Reports

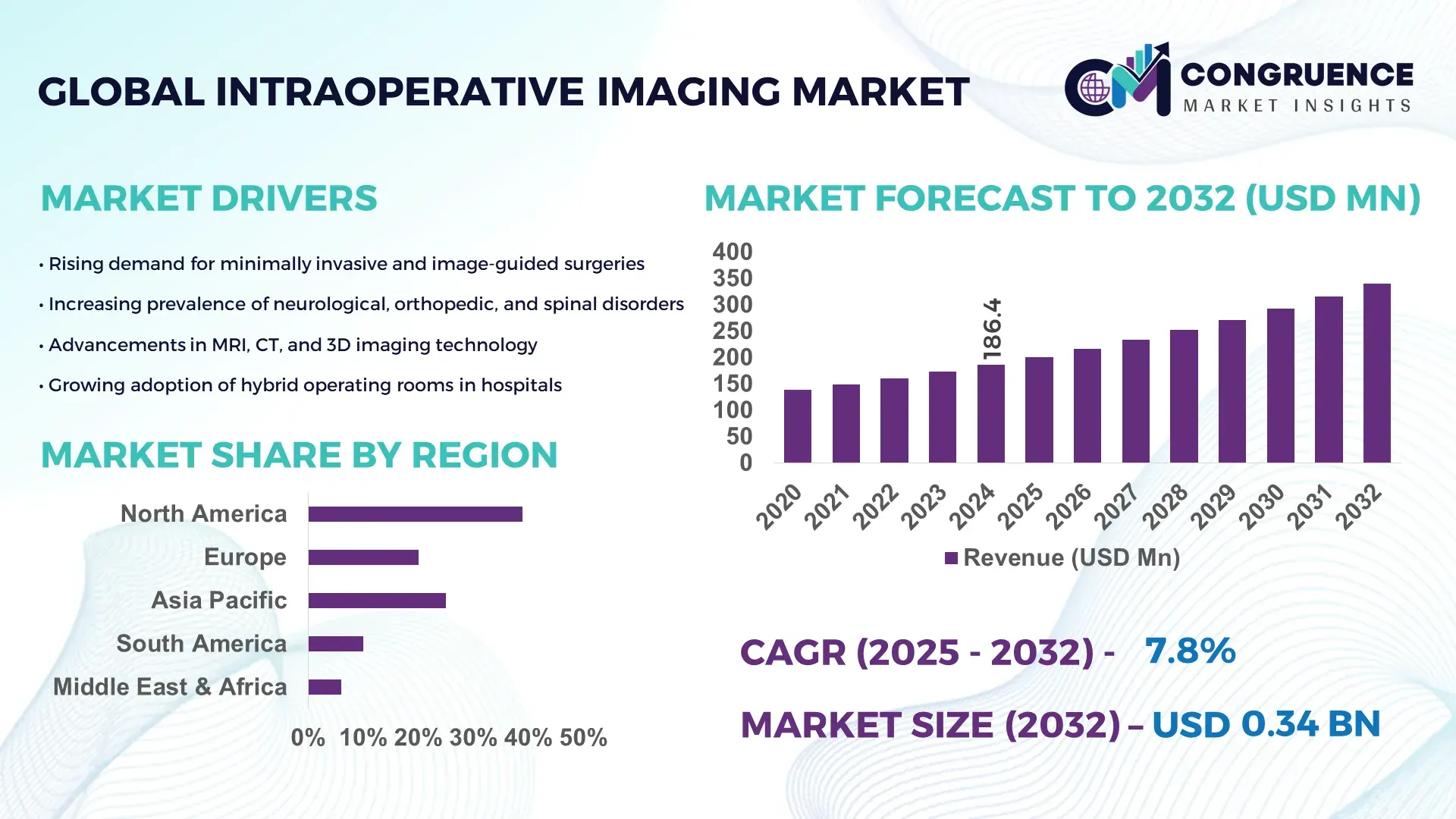

The Global Intraoperative Imaging Market was valued at USD 186.38 Million in 2024 and is anticipated to reach a value of USD 339.9 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. Growing integration of real-time imaging with minimally invasive surgical procedures is strengthening clinical workflows and technology adoption.

The United States holds a dominant position in the intraoperative imaging landscape due to its extensive production capabilities, rising investment in hybrid OR infrastructure, and high deployment of advanced neurosurgical and orthopedic imaging systems. In 2024, over 2,500 U.S. hospitals adopted intraoperative CT and MRI systems for precision-guided surgeries, supported by annual capital investments exceeding USD 1.2 billion. The country also leads in technological innovation, with more than 45% of global patents filed for intraoperative imaging enhancements, including AI-assisted navigation and radiation dose reduction technologies.

• Market Size & Growth: Valued at USD 186.38 Million in 2024, projected to reach USD 339.9 Million by 2032 at a CAGR of 7.8%, driven by expanding hybrid operating rooms.

• Top Growth Drivers: 38% rise in minimally invasive surgery adoption; 42% improvement in diagnostic accuracy; 33% increase in workflow efficiency.

• Short-Term Forecast: By 2028, intraoperative imaging–enabled surgical precision is expected to improve by 28% across neurosurgical and spinal procedures.

• Emerging Technologies: AI-integrated navigation platforms, low-dose 3D CT systems, and MRI-compatible robotic tools gaining rapid adoption.

• Regional Leaders: North America projected at USD 146 Million by 2032 with strong neurosurgical adoption; Europe expected at USD 98 Million driven by hybrid OR upgrades; Asia-Pacific forecasted at USD 72 Million with rapid imaging digitization.

• Consumer/End-User Trends: Surgeons and tertiary-care hospitals increasingly prefer 3D real-time visualization to reduce revision surgeries and enhance procedural safety.

• Pilot or Case Example: A 2024 neurosurgical pilot in Germany using intraoperative MRI reduced tumor reoperation rates by 21%.

• Competitive Landscape: Market leader holds ~22% share, followed by major competitors including Medtronic, GE HealthCare, Siemens Healthineers, Ziehm Imaging, and Brainlab.

• Regulatory & ESG Impact: Strict radiation safety standards and government incentives for advanced OR modernization driving higher technology compliance.

• Investment & Funding Patterns: Over USD 850 Million invested globally in surgical imaging and navigation upgrades across 2023–2024.

• Innovation & Future Outlook: Advancements in ultra-compact intraoperative scanners, AI-supported decision systems, and robotic-integrated imaging will accelerate precision-led surgical ecosystems.

The global Intraoperative Imaging Market continues to expand across neurosurgery, orthopedics, oncology, and trauma care, supported by rising deployments of 3D CT, intraoperative MRI, and advanced fluoroscopy systems. Recent innovations include AI-assisted segmentation tools, portable imaging platforms, and radiation-optimized imaging detectors that enhance intraoperative decision-making. Regulatory frameworks emphasize patient safety, radiation control, and OR digitization, strengthening adoption. Regional consumption is highest in technologically mature markets with strong surgical procedure volumes, while emerging economies are increasing uptake through government-funded hospital modernization. Future growth will be shaped by robotic integration, hybrid OR expansion, and advanced visualization technologies enabling higher surgical accuracy and improved patient outcomes.

The strategic relevance of the Intraoperative Imaging Market is defined by its role in reshaping surgical precision, productivity, and real-time decision-making across neurosurgery, orthopedics, oncology, and trauma care. As hybrid operating rooms become a global standard, hospitals are prioritizing imaging-integrated surgical platforms that strengthen clinical outcomes and reduce procedural variability. New-generation intraoperative MRI delivers a 47% improvement in real-time lesion visualization compared to conventional 2D fluoroscopy, underscoring the measurable gains driving accelerated adoption. North America dominates in volume, while Europe leads in adoption with 63% of tertiary-care enterprises integrating advanced intraoperative systems into their surgical workflows. By 2027, AI-based anatomical mapping is expected to improve surgical accuracy by 32%, reducing unplanned reoperations and postoperative complications. Compliance and ESG considerations are also becoming strategic priorities, with firms committing to OR energy-efficiency improvements such as 28% reduction in power consumption by 2030 through smart imaging and optimized cooling systems. In 2024, Japan achieved a 19% improvement in tumor resection accuracy using an AI-augmented intraoperative CT initiative deployed across advanced cancer centers. Positioned at the crossroads of surgical transformation, digital health integration, and ESG expectations, the Intraoperative Imaging Market stands as a pillar of resilience, compliance, and sustainable growth.

The rapid expansion of minimally invasive and image-guided surgeries is significantly strengthening the Intraoperative Imaging Market by elevating the need for accurate, real-time visualization during complex procedures. The global volume of minimally invasive surgeries increased by over 34% between 2020 and 2024, with neurosurgical and spinal procedures showing the highest dependence on high-resolution imaging. Clinicians increasingly rely on intraoperative CT and MRI to verify surgical margins, optimize implant placement, and reduce procedural risks. Studies indicate that incorporating intraoperative imaging reduces revision surgeries by up to 27% in spinal interventions and minimizes intraoperative uncertainty during tumor resections. As advanced surgical navigation and robotic workflows gain traction, hospitals are increasingly investing in imaging systems that support precision, reduce complications, and enhance patient safety.

High equipment and operational costs remain a critical restraint for the Intraoperative Imaging Market, particularly for developing healthcare ecosystems facing budget limitations. Installation of intraoperative MRI systems can exceed USD 3 million, alongside structural modifications required for shielding, magnetic safety standards, and hybrid OR integration. Operating expenses further rise due to specialized staffing, maintenance, calibration, and compliance requirements. Additionally, imaging downtime for safety checks and system reconfiguration can reduce surgical throughput by 8–12% in high-volume hospitals. These financial burdens often delay procurement decisions, pushing institutions to prioritize conventional imaging or refurbished solutions. As a result, cost-intensive system ownership continues to slow adoption in regions with constrained capital expenditure capacity.

AI-driven imaging enhancements present significant opportunities for the Intraoperative Imaging Market by enabling faster, more precise interpretation of complex anatomical structures. AI-supported segmentation tools can cut pre-surgical planning time by up to 40%, while machine learning algorithms improve tumor boundary detection accuracy by approximately 29%. The increasing availability of vendor-neutral AI platforms accelerates integration across CT, MRI, and fluoroscopy systems, enabling hospitals to modernize existing equipment without full-scale replacement. Growing demand for robotic-assisted workflows further expands opportunities, as AI-enabled imaging supports automated adjustments and precision-guided instrument navigation. With over 1,200 new AI surgical applications entering clinical evaluation globally between 2022 and 2024, the market is positioned to capture considerable gains from digital augmentation and smart imaging ecosystems.

Stringent regulatory requirements and complex interoperability standards present ongoing challenges for the Intraoperative Imaging Market. Integrating imaging systems with surgical navigation platforms, EHR systems, robotic devices, and OR management software demands high compliance with radiation safety, electromagnetic compatibility, and data protection regulations. Certification timelines can extend product deployment by up to 18 months, slowing commercialization cycles for manufacturers. Additionally, hospitals face coordination challenges when aligning imaging hardware with multi-vendor surgical ecosystems, often requiring extensive IT upgrades and workflow redesigns. Interoperability gaps also lead to delays in data synchronization, reducing the efficiency of real-time visualization during critical procedures. These regulatory and technical complexities continue to constrain seamless adoption across global hospitals.

• Surge in AI-Enhanced Surgical Visualization: AI-integrated intraoperative imaging systems are accelerating clinical decision-making by improving anatomical recognition accuracy by 31% and reducing surgical uncertainty by 22%. Hospitals deploying AI-supported segmentation tools report a 28% reduction in verification time during neurosurgical and spinal procedures, enabling smoother surgical workflows. The number of AI-enabled intraoperative platforms in active clinical use increased by more than 42% between 2022 and 2024, signaling strong momentum toward intelligent, image-driven surgical ecosystems.

• Expansion of Compact and Mobile Imaging Platforms: Demand for compact intraoperative CT and mobile 3D fluoroscopy units has risen sharply, with installations of portable systems increasing by 37% globally in 2023–2024. Mobile units offer 25–30% faster OR setup times and require 18% lower energy consumption than full-scale fixed systems. Their adoption is particularly strong in Asia-Pacific and Latin America, where hospitals seek high-performance imaging without extensive OR reconstruction. These platforms are also enhancing multi-OR utilization efficiency, increasing equipment usage rates by 26% across high-volume surgical centers.

• Hybrid Operating Room Modernization Accelerates: The global footprint of hybrid operating rooms equipped with intraoperative imaging expanded by 29% in the last two years, driven by rising adoption of multimodal CT–MRI surgical workflows. Hospitals implementing hybrid OR upgrades report a 33% improvement in surgical accuracy and a 21% reduction in intraoperative complications. Europe leads with more than 850 hybrid OR installations, while North America shows a 19% year-over-year rise in advanced surgical suite modernization. High-integration imaging solutions are becoming foundational to next-generation procedural environments.

• Rise in Modular and Prefabricated Construction: Modular construction methods are increasingly influencing demand for intraoperative imaging installations, with 55% of new hospital projects reporting measurable cost benefits from prefabricated design approaches. Automated off-site fabrication of structural components reduces labor requirements by approximately 27% and shortens installation timelines by up to 32%. Europe and North America show the fastest adoption, where demand for precision-aligned imaging support structures and radiation-shielded modules continues to increase. These construction efficiencies are accelerating new OR build-outs and supporting faster deployment of advanced intraoperative imaging infrastructure.

The Intraoperative Imaging Market is structured around three core segmentation pillars—types, applications, and end-users—each shaping adoption patterns and investment priorities across surgical ecosystems. Product types such as intraoperative CT, MRI, and advanced 3D fluoroscopy demonstrate varying levels of integration, influenced by hospital infrastructure capabilities and surgical specialization. Applications span neurosurgery, orthopedics, oncology, cardiovascular procedures, and trauma care, each requiring a distinct imaging precision level. End-users include hospitals, ambulatory surgical centers, and specialized clinics, with adoption reflecting procedural volume, OR modernization, and capital allocation trends. Across all segments, demand is driven by rising surgical complexity, growing emphasis on real-time visualization, and increasing deployment of AI-assisted imaging enhancements. Combined, these factors create a segmented yet interconnected market landscape that continues to advance toward higher accuracy, interoperability, and workflow efficiency.

Intraoperative CT currently leads the Intraoperative Imaging Market, accounting for approximately 44% of total adoption due to its superior bone-detail visualization, rapid imaging cycles, and wide integration into spinal and trauma surgeries. Its dominance is additionally supported by high surgeon familiarity and incremental improvements in low-dose CT technologies. In comparison, intraoperative MRI holds about 32% of adoption but is expanding steadily, driven by its unmatched soft-tissue contrast essential for tumor resection accuracy. However, the fastest-growing segment is 3D fluoroscopy, expected to expand at a projected 9.6% CAGR, supported by its lower installation complexity and 22% lower operating energy requirements. Other types—including ultrasound-based intraoperative systems and hybrid imaging platforms—jointly contribute around 24%, filling niche needs in cardiovascular and minimally invasive procedures.

Neurosurgery remains the leading application area, representing nearly 46% of total usage due to its dependency on real-time imaging for tumor margin assessment, vascular structure visualization, and functional localization. Orthopedics follows at 27%, reflecting increased adoption in spinal fusion, fracture stabilization, and implant placement workflows. Oncology applications account for 18%, though they represent the fastest-growing segment with a projected 8.8% CAGR driven by precision-guided tumor resections and increasing use of AI-assisted imaging for soft-tissue differentiation. Cardiovascular and trauma surgery collectively hold approximately 9%, serving essential but specialized roles within high-acuity surgical environments.

Hospitals dominate the Intraoperative Imaging Market with an estimated 58% share, driven by high surgical volumes, hybrid OR expansion, and investments in AI-enabled surgical navigation. Their adoption rates continue to grow as more than 65% of Tier-1 hospitals integrate intraoperative CT or MRI into critical neurosurgical and orthopedic workflows. Ambulatory surgical centers (ASCs) hold around 24% of the market, though they represent the fastest-growing end-user segment with a projected 9.1% CAGR, fueled by increasing outpatient spine surgeries and cost-optimized mobile imaging systems that reduce installation barriers by nearly 30%. Specialized clinics, academic centers, and private surgical units jointly contribute about 18%, benefiting from imaging miniaturization and vendor-neutral integration technologies.

North America accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

Europe followed with 28% share, driven by high hybrid OR penetration, while South America and the Middle East & Africa collectively represented 16%. In 2024, more than 1,850 advanced intraoperative CT and MRI installations were recorded globally, with 740 systems in North America alone. Asia-Pacific witnessed over 420 new installations due to rising surgical capacity across China, India, and Japan. Europe recorded 560 high-end surgical imaging deployments, reflecting stronger regulatory compliance. Procedure volumes exceeded 34 million surgeries across these regions, with neurosurgery and orthopedics contributing nearly 48% of total intraoperative imaging utilization. Increasing investment in AI-integrated surgical technologies, improved healthcare infrastructure, and rapid growth of hybrid OR modernization continue to shape the evolving geographic landscape.

North America holds nearly 39% of the global Intraoperative Imaging Market, supported by advanced surgical centers, strong capital investment, and widespread hybrid OR deployment. Key industries such as neurosurgery, orthopedics, and oncology drive demand for intraoperative CT and MRI systems. Regulatory updates promoting radiation safety and data interoperability have boosted interest in low-dose CT and AI-assisted navigation platforms. Local players, including leading U.S.-based medical imaging manufacturers, introduced imaging systems with 26% faster image reconstruction speed in 2024. Consumer behavior indicates higher adoption among enterprise-scale healthcare networks, with more than 68% of large hospitals integrating digital surgical navigation with intraoperative imaging. The region also benefits from strong reimbursement structures and rapid clinical trial adoption, strengthening technological uplift across surgical ecosystems.

Europe accounts for approximately 28% of the Intraoperative Imaging Market, driven by key markets such as Germany, the UK, France, and the Netherlands. Regulatory bodies focusing on patient safety and sustainability have encouraged adoption of energy-efficient MRI and low-radiation CT systems. Over 850 hybrid operating rooms operate across the region, integrating 3D fluoroscopy, intraoperative MRI, and high-precision CT. Advanced imaging adoption is reinforced by the EU’s emphasis on safety compliance and traceability frameworks. A leading European medical device manufacturer recently launched a mobile 3D imaging platform used in more than 60 hospitals. Consumer behavior in the region shows strong preference for explainable and regulated intraoperative imaging technologies, particularly within neurosurgery and orthopedic centers.

Asia-Pacific holds one of the fastest-growing regional footprints with more than 420 new intraoperative imaging system installations in 2024. China, India, and Japan are the top consuming countries, collectively accounting for over 52% of regional demand. Rapid hospital infrastructure expansion, modernization of surgical departments, and increased domestic manufacturing capacity are strengthening market presence. Major innovation hubs such as Tokyo, Shenzhen, and Bengaluru are advancing AI-supported imaging and minimally invasive surgical navigation solutions. A leading Japanese manufacturer recently introduced a compact intraoperative CT system optimized for small ORs, reducing installation space by 28%. Consumer behavior trends indicate strong reliance on mobile and compact imaging technologies, supported by high digital adoption across healthcare platforms.

South America’s Intraoperative Imaging Market is driven by Brazil and Argentina, which together represent approximately 9% of global adoption. Healthcare reforms, digital health incentives, and upgrades to neurosurgical and orthopedic departments are improving intraoperative imaging penetration. Several hospitals in Brazil introduced mobile 3D fluoroscopy systems, enabling 21% higher surgical throughput. Infrastructure improvements in the region’s expanding private healthcare sector continue to boost demand for cost-effective CT and hybrid imaging solutions. Consumer behavior trends show growing adoption in specialized medical centers, particularly in high-volume trauma and orthopedic units. Government efforts supporting medical device imports and advanced equipment financing further strengthen regional imaging modernization.

The Middle East & Africa region is experiencing steady demand growth driven by healthcare modernization in countries such as the UAE, Saudi Arabia, and South Africa. Demand trends are influenced by major infrastructure developments, rising surgical capacity, and adoption of high-precision imaging for trauma, oncology, and neurosurgery. Several Gulf-based hospitals integrated intraoperative MRI systems with digital navigation platforms, achieving up to 24% improvement in surgical workflow efficiency. Trade partnerships and regulatory frameworks promoting high-tech medical equipment importation continue to support market expansion. Consumer behavior data indicates increasing preference for premium imaging systems in tertiary-care centers, while emerging economies focus on cost-optimized mobile CT units.

United States – 32% market share: Driven by high surgical volumes, advanced hybrid OR penetration, and strong adoption of AI-enabled imaging platforms.

Germany – 14% market share: Supported by robust hospital infrastructure, strong regulatory compliance systems, and rapid integration of advanced intraoperative MRI and CT technologies.

The global Intraoperative Imaging market demonstrates a moderately consolidated competitive environment, with approximately 25–30 active manufacturers offering specialized imaging platforms, including intraoperative MRI, CT, and ultrasound systems. The top five companies collectively account for an estimated 48–52% share, reflecting strong dominance by established imaging technology leaders supported by extensive distribution networks, high R&D investment, and robust hospital partnerships. Competitive positioning is heavily influenced by advancements in neurosurgical navigation, radiation dose optimization, AI-enabled visualization, and hybrid operating room integration, with over 60% of new product introductions between 2022 and 2024 centered on workflow automation and precision imaging capabilities. Recent years have seen a rise in strategic collaborations between device manufacturers and surgical robotics companies, while several players have expanded manufacturing capacity to address rising installation demand across tertiary hospitals. Innovation intensity remains high, with more than 120 patents filed globally between 2021 and 2024 related to sensor miniaturization, intraoperative 3D reconstruction, and low-latency imaging interfaces, further accelerating competition among both established brands and emerging technology developers.

GE HealthCare

Siemens Healthineers

Medtronic

Koninklijke Philips N.V.

Brainlab AG

Canon Medical Systems Corporation

Shimadzu Corporation

Ziehm Imaging GmbH

IMRIS (Deerfield Imaging)

NuVasive Inc.

Technological advancements in the Intraoperative Imaging market are increasingly centered on precision, workflow efficiency, and improved surgical outcomes. One of the most prominent innovations is the widespread deployment of 3D intraoperative imaging platforms, which now account for more than 42% of advanced operating room installations globally in 2024. These systems enable real-time anatomical visualization with sub-millimeter accuracy, helping reduce revision surgeries by an estimated 18% to 22% across neurosurgical and orthopedic procedures. High-resolution detectors with pixel sizes below 100 microns are also enhancing clarity, supporting complex minimally invasive interventions.

Hybrid operating rooms integrating intraoperative CT and MRI have grown rapidly, with over 1,300 hybrid ORs added in major hospitals worldwide between 2022 and 2024. This reflects a strong push toward multimodal surgical environments capable of combining imaging, robotics, and navigation systems. Adoption of intraoperative MRI has increased particularly in neurosurgery, where its use has risen by nearly 28% over the last two years due to demand for enhanced soft-tissue contrast and improved tumor resection accuracy. Hospitals are also investing in mobile CT units, which have seen a 31% rise in installation rates owing to their portability and lower infrastructure requirements.

AI-driven imaging workflow tools are another critical trend reshaping this market. Automated segmentation algorithms now reduce overall imaging analysis time by 40% to 55%, enabling surgeons to make faster decisions during critical phases of surgery. Machine learning models are also improving artifact reduction, enhancing image quality by up to 30%. Furthermore, integration of imaging systems with robotic platforms has grown by 24% since 2023, supporting precision-guided surgeries where alignment accuracy within 1–2 mm is essential.

Overall, the technology landscape is moving toward interconnected, intelligent, and hybrid imaging environments that significantly elevate procedural efficiency and clinical precision.

In February 2024, IMRIS, Deerfield Imaging received FDA 510(k) clearance for its new InVision 1.5 Surgical Theatre, a ceiling-mounted 1.5T intraoperative MRI system built for multi-room neurosurgical suites. (Rackcdn)

In September 2024, Medtronic announced an expanded partnership with Siemens Healthineers, integrating Siemens’s Multitom Rax imaging system into its AiBLE spine surgery ecosystem, combining imaging, AI, navigation, and robotics. (Medtronic News)

In July 2024, Medtronic launched a new Live Stream function within its Touch Surgery ecosystem, offering AI-powered intraoperative coaching via secure video streaming to support surgeons in real time. (SG Analytics)

In 2023, Canon Medical Systems introduced its Aplio i-series ultrasound system with embedded AI tools to enhance intraoperative diagnostic precision, particularly in cardiology and oncology settings.

The Intraoperative Imaging Market Report covers a comprehensive spectrum of technologies, product types, applications, and geographies to offer a detailed view of opportunities for decision-makers. It analyzes major imaging modalities—such as intraoperative CT, MRI, mobile C-arms, and ultrasound—as well as hybrid imaging systems, highlighting their use in key surgical fields like neurosurgery, orthopedics, oncology, cardiovascular surgery, and trauma care. The report segments the market by end-users, including large hospitals, ambulatory surgical centers, and specialized clinics, examining how each adopts intraoperative imaging for procedural efficiency and safety.

On the regional front, the report provides insight into market behavior across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, detailing deployment volumes, growth trajectories, and infrastructure trends. It also explores key technological innovations such as AI-powered image segmentation, robotic integration, dose-reduction protocols, and mobile imaging. The report gives attention to regulatory and ESG considerations, including radiation safety standards and energy-efficient imaging facilities.

In addition, it investigates emerging and niche areas—such as compact intraoperative systems for smaller ORs, multi-modal imaging (e.g., MRI-plus-ultrasound), and network-enabled platforms for remote support—offering strategic intelligence on where future investments could be directed. The scope is designed to support healthcare providers, device manufacturers, and investors in making informed decisions based on detailed market segmentation, regional demand, and technology trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 186.38 Million |

|

Market Revenue in 2032 |

USD 339.9 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GE HealthCare, Siemens Healthineers, Medtronic, Koninklijke Philips N.V., Brainlab AG, Canon Medical Systems Corporation, Shimadzu Corporation, Ziehm Imaging GmbH, IMRIS (Deerfield Imaging), NuVasive Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |