Reports

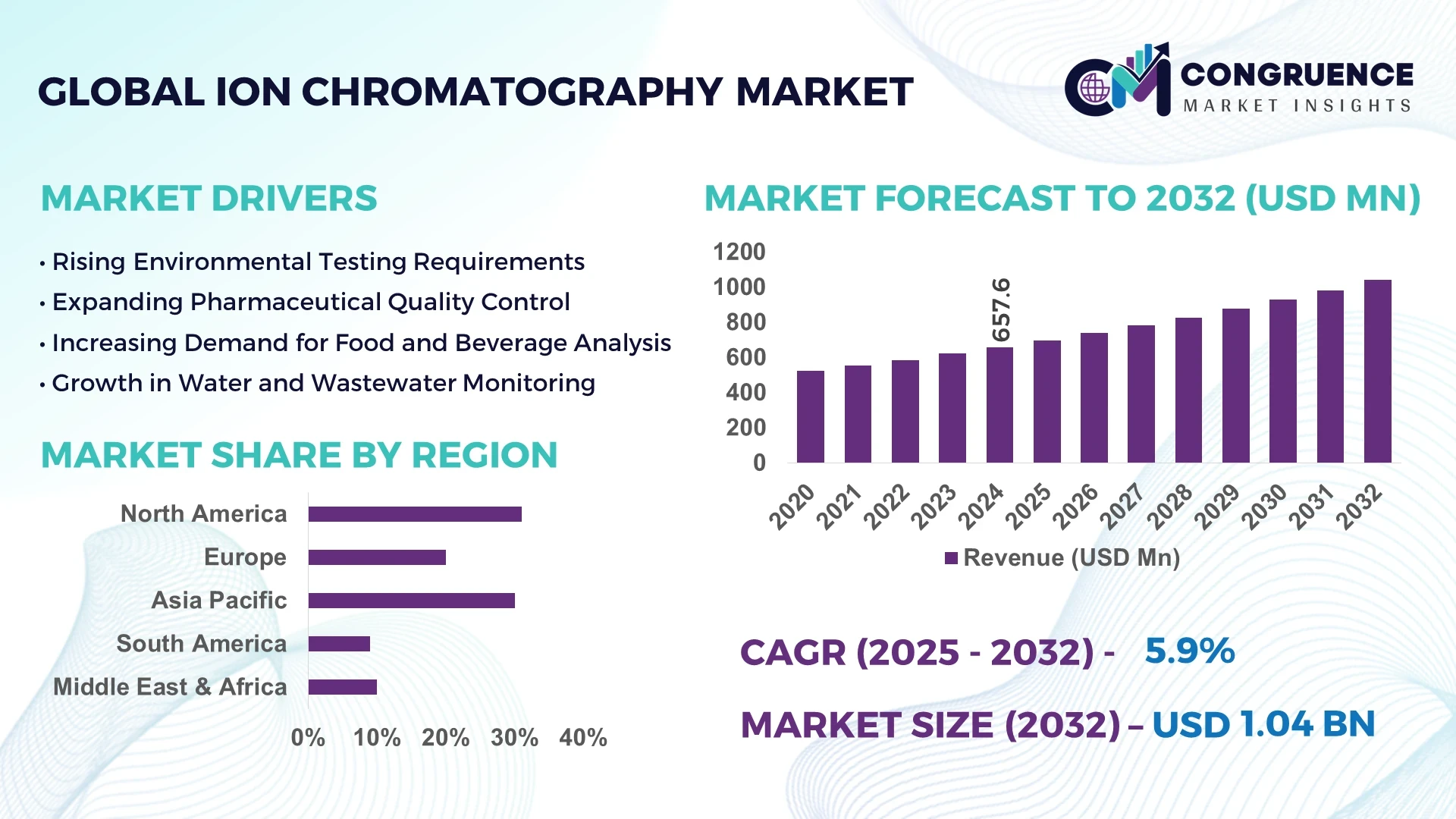

The Global Ion Chromatography Market was valued at USD 657.63 Million in 2024 and is anticipated to reach a value of USD 1,040.29 Million by 2032, expanding at a CAGR of 5.9% between 2025 and 2032. This growth is attributed to the increasing demand for precise analytical techniques across various industries, including pharmaceuticals, environmental testing, and food safety.

The United States leads the global market, driven by substantial investments in research and development, a robust regulatory framework, and a high adoption rate of advanced analytical technologies. In 2024, the U.S. accounted for over 45% of the global ion chromatography market, reflecting its dominant position in the industry.

Market Size & Growth: Valued at USD 657.63 million in 2024, projected to reach USD 1,040.29 million by 2032, with a CAGR of 5.9%. Growth is driven by rising demand for accurate analytical methods across various industries.

Top Growth Drivers: Increased adoption in pharmaceutical applications (45%), environmental testing (30%), and food safety analysis (25%).

Short-Term Forecast: By 2028, a 15% reduction in analysis time is expected due to advancements in automation and system integration.

Emerging Technologies: Integration of ion chromatography with mass spectrometry (IC-MS) and development of miniaturized, portable ion chromatography systems.

Regional Leaders: North America (USD 450 million by 2032), Europe (USD 350 million by 2032), Asia-Pacific (USD 240 million by 2032), with North America leading in pharmaceutical applications.

Consumer/End-User Trends: Pharmaceutical companies increasingly adopting ion chromatography for Active Pharmaceutical Ingredient (API) analysis; environmental agencies focusing on water quality monitoring.

Pilot or Case Example: A pharmaceutical company in the U.S. implemented an ion chromatography system in 2023, resulting in a 20% increase in throughput and a 10% reduction in operational costs.

Competitive Landscape: Thermo Fisher Scientific (market leader with 25% share), followed by Metrohm, Shimadzu, Tosoh Bioscience, and Bio-Rad Laboratories.

Regulatory & ESG Impact: Stringent regulations in North America and Europe mandating the use of ion chromatography for environmental and pharmaceutical testing; increasing emphasis on environmental sustainability.

Investment & Funding Patterns: Over USD 500 million invested in ion chromatography technologies in 2024, with a focus on automation and integration capabilities.

Innovation & Future Outlook: Development of hybrid systems combining ion chromatography with other analytical techniques, and expansion into emerging markets in Asia-Pacific.

The ion chromatography market is experiencing significant growth, driven by technological advancements and increasing demand across various industries. The integration of ion chromatography with other analytical techniques, such as mass spectrometry, is enhancing the capabilities of these systems, enabling more precise and efficient analyses. Additionally, the focus on automation and miniaturization is making ion chromatography more accessible and cost-effective for a broader range of applications. As regulatory requirements become more stringent, the adoption of ion chromatography is expected to rise, particularly in environmental testing and pharmaceutical sectors. Emerging markets in Asia-Pacific are also contributing to the market's expansion, offering new opportunities for growth and innovation.

The strategic relevance of the Ion Chromatography Market lies in its critical role across pharmaceutical, environmental, and food safety sectors. Automation-enabled ion chromatography delivers 15% faster analysis compared to conventional manual systems, enhancing laboratory throughput and accuracy. North America dominates in volume, while Europe leads in adoption with 60% of enterprises implementing advanced IC technologies. By 2027, AI-assisted chromatographic data interpretation is expected to improve analytical precision by 20%, reducing error rates and accelerating decision-making. Firms are committing to ESG improvements such as 25% reduction in chemical waste and enhanced recycling of solvents by 2030. In 2024, a leading U.S.-based pharmaceutical company achieved a 12% reduction in operational downtime through the integration of automated IC-MS systems. Forward-looking strategies indicate that the Ion Chromatography Market will continue to serve as a pillar of resilience, regulatory compliance, and sustainable growth, supporting innovation while meeting increasingly stringent quality and environmental standards. Its adoption trajectory underscores the market’s potential for long-term stability, technological advancement, and global relevance in analytical applications.

Automation and system integration are driving the Ion Chromatography Market by reducing human error, improving repeatability, and increasing throughput. Automated eluent generation, sample injection, and data processing streamline workflows, enabling laboratories to perform high-volume analyses with greater accuracy. Pharmaceutical companies implementing automated IC systems have reported a 20% improvement in testing efficiency and a 15% reduction in reagent waste. Environmental agencies using integrated IC solutions for water and soil testing have achieved faster detection times and improved compliance with regulatory standards. The scalability and adaptability of automated IC systems allow enterprises to optimize operations and invest in innovation, fostering growth across diverse industries.

High upfront costs of ion chromatography instruments limit adoption, particularly for small and mid-sized laboratories. Advanced IC systems, which include automation and integration with mass spectrometry, require substantial capital expenditure, often exceeding USD 150,000 per setup. Additionally, ongoing maintenance, training for skilled operators, and software updates contribute to the total cost of ownership. In emerging markets, budget constraints restrict access to these technologies, slowing adoption rates despite clear operational advantages. These financial barriers challenge the broader implementation of IC systems, as laboratories must balance performance improvements with investment limitations, creating a restraint on market expansion.

The integration of ion chromatography with mass spectrometry (IC-MS) opens significant opportunities by enabling simultaneous separation and identification of ions in complex matrices. This integration allows for higher sensitivity, lower detection limits, and comprehensive profiling of environmental, pharmaceutical, and food samples. Adoption of IC-MS has led to measurable improvements, such as a 25% increase in detection accuracy for trace ions in water quality monitoring. Emerging markets, particularly in Asia-Pacific, present untapped potential for IC-MS solutions, driven by regulatory emphasis on analytical precision. The opportunity lies in leveraging hybrid technologies to meet industry demands, expand applications, and enhance analytical reliability.

The Ion Chromatography Market faces competition from alternative analytical techniques, including high-performance liquid chromatography (HPLC), capillary electrophoresis, and ion-selective electrodes. These methods are often more familiar to laboratories and can be cost-effective, reducing the perceived need for IC systems. HPLC, for instance, offers similar separation capabilities in certain pharmaceutical and food applications. Additionally, regulatory acceptance of alternative techniques in some regions allows laboratories to choose less expensive solutions. Overcoming this challenge requires IC systems to demonstrate superior performance, enhanced accuracy, and compliance with stringent environmental and safety standards, ensuring continued adoption despite competitive pressures.

Increased Adoption of Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Ion Chromatography market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Ion Chromatography with Mass Spectrometry: The integration of ion chromatography with mass spectrometry (IC-MS) is gaining momentum, enhancing analytical capabilities. This combination allows for simultaneous separation and identification of ions in complex matrices, improving sensitivity and detection limits. The pharmaceutical and environmental sectors are leading adopters, aiming for more precise and comprehensive analyses.

Shift Towards Automation and AI in Analytical Processes: Automation and artificial intelligence (AI) are transforming analytical laboratories by streamlining workflows and reducing human error. Automated ion chromatography systems equipped with AI algorithms can process large volumes of samples with high accuracy, leading to increased throughput and efficiency. This trend is particularly evident in high-throughput environments such as pharmaceutical quality control and environmental monitoring.

Rising Demand for Sustainable and Green Analytical Solutions: There is a growing emphasis on sustainability within the Ion Chromatography market, driven by environmental regulations and corporate social responsibility initiatives. Laboratories are seeking green analytical solutions that minimize chemical waste and energy consumption. The development of eco-friendly elution systems and recyclable materials for chromatographic columns are examples of innovations addressing these sustainability concerns.

The Ion Chromatography market is segmented based on type, application, and end-user. By type, ion-exchange chromatography dominates due to its widespread use in separating anions and cations. In terms of application, environmental testing leads, driven by stringent regulations on water and air quality. The pharmaceutical industry is a significant end-user, utilizing ion chromatography for drug analysis and quality control. Emerging regions in Asia-Pacific are increasingly adopting IC systems, while North America and Europe maintain high adoption levels due to established infrastructure and regulatory frameworks.

Ion-exchange chromatography is the leading type, accounting for approximately 66.2% of the market share. This dominance is attributed to its efficiency in separating ions and its versatility across various applications. The fastest-growing segment is ion-exclusion chromatography, driven by increasing adoption in food and beverage analysis, particularly for organic acid determination. Other types, including ion-pair chromatography and non-suppressed ion chromatography, collectively hold a combined share of 33.8%, serving niche applications in specialized industries.

Environmental testing is the leading application, comprising 40% of the market. This sector's growth is fueled by escalating concerns over pollution and the need for stringent environmental regulations. The pharmaceutical industry follows closely, accounting for 35% of the market, driven by the necessity for rigorous drug testing and quality assurance. Food and beverage analysis holds a 15% share, with increasing demand for safety and quality control measures. Water analysis applications contribute to the remaining 10%, reflecting the critical importance of water quality monitoring. In 2024, more than 38% of enterprises globally reported piloting Ion Chromatography systems for environmental compliance monitoring.

