuously analyzing traffic, weather conditions, delivery schedules, and vehicle load profiles, AI systems automatically adjust itineraries to reduce idle time and fuel usage. Integration of AI with edge IoT devices onboard vehicles allows low-latency decision-making without backhaul to central servers, improving operational performance and responsiveness in remote or low-connectivity environments. In the IoT Fleet Management Market, deployment of AI-powered dashboards and automated reporting systems has empowered fleet supervisors to monitor key fleet KPIs—such as on‑time delivery rates, fuel efficiency, and driver performance—via unified cloud-based platforms.

AI also enhances operational scalability by automating fleet compliance audits and predictive alerts for inspection schedules, enabling fleet operators to stay ahead of regulatory requirements. The IoT Fleet Management Market is increasingly embracing AI-driven telematics and digital platforms to transform reactive systems into proactive networks, driving measurable efficiency gains and cost reduction across large-scale vehicle operations.

“In 2024, Penske Truck Leasing deployed an AI-based system analyzing over 300 million telematics data points daily across its fleet, enabling early detection of mechanical anomalies and cutting unscheduled maintenance interventions by more than 25%.”

The IoT Fleet Management Market is shaped by trends in logistics automation, digital transformation of transportation, and regulatory requirements for safety and emissions. Growing pressure for efficient route planning, asset utilization tracking, and real-time performance monitoring drives adoption. Increasing use of edge computing and 5G connectivity enhances data processing capabilities within vehicles. Fleet size consolidation and software standardization are resulting in demand for scalable platforms. The integration of IoT hardware with AI analytics and cloud dashboards is providing decision-makers with centralized control over dispersed vehicle networks and remote assets. Cybersecurity, data privacy regulations, and interoperability standards are influencing vendor development practices. These dynamics create a rapidly evolving environment in which technical innovation, operations optimization, and compliance mandates converge to shape strategy in the IoT Fleet Management Market.

The demand for predictive maintenance within the IoT Fleet Management Market is intensifying. Fleet operators are installing advanced sensors and telematics modules on vehicles to continuously monitor engine diagnostics, brake wear, and tire pressure. Real‑time anomaly detection allows maintenance teams to proactively schedule servicing, resulting in substantial uptime reductions. For example, several operators have reported a 20 – 30% decrease in unexpected breakdowns and up to 15% longer operational availability. Predictive maintenance improves vehicle lifecycle costs, minimizes repair-related downtime, and enhances overall fleet reliability. These measurable benefits support investment in telematics and AI integration across commercial, logistic, and public transit fleets.

Despite proliferation of IoT fleet technologies, limited network coverage in remote or rural regions remains a key restraint. Many fleet operations in logistics corridors or rural transport routes face intermittent cellular signals or high roaming costs, causing data latency or loss. In addition, hardware installation costs—especially for legacy fleets—can be significant, and some vehicles lack power infrastructure to support heavy sensors or edge computing devices. These limitations slow deployment in rural logistics and intercity operations. Connectivity challenges also impact real-time tracking accuracy, predictive analytics timeliness, and driver monitoring reliability—critical components for fleet management platforms to deliver premium service levels.

The IoT Fleet Management Market is increasingly exploring edge-based AI and federated learning to enable distributed analytics while preserving data privacy. By deploying machine learning models at the edge within in-vehicle gateways, fleets can derive insights on maintenance, route efficiency, and driver behavior without transmitting sensitive data to central servers. Federated learning frameworks allow multiple vehicles or fleet locations to collaboratively train models while preserving data locality. This opportunity enables scalability in international deployments, supports compliance with privacy mandates, and reduces network bandwidth costs. Early adopters have reported up to 40% reductions in cloud data transmission and improved model responsiveness across distributed fleets.

A significant challenge in the IoT Fleet Management Market is the lack of unified standards across telematics hardware, sensor formats, and integration protocols. Fleet operators often need to integrate devices from different vendors, leading to compatibility issues, data inconsistencies, and difficult system integration. Lack of standard APIs and varying firmware versions can delay deployment, complicate maintenance, and increase support overhead. Integration with legacy dispatch, ERP, or maintenance software requires additional middleware or bespoke engineering. Without industry-wide interoperability standards, scaling integrated fleet solutions across multinational or multi-vendor environments remains complex and costly.

Surge in Video Telematics and AI-Driven Safety Monitoring: In 2024, fleets deploying AI-enabled video telematics systems increased by over 50% in North America, enabling automatic detection of risky driving patterns and delivering real-time alerts to improve driver safety and reduce insurance costs.

Centralization via Unified Fleet Management Platforms: Organizations adopting single-pane‑view cloud platforms for telematics, maintenance, compliance, and dispatch operations report 30‑40% reduction in manual data consolidation hours among fleet administrators, boosting productivity and strategic oversight.

Integration of 5G‑Capable IoT Devices and Edge Analytics: The deployment of 5G‑enabled telematics units in urban delivery fleets doubled year-over-year in several APAC cities, enabling sub-second data transmission, onboard decision-making, and low-latency route adjustments.

Expansion of Modular, Retrofit IoT Kits for Existing Fleets: Retrofit IoT module shipments increased by nearly 25% globally in 2024 as operators adopted plug‑and‑play kits to modernize older vehicles, enabling predictive maintenance, GPS tracking, and connectivity without full vehicle replacement.

The IoT Fleet Management Market is segmented based on type, application, and end-user, each playing a crucial role in shaping the market's overall dynamics. From a type perspective, key solutions include tracking and monitoring systems, route optimization tools, fuel management, remote diagnostics, and vehicle maintenance platforms. These components work in synergy to provide real-time visibility and operational control. On the application side, the market is structured around freight transportation, passenger transit, logistics services, and last-mile delivery operations. Each application category benefits from advancements in connectivity and analytics. The end-user spectrum is wide-ranging—covering commercial vehicle fleets, public transport agencies, logistics service providers, and utility service operators. Increasing demand for real-time data, compliance automation, and asset optimization has created nuanced needs across these segments. As businesses prioritize operational efficiency and regulatory adherence, segment-specific IoT fleet management solutions are being tailored to meet evolving industry requirements.

In the IoT Fleet Management Market, tracking and monitoring solutions represent the leading type, largely due to their role in enabling real-time location visibility, geofencing, and asset security. Fleet operators prioritize these systems to reduce theft risk, monitor route adherence, and ensure compliance with transportation regulations. These platforms often include GPS modules, integrated dashboards, and real-time alerts, forming the foundation of modern fleet operations.

Among the fastest-growing types are remote diagnostics and predictive maintenance systems. These solutions leverage sensor data and analytics to anticipate vehicle failures, thereby minimizing downtime and improving maintenance scheduling. Their growth is propelled by rising demand for uptime assurance, cost control, and enhanced safety protocols.

Other relevant types include fuel management systems, which help reduce fuel consumption through optimization algorithms, and driver behavior monitoring tools, which evaluate fatigue, speed, and safety compliance. Although these systems serve niche or supplementary purposes, they play a pivotal role in fine-tuning fleet efficiency and enhancing ROI across diverse fleet types.

Freight and cargo transportation is currently the dominant application in the IoT Fleet Management Market, driven by the sector’s need for real-time tracking, cargo safety, and regulatory compliance across long-haul and cross-border logistics. Advanced IoT solutions are being deployed to optimize load capacity, monitor cargo conditions, and track performance metrics at scale.

The fastest-growing application is last-mile delivery. Fueled by rapid e-commerce growth, urban mobility challenges, and evolving customer expectations, this segment demands high-frequency route optimization, dynamic dispatching, and proof-of-delivery systems. The use of IoT tools in this segment enables real-time updates, reduces delivery windows, and ensures customer satisfaction.

Other important applications include public transit and shared mobility, where IoT platforms are utilized to manage schedules, optimize routes, and improve passenger safety. In addition, utility fleets and field service vehicles are integrating IoT tools for scheduling optimization, fuel monitoring, and remote diagnostics. These diverse applications showcase the scalability and adaptability of IoT technologies across the transport ecosystem.

Logistics and transport service providers are the leading end-users in the IoT Fleet Management Market, owing to their extensive reliance on high-volume, real-time data analytics to manage large and dispersed fleets. These operators use IoT solutions to streamline dispatch operations, improve ETA accuracy, and monitor vehicle performance under varying conditions.

The fastest-growing end-user segment is e-commerce delivery services, particularly in urban areas. As online retail continues to expand, companies are deploying telematics and IoT platforms to meet tighter delivery schedules, improve last-mile efficiency, and provide end-to-end visibility. This surge is fueled by the rising demand for same-day or next-day delivery, customer tracking preferences, and fleet scalability requirements.

Other significant end-users include public transport authorities, utility service providers, and construction companies. Public sector fleets are adopting IoT platforms for safety, emissions tracking, and vehicle availability management. Meanwhile, utilities and industrial operators focus on maximizing asset uptime and operational reliability. Each of these segments contributes uniquely to the market’s robust and evolving structure.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.1% between 2025 and 2032.

The IoT Fleet Management Market in North America benefits from a mature logistics sector, early adoption of advanced telematics, and strong support from regulatory bodies mandating ELD (Electronic Logging Device) compliance. Meanwhile, Asia-Pacific is experiencing a surge in fleet digitization due to growing e-commerce, urban logistics demand, and infrastructure development. Countries such as China and India are investing heavily in smart transportation systems, supported by favorable policies and expanding 5G and IoT ecosystems. Additionally, technological hubs like Japan and South Korea continue to influence the regional innovation curve, enhancing demand for real-time fleet tracking, predictive maintenance, and route optimization solutions. These factors collectively make Asia-Pacific a high-potential region for future growth in the IoT Fleet Management Market.

North America held the dominant share in the global IoT Fleet Management Market in 2024, accounting for 38.4% of total market volume. This leadership position is driven by strong adoption of telematics in logistics, last-mile delivery, and public transportation sectors. The U.S. remains the core market, supported by regulatory enforcement of electronic logging devices (ELDs) and safety mandates. Additionally, Canada's smart transportation investments and Mexico’s expanding logistics infrastructure also contribute significantly. Key industries such as retail, e-commerce, and oil & gas are increasingly digitizing their fleets to cut operational costs and enhance supply chain visibility. Government initiatives around smart mobility and emissions reduction are further accelerating adoption. Cloud-based platforms, edge computing, and AI-integrated route planning tools are widely being adopted to enhance operational efficiencies. Overall, digital transformation and data-driven decision-making are core to the North American IoT fleet strategies.

Europe is one of the leading regions in the IoT Fleet Management Market, holding approximately 26.2% of the global share in 2024. Germany, the United Kingdom, and France are key markets propelling growth due to their advanced logistics infrastructure and strong regulatory backing. The European Union’s strict environmental policies, such as the Green Deal and carbon neutrality targets, have prompted logistics companies to adopt real-time tracking, fuel management, and predictive maintenance systems. Moreover, the region is embracing V2X (Vehicle-to-Everything) and smart city initiatives to optimize fleet operations. Regulatory frameworks such as the Euro VI emissions standard are pushing fleet modernization across Europe. Digital twins, AI-enabled fleet analytics, and blockchain-based compliance reporting tools are gaining traction, creating a robust ecosystem for intelligent fleet management. These innovations are further supported by EU-wide funding programs and industry collaborations aiming at reducing urban congestion and increasing freight reliability.

Asia-Pacific is emerging as the fastest-growing region in the IoT Fleet Management Market, led by economies such as China, India, and Japan. The region ranked first in growth momentum in 2024, driven by expanding urban delivery networks, rising vehicle ownership, and increasing logistics outsourcing. China leads with large-scale implementation of IoT in last-mile delivery and public transport, aided by its strong manufacturing ecosystem and AI capabilities. India follows closely, with a booming e-commerce sector, government-driven digitization (such as FASTag and AIS 140), and smart city investments boosting demand for connected fleets. Japan and South Korea are investing in autonomous vehicle fleets and sensor-based monitoring technologies to enhance transport efficiency. The integration of 5G, cloud-based fleet software, and cross-border freight networks further strengthens Asia-Pacific’s positioning. With regional governments supporting logistics digitization and emissions regulation, the market outlook remains highly promising.

South America’s IoT Fleet Management Market is gaining traction, particularly in Brazil and Argentina, which are leading regional players. Brazil’s logistics sector, supported by expansive road networks and trade volume, accounted for a sizable share of the market in 2024. The market is driven by growing investment in transportation infrastructure and demand for efficient cargo monitoring solutions. Argentina is following suit, especially in agriculture and mining sectors where connected fleet solutions optimize delivery and operational performance. Regional governments are promoting IoT adoption through tax incentives and digital economy policies. Technology providers are introducing affordable telematics systems suited for developing markets, facilitating market penetration. Additionally, sectors such as energy, agriculture, and logistics are increasingly adopting predictive maintenance and fuel tracking systems. Although still developing, the region's adoption of smart logistics solutions is on the rise, presenting opportunities for scalable IoT applications across fleets.

The Middle East & Africa region is witnessing steady growth in the IoT Fleet Management Market, with notable demand emerging from UAE, Saudi Arabia, and South Africa. Infrastructure projects, such as those linked to Vision 2030 and the African Continental Free Trade Area (AfCFTA), are fostering the need for smart fleet management. In the UAE and Saudi Arabia, the oil & gas sector is a primary adopter of IoT-based fleet tracking systems due to the need for safety and efficiency in remote operations. South Africa is digitizing its public and cargo transportation networks, leveraging IoT to improve fleet uptime and reduce theft. Regional governments are also forging partnerships to introduce regulations promoting connected mobility. Key trends include deployment of solar-powered tracking devices, AI-based driver monitoring, and integration of IoT in cold chain logistics. These advancements are facilitating greater transparency, sustainability, and operational efficiency across the region’s diverse fleet sectors.

United States – 32.7% Market Share

High telematics adoption, regulatory mandates, and digital-first fleet operations solidify the U.S. leadership in the IoT Fleet Management Market.

China – 21.5% Market Share

Robust logistics demand, e-commerce boom, and large-scale investment in AI and smart transportation infrastructure drive China’s dominance in the IoT Fleet Management Market.

The IoT Fleet Management Market is characterized by a moderately fragmented competitive environment with over 80 active global and regional players. Market participants range from established telematics providers to niche IoT solution developers, each striving for technological leadership and customer-centric innovations. Companies are focused on enhancing real-time analytics, cloud-native platforms, and predictive maintenance to differentiate themselves. Strategic initiatives such as collaborations between vehicle OEMs and software developers are increasing, enabling more integrated fleet solutions. Product launches remain a key strategy, particularly in AI-powered dashboard tools, driver safety systems, and route optimization modules. Mergers and acquisitions are prevalent, especially as leading firms aim to expand their geographic reach and technological capabilities. Key competitors are also investing in 5G and edge computing to improve latency and expand operational control. Furthermore, regional players in emerging economies are leveraging cost-effective solutions to penetrate underserved markets. The push for sustainability, compliance, and connected mobility continues to shape competitive dynamics globally.

Geotab Inc.

Trimble Inc.

Verizon Connect

Omnitracs, LLC

AT&T Inc.

TomTom Telematics

Zonar Systems, Inc.

MiX Telematics

Samsara Inc.

Orbcomm Inc.

Teletrac Navman

Fleet Complete

Gurtam

KeepTruckin Inc.

Inseego Corp.

The IoT Fleet Management Market is driven by a broad set of technologies that support fleet tracking, automation, diagnostics, and communication. Core technologies include Global Positioning System (GPS) and cellular-based connectivity (4G/5G), which are essential for real-time location and status tracking. The integration of edge computing is becoming increasingly important, enabling faster processing of data on the vehicle level, reducing latency, and improving responsiveness. Fleet management platforms are increasingly cloud-based, offering scalability and centralized control over large vehicle networks.

Artificial Intelligence (AI) and machine learning (ML) are transforming predictive maintenance, driver behavior analysis, and fuel optimization. AI-powered video telematics and in-cab cameras now allow for real-time coaching and safety alerts. Vehicle-to-Everything (V2X) communication is gradually being tested to facilitate connected infrastructure and collaborative mobility scenarios.

Blockchain is emerging in fleet contracts and compliance recordkeeping, while digital twins are being used for simulation and performance modeling. IoT sensors embedded in tires, engines, and trailers enable smart diagnostics, while Over-The-Air (OTA) software updates improve vehicle uptime and reduce service downtime. The convergence of Big Data analytics, cloud platforms, and AI is central to next-generation fleet orchestration strategies, providing companies with granular control over fuel use, route planning, maintenance, and compliance.

• In February 2024, Samsara Inc. launched its Camera Connector solution, allowing businesses to integrate third-party cameras with its existing dashboard, enhancing video visibility and fleet safety performance across different vehicle models.

• In March 2024, Verizon Connect expanded its platform to support AI-based anomaly detection in fleet fuel usage, helping businesses prevent theft and optimize route-level efficiency across large fleets.

• In August 2023, Trimble and Stellantis entered a collaboration to integrate Trimble's fleet telematics systems directly into Stellantis commercial vehicles, enabling factory-fit connectivity and seamless data access for fleet managers.

• In December 2023, Geotab announced the opening of a new data center in Germany to support regional data compliance requirements and expand its service availability across European commercial vehicle markets.

The IoT Fleet Management Market Report offers a comprehensive analysis of the global landscape of intelligent vehicle monitoring and fleet optimization technologies. It covers a wide spectrum of segments including vehicle types (light, medium, heavy-duty fleets), deployment models (cloud-based, on-premise), and components (hardware, software, and services). Key application areas assessed in the report include driver management, vehicle tracking, fuel management, predictive maintenance, asset monitoring, and safety compliance.

The report provides detailed geographic coverage, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting region-specific trends and adoption drivers. It also examines the role of end-user industries such as transportation & logistics, construction, oil & gas, government fleets, and utilities, offering insight into vertical-specific challenges and technology uptake.

Emerging areas such as AI-powered video telematics, blockchain for fleet compliance, and digital twins for vehicle modeling are also explored. Additionally, the report evaluates the impact of technological convergence (5G, cloud computing, IoT) and examines the competitive positioning of key market players, helping decision-makers understand innovation pipelines, expansion strategies, and market entry opportunities across mature and emerging regions.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 9,030 Million |

| Market Revenue (2032) | USD 21,111.8 Million |

| CAGR (2025–2032) | 11.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Technology Insights, Segment & Fleet‑Type Analysis, Regional & Country Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Geotab Inc., Trimble Inc., Verizon Connect, Omnitracs, LLC, AT&T Inc., TomTom Telematics, Zonar Systems, Inc., MiX Telematics, Samsara Inc., Orbcomm Inc., Teletrac Navman, Fleet Complete, Gurtam, KeepTruckin Inc., Inseego Corp. |

| Customization & Pricing | Available on request (10 % Customization is Free) |