The pharmaceutical industry is the leading end-user, utilizing ion chromatography for drug development and quality control processes, accounting for 42% of adoption. Environmental laboratories are the fastest-growing end-user segment, driven by regulatory demands and rising environmental concerns, with a projected growth rate of 9.2% through 2032. Academic and research institutions, healthcare facilities, and food and beverage companies collectively account for the remaining market share, each contributing to the demand for precise analytical techniques. In 2024, over 38% of laboratories globally reported piloting IC systems for research applications.

North America accounted for the largest market share at 31.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.9% between 2025 and 2032.

North America leads due to stringent environmental regulations, robust pharmaceutical R&D, and advanced analytical infrastructure. The U.S. EPA’s sub-ng/L PFAS limits are driving upgrades in instrumentation, while Canada’s biosimilar programs sustain demand for impurity testing. Mexico’s expanding industrial sector, supported by recent vendor expansions, adds growth potential. Skilled workforce availability supports high analytical throughput, despite higher labor costs. Asia-Pacific growth is propelled by China, India, and Japan, with government investments, regulatory compliance, and expanding healthcare and industrial infrastructure. Europe maintains a strong presence with Germany, France, and the UK leading adoption, driven by EMA and EEA standards and sustainability initiatives. South America, led by Brazil and Mexico, benefits from government incentives, trade policies, and energy sector expansion. Middle East & Africa demand is fueled by UAE and South Africa investments, oil & gas industry needs, and modernization projects.

What Factors Are Propelling Growth in the Ion Chromatography Market in North America?

North America holds approximately 31.8% of the global ion chromatography market in 2024. The pharmaceutical and environmental testing sectors drive demand due to stringent regulations and quality standards. Technological advancements, including AI and automation in analytical systems, enhance efficiency and accuracy. Local players like Thermo Fisher Scientific are innovating with products such as the Dionex Inuvion Ion Chromatography system to streamline ion analysis. Enterprise adoption is higher in healthcare and finance sectors, reflecting the demand for precise and reliable analytical tools. Regulatory compliance and ongoing digital transformation also support market expansion.

How Are Regulatory Pressures Influencing the Ion Chromatography Market in Europe?

Europe accounted for a significant share of the ion chromatography market in 2024, with Germany, France, and the UK leading adoption. Regulatory bodies such as the European Medicines Agency and European Environment Agency enforce strict standards, driving demand for precise analytical solutions. Sustainability initiatives further fuel the adoption of advanced IC systems. Local players invest in R&D to meet regulatory requirements and innovate. Consumer behavior emphasizes the need for explainable and transparent analytical processes, shaped by regulatory pressures and environmental commitments.

What Are the Key Drivers of Growth in the Ion Chromatography Market in Asia-Pacific?

Asia-Pacific is projected to experience the fastest growth, driven by China, India, and Japan. Infrastructure developments, regulatory compliance, and rising healthcare and industrial demands fuel expansion. Adoption of advanced technologies and research capabilities supports the market, while local players develop cost-effective, efficient solutions. Consumer behavior is influenced by e-commerce, mobile applications, and the need for rapid and reliable analytical results. Regional innovation hubs and technology adoption enhance the market’s competitive landscape.

What Are the Emerging Trends in the Ion Chromatography Market in South America?

South America shows steady growth, with Brazil and Mexico as key markets. Government incentives and trade policies strengthen industrial capabilities, supporting market expansion. The energy sector and rising environmental awareness drive demand for IC systems. Local players focus on expanding operational capacities to meet regional needs. Consumer behavior is influenced by media and language localization, which shapes the demand for analytical solutions tailored to regional industries.

How Are Technological Modernization and Regulations Shaping the Ion Chromatography Market in the Middle East & Africa?

Middle East & Africa demonstrates varied demand, with UAE and South Africa investing in technological modernization. The oil & gas industry is a key driver, complemented by infrastructure projects. Local regulations and trade partnerships impact market dynamics, emphasizing adoption of advanced analytical techniques. Regional players are developing solutions catering to reliability and compliance requirements. Consumer behavior is shaped by economic conditions and the need for efficient, compliant analytical solutions.

United States: Market share of 31.8%; driven by stringent environmental regulations and robust pharmaceutical R&D.

Germany: Market share of 9.2%; strong industrial base and adherence to EU regulatory standards.

The global ion chromatography market is moderately fragmented, with a diverse array of active competitors ranging from established multinational corporations to specialized regional players. The top five companies—Thermo Fisher Scientific, Metrohm AG, Agilent Technologies, Shimadzu Corporation, and Waters Corporation—collectively hold a significant share of the market, though no single entity dominates. This competitive landscape fosters innovation and drives advancements in technology, as companies strive to differentiate themselves through product development, strategic partnerships, and geographic expansion.

Strategic initiatives are pivotal in shaping the market dynamics. For instance, Thermo Fisher Scientific's acquisition of Solventum's Purification & Filtration Business for USD 4.1 billion in 2025 underscores the trend of consolidation aimed at enhancing product portfolios and expanding market reach. Similarly, companies are investing in research and development to introduce advanced ion chromatography systems that offer improved sensitivity, automation, and integration with other analytical techniques.

Innovation trends are also influencing competition. The integration of ion chromatography with mass spectrometry (IC-MS) is gaining traction, providing enhanced detection capabilities for complex samples. Additionally, the development of miniaturized systems and automated eluent generation technologies is streamlining workflows and reducing operational costs, further intensifying the competitive environment.

Shimadzu Corporation

Waters Corporation

Bio-Rad Laboratories Inc.

PerkinElmer Inc.

Danaher Corporation (Cytiva)

Mitsubishi Chemical Corporation

Ion chromatography (IC) is experiencing significant technological advancements that are enhancing analytical capabilities and operational efficiency. One notable development is the integration of hybrid multi-detector configurations in IC systems. Since 2023, approximately 48% of new systems launched support such configurations, combining detectors like UV-VIS, conductivity, and mass spectrometry. This integration improves compound identification accuracy by 27% and reduces analysis time by 38%, making it particularly beneficial for pharmaceutical and research laboratories.

Another emerging trend is the adoption of compact benchtop systems. These systems, now accounting for 41% of new installations, are favored by mid-sized laboratories and field testing units due to their space efficiency and ability to process over 90 samples daily. Their design under 60 cm in width allows for easy integration into various laboratory setups.

Automation is also playing a crucial role in modern IC systems. Since 2023, 62% of new systems launched feature automated eluent generation, which minimizes reagent consumption by 31% and reduces operator intervention by 45%. This automation not only enhances operational efficiency but also ensures consistent and reproducible results.

Furthermore, the incorporation of cloud-based monitoring features is gaining traction. Approximately 29% of ion chromatography systems now support real-time data upload and remote diagnostics, facilitating centralized monitoring and maintenance across multiple sites. These advancements are driving the evolution of ion chromatography, making it more efficient, user-friendly, and adaptable to diverse analytical needs.

In October 2023, a study highlighted the use of ion chromatography for measuring organic acids and organic anions with precision. This advancement is crucial for applications in environmental monitoring and pharmaceutical analysis, ensuring accurate and reliable results in complex sample matrices. Source: www.chromatographytoday.com

In November 2024, a new method for isolating plutonium isotopes from environmental samples using ion chromatography was reported. This technique enhances the sensitivity and efficiency of radiochemical analysis, supporting environmental safety and regulatory compliance efforts. Source: arxiv.org

In May 2024, a proposal for laser resonance chromatography of $^{229}$Th$^{3+}$ ions was presented. This method aims to detect specific electronic states of thorium ions, potentially advancing applications in nuclear physics and quantum computing research.

The Ion Chromatography Market Report provides a comprehensive analysis of the global ion chromatography landscape, encompassing various market segments, geographic regions, applications, technologies, and industry focus areas. The report delves into the different types of ion chromatography systems, including ion-exchange, ion-exclusion, and ion-pair chromatography, highlighting their respective market shares and growth trends. Geographically, the report examines key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional market dynamics, demand drivers, and technological advancements. It also explores the adoption of ion chromatography across various applications, including environmental testing, pharmaceuticals, food and beverage analysis, and chemical industries.

Technologically, the report discusses emerging trends such as the integration of multi-detector systems, automation in eluent generation, and the adoption of cloud-based monitoring features. These technological innovations are shaping the future of ion chromatography, enhancing analytical capabilities, and improving operational efficiency. Furthermore, the report addresses industry-specific focus areas, providing valuable information for business decision-makers and industry professionals seeking to understand the current state and future prospects of the ion chromatography market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 657.63 Million |

|

Market Revenue in 2032 |

USD 1040.29 Million |

|

CAGR (2025 - 2032) |

5.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific Inc., Agilent Technologies Inc., Metrohm AG, Shimadzu Corporation, Waters Corporation, Bio-Rad Laboratories Inc., PerkinElmer Inc., Danaher Corporation (Cytiva), Mitsubishi Chemical Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |